SOUTH KOREA: No FX Discussions Between Korean Minister & U.S. Trade Rep

South Korean Trade Minister Heong notes that FX matters didn’t come up in the meeting with his U.S. TR Greer.

- A reminder that the KRW has recently benefitted from a BBG report pointing to the two countries discussing FX policy earlier in May, with the prior meeting apparently generating an agreement to share a mutual understanding of principles when it comes to forex, as well as indicating “continued discussions on related policy”.

- USD/KRW initially trades up to 1,395 before moving back towards pre-headline levels, last 1,390.

- As noted above, the USD is still lower vs. all G10 peers on the day.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

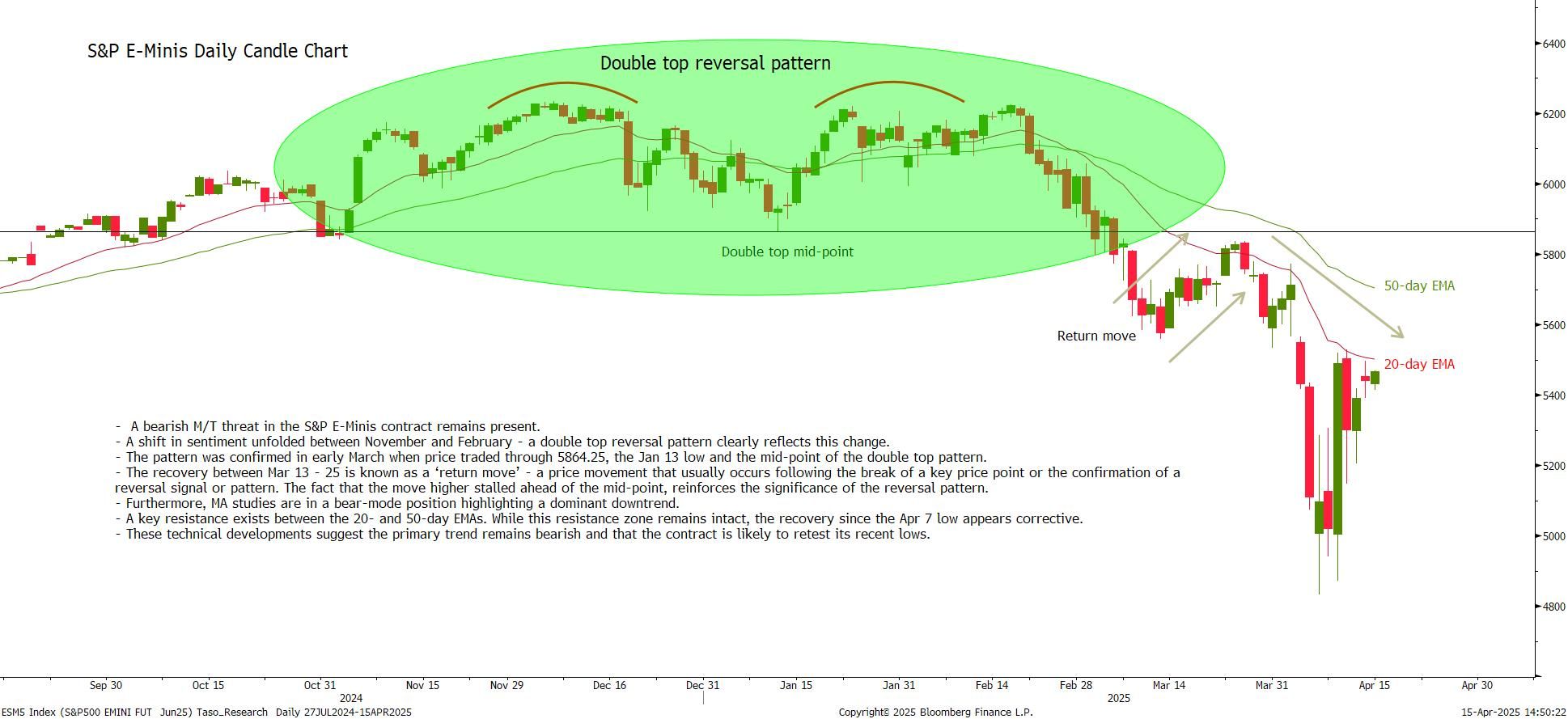

EQUITY TECHS: E-MINI S&P: (M5) Resistance Remains Intact

- RES 4: 5906.75 High Mar 6

- RES 3: 5837.25 High Mar 25 and the reversal trigger

- RES 2: 5701.85 50-day EMA

- RES 1: 5498.03 20-day EMA

- PRICE: 5357.25 @ 07:17 BST Apr 16

- SUP 1: 5098.16 61.8% retracement of the Apr 7 - 10 bounce

- SUP 2: 4832.00 Low Apr 7 and the bear trigger

- SUP 3: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

- SUP 4: 4663.75 1.764 proj of the Feb 19 - Mar 13 - 25 price swing

A reversal higher in S&P E-Minis last week highlights the start of a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind. Initial resistance to watch is 5498.03, the 20-day EMA. Resistance at the 50-day EMA is at 5701.85. On the downside, key support and the bear trigger has been defined at 4832.00, the Apr 7 low. A break of this level would resume the M/T downtrend.

SCANDIS: Morgan Stanley Pull Forward Final Riksbank Cut; Norges Forecast Unch

Taking into account the US reciprocal tariff announcement and related growth outlook revisions for the Eurozone, US and UK, Morgan Stanley now expect the Riksbank to cut rates by 25bp to a terminal of 1.75% in September, rather than March 2026. They continue to expect a 25bp rate cut in June to 2.00%.

- “We maintain our call for a rate cut to come in June. The growth momentum at the beginning of the year will likely be even weaker than expected (MSe: 0.1%Q, Riksbank: 0.5%Q). And despite the additional spending announced under the Spring budget, we do not think this will move the needle”.

- “The disinflation process should also be underway, supported by the stronger SEK and lower energy prices”.

- “With inflation declining towards the target, the likelihood of an inflation undershoot in 2026 rising, and the worsened growth outlook (weaker external demand, prolonged pick up in domestic demand), there is a clear case for faster cuts. We think the Riksbank will front-load its rate cutting cycle and deliver its final rate cut already in September 2025”.

Morgan Stanley’s Norges Bank rate forecast remains unchanged (Dec ’25 rate at 3.75%, Dec ’26 rate at 3.00%), but their conviction of the cutting cycle starting in June has strengthened.

- “Our journey to June is preconditioned on: i) wage growth coming in below Norges Bank's forecast (actual: 4.4%, NB: 4.5%), ii) continuation of disinflation process, mainly in domestic goods and services, iii) NOK remaining supportive for disinflation process”.

- “However, the weakening of NOK raises risks of stronger inflationary pressures (if permanent)”.

BUNDS: Tariffs drive the Risk Off Tone

- The German Bund saw a small gap higher on the open but didn't quite managed to break Yesterday's high at 131.57, after only managing a 131.35 Overnight.

- The German contract benefits from its Safer Haven status, but Desks have also positioned ahead of the ECB's expected cut on Growth Concerns, as Tariff Risks weigh on the Global Economies.

- The UK CPI was just a touch below Consensus and was only worth a 5 ticks gain in Bund, as Tariff news supersede, still Bund tested a session high post Cash Open.

- Trump is now restricting NVIDIA to sell its H20 chip to China, hence the Tech sector and wider Indices are under pressure going into the Europe session and will be watched on the EU Cash Open, NQM5 is down 2.0% vs 2.3% earlier.

- Trump has also launched a probe on the need for potential Tariffs on critical minerals.

- Today sees, EU, Italy final CPIs, US Retail Sales and IP, but the main Focus is on Fed Powell.

- SUPPLY: Germany 2025, 2030 (equates combined 20.3k Buxl) should weigh into the bidding deadline. There's a UK Tender but won't Impact Gilt.

- SYNDICATION: Italy dual Tranche.

- SPEAKERS: Fed Powell, Hammack.