EUROPEAN INFLATION: German CPI Details Suggest Ongoing But Slow Services Disinfl

Jun-13 08:43

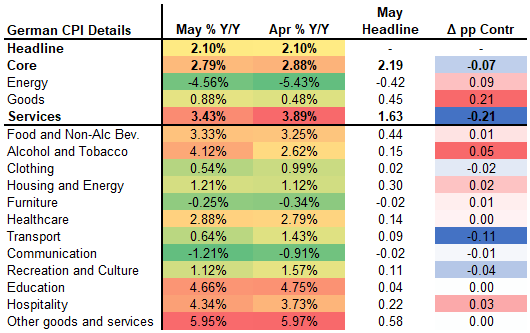

German final May HICP was unrevised from the flash readings at 2.1% Y/Y (2.2% prior) and 0.2% M/M. The final reading to CPI was also unrevised at 2.1% Y/Y (2.1% prior) and 0.1% M/M. Core CPI decelerated 0.1pp to 2.8% Y/Y, a rate not seen since January.

- Overall, the data confirms the main conclusions from the flash / state-level reading - services decelerated materially (contribution to headline -0.21pp vs prior on the back of the Easter effect unwind) while goods inflation accelerated (contribution +0.21pp vs prior) following firmer energy and alcohol / tobacco Y/Y rates (details see table).

- Abstracting from Easter-driven short-term trends, the contribution of services CPI to headline over the last two months combined excl. volatile travel-related categories (airfares, hotels, package holidays) is -0.03pp - suggesting an ongoing but slow underlying disinflation process in the category in Germany.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Support In Futures Holds

May-14 08:35

Gilts trade on the defensive over the last hour or so, perhaps in part owing setup for this morning’s 10-Year supply.

- Initial support in futures (91.43) holds on the first test.

- A break would deepen the bearish threat and expose the 76.4% retracement of the April 9 -May 2 rally (90.92).

- Yields now little changed on the day.

FOREX: FX OPTION EXPIRY

May-14 08:34

Of note:

AUDUSD 1.86bn at 0.6480/0.6500 (could act as magnet).

EURUSD 1.4bn at 1.1175 (a little far).

USDJPY 1.06bn at 147.00 (thu).

AUDUSD 1.32bn at 0.6475 (thu).

EURUSD 2.53bn at 1.1200 (fri).

- EURUSD: 1.1175 (1.4bn), 1.1200 (835mln).

- USDCAD: 1.3910 (366mln).

- AUDUSD: 0.6480 (945mln), 0.6500 (911mln).

- USDCNY: 7.2000 (758mln).

CROSS ASSET: UBS: CTAs Supporting Risk Rally, Wary Of Negative Duration Bias

May-14 08:30

UBS suggest that “CTAs have been supporting the rebound in risky assets”.

- Since their last update (April 28) UBS calculate that CTAs “have bought ~$30bln worth of global stocks, with a clear tilt towards DM indices”.

- UBS think that given “uninspiring price action and negative base effects (Q2-Q3 '24 rally falling out of the 1-Year rolling window), CTAs are about to turn negative duration again. We expect them to sell ~$50mln of bond DV01 over the next two weeks. All regions & tenors are likely to face selling pressure in the near term, with Korea 10s being the most at risk”.

- Elsewhere, they find that “in credit, CTAs have already covered their shorts, and are about to initiate new longs. The recent tightening, coupled with the elevated carry, make short positions difficult to sustain”.

- In FX, UBS believe that “CTAs continued to be heavy sellers of the USD in May (~$30bln). After aggressively buying G10 FX between February and April, their focus switched to EM FX this month. Going forward, we expect decent profit-taking in G10 FX, especially in JPY, and limited flows in EM FX”.

- Finally, for commodities, UBS point to “a little bit of agricultural selling this month, not much action elsewhere. CTAs remain heavily long gold and heavily short energy. We foresee some profit taking there”.