MNI US OPEN - QT Decision Key for September BoE Meeting

EXECUTIVE SUMMARY

- MNI FED REVIEW - NO RISK-FREE PATHS NOW

- MNI BOE PREVIEW - QT DECISION KEY

- NORGES BANK CUTS BUT RAISES RATE PATH

- LECORNU GOV'T ALREADY IN SHAKY POSITION AS FRANCE FACES MASS STRIKES

- NEW ZEALAND GDP CONTRACTS 0.9% Q/Q IN Q2

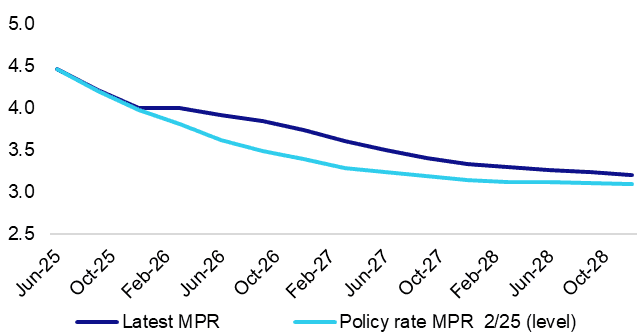

Figure 1: Norges Bank MPR forecast revised higher

Source: Norges Bank, MNI

MNI REPORTS

MNI FED REVIEW: No Risk-Free Paths Now

The Fed resumed its easing cycle with the first cut of the year on September 17, of 25bp to a range of 4.00-4.25%. That decision was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. Despite a lower rate path signalled in the new Dot Plot, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

MNI BOE PREVIEW: QT Decision Key

The outcome for this week’s MPC meeting can be boiled down to two discrete topics: the vote surrounding the pace of APF reduction and any updates on communications and the vote surrounding Bank Rate. The biggest uncertainty and market reaction is expected around the former, with much less focus being placed upon the latter – but neither aspect should be ignored. A 7-2 vote split is widely expected (by us and the analyst previews we have read) with both Dhingra and Taylor dissenting for a 25bp cut.

MNI BOJ PREVIEW: Maintain Cautious Stance on Hikes

The Bank of Japan is expected to keep policy unchanged in September, with future decisions hinging on October’s Tankan survey and branch managers’ meeting, which will clarify corporate sentiment and investment trends. External risks, particularly the impact of U.S. tariffs and potential weakness in U.S. labour markets, are now the central concern, limiting the urgency for near-term rate hikes despite inflation hovering near 3%.

MNI SARB PREVIEW: Target Reform Clouds Outlook

The SARB is expected to stand pat on interest rates this week, leaving the repo rate at 7.00% after a series of five sequential cuts interrupted by a brief pause in March. The inflation picture remains benign, as survey- and market-based measures confirm an ongoing moderation in inflation expectations, while a strong exchange rate weighs on import prices. However, current inflation is in a phase of cyclical upturn, which may encourage the MPC to hold as they remain under pressure to demonstrate credibility amid the ongoing inflation-target overhaul.

NEWS

US/CHINA (FT): China Drops Google Antitrust Probe During US Trade Talks

China is dropping an antitrust probe into Google, as Beijing and Washington step up negotiations over TikTok, Nvidia and trade at a time of heightened tensions between the superpowers. The State Administration for Market Regulation has decided to terminate its competition investigation against Google, a status known as “zhongzhi” in Chinese, said two people briefed on the decision. The Google investigation, which was formally opened in February, centred on the dominance of the US group’s Android operating system and its impact on Chinese phonemakers, such as Oppo and Xiaomi, that use the software.

US (BBG): Shutdown Risks Rise as Democrats Issue Ambitious Counteroffer

An increasingly rancorous standoff over funding the US government intensified Wednesday as congressional Democrats swung big on a counteroffer, ratcheting up the risk of an Oct. 1 shutdown. Democrats are demanding President Donald Trump and congressional Republicans agree to health care policy changes that House Speaker Mike Johnson has said have “zero” chance of becoming law as part of the spending bill.

NORGES BANK (MNI): Norges Bank Cuts But Raises Rate Path

Norges Bank cut its policy rate by 25 basis points to 4.0% but raised its rate path and tilted away from a further rate cut this year, it said on Thursday. The rate path showed the policy rate at 3.9% next year, 0.3 percentage point higher than in the previous quarterly forecast in June, and only declining to 3.3% by the end of the three-year forecast, 0.2 pp above the June prediction. "If the economy evolves broadly as currently projected, the policy rate will be reduced further in the course of the coming year," the Bank's Monetary Policy and Financial Stability Committee stated in its guidance.

ECB (MNI): Risk of Undershooting Not Big - ECB's De Guindos

The risk of the European Central Bank undershooting its 2% inflation target is “not big, not relevant for us,” Vice President Luis de Guindos told in an MNI Connect Event on Thursday, pointing to the last projections exercise that saw 2026 and 2027 inflation at 1.7% and 1.9%, respectively. However, he noted that the impacts of U.S. tariffs on the economy, activity and even inflation have yet to be seen, and that risks to inflation are balanced in both directions.

FRANCE (MNI): Lecornu Gov't Already in Shaky Position as France Faces Mass Strikes

The new gov't of PM Sebastien Lecornu finds itself in a vulnerable political position after just a week in office, with the centre-left Socialist Party (PS) and far-right Rassemblement National (National Rally, RN) warning Lecornu that the threat of a censure motion remains ever-present following meetings held on 17 Sep between the PM and opposition parties. Today (18 Sep), Lecornu, and indeed the entire Macron administration, face a major social challenge in the form of mass strikes taking place across the country. For the first time since June 2023, France's major trade unions have jointly called for a day of industrial action that is set to halt transport networks and close schools, pharmacies, and national monuments, with more than 800,000 union members expected to protest at 220+ rallies.

GERMANY (BBG): Germany Lifts Debt Sales for Defense, Infrastructure Boost

Germany will borrow about a fifth more than planned in the fourth quarter to help fund a surge in spending on infrastructure and the armed forces. The Frankfurt-based finance agency, which manages federal government debt, aims to raise €90.5 billion ($107 billion) in the October-December period, excluding green bonds, according to an updated plan published Thursday. That’s €15 billion more than December’s original program and follows an increase of €19 billion in the third quarter.

JAPAN (MNI): Takaichi Confirms Run for LDP Presidency, Sets Up 2-Horse Race w/Koizumi

Former Minister of State for Economic Security Sanae Takaichi has confirmed she will run for the presidency of the governing Liberal Democratic Party (LDP) following the announced resignation of PM Shigeru Ishiba. Takaichi's entry into the race was widely expected, and she is set to speak at a press conference on 19 September to outline her policies in more detail. Takaichi finished as runner-up to Ishiba in the 2024 LDP presidential election. She enters the contest as one of the two frontrunners, alongside Agriculture, Forestry and Fisheries Minister Shinjiro Koizumi, in what is viewed by most observers as a two-horse race.

JAPAN (MNI): Kyodo News-Fmr. Minister Kono Offers Support to Koizumi in LDP Election

Kyodo News reports that former Minister for Digital Transformation Taro Kono has informed close associates that he does not intend to run for the presidency of the governing Liberal Democratic Party (LDP), and instead will offer his support to Agriculture, Forestry, and Fisheries Minister Shinjiro Koizumi. Kono, who has also served as Minister ofDefence and Minister of Foreign Affairs, is viewed as an influential figure within the LDP, having come second behind Fumio Kishida in the 2021 LDP leadership race.

JAPAN (BBG): Japan LDP’s Hayashi Aims for Sustained 1% Real Wage Gains

Japan’s top government spokesman Yoshimasa Hayashi vowed to ensure that real wages grow at a sustained pace of about 1% as part of a policy platform that he hopes will help him win the ruling party’s leadership race. The chief cabinet secretary presented policy proposals Thursday that he’s dubbed the “Hayashi Plan,” with wage growth a key priority. Hayashi emphasized his intention to build on the achievements of the administrations of both outgoing Prime Minister Shigeru Ishiba and his predecessor Fumio Kishida, positioning himself as a continuity candidate.

CHINA/S.KOREA (BBG): Top Envoys of China, South Korea Agree to Boost Strategic Ties

China and South Korea’s top diplomats pledged to deepen their strategic partnership in their first meeting since Seoul’s leadership change earlier this year. South Korean Foreign Minister Cho Hyun met with China’s Wang Yi in Beijing on Wednesday, urging Beijing’s cooperation to bring North Korea back to the dialogue table. South Korean President Lee Jae Myung’s administration has vowed to improve ties with both North Korea and China but Pyongyang has shunned Seoul’s efforts to reduce tensions.

RBA (MNI EXCLUSIVE): RBA Sees Risk That NAIRU Slightly Lower Than 4.5%

MNI discusses the RBA's labour market view. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

RBNZ (MNI): RBNZ Names New MPC Member

Finance Minister Nicola Willis has appointed Hayley Gourley to the Reserve Bank of New Zealand’s Monetary Policy Committee, replacing longtime member Bob Buckle. Gourley, who has an extensive background in New Zealand’s agribusiness sector, will join the Committee for the October Monetary Policy Review, following the end of Buckle’s term on Sept. 30. The appointment comes amid significant leadership changes at the RBNZ this year, with Governor Adrian Orr and Chair Neil Quigley departing.

BRAZIL (MNI): Copom Reiterates Higher for Longer Strategy

The Central Bank of Brazil reinforced a higher-for-longer strategy in its statement Wednesday, taking one more step to curb premature expectations for cuts by saying it will keep borrowing costs elevated for a "prolonged period." Holding the Selic rate at 15.00% for a second straight meeting, the BCB removed a reference to a "continuation of the interruption" of the hiking cycle from its statement, potentially signaling policymakers are no longer considering raising rates.

DATA

EUROZONE JUL CONSTRUCTION OUTPUT +0.5% M/M, +3.2% Y/Y (MNI)

SWITZERLAND DATA (BBG): Swiss Exports to US Collapsed in First Month of 39% Tariff

The highest US tariff among developed nations dealt a severe blow to Swiss exports, according to the first reading since the 39% levy took effect. Foreign sales to America, adjusted for seasonal swings, were 22% lower in August than in July, Swiss customs data showed Thursday. Imports from the world’s biggest economy held steady. That narrowed the US trade deficit with Switzerland to 2.06 billion francs ($2.6 billion) — from 2.93 billion francs the previous month — the second lowest reading since 2020.

JAPAN DATA (MNI): July Core Machine Orders Below Forecasts, Y/Y Momentum Holding Up

- JAPAN JULY CORE MACHINE ORDERS -4.6% M/M; JUNE +3.0%

Japan July core machine orders printed below forecasts. We fell 4.6%m/m in July against a -1.5% forecast (and after a 3.0% rise in June). In y/y terms we rose 4.9%, against a 5.2% forecast and 7.6% gain in June. In terms of the detail, government/public machine orders were up 21.3%m/m, but this segment is very volatile. Manufacturing and non-manufacturing both recorded rises in the month, but this was likely due to volatile components, which are excluded from the core machine headline outcome.

JAPAN DATA (MNI): Japan Household Financial Assets at Record at End-June

The balance of financial assets held by Japanese households rose 1.0% y/y to a record JPY2,239 trillion at the end of June, marking a 10th straight quarterly gain, preliminary Bank of Japan data showed Thursday. Cash and deposits stood at JPY1,126 trillion, slipping 0.1% y/y for the first decline since 2006 but still accounting for 50.3% of total assets, underscoring households’ caution in shifting into riskier investments.

AUSTRALIA DATA (MNI): Aussie Employment Lower Over August

- AUSTRALIA AUG EMPLOYED PERSONS CHANGE -5.4K

- AUSTRALIA AUG F-T EMPLOYED PERSONS CHANGE -40.9K

- AUSTRALIA AUG UNEMPLOYMENT RATE +4.2%

- AUSTRALIA AUG LABOR PARTICIPATION RATE +66.8%

Australia lost 5,400 jobs in August, well short of the 21,000 expected to be created, while the unemployment rate held steady at 4.2%, Australian Bureau of Statistics data showed Thursday. The employment-to-population ratio slipped 0.1 point to 64.0%. Full-time employment fell by 41,000, partly offset by a 36,000 rise in part-time jobs. Female full-time employment declined by 30,000 and male full-time by 11,000, while part-time roles rose 18,000 for women and 17,000 for men.

NEW ZEALAND DATA (MNI): NZ Q2 GDP Contracts 0.9% Q/Q

New Zealand’s economy contracted 0.9% q/q in Q2, sharply undershooting the Reserve Bank of New Zealand and market expectations for a 0.3% decline, official data showed Thursday. The fall followed a 0.9% rise in Q1, leaving GDP down 1.1% y/y in the year to June 2025. Expenditure on GDP dropped 0.9% in Q2 after rising 1.2% in Q1, and fell 0.6% over the year. Manufacturing was the largest drag, down 3.5% on weaker transport equipment, food, and metal products, while construction fell 1.8%.

By contrast, information media and telecommunications rose 1.8%, wholesale trade gained 1.4%, and rental and real estate services climbed 0.7%.

FOREX: NZD Weakness Extends Following Particularly Soft Q2 GDP

- The lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. This prompted the USD’s bearish momentum to stall on Wednesday and aggressively reverse higher. This theme was also on display early Thursday, with the USD index briefly extending its recovery from fresh cycle lows to 1.15% before easing back to unchanged levels on the session.

- The New Zealand dollar is the standout in the G10 space, following a particular weak set of Q2 GDP data. The -0.6% annual read has weighed heavily on the Kiwi, currently down 1.05% against the dollar and testing back below 0.5900. The data trumped the weaker-than-expected Aug employment change figure out of Australia, which has notably seen AUDNZD rise above 1.12 for the first time since late 2022. The cross has extended to its next target of 1.1250 in recent trade, the 76.4% Fibonacci retracement of the 2022 price swing.

- USDJPY tracks 0.3% higher on Thursday, extending the strong bounce following the FOMC. Notably for the pair, yesterday is a hammer candle formation - a bullish reversal signal. If correct, it signals scope for a recovery, with pivot support now established at 145.49, Wednesday’s low.

- Strong performance for equities has supported a significant move higher for EURJPY, breaking above key resistance at 173.97 and rising to a high of 174.31. The break higher opens 174.86, a Fibonacci projection, and 175.43, the Jul 11 ‘24 high and a key medium-term resistance.

- Support for the single currency has seen EURUSD bounce around 50 pips from the overnight 1.1781 lows. As a reminder, spot traded at fresh multi-year highs following the fed decision, printing 1.1919 and trading to within 4 pips of touted resistance. Support to watch is the 50-day EMA, at 1.1659.

- The September Bank of England decision headlines Thursday’s event risk, while the August US leading index, September Philly Fed and jobless claims data are all scheduled.

EGBS: Limited Swings in Bund Futures Around Supply and DE Issuance Plan

Bund futures are -1 tick at 128.90, comfortably within yesterday’s range. The passing of Spanish and French supply has helped futures away from the 128.72 low, alongside suggestions from the German Finance Ministry that they are not considering a 50-year Bund at present. Initial support in Bunds remains unchanged at 128.51.

- The German Q4 issuance plan saw bond issuance rise by E10.5bln, below our E12-13bln expectations. The main point to note that DFA plans only one E3bln auction for the 7-year line, rather than the two we had expected. While 30-year auction sizes were increased, it wasn’t too large in the grand scheme of things.

- The German curve leans bear steeper (yields flat to +2bps), but this doesn’t appear to be related to the German issuance plan. Long-end German ASWs aren’t underperforming the rest of the curve.

- 10-year EGB spreads to Bunds are biased tighter, with European equities staging a solid 1.3% recovery after Tuesday’s selloff.

- ECB Vice President de Guindos hasn’t given much away at today’s MNI Connect event. He said that the risk of persistent inflation undershooting is not that big.

- Today’s data (July current account and construction output) haven’t been market moving.

GILTS: Off Lows, BoE QT Decision Eyed

A bid in equities and some spillover from the presence of this morning’s EGB supply weighed on gilts, before the passage of the supply helped provide some stabilisation.

- Futures last little changed at 91.61.

- The bullish technical theme remains intact, with initial support and resistance located at 90.65 & 91.82, respectively.

- Benchmark yields within 1bp of yesterday’s close. 2s10s and 5s30s ~15bp off Sep closing highs.

- 10-Year spread to Bunds 1bp tighter at ~194bp.

- The outcome of today’s MPC meeting can be boiled down to two discrete topics: the vote surrounding the pace of APF reduction and any updates on communications and the vote surrounding Bank Rate.

- With rates seen on hold (and a 7-2 vote split expected), the biggest uncertainty and market reaction is expected around the former, with much less focus being placed upon the latter - but neither aspect should be ignored.

- If the APF decision was down to us, we would favour a target of GBP60-65bln with active sales in line with this year but with a change to the maturity buckets to re-align with the DMO. That would see short remaining at 3-7 years, medium to 7-15 years (rather than BOE’s 7-20 years) and long 15+ years (rather than 20+ years).

- Around 70% of analysts look for the decision to be between GBP60-75bln - but the range is wide from ending active sales (GBP49bln total reduction) to continuing with the total reduction of GBP100bln.

- BoE-dated OIS showing 6.5bp of cuts through year-end, 28bp through April, market operates at hawkish end of recent range.

- We will provide scenario analysis for gilt curves in due course.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.978 | +1.0 |

Nov-25 | 3.943 | -2.4 |

Dec-25 | 3.904 | -6.3 |

Feb-26 | 3.801 | -16.6 |

Mar-26 | 3.763 | -20.5 |

Apr-26 | 3.687 | -28.0 |

EQUITIES: E-Mini S&P Reaches Fresh Cycle Highs Post-Fed

Eurostoxx 50 futures recently traded through resistance around the 20-day EMA - a bullish development for now. The move higher undermines a recent bearish theme and signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. For now, Tuesday’s move down appears corrective. A bull cycle in S&P E-Minis remains intact and the contract is trading closer to its recent highs. A fresh cycle high on Tuesday reinforces current bullish conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6700.00 handle next and 6712.33, a Fibonacci projection. On the downside, initial support to watch is 6569.89, the 20-day EMA.

- Japan's NIKKEI closed higher by 513.05 pts or +1.15% at 45303.43 and the TOPIX ended 13.04 pts higher or +0.41% at 3158.87.

- Elsewhere, in China the SHANGHAI closed lower by 44.685 pts or -1.15% at 3831.656 and the HANG SENG ended 363.54 pts lower or -1.35% at 26544.85.

- Across Europe, Germany's DAX trades higher by 302.1 pts or +1.29% at 23659.35, FTSE 100 higher by 28.91 pts or +0.31% at 9237.42, CAC 40 up 86.21 pts or +1.11% at 7873.19 and Euro Stoxx 50 up 62.94 pts or +1.17% at 5432.64.

- Dow Jones mini up 301 pts or +0.65% at 46322, S&P 500 mini up 52.5 pts or +0.8% at 6653.75, NASDAQ mini up 242.25 pts or +1% at 24464.75.

Time: 10:00 BST

COMMODITIES: Short-Term Weakness for Gold Considered Corrective

The trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low. Gold remains in a clear bull cycle and short-term weakness is for now, considered corrective. A fresh all-time high, once again this week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3705.2, a Fibonacci projection. Initial firm support lies at $3558.4, the 20-day EMA. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend.

- WTI Crude up $0.08 or +0.12% at $64.12

- Natural Gas down $0.03 or -0.87% at $3.072

- Gold spot up $5.64 or +0.15% at $3665.34

- Copper down $1.4 or -0.3% at $461.8

- Silver up $0.15 or +0.37% at $41.827

- Platinum up $23.64 or +1.73% at $1393.57

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |