MNI US OPEN - Qatar Comments Raise Risk of Supply Interruption

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW: SOFTER, WITH MANY MOVING PARTS

- QATAR WARNS WAR WILL FORCE GULF TO STOP ENERGY EXPORTS WITHIN WEEKS: FT

- TRUMP TEAM DOWNPLAYS TREASURY OIL FUTURES TRADES AS PRICES SURGE

- EU SEES NO JUSTIFICATION TO RELEASE OIL STOCKS AMID IRAN WAR: BBG

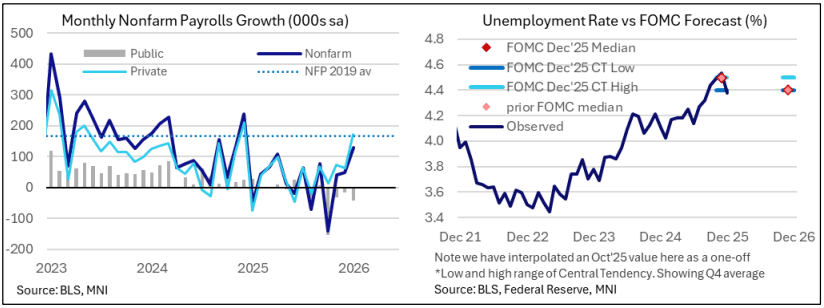

Figure 1: Recent US labour market developments

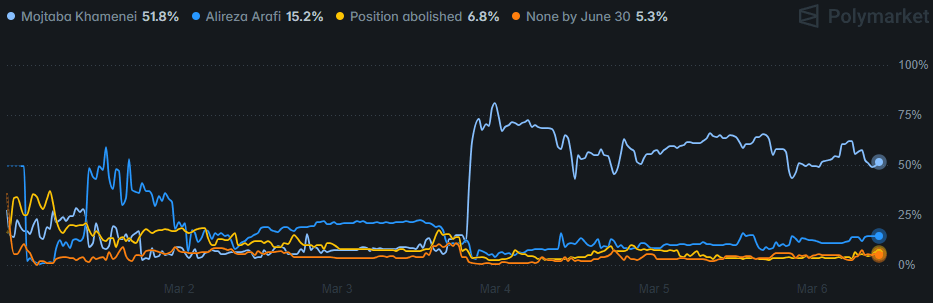

Figure 2: Prediction market implied probability of next Supreme Leader of Iran

Source: Polymarket

NEWS

MNI US PAYROLLS PREVIEW: Softer, With Many Moving Parts

Nonfarm payrolls are expected to increase 58k in February with gains coming entirely from the private sector, pulling back from a surprisingly strong January. One temporary impact known in advance was an additional 31k of striking workers over the payrolls reference period, the highest rise since late 2024. 32k workers will return in the March payrolls count. Beyond that, there are questions over the extent to which healthcare jobs pull back after a potential boost from a severe January flu season, with Scotiabank, at the low end of consensus, again eyeing a drag from ACA subsidies expiring at the end of the last year.

OIL (FT): Qatar Warns War Will Force Gulf to Stop Energy Exports Within Weeks

Qatar’s energy minister has warned that war in the Middle East could “bring down the economies of the world”, predicting that all Gulf energy exporters would shut down production within weeks and drive oil to $150 a barrel. Saad al-Kaabi told the FT that even if the war ended immediately it would take Qatar “weeks to months” to return to a normal cycle of deliveries following an Iranian drone strike at its largest liquefied natural gas plant. Qatar, the world’s second-largest producer of LNG, was forced to declare force majeure this week after the strike at its Ras Laffan plant.

US (BBG): Trump Team Downplays Treasury Oil Futures Trades as Prices Surge

The Trump administration is ruling out deploying the Treasury Department to trade oil futures for now, according to a person familiar with the matter, as government officials look tame to energy prices that have climbed amid the Iran war. Administration officials have discussed getting the Treasury Department involved in selling and buying energy futures but believe the agency’s ability to meaningfully affect the market is limited, said the person, who requested anonymity to discuss private conversations. Daily activity in the oil futures market has ballooned amid the conflict, diluting the potential impact of any one participant, the person said.

US (BBG): US Mulls Requiring Permits for Global Nvidia, AMD AI Chip Sales

Nvidia Corp. has long been the world’s AI kingmaker. Now, the Trump administration is considering taking a formal role in the industry that would include similarly sweeping powers. Officials at the US Commerce Department have written draft regulations that would restrict AI chip shipments to anywhere in the world without American approval, giving Washington broad control over whether other countries can build facilities for training and running artificial-intelligence models — and under what conditions. The proposed rule — which could change substantially or be shelved entirely — would require companies to seek US permission for virtually all exports of AI accelerators from the likes of Nvidia and Advanced Micro Devices Inc., a global expansion of curbs that currently cover around 40 countries, according to people familiar with the matter.

US (NYT): Trump Announces He Is Replacing Noem With Oklahoma Senator

President Trump fired Kristi Noem as homeland security secretary on Thursday and announced plans to replace her with Senator Markwayne Mullin of Oklahoma, concluding a long-building frustration with Ms. Noem that had come to a head this week with her grilling by Republicans at congressional hearings. Mr. Trump announced the change on social media, along with a new, and previously nonexistent, role for Ms. Noem inside the administration: special envoy for the Shield of the Americas, which he said would be a new security initiative for the Western Hemisphere.

US/RUSSIA (WSJ): U.S. Has a Big Ask for China: Buy Less Oil from Russia, More From America

Ahead of President Trump’s visit to Beijing, Treasury Secretary Scott Bessent is considering putting a tricky trade-off on the agenda for coming talks with his Chinese counterpart: reducing China’s oil purchases from U.S. adversaries like Russia. In private consultations held in recent days with former U.S. officials, business executives and policy analysts, Bessent described a continuing effort to try to get China to instead buy American oil-and-gas products, said people familiar with the meetings. Bessent is thinking about raising the energy issue, the people said, in a meeting with his Chinese counterpart, Vice Premier He Lifeng, in Paris in mid-March. They are planning to firm up a framework for the summit between Trump and Chinese leader Xi Jinping, currently slated for the beginning of April.

US/INDIA (BBG): US Grants Temporary Waiver for India to Import Russian Oil

The US has cleared the way for India to temporarily increase its purchases of Russian oil, reversing months of pressure on the world’s third-largest crude importer as an escalating conflict in the Persian Gulf upends energy flows. A license issued late on Thursday covers transactions related to Russian crude oil and petroleum products loaded onto vessels before March 5, so long as it’s delivered to India and purchased by an Indian firm. The measure expires April 4 at 12:01 a.m. Washington time.

UAE/IRAN (WSJ): U.A.E. Explores Freezing Iranian Assets to Punish Tehran for Attacks

The United Arab Emirates is weighing freezing billions of dollars of Iranian assets held in the Gulf state, according to people familiar with the discussions, a move that could sever one of Tehran’s most important economic lifelines. If the U.A.E. goes ahead, it would significantly curb Tehran’s access to foreign currency and global trade networks as its domestic economy, already buckling under inflation, is now engulfed in a military conflict. Emirati officials have privately warned Iran—which has fired more than 1,000 drones and missiles at targets in the U.A.E.—of the possible action, people familiar with the warnings said. It isn’t clear when, or if, the Emirati government will decide to act.

CANADA/JAPAN (MNI): Carney Arrives Ahead of Summit w/Takaichi

Canadian PM Mark Carney has touched down in Japan ahead of his summit later today with PM Sanae Takaichi. The trip is set to see the two countries upgrade their formal ties to the level of 'comprehensive strategic partnership'. Japan Times reports that the two sides will also "establish an economic security dialogue to reinforce supply chains for critical minerals and energy resources as well as to reduce dependence on any single country." Both Tokyo and Ottawa view closer relations as a geoeconomic imperative. Canada is a major producer of oil and LNG, while also possessing large supplies of critical minerals such as nickel, cobalt, lithium, graphite and copper. Japan purchases much of its oil from the Gulf and is vulnerable to the current crisis hindering cargoes through the Strait of Hormuz. Between Canada and Japan, there is no geopolitical chokepoint, making a closer partnership on energy an attractive prospect for Tokyo.

EU (BBG): EU Sees No Justification to Release Oil Stocks Amid Iran War

The European Union told member states this week that there is currently no justification to release strategic oil stocks, even as the Iran War continues to hamper key shipping lanes in the Strait of Hormuz, according to people familiar with the matter. The European Commission, the bloc’s executive arm, told a specially-convened Energy Union Task Force Thursday that member states hold strategic oil stocks covering 90 days of consumption — an obligation laid out by the International Energy Agency — and that at this stage there is no need to start releasing them, the people said. It said that particular attention was being paid to diesel and jet fuel supply, where dependence on the Middle East is higher.

ECB (BBG): ECB Highly Unlikely to Move Rates at Next Meeting, Escrivá Says

The European Central Bank probably won’t change its interest-rate stance at its March 19 policy decision, according to Governing Council member Jose Luis Escrivá. “With the information I currently have, I believe it is very unlikely that the Governing Council will change interest rates at the next meeting,” the Spanish central bank chief told TV3 on Friday. “Temporary movements should not lead us to make decisions — instead, we need to continue monitoring the situation.”

CHINA (MNI): PBOC to Keep Modest Easing, Liquidity Ample - Pan

MNI (Beijing) The People's Bank of China will continue with a moderately loose policy stance, cut reserve requirement ratios and policy rates at a flexible pace and promote the integrated effect of monetary and fiscal policies, Governor Pan Gongsheng told a briefing on Friday. The Bank will combine short-, medium-, and long-term policy tools, including reverse repos and government bond trading, in order to ensure ample liquidity and align the growth of aggregate financing and the money supply with targets for economic growth and price levels, he said.

CHINA (MNI): PBOC to Keep Yuan Stable - Pan

MNI (Beijing) The People’s Bank of China will correct any herd behavior and negative self-reinforcement in foreign exchange markets, maintaining the stability of the currency, Governor Pan Gongsheng told a briefing on Friday. The yuan is in the middle of its range against the dollar of recent years, and has appreciated against the greenback since the beginning of this year due to China's economic recovery and a weakening dollar index, Pan said, adding that the yuan China has neither the need nor the intention to gain trade competitive advantage through currency depreciation.

CHINA (MNI): China's 2026 GDP Growth Likely CNY6 Trillion - NDRC

MNI (Beijing) China’s GDP growth this year is expected to exceed CNY6 trillion, providing strong support for stabilising employment, improving social welfare, and preventing risks, Zheng Shanjie, director of the National Development and Reform Commission told reporters on Friday. The NDRC will further implement the special action to boost consumption, while promoting constructions of national projects, said Zheng. New investment led by the government is expected to exceed CNY7 trillion, with a focus on projects in the fields of transportation, consumption, low-altitude economy, artificial intelligence, education and medical care.

BOJ (MNI): BOJ's Himino Sees Inflation; Decision Up to Govt

Bank of Japan Deputy Governor Ryozo Himino said Friday that Japan is currently experiencing inflation, judging from the recent rise in consumer prices, but whether the country has escaped from deflation will ultimately be decided by the government. Himino told lawmakers that underlying CPI inflation is rising moderately toward the 2% target. He also said the weak yen is pushing up consumer prices through higher import costs and corporate pass-through.

TURKEY (BBG): Turkey Spends $12 Billion to Defend Lira From War-Fueled Turmoil

Turkey has spent $12 billion, equal to roughly 15% of its foreign-currency reserves, to keep the lira stable during a week of global market volatility triggered by the war in Iran. The Turkish central bank tightened liquidity conditions before markets opened on Monday and, when trading began, lenders stepped in to sell dollars to deter volatility, according to traders familiar with the deals, who asked not to be identified due to the private nature of the transactions. The amount of dollar sales declined throughout the week with no such transactions observed on Thursday, they said.

DATA

EUROZONE DATA (MNI): Q4 GDP Details Roughly as Expected

- EUROZONE Q4 GDP +0.2% Q/Q, +1.2% Y/Y (VS +0.3% Q/Q, +1.4% Y/Y Q3)

Q4 real GDP growth was revised to 0.20% Q/Q from 0.35% pre-rev (this was impacted by Ireland) after 0.30% in Q3 (from 0.27% pre-rev). Final domestic demand details seem broadly in line with consensus except for weaker investment although that was offset by an upward revision to Q3: Consumption 0.44% Q/Q (vs 0.4% cons) after Q3 revised to 0.25% from 0.15% pre-rev. Gross fixed capital formation 0.61% Q/Q (vs 0.8% cons) after Q3 revised to 1.25% from 1.01% pre-rev. Government spending 0.54% Q/Q (vs 0.5% cons) after Q3 revised to 0.67% from 0.72% pre-rev.

EUROZONE DATA (MNI): Q4 Compensation Per Employee a Little Below ECB Projections

Eurozone compensation per employee growth eased to 3.7% in Q4, down from 4.0% in Q3. This was below the ECB's 3.9% projection made in December.

UK DATA (MNI): BRC Footfall Worst Since Early 2025, Likely Boosted Online Store Sales

UK footfall data released overnight declined 4.7% Y/Y in February, down notably from -0.6% Y/Y in January (which was the highest since last August) - with wet weather highlighted as the key driver. The February reading is the weakest since March 2025, slightly dampening the early signs of the retail sector's bounce back from a relatively poor Q4 2025. Still, we note that recent hard retail sales data has been on the stronger side - but this release may present some downside risk to upcoming data. Comments from the press release: "One of the wettest Februarys on record saw shoppers shy away from in store visits last month ... a blow felt most keenly by clothing and footwear retailers."

UK DATA (The Times): UK House Prices Beat Expectations to Hit Record High

British house prices grew more than expected to a new record high in February as the property market maintained its early-year momentum, figures from the mortgage lender Halifax showed. Average property prices rose 0.3 per cent last month, after returning to growth in January. On an annual basis, the average house price gained 1.3 per cent, the strongest level in four months. Economists had forecast prices to be up 0.9 per cent on an annual basis and 0.3 per cent higher month on month.

FOREX: Dollar Boosted Amid Renewed Pressure on Risk

- Reports on Iran’s intended use of newer missiles in the coming days and the FT report from Qatar suggesting Gulf energy exporters would shut down production within weeks have sparked the latest round of market volatility. Oil prices have spiked higher and have taken out yesterday’s highs, while equities are coming under renewed pressure.

- These dynamics have had less of an impact on the FX markets, but have placed the greenback on the front foot, with the DXY rising to a fresh session high, although we remain around 10/15 pips off yesterday’s best levels.

- Notable pull lower for EURUSD back under 1.16, with specific pressure on the likes of EURCAD and EURNOK notable. EURCHF also continues to trade with a bearish tilt this week, moving to within 25 pips of the 0.9025 cycle lows.

- Risk sensitive currencies have remained in focus, with AUD volatility a key characteristic across the G10 complex. AUDUSD has slipped back towards 0.70, but remains well off key 50-day EMA support which now intersects at 0.6934. NZDUSD weakness more notable, dropping 0.3% to 0.5880.

- USDJPY has been less volatile this week, however, the higher core yields and renewed greenback strength are edging spot closer to the 157.97 highs from Tuesday’s session. USDJPY will be carefully monitored into the US employment data today, and as we approach levels where prior rate checks from both the BOJ and Fed were reported to have taken place in January.

- Today's NFP and retail sales are unlikely to alter the Fed’s March decision itself, with a next Fed cut currently not priced until September following the recent energy price surge. Nevertheless, they can help shape the revised quarterly projections. 9 Fed speakers are scheduled to appear next to RBA's Hauser and ECB's Cipollone & Schnabel.

EGBS: Sharp Repricing in ECB Hike Expectations Drives More Curve Flattening

- The German curve has twist flattened, with Schatz yields up 4bps to 2.28% amid another sharp hawkish repricing in ECB rate expectations. ECB-dated OIS now price 23bps of hikes through year-end, with prospects for a near-term offramp in the Middle East conflict appearing increasingly limited.

- Reports on Iran’s intended use of newer missiles in the coming days and the FT report from Qatar suggesting Gulf energy exporters would shut down production within weeks have sparked the latest round of market volatility. Oil prices have spiked higher and have taken out yesterday’s highs, while equities are coming under renewed pressure.

- 10-year German yields are up 2bps to 2.86%, while 30-year yields are marginally lower at 3.42%.

- Theres been a meaningful extension of the flattening on the EUR 10s30s swaps curve, alongside a sell-off in long end German swap spreads & ASWs. This points to a continued unwind of crowded longs in the likes of EUR 10s30s steepeners and swap spread/ASW widener exposure (which were heavily favoured plays surrounding expectations re: the Dutch pension transition).

- Bund futures are -5 ticks at 127.13. Volumes have been extremely heavy through the week, with almost 700k lots having traded this morning alone.

- 10-year EGB spreads to Bunds are up to 2bps wider, with GGBs underperforming.

- In data, Eurozone Q4 final GDP was revised down to 0.2% Q/Q (vs 0.3% flash), largely owing to a revision in Ireland. Compensation per employee growth of 3.7% Y/Y was below the ECB’s 3.9% projection.

- A reminder that the US labour market report is due at 1330GMT. Meanwhile, ECB's Schnabel will speak at 1700GMT.

GILTS: Bear Flattening Extends Alongside Hawkish BoE Repricing

Gilts remain under pressure with Qatar’s warning on upside potential for crude oil providing the latest headwind for core global FI markets and tailwind for energy prices, with ongoing missile activity in the Middle East also noted.

- Futures as low as 90.37 before a recovery to 90.60, -65 or so on the day. Fibonacci support (90.72) and the February 11 low (90.60) pierced, exposing key support at the February 9 low (89.79).

- Yields 4-9bp higher, curve flattens.

- 2s to the highest level in October. Bears will look to close the October 14 gap lower in the benchmark (3.950%)

- 10s through broke November highs (4.619%). October 14 gap lower would be closed at (4.658%)

- 2s10s registered a fresh low at 67.02bp on the move.

- The latest leg of hawkish repricing resulted in fresh cycle lows for SONIA futures, with SFIZ6 & SFIZ7 hitting the lowest levels seen since May. Next support levels of note there located at 96.225 & 96.115, respectively.

- BoE-dated OIS briefly priced less than 10bp of easing through year-end, back to ~14bp last and compares to 52-53bp late last week.

- Global cues dominate domestic matters in recent sessions, with inflationary risks stemming from the escalation in the Middle East at the fore, more than countering the market impact of February’s dovish hold from the BoE.

- Geopolitical matters centred on the Middle East and the U.S. NFP release in focus into the weekend.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.704 | -2.7 |

Apr-26 | 3.661 | -6.9 |

Jun-26 | 3.625 | -10.5 |

Jul-26 | 3.604 | -12.6 |

Sep-26 | 3.604 | -12.6 |

Nov-26 | 3.597 | -13.3 |

Dec-26 | 3.593 | -13.7 |

EQUITIES: E-Mini Remains Within a Tight Range, Attention on Support at 6751.50

A strong short-term reversal in EuroStoxx 50 futures has resulted in a breach of both the 20- and 50-day EMAs. This continues to highlight potential for a deeper pullback and Tuesday’s sell-off confirms this threat. Sights are on 5689.00 next, the Dec 18 ‘25 low. On the upside, initial firm resistance is 5956.56, the 50-day EMA ahead of 5999.50, the 20-day EMA. For now, short-term gains would likely be corrective. S&P E-Minis have recovered from their most recent lows. For now, the contract continues to trade inside a range. Attention is on the base of this range at 6751.50, the Feb 6 low. This support has been pierced, a clear break of it would highlight a stronger bear threat. On the upside, a resumption of gains and a breach of 6983.75, the Feb 25 high, would instead refocus attention on key resistance and the range top at 7043.00, the Jan 28 high.

- Japan's NIKKEI closed higher by 342.78 pts or +0.62% at 55620.84 and the TOPIX ended 14.26 pts higher or +0.39% at 3716.93.

- Elsewhere, in China the SHANGHAI closed higher by 15.628 pts or +0.38% at 4124.194 and the HANG SENG ended 435.95 pts higher or +1.72% at 25757.29.

- Across Europe, Germany's DAX trades lower by 21.92 pts or -0.09% at 23793.68, FTSE 100 higher by 8.61 pts or +0.08% at 10422.56, CAC 40 down 9.89 pts or -0.12% at 8035.91 and Euro Stoxx 50 down 15.66 pts or -0.27% at 5767.23.

- Dow Jones mini down 125 pts or -0.26% at 47855, S&P 500 mini down 23 pts or -0.34% at 6812, NASDAQ mini down 101 pts or -0.4% at 24948.75.

Time: 10:15 GMT (05:15 ET)

COMMODITIES: WTI Futures Through $80/bbl, Volatile Bull Cycle Intact

A volatile bull cycle in WTI futures remains intact. Despite being in overbought territory the contract traded higher again, Thursday, to confirm a resumption of the current uptrend. The move higher paves the way for a climb towards the $82.92 next, a Fibonacci projection. The first key support to monitor is $68.11, the 20-day EMA. A pullback would allow the overbought condition to unwind. Gold is unchanged and continues to trade below Monday’s intraday high. For now, a short-term bullish theme remains intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $5083.0, the 20-day EMA.

- WTI Crude up $3.24 or +4% at $84.28

- Natural Gas up $0.02 or +0.8% at $3.025

- Gold spot up $3.41 or +0.07% at $5087.69

- Copper up $1.6 or +0.28% at $582

- Silver up $0.57 or +0.69% at $82.7135

- Platinum up $24.81 or +1.17% at $2142.47

Time: 10:15 GMT (05:15 ET)

| Date | GMT/Local | Impact | Country | Event |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/1430 | ECB Cipollone Presentation at European Banking Federation Meeting | ||

| 06/03/2026 | 1330/0830 | *** | Retail Sales | |

| 06/03/2026 | 1500/1000 | * | Ivey PMI | |

| 06/03/2026 | 1500/1000 | * | Business Inventories | |

| 06/03/2026 | 1515/1015 | San Francisco Fed's Mary Daly | ||

| 06/03/2026 | 1515/1015 | Philadelphia Fed's Anna Paulson | ||

| 06/03/2026 | 1630/1130 | Kansas City Fed's Jeff Schmid | ||

| 06/03/2026 | 1700/1800 | ECB Schnabel Keynote at Booth School of Business Policy Forum | ||

| 06/03/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/03/2026 | 1820/1320 | Boston Fed's Susan Collins | ||

| 06/03/2026 | 1830/1330 | Cleveland Fed's Beth Hammack | ||

| 06/03/2026 | 2000/1500 | * | Consumer Credit | |

| 09/03/2026 | 2330/0830 | ** | Average Wages (p) | |

| 09/03/2026 | 2350/0850 | Balance of Payments |