EUROPEAN INFLATION: ECB Data Suggests Broad Message of Jun Flash Release Intact

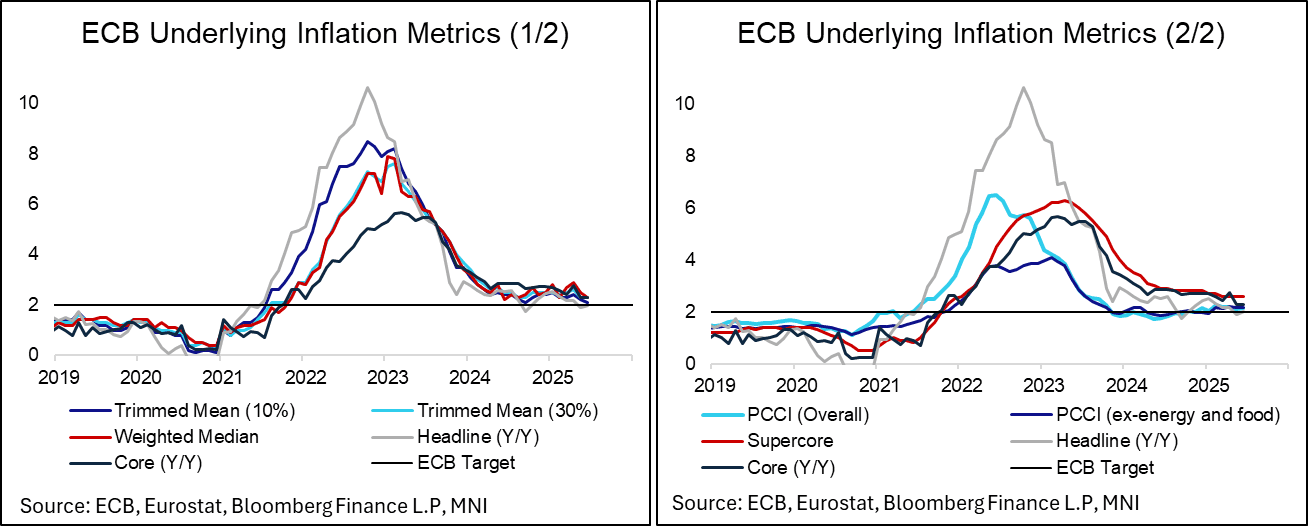

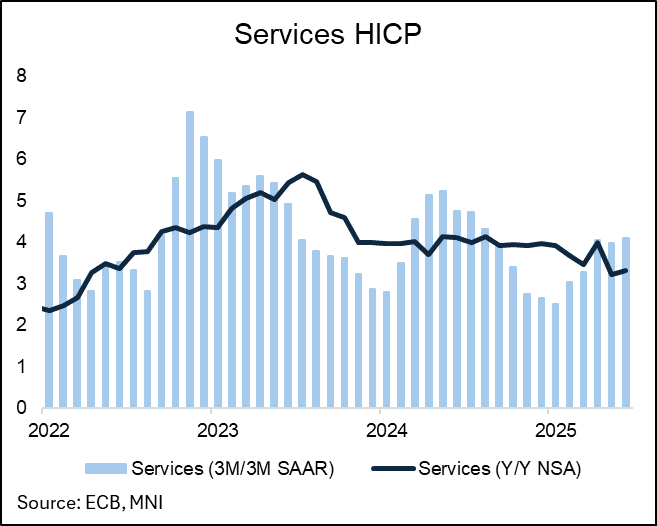

Taking into account the ECB’s underlying inflation metrics and updated ECB seasonally adjusted data, the broad message of the Eurozone June flash release remains unchanged: There remains some stickiness in underlying services inflation, but not enough to concern to the ECB at this stage.

- There was a modest uptick in the ECB’s preferred underlying inflation measure in June, with headline PCCI rising to 2.15% from 2.10% in May. However, PCCI remains below levels seen between February and April.

- Core PCCI was largely stable at 2.16% (vs 2.14% prior), while other underlying inflation metrics were either steady (supercore 2.6% Y/Y; 30% trimmed mean 2.3% Y/Y) or fell (10% trimmed mean 2.1% vs 2.2% prior; weighted median 2.3% vs 2,5% prior).

- Seasonally adjusted services inflation was revised slightly higher in the final release to 0.45% M/M (vs 0.41% flash, -0.14% prior). That meant a small upward revision in 3m/3m momentum to 4.10% (vs 4.07% flash, 3.98% prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA DATA: Biggest Foreign Divestment Of Canadian Bonds Since 2018

- Foreign investors sold Canadian CAD9.4B Canadian securities in April, including CAD25.1b of bonds that was the largest divestment since Dec 2018. Bond decline largely due to debt retirements.

- Canadian investors purchased CAD4.1B of foreign securities in April.

YTD foreign investment in Canadian securities from Jan to April -CAD15.1B vs +CAD64.3B over the same period last year.

STIR: Small Hawkish Fed Repricing As Ctrl Group Outweighs Headline Retail Sales

Initial dovish market readthrough from the softer-than-expected headline retail sales data & negative revisions is more than countered by the firmer-than-expected retail sales control group reading (and positive revision) and firmer-than-expected import prices (which will have been influenced by the weaker USD).

- That leaves Fed Funds pricing 0bp of cuts for this month, 3bp through July, 18bp through September, 31.5bp through October and 48bp through December.

- This compares to 0bp, 3.5bp, 19.5bp, 32.5bp and 49.5bp ahead of the release.

- SOFR implied terminal rate pricing (SFRZ6) stands at 3.30% vs. 3.29% ahead of the data. Contract sticks comfortably within the 3.165-3.500% implied rate range in play since May 9.

MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

- MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

- US REDBOOK: STORE SALES +5.2% WK ENDED JUN 14 V YR AGO WK