MNI US OPEN - Putin, Witkoff to Discuss Ukraine Peace Plan

EXECUTIVE SUMMARY

- PUTIN TO MEET WITH WITKOFF AS US PUSHES FOR UKRAINE DEAL

- TRUMP OFFICIAL URGES HIGH COURT TO TAKE BAYER APPEAL

- BOE SEES INCREASED FINANCIAL STABILITY RISKS

- UEDA SHARPENS DEC RATE HIKE, RISKS CREDIBILITY – MNI EXCLUSIVE

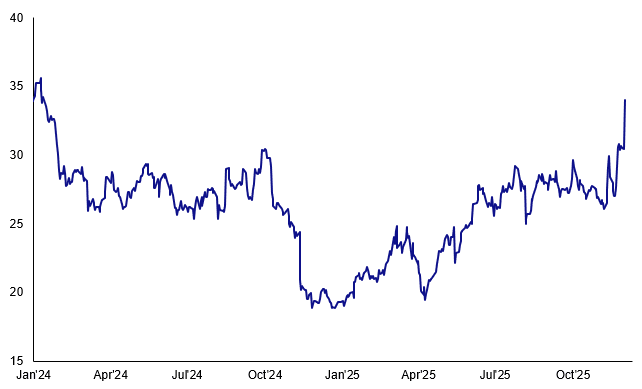

Figure 1: Largest 1-day surge for Bayer AG in over 2 decades after Trump official backs US Supreme Court review

Source: MNI, Bloomberg Finance L.P.

NEWS

US/RUSSIA/UKRAINE (MNI): Putin/Witkoff Meet at 09:00ET/14:00GMT; Russia Claims Key Ukraine City

Russian President Vladimir Putin is set to meet at ~16:00 local time (09:00ET, 14:00GMT) with US presidential envoy Steve Witkoff and US President Donald Trump's son-in-law, Jared Kushner, to discuss the amended 19-point peace plan negotiated between American and Ukrainian officials in late November. Putin had called the initial 28-point peace plan a potential "basis" for a future agreement. However, this plan was viewed by Kyiv, its European allies, and Russia hawks in the US as too favourable towards Moscow. The meeting comes after Russia claimed that it has taken the key 'fortress belt' city of Pokrovsk in the Donbas. Pokrovsk has seen some of the most intense fighting of the war. Ukraine's armed forces deny that the city has been fully captured by Russian troops.

US (BBG): Trump Official Urges High Court to Take Bayer Appeal

The Trump administration urged the US Supreme Court to take up Bayer AG’s appeal targeting thousands of lawsuits blaming its top-selling Roundup weedkiller for causing cancer. US Solicitor General D. John Sauer – the administration’s top courtroom lawyer – recommended Monday that the high court agree to hear Bayer’s challenge to a $1.25 million Missouri jury verdict over Roundup on the grounds some of the claims were preempted by federal law. Bayer shares surged as much as 15% on the news, the most in more than two decades.

US (WSJ): Trump Administration to Take Equity Stake in Former Intel CEO's Chip Startup

The Trump administration has agreed to inject up to $150 million into a startup trying to develop more advanced semiconductor manufacturing techniques in the U.S., its latest bid to support strategically important domestic industries with government incentives. Under the arrangement, the Commerce Department would give the incentives to xLight, a startup trying to improve the critical chip-making process known as extreme ultraviolet lithography, the agency said in a Monday release. In return, the government would get an equity stake that would likely make it xLight's largest shareholder.

UKRAINE (MNI): ECB Will Not Provide Backstop for EUR140bln 'Reparations Loan' - FT

The FT reported that, according to people familiar with the matter, the ECB has "concluded the EU plan to raise a 'reparations loan' backed by frozen Russian assets violated its mandate". With Ukraine's funding needs reaching a critical juncture (it will run out of funds by April 2026 if nothing is provided), there has been increasing pressure within the EU to use EUR140bln of the frozen Russian assets held at Belgium's Euroclear to act as collateral for 'reparations loans' that would be used to fund Ukraine's resistance and reconstruction, and repaid by Russia once the war is over.

BOE (MNI): BOE Sees Increased Financial Stability Risks

Risks to financial stability have increased during 2025 and global risks remain elevated and material uncertainty in the global macroeconomic outlook persists, the Bank of England's latest Financial Stability Report says. Key sources of risk include geopolitical tensions, fragmentation of trade and financial markets, and pressures on sovereign debt markets. Elevated geopolitical tensions increase the likelihood of cyberattacks and other operational disruptions, the report published Tuesday noted. The Tier 1 capital requirement, previously set at around 14% of risk weighted assets, was lowered to 13%, with the FPC saying that the UK banking system has maintained robust liquidity and funding positions and that asset quality remained strong. The countercyclical capital buffer, designed to protect against future shocks, was maintained at two percent.

BOJ (MNI EXCLUSIVE): Ueda Sharpens Dec Rate Hike, Risks Credibility

MNI discusses the BOJ's key concerns ahead of its December policy meeting. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japanese Ministers Refrain From Pushback After BOJ’s Hike Signal

Japan’s finance and economic ministers didn’t indicate any objections a day after Bank of Japan Governor Kazuo Ueda delivered the clearest hint yet pointing to the possibility of an interest rate increase this month. “The specific methods of monetary policy are, and should be, left to the BOJ, as a general rule, and I also believe this is the case,” Minister of Finance Satsuki Katayama said Tuesday at a post-cabinet meeting press conference. She added that the government expects the central bank “to appropriately implement monetary policy and operations” toward achieving its 2% inflation target.

JAPAN (BBG): Japan Panel Pushes Back on Takaichi’s Primary Balance Downgrade

Japan should still keep an eye on its primary balance, according to a Finance Ministry advisory panel, even after Prime Minister Sanae Takaichi signaled a shift away from a long-standing ministry target of achieving a surplus. “The primary balance remains a very important flow indicator for finance, so we told the government it needs to keep that firmly in mind when putting together next year’s budget,” Hiroya Masuda, acting chief of the panel, told reporters after submitting its recommendations Tuesday.

DATA

EUROZONE DATA (MNI): 2dp HICP Only Just Rounds Up to 2.2% Y/Y

- Headline 2.16% (2.1% MNI tracking and consensus, 2.10% prior)

- Core 2.41% (2.4% MNI median, 2.37% prior)

- Services 3.46% (3.4% MNI median, 3.36% prior)

UK DATA (MNI): BRC Shop Prices Slow Further in November, Black Friday Impact Possible

- UK NOV BRC SHOP PRICES -0.1% M/M, +0.6% Y/Y

The BRC-NIQ Shop Price Monitor slowed again in November, posting a 0.6% Y/Y increase (vs 1.0% Oct). The BRC cites Black Friday deals beginning "earlier than normal" this year pushing prices down. Do note there the different survey periods for the BRC and ONS official CPI data and so disinflation in the BRC series may therefore not be followed through with similar disinflation in the official CPI data. Similar to October, there was a slowdown in inflation across most categories. However, this time fresh food inflation also decreased for the first time since March (following a peak of 4.2% in October) - meaning that all broad categories saw a decline.

UK DATA (FT): UK House Prices Edge Higher Despite Budget Uncertainty

UK house prices withstood market nervousness in the run-up to the Budget and pressures from high interest rates, gaining 0.3 per cent in November on the previous month. The month-on-month rise took the average property cost to £272,998, according to data from lender Nationwide published on Tuesday. Prices were up 1.8 per cent from November last year, an easing from the 2.4 per cent in the previous month.

GERMANY DATA (MNI): VDMA Orders Driven Up by Base Effects in October

German VDMA machinery orders were higher on a Y/Y basis in October, at 4%, with domestic orders at 0% Y/Y and foreign orders up 6%. "Overall, however, this small increase can unfortunately only be seen as consolidation at a low level, as October of the previous year was one of the weakest months of 2024. For the current year 2025, for the period from January to October, there is still a real decline of one per cent in order intake", VDMA concludes.

JAPAN DATA (MNI): Japan Consumer Confidence Posts 4th Straight Rise

Japan’s consumer confidence index posted a fourth straight rise in November, climbing 1.7 points to 37.5 from 35.8 in October, though the government left its overall assessment unchanged, data released by the Cabinet Office on Tuesday showed. Indexes tracking overall economic well-being, perceptions of income conditions, the labour environment and willingness to buy durable goods all improved. An official told reporters that the rise in the Nikkei Stock Average appeared to be behind the improvement in sentiment, although the government said it had not asked respondents about the reasons for the change from the previous month.

AUSTRALIA DATA (MNI): Sideways Dwelling Approvals to Add to Housing Inflation

- AUSTRALIA OCT BUILDING APPROVALS -6.4% M/M, -1.8% Y/Y

The number of building approvals fell 6.4% m/m in October, weaker than expected, after rising 11.1% m/m to be down 1.8% y/y. Multi-dwelling approvals have been driving the volatility in the headline number but annual growth in both it and private houses is soft and likely to add to already strong house price growth. Approvals have moved sideways this year. Private houses fell 2.1% m/m in October to be up only 1.3% y/y but better than September's -0.5% y/y. 3-month momentum turned positive in October though.

AUSTRALIA DATA (MNI): Slight Q3 Net Export Detraction as Trade Surplus Narrows

- AUSTRALIA Q3 CURR ACCT BALANCE -16646M

Net exports detracted 0.1pp from Q3 quarterly GDP growth, which with the inventory print would normally pose a downside risk to consensus' forecast of +0.7% q/q but public demand's 0.4pp contribution is an upside risk. Q3 balance of payments was also released and not only did the current account deficit widen, when a narrowing was forecast, but it was revised substantially higher in Q2 to $16.2bn. Q3 was $0.4bn higher at $16.6bn, the highest since Q4 2024, as the trade surplus narrowed.

FOREX: USDJPY Bounce Off Lows Erases Much of Monday Decline

- USDJPY extended its recovery from yesterday's 154.67 lows, erasing a large part of the move triggered by Ueda at the beginning of the week. The pair has pierced back above the 20-day EMA - which remains a key intraday pivot point. A stronger risk backdrop has helped, with the ~150 pip bounce back above 156.00 looking convictive. Technical considerations would also suggest the trend set-up in USDJPY is bullish and the latest pullback can be considered corrective. The bull trigger for USDJPY remains 157.89, the November 20 high.

- GBPUSD meanwhile weakened below the 1.3200 handle as BoE's Bailey talks through the Bank's Financial Stability Report, in which the FPC see the economy as being exposed to greater risks to financial stability. The trend theme in GBPUSD is unchanged, it remains bearish and a recovery in November appears corrective. Initial support sits at 1.3125, the Nov 26 low.

- Russian President Putin is set to meet US's Witkoff and Kushner later today to discuss the amended 19-point peace plan negotiated between American and Ukrainian officials in late November. A breakthrough would undoubtedly be risk-positive but prediction markets remain sceptical of a ceasefire in the very near term.

- The rest of today's calendar is light, with only Redbook Retail Sales scheduled in the US and the Fed remaining in blackout. ECB's Dolenc is scheduled to speak but unlikely to move the needle.

EGBS: Bear Cycle in Bund Futures Intact, Sep 25 Low the Next Downside Target

Bund futures breached key short-term support at 128.37 yesterday, confirming a resumption of the bear cycle that started on October 17. Next support is the Sep 25 low at 127.88. Intraday, moves have been relatively modest, with futures down 5 ticks at 128.26.

- There was no tangible reaction in the short-end to slightly firmer-than-expected Eurozone headline HICP data. Core HICP was in line at 2.41% Y/Y (2.4% MNI median, 2.37% prior).

- Germany sold E4.5bln of the 2.00% Dec-27 Schatz, concluding its 2025 capital markets issuance. Demand metrics were a little better than the November re-opening, albeit for a smaller auction size.

- German yields are little changed across the curve. The 10-year Bund yield is consolidating just above the 2.75% figure. The initial topside target in yields is 2.780%, the Sep 25 high.

- The EUR 10s30s curve has established itself above 30bp since mid-November, with the next upside target of note located at the Oct ’21 closing high (35.03bp). The Dutch pension transition remains the medium-term focal point for participants in the long end of the EUR swaps curve

- 10-year EGB spreads to Bunds are marginally tighter, with European equities up almost 0.5%. Budget negotiations remain in focus in France. The 70bp level continues to provide support to the 10-year OAT/Bund spread for now, but agreement on the 2026 budget would pave the way for a move towards 65bps. French core state budget data for October saw a further improvement in YTD tracking.

- In addition to the flash Eurozone inflation data, the Eurozone unemployment rate was a tenth higher than consensus at 6.4% (September was also revised up a tenth to 6.4%).

GILTS: Round Numbers Limit Sell Off

Round numbers once again provide good support for gilts, with bears only managing to push futures a little below 91.00 (basing at 90.98) before a recovery to ~91.15, while 4.50% held in 10-Year yields.

- Bears eye 90.53 on any extension lower in the contract, while bulls need to retake 91.93 to start to regain momentum.

- Yields little changed across the curve after the move off last week’s post-Budget lows.

- Comments from OBR’s Miles were not particularly pertinent for markets. A reminder that Richard Hughes has resigned from his position as head of the OBR following the early release of its forecasts and documentation that were supposed to come after the Chancellor had delivered the Budget.

- Elsewhere, BoE Governor Bailey has noted that a change of market structure and trading norms isn’t limited to just the gilt market. This isn’t market moving and the BoE has covered the evolution of gilt market structure/alterations in participation on many occasions.

- Aug-31 I/L supply passed smoothly.

- STIRs continue to price over 80% odds of a December rate cut from the BoE despite this week’s sell off in wider core global FI markets. Terminal rate pricing remains steady around 3.35%, while SFIZ6 is 6.5 off year-to-date highs.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.751 | -21.8 |

Feb-26 | 3.685 | -28.5 |

Mar-26 | 3.599 | -37.0 |

Apr-26 | 3.489 | -48.0 |

Jun-26 | 3.444 | -52.5 |

Jul-26 | 3.380 | -58.9 |

Sep-26 | 3.363 | -60.6 |

EQUITIES: E-Mini S&P Holding Onto Gains Following Recovery From Nov 21 Low

Recent gains in Eurostoxx 50 futures undermines a recent bearish theme and the contract is holding on to its gains. Price has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5742.40, a Fibonacci retracement point. For bears, a reversal lower would instead expose the key short-term support and bear trigger at 5475.00, the Nov 21 low. S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed higher by 0.17 pts or +0% at 49303.45 and the TOPIX ended 2.73 pts higher or +0.08% at 3341.06.

- Elsewhere, in China the SHANGHAI closed lower by 16.294 pts or -0.42% at 3897.712 and the HANG SENG ended 61.79 pts higher or +0.24% at 26095.05.

- Across Europe, Germany's DAX trades higher by 132.89 pts or +0.56% at 23722.6, FTSE 100 higher by 15.68 pts or +0.16% at 9718.15, CAC 40 up 18.01 pts or +0.22% at 8114.31 and Euro Stoxx 50 up 30.42 pts or +0.54% at 5697.89.

- Dow Jones mini up 37 pts or +0.08% at 47389, S&P 500 mini up 9 pts or +0.13% at 6835.5, NASDAQ mini up 56.75 pts or +0.22% at 25448.5.

Time: 10:05 GMT

COMMODITIES: Short-Term Gains for WTI Futures Considered Corrective

Short-term gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. Note that the recovery since Oct 28 signals the end of the corrective cycle. Key support to watch lies at the 50-day EMA, at $4001.1. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude down $0.15 or -0.25% at $59.17

- Natural Gas down $0.01 or -0.18% at $4.917

- Gold spot down $41.42 or -0.98% at $4191.49

- Copper down $3.6 or -0.68% at $526.7

- Silver down $1.01 or -1.74% at $56.9997

- Platinum down $48.08 or -2.88% at $1618.74

Time: 10:05 GMT

| Date | GMT/Local | Impact | Country | Event |

| 02/12/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 02/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 02/12/2025 | 1500/1000 | Fed Vice Chair Michelle Bowman | ||

| 03/12/2025 | 2200/0900 | * | S&P Global Services PMI (f) | |

| 03/12/2025 | 2200/0900 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0030/0930 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0030/1130 | *** | Quarterly GDP | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0145/0945 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0700/0200 | * | Turkey CPI | |

| 03/12/2025 | 0730/0830 | *** | CPI | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 0930/0930 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0930/0930 | *** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 1000/1100 | ** | EZ PPI | |

| 03/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/12/2025 | 1030/1130 | ECB Lane Keynote at Banca d'Italia Workshop on Exchange Rates | ||

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services PMI (f) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Composite PMI (f) | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies |