MNI US OPEN - Iran Retaliates Following Major Israeli Strikes

EXECUTIVE SUMMARY

- IRAN LAUNCHES RETALIATORY DRONE WAVE FOLLOWING ISRAELI STRIKES

- TRUMP CAN KEEP DEPLOYING TROOPS IN LA FOR NOW, COURT SAYS

- HUNDREDS OF ‘NO KINGS’ RALLIES PLANNED IN OPPOSITION TO TRUMP

- BOJ IS SAID TO SEE INFLATION RUNNING STRONGER THAN EXPECTED

Figure 1: Where Israel attacked Iran

Source: NYT

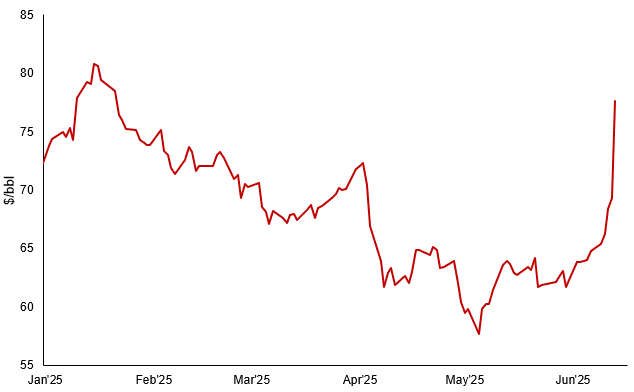

Figure 2: WTI futures posts intraday gain of as much as 14%, before fading

Source: MNI/Bloomberg Finance L.P.

NEWS

MIDEAST (MNI): Iran Launches Retaliatory Drone Wave Following Israeli Strikes

Reuters reports that, according to the US State Department, the US Embassy (likely in Amman) has "indications there may be missiles, drones, or rockets flying over Jordanian airspace". There have been numerous reports over the past hour that Iran has launched at least a first wave of ~100 retaliatory drones/missiles against Israel following the overnight attacks on nuclear and political sites and key military commanders and scientists. AP reported that the Israeli military has said it has begun intercepting Iranian drones following Israel's strikes on Iran overnight.

A response of this scale was always likely, and given the scope of Israel's Iron Dome air defences, as well as those of Jordan and Israeli allies with military deployments in the region, such as the US and UK, this wave is unlikely to cause significant trouble for Israel. Iranian Supreme Leader Ayatollah Ali Khamenei has said Israel will face a 'severe punishment' for the attacks.

MIDEAST (BBG): Israel Attacks Iran’s Nuclear Sites in Major Escalation

Israel launched airstrikes across Iran on Friday morning, targeting nuclear facilities and killing senior military commanders in a major escalation that could spark a broad war in the Middle East. Explosions were heard across Tehran, Natanz — home to a key atomic site — and other cities, according to local and social media. Israeli Prime Minister Benjamin Netanyahu said Israel — which used 200 air force planes and said it hit around 100 targets — had “struck at the heart of Iran’s nuclear enrichment program.” The head of the Islamic Revolutionary Guard Corps, Hossein Salami, and the military’s chief of staff, Mohammad Bagheri, were both killed, according to Iranian media.

US (BBG): Trump Can Keep Deploying Troops in LA for Now, Court Says

The Trump administration won a brief reprieve from a judge’s order to pull back on its use of military troops in Los Angeles to deal with protests over the president’s immigration raids. A three-judge panel of the 9th US Circuit Court of Appeals in San Francisco put the judge’s order on hold and scheduled a hearing for Tuesday to discuss further action in the case. The move came hours after US District Judge Charles Breyer directed the federal government to return control of the California National Guard to state leaders and cease efforts to direct those troops to respond to protests while a lawsuit challenging the actions proceeds.

US (WSJ): Hundreds of ‘No Kings’ Rallies Planned in Opposition to Trump

Boasting tanks, cannons, soldiers and fireworks, President Trump’s military parade Saturday is designed to be a spectacle. Opponents to Trump want their nationwide protests that day to be an even bigger one. Progressive groups including the American Civil Liberties Union, American Federation of Teachers, Planned Parenthood and Sen. Bernie Sanders’s campaign office are planning peaceful protests in over 2,000 cities across the U.S.

US (WSJ): House Narrowly Passes DOGE Cuts After Holdout Republicans Change Votes

House Republicans narrowly passed a $9.4 billion rescissions package that includes cuts to foreign aid as well as the entity that funds National Public Radio and the Public Broadcasting Service. The vote was 214-212, after some last-minute arm twisting by GOP leaders convinced two Republicans—Reps. Nick LaLota of New York and Don Bacon of Nebraska—to switch their votes to yes from no.

US (FT): China Delays Approval of $35bn Us Chip Merger Amid Donald Trump’s Trade War

A $35bn US semiconductor industry merger is being delayed by Beijing’s antitrust regulator, after Donald Trump tightened chip export controls against China in a move that exacerbated trade tensions between the world’s two largest economies. China’s State Administration for Market Regulation has postponed its approval of the proposed deal between Synopsys, a maker of chip design tools, and engineering software developer Ansys, according to two people with knowledge of the matter.

BOJ (BBG): BOJ Is Said to See Inflation Running Stronger Than Expected

Bank of Japan officials see prices rising a little stronger than they expected earlier in the year, a factor that may open the door to discussions over whether to raise interest rates if global trade tensions ease, according to people familiar with the matter. The officials expect the central bank’s benchmark interest rate to be left at 0.5% at the end of a two-day gathering next week as they need to monitor developments in tariff talks globally and their economic implications, the people said.

UK (FT): A Quarter of Top Companies in London’s IPO Class of 2021 Quit Stock Exchange

A quarter of the biggest companies in London’s bumper crop of 2021 listings have since left the stock market while those remaining have lost £10bn in value, highlighting the exchange’s struggle to retain top-tier businesses. This week alone two businesses in the 2021 vintage have succumbed to cut-price takeovers. Analysis by the Financial Times shows that eight of the 33 companies that raised more than £100mn by listing in London in 2021 have since been sold, delisted or fallen into administration.

PERU (BBG): Peru Holds Key Rate as Policymakers Weigh Risks to Growth

Peru held interest rates unchanged as the central bank gauges whether US tariff policy will jeopardize its combination of the fastest growth and the lowest inflation among Latin America’s major economies. Policymakers held borrowing costs at 4.5% on Thursday, as expected by 13 of 14 economists surveyed by Bloomberg. Just one analyst forecast a second straight quarter-point rate reduction to 4.25%. “Most indicators and expectations remained in the optimistic range, in a context where economic activity is hovering around its potential level,” the bank said in its policy statement.

DATA

EUROZONE DATA (MNI): Industrial Production Deterioration Driven by Ireland

- EUROZONE APR IP -2.4% M/M, +0.8% Y/Y

Eurozone industrial production deteriorated at the start of Q2, printing below consensus expectations at -2.4% M/M in April (-1.7% cons; 2.4% March, downwardly revised by 0.2pp). However, the drop appears to be driven by a material reversal of previous strength from Ireland. Irish IP was -15.2% M/M in April vs +14.3% in March and +11.6% in February. Ireland benefitted strongly in Q1 from US tariff front-running, particularly in the pharma sector. ECB's Lagarde has mentioned in last week's press conference that the general economic outlook for the Eurozone has deteriorated for the remainder of 2025.

UK DATA (MNI): Consumer Inflation Expectations Remain High in Medium-Term

The MPC will be relieved that consumer inflation expectations did not pick up further in the quarterly BOE / Ipsos Inflation Attitudes Survey which was conducted in May, but will remain wary that the 12-24 month and 5-year ahead inflation expectations remain so high. This has been flagged as a big concern for the MPC regarding second round effects and future wage demands. Year-ahead expectations fell back to 3.2% in May from 3.4% in February (which had been the highest level since August 2023). Expectations for 12-24 months remained at 3.2% in May (as they were in February after seven consecutive quarters of between 2.6-2.8% when rounded to 1dp).

UK DATA (MNI): KPMG-REC Report on Jobs: Candidate Availability Lowest Since Dec 2020

Following the ONS labour market release on Tuesday which showed a very soft payrolls print, the KPMG-REC Report on Jobs released overnight had some more gloomy details. Most notably, it showed that the availability of candidates rose at the quickest pace since December 2020 "amid reports of redundancies and fewer job opportunities." However, the decline in vacancies was the smallest in eight months and there were some increases in pay with the availability of candidates matching the skills required for new positions limited - and pay growth was below the long-term average.

GERMANY DATA (MNI): CPI Details Suggest Ongoing But Slow Services Disinflation

- GERMANY MAY FINAL HICP AND CPI UNREVISED FROM FLASH

German final May HICP was unrevised from the flash readings at 2.1% Y/Y (2.2% prior) and 0.2% M/M. The final reading to CPI was also unrevised at 2.1% Y/Y (2.1% prior) and 0.1% M/M. Core CPI decelerated 0.1pp to 2.8% Y/Y, a rate not seen since January. Overall, the data confirms the main conclusions from the flash / state-level reading - services decelerated materially (contribution to headline -0.21pp vs prior on the back of the Easter effect unwind) while goods inflation accelerated (contribution +0.21pp vs prior) following firmer energy and alcohol / tobacco Y/Y rates.

GERMANY DATA (MNI): No Progress in German Inflation Breadth in May

MNI's inflation breadth tracker shows disinflation overall stalling in May, with the percentage of ECOICOP (European classification of individual consumption according to purpose, a standardized category split) items printing at or below 1% falling 2.8pp to 40.0%. In the high-inflation categories, similar trends could be observed, with the percentage of categories above 5% rising 0.8pp to 15.6% in May.

FRANCE DATA (MNI): Airfares and Package Holidays Weigh on French May Services

- FRANCE MAY HICP -0.2% M/M, +0.6% Y/Y

- FRANCE MAY CPI -0.1% M/M, +0.7% Y/Y

French headline HICP confirmed flash estimates on a rounded basis at 0.59% Y/Y (vs 0.62% flash, 0.92% prior), with CPI also confirmed at 0.66% Y/Y (vs 0.67% flash, 0.82% prior). INSEE's seasonally adjusted CPI series highlights waning 3m/3m momentum in France (-0.66% in May vs -0.65% prior), which is coming alongside weak developments in the labour market outlook. Services CPI inflation was confirmed at 2.1% Y/Y (vs 2.4% prior).

SPAIN DATA (MNI): Spain Upwardly Revised, Symmetrical Revision Risks to EZ

- SPAIN MAY HICP +0% M/M, +2% Y/Y

Spain HICP was upwardly revised for May by one tenth to 2.0% Y/Y (1.98% to 2dp, 2.24% Apr). On downside drivers vs April on final national CPI (which was also upwardly revised by 0.1pp), INE flagged leisure and culture (0.5pp lower at 2.2%) as well as housing (0.4pp lower to 3.8%). Contrary to the flash release, INE do not explicitly mention transport prices as a downside driver this time - this makes it possible that that category drove the headline upside revision at least to some extent.

SWEDEN DATA (MNI): Unsurprising Drivers in May Inflaiton Report; Momentum Still Eases

- SWEDEN FINAL MAY CPIF +2.3% Y/Y

Swedish May CPIF ex-energy confirmed flash estimates at 2.47% Y/Y (vs 3.10% prior), below the Riksbank's 2.68% March MPR projection. Headline CPIF also confirmed the flash at 2.26% Y/Y (vs 2.30% prior), in line with the Riksbank's projection. MNI's estimate of seasonally adjusted underlying inflation indicates benign price pressures in May, rising 0.02% M/M (vs 0.35% in April). That pulls 3m/3m momentum down to 3.04% (vs 3.90% prior). Although details of the report suggest one-off (and expected) factors pulled down inflation in May, the Riksbank's view that the Q1 uptick in inflationary pressures was temporary is being affirmed. This could support a 25bp cut next Wednesday.

CHINA DATA (MNI): China May New Loans, Aggregate Finance Rise Further

- CHINA JAN-MAY TSF CNY18.63 TRLN VS MEDIAN CNY18.54 TRLN

- CHINA JAN-MAY NEW LOANS CNY10.68 TRLN VS MEDIAN CNY10.96 TRLN

- CHINA END-MAY M0 +12.1% Y/Y VS +12.0% Y/Y END-APR

- CHINA END-MAY M1 +2.3% Y/Y VS +1.5% Y/Y END-APR

- CHINA END-MAY M2 +7.9% Y/Y VS MEDIAN +8.1%; END-APR +8.0% Y/Y

MNI (Beijing) China's total social financing rose by CNY2.29 trillion in May, nearly doubling April's CNY1.16 trillion, mainly driven by the accelerated issuance of government bonds and increased corporate bond financing amid low interest rate environment, data released on Friday by the People's Bank of China showed. Banks extended CNY620 billion in new loans in May, rising from April's CNY280 billion.

RATINGS: Fitch on Belgium Headlines Sovereign Update Schedule This Evening

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Fitch on Belgium (current rating: AA-; Outlook Negative) & Norway (current rating: AAA; Outlook Stable)

- Moody’s on Finland (current rating: Aa1; Outlook Stable) & Slovakia (current rating: A3; Outlook Stable)

- S&P on Germany (current rating: AAA; Outlook Stable) & Sweden (current rating: AAA; Outlook Stable)

- Scope Ratings on Poland (current rating: A; Outlook Stable)

FOREX: USD Partially Regains Haven Status, But Downtrend Not Under Threat

- The dollar has been the main beneficiary of the risk-off price action seen following the Israeli strikes on Iran overnight, but the commodity-sensitive NOK and CAD have shown more resilience than other G10 peers.

- Having underperformed all week - the dollar is benefiting from the risk-off, rally in oil prices and downtick in equities following the Israeli strikes on Iran. Resultantly, the USD Index is back above 98.00, but the bounce remains shallow: prices are already fading, and failed to top yesterday's high - let alone the levels of the first half of the week.

- As such, the broader downtrend holds firm, with the downtrendline drawn off the early February highs (today at 99.235) under very little threat from this dollar bounce.

- Although off session highs, Brent crude futures remain up almost 7%, with TTF futures also up over 4%. Our Commodities team notes that attention has shifted to Iran's response to the strikes, as some experts cited by Bloomberg predict an extended campaign by Israel to disable Iran's nuclear program. That leaves EURNOK down 0.4% and NOKSEK up 0.5% on the session, with fresh krone strength seen over the past hour.

- Focus for the remainder of Friday trade rests on any further escalation in Iran/Israel tensions, particularly as the Iranian President is to imminently be delivering a speech on, presumably, the Iranian response to the Israeli strikes.

EGBS: Bunds Back to Unchanged Despite Ratchet Higher in Geopol Risk

- Despite a ratchet higher in geopolitical risk following Israel’s strikes on Iran, Bund futures have pulled back from overnight highs to trade little changed on the session at 131.32. Resistance at 131.85 (Apr 22 high) was pierced but has held, alongside the 2.43% support in the 10-year Bund yield (Apr 7 low).

- The German curve has lightly bear flattened, with Schatz yields up 1bp and 30-year Bund yields little changed.

- Today’s Euribor fixing spurred a burst of downside activity in the EUR front-end, which partly spilled over into Schatz futures.

- Weak risk sentiment sees BTP futures (-35 ticks at 121.17) underperform Bunds. In cash markets, the 10-year BTP/Bund spread has widened 3bps to 96bps, after tracking within a 90-92bp range through this week.

- Today’s regional data has not been market moving. Final May HICP prints from Germany, France and Spain confirm an unwind of Easter effects, while April EZ industrial production was weaker-than-expected (likely due to an unwind of Q1 Irish tariff front-running).

- Geopolitics remains the focus for the rest of the session, with only the US June UoM survey due at 1500BST.

GILTS: Yields Hold Higher as Initial Risk-Off Reverses

Gilts hold lower on the day after the rally seen at the open quickly faded.

- Our best guess is that the lack of meaningful Iranian response to the Israeli attack on its nuclear and military facilities (including the killing of high-ranking officials), as well as the fact that the market was already aware of non-negligible risks of such an attack, has driven the pullback.

- Oil is also off Asia highs, given the lack of damage to Iranian oil infrastructure.

- Futures traded as high as 93.68 before fading back to ~93.00.

- The May 8 high (from a continuation chart) has been pierced, with the recent bullish phase extending. Initial support and resistance now located at 92.80 & 93.73.

- Yields 2.0-3.5bp higher, curve bear flattens.

- The recent rally has seen 20- & 30-Year yields pierce their May lows.

- Local data releases have included another gloomy round of labour market data (REC report on Jobs) and the latest BoE/Ipsos inflation expectations survey. For the latter, the MPC will be relieved that consumer inflation expectations did not pick up further but will remain wary that the 12-24 month and 5-year ahead expectations remain so high.

- BoE-dated OIS back to pricing ~50bp of cuts after printing 52-53bp late yesterday.

- Tensions in the Middle East and the U.S. UoM survey will provide inputs from further afield.

EQUITIES: E-Mini S&P Pierces Support at 20-Day EMA

Today’s move down in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5298.00. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would highlight a short-term top and signal scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5374.40, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high on Wednesday, reinforcing current bullish conditions. For now, today’s pullback is considered corrective. The contract has pierced support at 5933.69, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5825.83. Key short-term resistance has been defined at 6074.75, the Jun 11 high.

- Japan's NIKKEI closed lower by 338.84 pts or -0.89% at 37834.25 and the TOPIX ended 26.5 pts lower or -0.95% at 2756.47.

- Elsewhere, in China the SHANGHAI closed lower by 25.662 pts or -0.75% at 3376.996 and the HANG SENG ended 142.82 pts lower or -0.59% at 23892.56.

- Across Europe, Germany's DAX trades lower by 388.83 pts or -1.64% at 23385.33, FTSE 100 lower by 45.35 pts or -0.51% at 8840.74, CAC 40 down 88.08 pts or -1.13% at 7683.75 and Euro Stoxx 50 down 81.92 pts or -1.53% at 5283.97.

- Dow Jones mini down 517 pts or -1.2% at 42472, S&P 500 mini down 74.5 pts or -1.23% at 5974.25, NASDAQ mini down 331 pts or -1.51% at 21599.75.

Time: 10:00 BST

COMMODITIES: WTI Futures Rally Sharply, Continuation Would Expose $80 Handle

WTI futures have traded sharply higher this week and today's rally marks an acceleration of the current bull phase. Price action is likely to be volatile and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. Initial support lies at $71.50, the Apr 2 high. A firmer support is noted at today’s intraday low - at $68.49. A bullish theme in Gold remains intact and this week’s gains reinforce bullish conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen bullish conditions and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3255.2, the 50-day EMA.

- WTI Crude up $5 or +7.35% at $73.1

- Natural Gas up $0.05 or +1.35% at $3.538

- Gold spot up $38.83 or +1.15% at $3425.54

- Copper down $8.35 or -1.71% at $480.7

- Silver up $0.02 or +0.07% at $36.362

- Platinum down $23.21 or -1.79% at $1275.28

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |