KRW: USD/KRW Can't Break Late Sep Lows, Local Equities Up Despite US Losses

The recent downtrend in USD/KRW has paused somewhat, as US equity jitters and uncertainty on the US-South Korea trade deal temper won sentiment. We were last 1418/19, just up from end Thursday levels. Intra-session lows from Thursday were at 1414.45, close to late Sep levels. The 20-day EMA support point is near 1408.5, while on the topside recent highs were at 1435.35.

- US equity market weakness was concentrated in the finance space on Thursday amidst credit concerns. The SOX index rose 0.49%, while the MSCI IT index gained a more modest 0.15%. Local stocks remain strong with the Kospi rallying a further 1% to fresh record highs (last near 3800).

- This isn't imparting a firmer won trend at this stage but maybe helping curb the upside.

- South Korea officials are in the US for trade talks, via Yonhap/BBG: "South Korea has conveyed the government’s concerns about US demand for “upfront payment” on the $350b but persuading US President Donald Trump to accept the terms remains uncertain, Yonhap News says, citing Finance Minister Koo Yun-cheol speaking to reporters in Washington DC." This sounds a little less positive than recent Bessent comments, which hinted the trade deal would be wrapped up soon.

- On the data front earlier we had the unemployment tick down to 2.5% for Sep (versus 2.6% forecast). Jobs growth was +312ky/y, versus +166k prior. This, at the margin, helps the BoK on hold case next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Slightly Cheaper Ahead Of Today's 20Y Supply

In Tokyo morning trade, JGB futures are slightly weaker, -2 compared to settlement levels.

- Japan headline Aug trade figures were mixed. Exports were -0.1%y/y, against a -2.0% forecast (-2.6% was the July outcome). On the import side, we fell -5.2%y/y, against a -4.1% forecast and -7.4% prior outcome. The trade deficit was -242.5bn, against a -512.6bn forecast, while July's print was -118.4bn. In seasonally adjusted terms the trade deficit was -150.1bn, which was also better than forecast, but sub recent cycle highs for the balance (+166.5bn in Feb).

- Tariff impact was seen, with exports to the US down -13.8%y/y. To the EU exports rose 5.5%y/y, while to China exports were down a modest -0.5%y/y. The trade surplus Japan has with the US narrowed to 324bn. In Feb this year the surplus was at 918.5bn.

- Automobile exports fell 7.9% in August, the fifth consecutive decline following an 11.4% fall in July. Iron and steel exports dropped 14.9%, easing from July's 21.0% fall. Auto exports to the US fell by 28.4%.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest rally.

- Cash JGBs are flat to 2bps cheaper across benchmarks. The benchmark 20-year yield is 1.0bp higher at 1.611% ahead of today’s supply.

- Swap rates are ~1bp higher. Swap spreads are mixed.

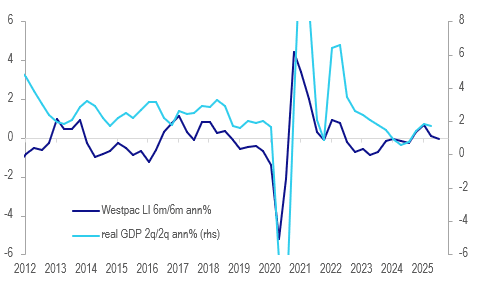

AUSTRALIA DATA: Westpac Lead Indicator Signals Slower Growth

Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

Australia growth outlook %

Source: MNI - Market News/LSEG

- Westpac is forecasting Australian GDP growth of 1.9% in 2025 up from 2024’s 1.3% with it returning to trend next year. Its Card Tracker suggests that private consumption slowed over Q3 to early September. It expects the RBA to be on hold in September but then ease 25bp in November and twice more in 2026.

- Westpac consumer unemployment expectations has been the largest contributor to the moderation in the lead index over the last half year. It rose 4.6% in September’s consumer sentiment survey to the highest in a year and just under the series average. Thus it and confidence (-3.1% m/m Sept) are likely to continue to weigh in the next lead index.

- Commodity prices in AUDs, Westpac consumer sentiment and dwelling approvals also contributed to the moderation. Hours worked, the yield spread and US IP also made slight negative contributions with only Australian equities positive.

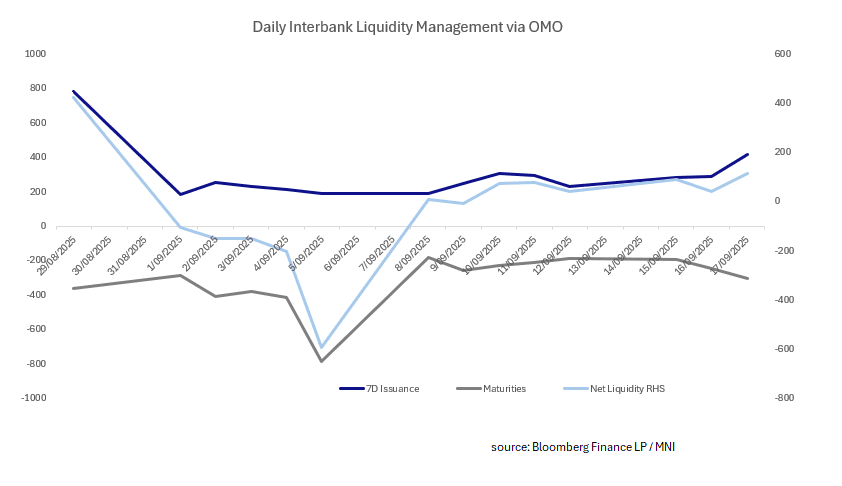

CHINA: Central Bank Injects CNY114.5bn via OMO

- The PBOC issued CNY418.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY304bn.

- Net liquidity injects CNY114.5bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.49%, from prior close of 1.49%.

- The China overnight interbank repo rate is at 1.51%, from the prior close of 1.46%.

- The China 7-day interbank repo rate is at 1.57%, from the prior close of 1.50%.