MNI ASIA MARKETS ANALYSIS: US/China Extend Tariff Deadline

HIGHLIGHTS

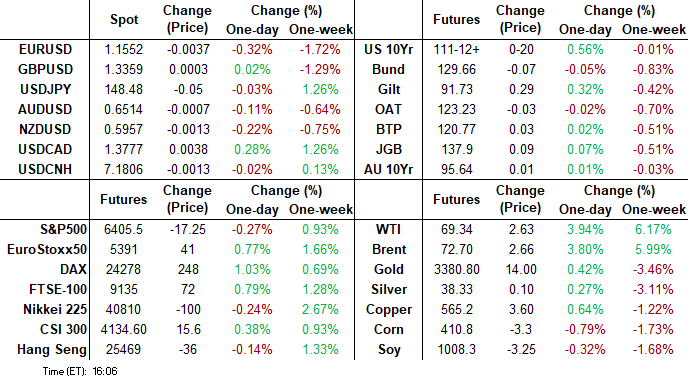

- Treasuries climbed to 1-week highs ahead Wednesday's FOMC rate announcement, curves bull flattening as projected rate cuts through year end remained muted.

- Less optimistic earnings from United Health and Merck coupled with uncertainty over US trade policy with the world contributed to indexes retreating from Monday's record highs.

- WTI crude rallied after President Trump gave Russia a 10-day deadline for an end to hostilities in Ukraine, adding to support from a US-EU trade deal.

- US and Chinese negotiators came to an agreement for an extension to the current deadline before reciprocal tariffs apply.

US TSYS

MNI US TSYS: Treasuries Bid Ahead FOMC, Strong 7Y Sale, JOLTS Jobs Recede

- Treasuries look to finish near late session highs, TYU futures back at last week's highs on July 22 as markets consolidate ahead of tomorrow's FOMC rate annc.

- A strong 7Y note auction helped rates extend highs after the $44B note sale (91282CNR8) stopped through again: 4.092% high yield vs. WI of 4.120%; bid-to-cover 2.79x from 2.46x prior. Peripheral stats: Indirect take-up retreats to 62.26% vs. 76.74% prior; Direct take-up climbed to new high at 33.68% vs. 11.62% prior; Dealers fell to new low of 4.06% vs. 11.64% prior.

- First half support: Tsys extended highs briefly after lower than expected JOLTS openings, quits level lower (prior down-revised), layoffs broadly lower than expected. Prior to JOLTS, little react to Advance Goods Trade Balance, import decline and less negative goods export. Wholesale inventories slightly higher than expected, retail inventories in-line.

- Tsy Sep'25 10Y contract trades +19 at 111-11.5 vs. 111-12.5 high; nearing initial technical resistance at 111-14.5 (High Jul 22). A clear break would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme.

- Curves bull flatten: 2s10s -3.051 at 44.734, 5s30s -3.148 at 95.557.

- Cross asset: Bbg US$ index firmer but off highs: BBDXY +1.65 at 1209.76 (1212.47 high); stocks moderately lower (SPX eminis -19.75 at 6403.0); gold firmer +9.30 at 3323.91.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.00), volume: $2.783T

- Broad General Collateral Rate (BGCR): 4.35% (+0.00), volume: $1.142T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.00), volume: $1.101T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation

RRP usage inches up to $171.018B this afternoon from $170.463B yesterday, total number of counterparties at 33. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported heavy SOFR & Treasury put volumes Tuesday - fading the bid in underlying futures firmer/near post-auction highs (TYU5 +19 at 111-11.5) ahead of Wednesday's FOMC annc. Projected rate cut pricing gain slightly vs. early morning (*) levels: Jul'25 at -0.5bp (-0.8bp), Sep'25 at -16.9bp (-16.6bp), Oct'25 at -29.1bp (-28.1bp), Dec'25 at -46bp (-44.4bp). Year end projection well off early July level of appr -65.0bp.

SOFR OPTIONS

+18,000 SFRZ5 95.68 puts, 1.25 ref 96.09

+8,000 SFRH6 95.68 puts, 2.0 ref 96.305

Block, 10,000 SFRF6 93.37/96.50/96.62/96.81 call condors 1.0 ref 96.305

Block, 5,000 SFRU5 95.68/95.75 2x1 put spds, 1.25 ref 95.845

-45,000 SFRU5 95.37.95.62.95.87 put flys, 8.75 vs. 95.83/0.46%

+10,000 SFRU5 95.62/95.68 2x1 put spds, 0.5 ref 95.84

+7,500 SFRF6 96.31/96.43/96.50/96.68 broken call condors, 0.5 ref 96.295

-5,000 SFRZ5 95.93/96.12 put spds, 10.25 ref 96.07/0.20%

-4,000 SFRZ5 95.81/96.50 strangles, 9.5

-1,500 SFRH6 96.25 straddles, 46.0

+4,000 SFRH6 96.50/97.00 call spds .375 over 2QH6 97.00/97.50 call spds

+2,500 SFRV5 96.06/96.12/96.25/96.31 call condors, 1.5

Block, 4,000 SFRQ5 95.68/95.75/95.81 put flys, 1.5

Block, +20,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 3.25 ref 96.075

Block, 5,000 SFRQ5 95.81/95.93/96.00 broken call flys, 3.75 ref 95.84

1,500 SFRZ5 95.25/95.62/95.75 broken put flys ref 96.075

9,200 SFRZ5 96.25/96.50/96.75/97.00 call condors ref 96.05

2,000 SFRZ5 96.25/0QZ5 97.18 call spds, 0.5

+10,300 SFRQ5 95.87/95.93 call spds, 1.25 vs. 95.835/0.15%

Block, 2,500 SFRV5 96.18/96.43 call spds, 4.75 ref 96.07

3,000 SFRU5 96.62/97.25 2x1 put spds, 6.5 ref 96.655

2,000 SFRH6 95.87/96.25 2x1 put spds over 96.87/97.12 call spds ref 96.28

9,000 SFRV5 96.25/96.31 put spds over 96.50/96.75 call spds, 3.5 net ref 96.07

+1,200 SFRU5 96.00/96.18, 1.0

1,250 SFRU5 95.68/95.75/95.81 put flys, 0.75 ref 95.835

+1,300 0QV5 96.31 puts, 3.0

Treasury Options

+50,000 wk5 TY Thursday 110.75 puts, 3 - expire 7/31 - day after FOMC

Block/screen, 23,000 TYU5 112.5 calls, 15

4,000 TYU5 110 puts, 11 ref 111-11.5 to -12

+20,000 FVU5 108 puts, 14

+20,000 TYU5 108.5 puts, 3

2,000 USU5 106.5/110 put spds ref 113-20

12,000 TUV5 104.12/104.37 call spds ref 103-25.62

+1,500 wk2 TY 107.75/108.75 put over risk reversals, 0.5 net

2,450 TYU5 112/113 call spds, 8 ref 110-25

1,000 TUU5 103.75/104.12 call spds, 4.5 vs. 103-18.87/0.20%

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Modestly Underperform Ahead Of HICP Data

Curve bellies underperformed Tuesday.

- Bund yields largely traded within Monday's ranges, with Gilt yields fading an early rise.

- Early core FI losses didn't appear to reflect any new news, instead continuing to trade on speculation regarding the weekend's EU-US trade pact (some details remain scarce despite the EU releasing a fact sheet).

- US Treasuries drove much of the afternoon's price action, with soft labour market data helping boost global core instruments before a modest sell-off going into the close.

- In data, UK consumer credit data and Spanish Q2 prelim GDP were stronger-than-expected, though had little market impact.

- The German curve lightly bear steepened, with the UK's leaning bull flatter - though the 5-7Y segments underperformed in both cases. Periphery/semi-core EGB spreads tightened modestly.

- Wednesday brings Eurozone Q2 GDP data, but focus will likely be more firmly placed on the first readings of flash July inflation starting with Spain (MNI's preview is here). Global attention will be on the Federal Reserve's decision (though after Wednesday's cash close).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.4bps at 1.942%, 5-Yr is up 2.6bps at 2.293%, 10-Yr is up 1.9bps at 2.708%, and 30-Yr is up 0.8bps at 3.204%.

- UK: The 2-Yr yield is down 1.2bps at 3.894%, 5-Yr is down 0.8bps at 4.067%, 10-Yr is down 1.4bps at 4.633%, and 30-Yr is down 1.3bps at 5.441%.

- Italian BTP spread down 0.7bps at 81bps / French OAT down 0.6bps at 65.6bps

MNI OPTIONS: Multiple Upside Plays In Rates Seen Tuesday

Tuesday's Europe rates/bond options flow included:

- RXU5 134c, bought for 2 in 4.5k

- ERZ5 98.37/98.50 call spread, bought for 1.0 in 30k. Traded vs 98.105 and 98.110

- ERH6 97.875/98.375/98.875 call fly sold out at 21 in 25.5k

- SFIU5 96.15/96.25/96.30c fly, bought for 1 in 8.88k

- SFIX5 96.60/96.70cs, bought for 0.75 in 5k

- SFIZ5 96.65/96.75cs, was bought earlier for 0.75 in 10k

- SFIH6 96.75/96.90cs, bought for 2.25 in 8.88k

- SFIM6 97.40/97.50cs, bought for 0.75 in 10k

MNI FOREX: Markets Build on USD Gains; EUR/JPY Sees Worst 2-day Return in Months

- Markets built on Monday's sharp dollar rally, tipping the greenback to a new monthly high in the process. The USD Index cleared 98.950 to print the best level since June 23rd as markets continue to absorb the details of the EU-US tariff agreement struck yesterday and the impending deadline for global reciprocal tariffs from Friday onwards.

- US and Chinese negotiators came to an agreement for an extension to the current deadline before reciprocal tariffs apply. The agreement still needs final approval from President Trump, however it does little to improve prospects of a trade deal in the very near-term.

- JPY traded well, prompting a second session of declines for EUR/JPY. The cross slipped well through Y172.00 as well as support seen into the mid-July lows of 171.37. Ishiba's leadership remains a key local focus. The governing LDP confirmed that its executive committee will call a General Assembly of members "in the near future". This could prove pivotal for the tenure of the PM, with markets pricing a more than likely chance that he will leave office before the end of the year. This raises the importance of the 171.53 20-day EMA for the near-term trend. A clear breach of this average would signal scope for a deeper correction and highlight potential for a move towards the 50-day EMA, at 168.89.

- Q2 Australian inflation data is the highlight of the Wednesday APAC session, and a cursory look at NZ developments given the high correlation between the two countries’ inflation rates suggests that Australia’s may also post a small decline. This result would still be above the RBA’s May Q2 forecast of 2.6%.

- The July Fed decision is also due. While markets see very little chance of a change in headline rates policy, much focus will be paid to any signals on the prospects of easing at the Fed ahead of year-end, particularly in the context of recent Trump criticism of Powell and his approach to policymaking.

MNI FX OPTIONS: Expiries for Jul30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E765mln), $1.1550(E902mln), $1.1700-10(E1.1bln), $1.1800(E1.7bln)

- USD/JPY: Y147.50($878mln), Y148.25-30($989mln), Y148.65($945mln), Y149.00($853mln)

- AUD/USD: $0.6550(A$1.0bln), $0.6600-10(A$1.2bln)

- USD/CAD: C$1.3695-10($969mln), C$1.3770-75($1.7bln)

MNI US STOCKS: Late Equities Roundup: Taking Profits/Position Squaring Pre-FOMC

- Stocks gave back modest early gains and are holding near session lows late Tuesday as investors took profits ahead of Wednesday's FOMC policy announcement. Less optimistic earnings from United Health and Merck coupled with uncertainty over US trade policy with the world contributed to indexes retreating from Monday's record highs in SPX eminis and Nasdaq.

- Currently, the DJIA trades down 181.77 points (-0.41%) at 44656.01, S&P E-Minis down 9.75 points (-0.15%) at 6412.25, Nasdaq down 35.3 points (-0.2%) at 21142.79.

- Leading decliners in the second half included: Carrier Global -11.04%, Brown & Brown -9.73%, VeriSign -9.49%, United Parcel Service -9.14%, PayPal Holdings -7.88%, Johnson Controls -7.17%, Stanley Black & Decker -7.10%, UnitedHealth Group -5.96%, Moderna -4.66% and Eli Lilly & Co -4.46%.

- On the positive side, IT, estate management and Financials led first half gainers: Corning +12.62%, Incyte +9.41%, Cadence Design Systems +9.02%, Synopsys +6.93%, Globe Life +5.88%, Welltower +4.71%, Advanced Micro Devices +3.47%, Cincinnati Financial +3.11% and Western Digital +2.79%.

- Expected earnings announcements after the close include: Booking Holdings, Mondelez International, Caesars Entertainment, PPG Industries, Visa Inc, Expand Energy, Teladoc Health, Avis Budget Group, Electronic Arts Inc, Starbucks, Seagate Technology and Teradyne Inc.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6457.75 High Jul 28

- PRICE: 6434.00 @ 07:16 BST Jul 29

- SUP 1: 6391.50/6313.51 Low Jul 24 / 20-day EMA

- SUP 2: 6241.00 Low Jul 16

- SUP 3: 6163.71 50-day EMA

- SUP 4: 6130.75 Low Jun 25

The trend set-up in S&P E-Minis is unchanged and remains bullish. Recent cycle highs confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6163.71. Support at the 20-day EMA is at 6313.51.

MNI AMERICAS OIL: WTI crude rallied after President Trump gave Russia a deadline

WTI crude rallied after President Trump gave Russia a 10-day deadline for an end to hostilities in Ukraine, adding to support from a US-EU trade deal. However, the market stopped short of a technical breakout. US-China negotiations are ongoing in Stockholm, with expectations of a 90-day extension to the tariff truce.

- Trump gave Russia a ceasefire deadline of 10 days after setting a 10-12 day timeframe yesterday. He appears to have lost patience with Russian President Putin saying he’s “not so interested in talking any more” after the latter has said one thing and done another.

- The OPEC-8 meeting on August 3 to decide its output target for September remains in focus after the JMMC yesterday ended with no policy recommendations.

- WTI Sep futures were up 3.8% at $69.21

- WTI Oct futures were up 3.6% at $68.31

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/07/2025 | 0530/0730 | *** | GDP (p) | |

| 30/07/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/07/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 30/07/2025 | 0700/0900 | *** | HICP (p) | |

| 30/07/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | ECB Wage Tracker | ||

| 30/07/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/07/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP | |

| 30/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 30/07/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/07/2025 | 1430/1030 | BOC press conference | ||

| 30/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 30/07/2025 | 1800/1400 | *** | FOMC Statement | |

| 31/07/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/07/2025 | 2350/0850 | ** | Industrial Production | |

| 31/07/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/07/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/07/2025 | 0130/1130 | * | Building Approvals | |

| 31/07/2025 | 0130/1130 | ** | Retail Trade | |

| 31/07/2025 | 0130/1130 | *** | Retail trade quarterly | |

| 31/07/2025 | 0130/1130 | ** | Trade price indexes | |

| 31/07/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |