MNI ASIA OPEN: Strong 7Y Sale Gives Tsys Leg Up Ahead FOMC

EXECUTIVE SUMMARY

- MNI GLOBAL MACRO: Several Key Deals Still Outstanding

- MNI TARIFFS: Lutnick-Digital Services, Metals To Be On Table In Further EU Talks

- MNI JAPAN: LDP Confirms General Assembly That Could Decide PM Ishiba's Fate

- MNI US DATA: Consumer Confidence Off Lows, But Remains Weak Overall

- MNI US DATA: Hire Rates Extend Push Lower In A Net Dovish JOLTS Report

US

MNI GLOBAL MACRO: Several Key Deals Still Outstanding

Lutnick stated the US are not rushing to secure more trade deals ahead of Friday's deadline, and stressed Trump's openness to negotiating after the deadline passes. We make some tweaks to the latest list of still-outstanding key deals:

- Brazil: Communication ongoing; Alckmin & Lutnick negotiating, looking for delay

- Canada: Negotiations at an "intense phase"

- Chile: Expects copper tariff exception, officials in meetings today

- China: Stockholm talks pause for lunch; extension seems likely

- India: Preparing to face higher US tariffs of 20-25% temporarily, US delegation in mid-August. Expects deal by Sept/Oct

- Mexico: Aims for tariff agreement this week

- Norway: Tariff talks "still ongoing"

- Russian trade partners: Secondary tariffs could follow 10-12 day Ukraine ceasefire demand

- Singapore: US 'non-committal' on 10% tariff staying, rising or falling

- South Africa: Remains committed to solution, but is working on response plan

- South Korea: Proposes shipbuilding project, meeting with Bessent on July 31st

- UK: Not expecting steel deal during Trump's UK visit

- Global: Baseline RoW tariff will be 15-20%

NEWS

MNI TARIFFS: Lutnick-Digital Services, Metals To Be On Table In Further EU Talks

US Commerce Secretary Howard Lutnick, speaking to CNBC, talks on trade but offers little in the way of signals on the prospect of an agreement with China (talks currently taking place in Stockholm) or more details on the EU agreement. Regarding EU trade, in the wake of the deal announced over the weekend, Lutnick says he expects talks to continue. Says digital services as well as steel and aluminium will be on the table. Says that President Donald Trump "accepts that natural resources won't face tariffs".

MNI TARIFFS: India Braces for Higher US Tariffs But Eyes Broader Trade Deal: RTRS

India is preparing to face higher U.S. tariffs - likely between 20% and 25% - on some of its exports as a temporary measure, Reuters report citing sources.

MNI MACRO OUTLOOK: IMF Increases US and China Growth F'casts, But Risks To Downside

The International Monetary Fund on Tuesday boosted U.S. and China growth forecasts, citing a de-escalation of tariffs and increased fiscal stimulus while warning global growth is at risk because of trade disputes.

MNI JAPAN: LDP Confirms General Assembly That Could Decide PM Ishiba's Fate

The governing Liberal Democratic Party (LDP) confirmed on 29 July that its executive committee will call a General Assembly of LDP members of the National Diet 'in the near future'. This could prove pivotal for the tenure of PM Shigeru Ishiba following the disastrous performance of the LDP in the 20 July House of Councillors election. The executive committee's confirmation of the General Assembly meeting follows a 'roundtable discussion' of LDP lawmakers on 28 July.

MNI UKRAINE: EP-EU Pauses Aid Over Anti-Corruption Agency Row

Business and economics-focused Ukrainian outlet Ekonomichna Pravda reports that the EU has reduced its aid payments to Ukraine because of Kyiv's failure to hit its agreed milestones with regards to anti-corruption efforts. In the short term, it has also paused all aid due to President Volodymyr Zelenskyy's (now swiftly reversed) plans to strip two anti-corruption agencies of their powers.

MNI ISRAEL: Cabinet Could Meet Again Thurs As Pressure Mounts On PM For Gaza Truce

Amichai Stein at I24 posts on X: "After the limited cabinet discussion that addressed options in the war in Gaza, two things are currently being awaited: A. Perhaps Hamas will nonetheless soften its response. B. [Minister of Strategic Affairs Ron] Dermer and [National Security Advisor Tzachi] Hanegbi's talks in Washington. There is an expectation for a cabinet meeting this week, which might convene on Thursday."

US TSYS

MNI US TSYS: Treasuries Bid Ahead FOMC, Strong 7Y Sale, JOLTS Jobs Recede

- Treasuries look to finish near late session highs, TYU futures back at last week's highs on July 22 as markets consolidate ahead of tomorrow's FOMC rate annc.

- A strong 7Y note auction helped rates extend highs after the $44B note sale (91282CNR8) stopped through again: 4.092% high yield vs. WI of 4.120%; bid-to-cover 2.79x from 2.46x prior. Peripheral stats: Indirect take-up retreats to 62.26% vs. 76.74% prior; Direct take-up climbed to new high at 33.68% vs. 11.62% prior; Dealers fell to new low of 4.06% vs. 11.64% prior.

- First half support: Tsys extended highs briefly after lower than expected JOLTS openings, quits level lower (prior down-revised), layoffs broadly lower than expected. Prior to JOLTS, little react to Advance Goods Trade Balance, import decline and less negative goods export. Wholesale inventories slightly higher than expected, retail inventories in-line.

- Tsy Sep'25 10Y contract trades +19 at 111-11.5 vs. 111-12.5 high; nearing initial technical resistance at 111-14.5 (High Jul 22). A clear break would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme.

- Curves bull flatten: 2s10s -3.051 at 44.734, 5s30s -3.148 at 95.557.

- Cross asset: Bbg US$ index firmer but off highs: BBDXY +1.65 at 1209.76 (1212.47 high); stocks moderately lower (SPX eminis -19.75 at 6403.0); gold firmer +9.30 at 3323.91.

OVERNIGHT DATA

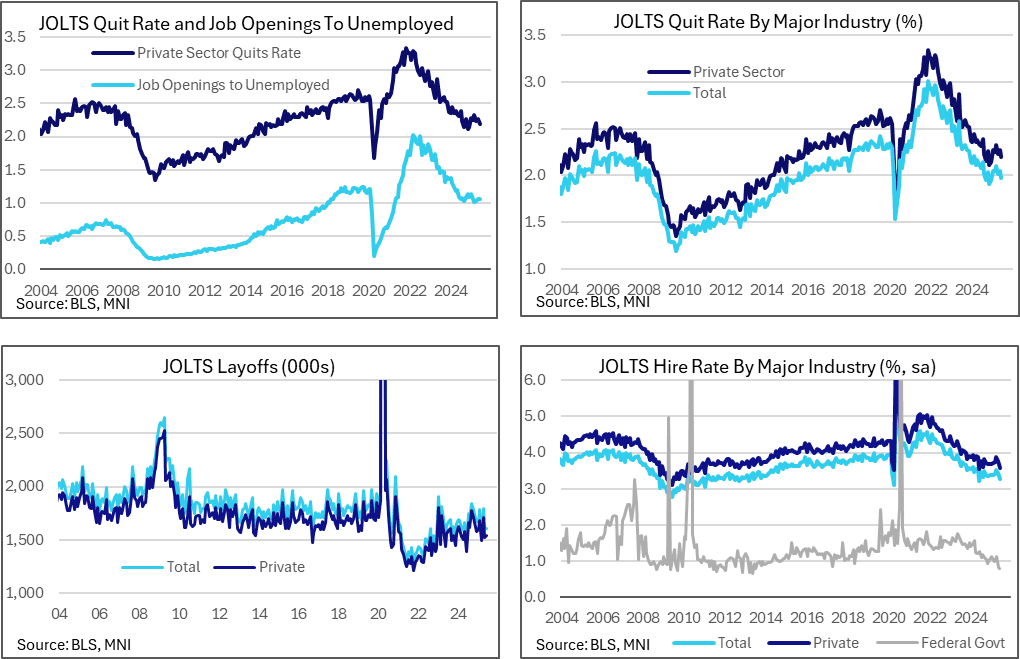

MNI US DATA: Hire Rates Extend Push Lower In A Net Dovish JOLTS Report

The JOLTS report for June was soft across the board. The ratio of openings to unemployed continued to show signs of stabilization rather than deterioration, broadly holding levels seen for the past year, but hire rates in particular cooled further. The latter leaves greater susceptibility to any slowdown in economic activity.

- Job openings were a little lower than expected in June at 7437k (sa, cons 7,500k) after an unrevised 7769k in May. The quit rate eased to 1.97% from a marginally downward revised 2.049% that was exacerbated by rounding having initially reported at 2.06%.

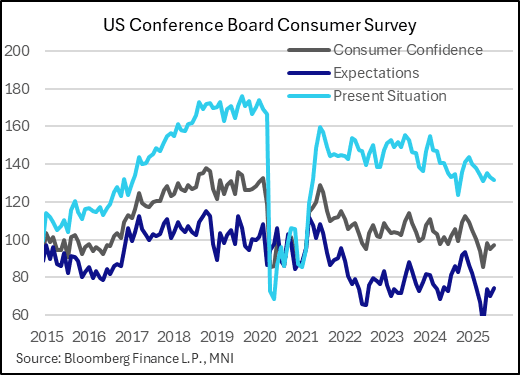

MNI US DATA: Consumer Confidence Off Lows, But Remains Weak Overall

The Conference Board's consumer confidence survey showed a notable improvement in sentiment in July, with the headline reading rising to 97.2 (96.0) from 95.2 prior (rev up from 93.0). The Present Situation reading dipped to 131.5 from an upwardly revised 133.0 in Jun (129.1 pre-rev), but Expectations improved to 74.4 from 69.9 (rev from 69.0). The report notes "all three components of the Expectation Index improved, with consumers feeling less pessimistic about future business conditions and employment, and more optimistic about future income."

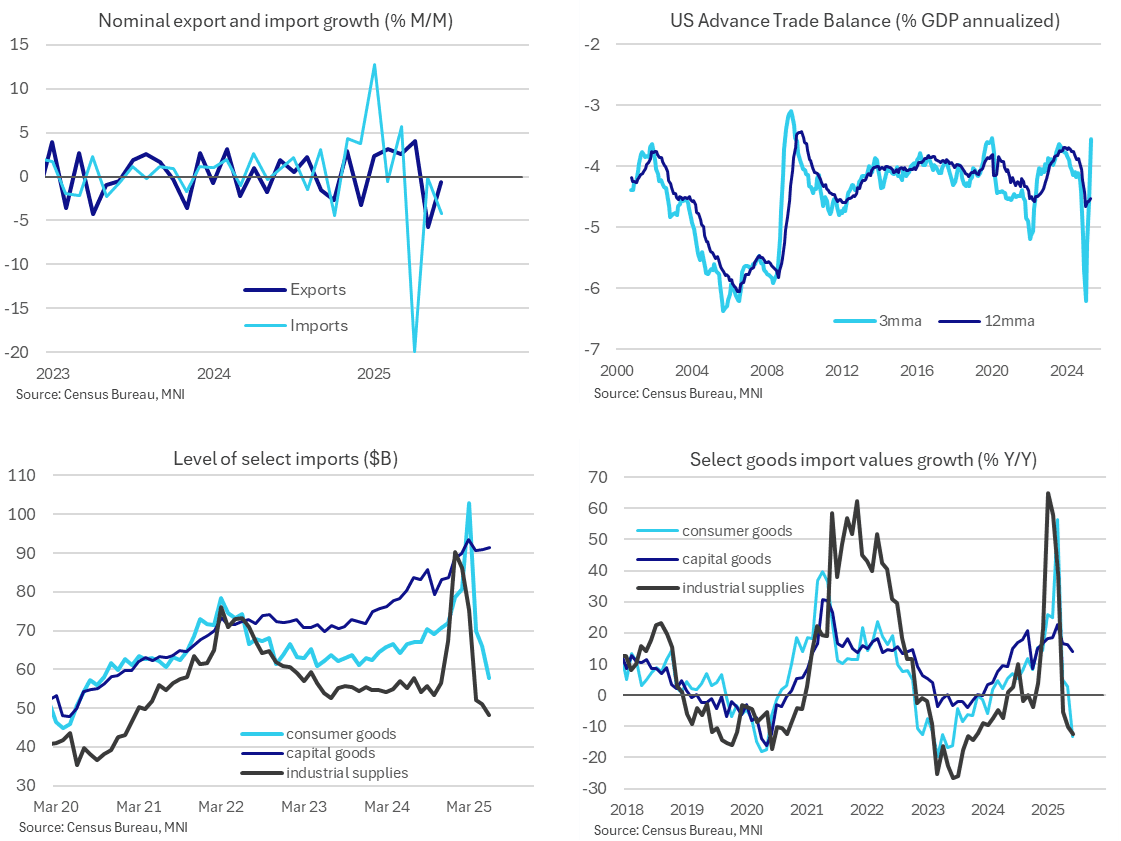

MNI US DATA: Capital Goods Imports Continue Protectionist Boost

The goods trade deficit was smaller than expected in June at $86bn (cons $98bn) after $96.6bn in May. It appears to be further payback from the huge deficits of Dec and Q1 driven by tariff front-running, primarily gold and then pharmaceutical products.

MNI US OUTLOOK/OPINION: Final GDPNow Estimate Picks Up, But Weaker Domestic Demand

The Atlanta Fed's final GDPNow estimate for Q2 GDP has risen to 2.9% from the prior 2.4% estimate made last week, due entirely to today's trade data which showed a smaller-than-expected goods trade deficit for June. This estimate is above the 2.5% currently seen by Bloomberg consensus for Wednesday's official GDP release.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 204.57 points (-0.46%) at 44632.99

S&P E-Mini Future down 17.5 points (-0.27%) at 6405.5

Nasdaq down 80.3 points (-0.4%) at 21098.29

US 10-Yr yield is down 8.9 bps at 4.3204%

US Sep 10-Yr futures are up 20/32 at 111-12.5

EURUSD down 0.0037 (-0.32%) at 1.1552

USDJPY down 0.05 (-0.03%) at 148.48

WTI Crude Oil (front-month) up $2.65 (3.97%) at $69.34

Gold is up $10.8 (0.33%) at $3325.46

European bourses closing levels:

EuroStoxx 50 up 41.62 points (0.78%) at 5379.2

FTSE 100 up 54.88 points (0.6%) at 9136.32

German DAX up 247.01 points (1.03%) at 24217.37

French CAC 40 up 56.48 points (0.72%) at 7857.36

US TREASURY FUTURES CLOSE

3M10Y -9.772, -3.08 (L: -3.08 / H: 5.888)

2Y10Y -3.045, 44.74 (L: 44.112 / H: 49.567)

2Y30Y -4.113, 98.437 (L: 97.71 / H: 104.254)

5Y30Y -3.076, 95.629 (L: 94.875 / H: 99.219)

Current futures levels:

Sep 2-Yr futures up 3/32 at 103-21 (L: 103-17.5 / H: 103-21)

Sep 5-Yr futures up 10.5/32 at 108-15 (L: 108-04 / H: 108-15)

Sep 10-Yr futures up 20/32 at 111-12.5 (L: 110-24 / H: 111-13)

Sep 30-Yr futures up 47/32 at 114-20 (L: 113-03 / H: 114-22)

Sep Ultra futures up 65/32 at 117-25 (L: 115-22 / H: 117-26)

MNI US 10YR FUTURE TECHS: (U5) Remains Above Support

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-28 High Jul 3

- RES 1: 111-14+ High Jul 22

- PRICE: 110-10+ @ 1430ET Jul 29

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures are unchanged and remain above last week’s low. Recent gains resulted in a break of the 20-day EMA, strengthening the recovery. Note too that resistance at 111-13+, Jul 10 high, has been pierced. A clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low.

SOFR FUTURES CLOSE

Sep 25 +0.015 at 95.850

Dec 25 +0.025 at 96.10

Mar 26 +0.040 at 96.330

Jun 26 +0.050 at 96.555

Red Pack (Sep 26-Jun 27) +0.060 to +0.080

Green Pack (Sep 27-Jun 28) +0.080 to +0.085

Blue Pack (Sep 28-Jun 29) +0.080 to +0.095

Gold Pack (Sep 29-Jun 30) +0.095 to +0.105

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.00), volume: $2.783T

- Broad General Collateral Rate (BGCR): 4.35% (+0.00), volume: $1.142T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.00), volume: $1.101T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation

RRP usage inches up to $171.018B this afternoon from $170.463B yesterday, total number of counterparties at 33. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

MNI PIPELINE: Corporate Bond Update: $750M EW Scrips 5NC2 Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/29 $2B #NextEra Energy 2Y +63

- 07/29 $1.5B #Sherwin Williams $500M each: 3Y +47, 5Y +62, 10Y +82

- 07/29 $750M #EW Scripps 5NC2 9.875%

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Modestly Underperform Ahead Of HICP Data

Curve bellies underperformed Tuesday.

- Bund yields largely traded within Monday's ranges, with Gilt yields fading an early rise.

- Early core FI losses didn't appear to reflect any new news, instead continuing to trade on speculation regarding the weekend's EU-US trade pact (some details remain scarce despite the EU releasing a fact sheet).

- US Treasuries drove much of the afternoon's price action, with soft labour market data helping boost global core instruments before a modest sell-off going into the close.

- In data, UK consumer credit data and Spanish Q2 prelim GDP were stronger-than-expected, though had little market impact.

- The German curve lightly bear steepened, with the UK's leaning bull flatter - though the 5-7Y segments underperformed in both cases. Periphery/semi-core EGB spreads tightened modestly.

- Wednesday brings Eurozone Q2 GDP data, but focus will likely be more firmly placed on the first readings of flash July inflation starting with Spain (MNI's preview is here). Global attention will be on the Federal Reserve's decision (though after Wednesday's cash close).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.4bps at 1.942%, 5-Yr is up 2.6bps at 2.293%, 10-Yr is up 1.9bps at 2.708%, and 30-Yr is up 0.8bps at 3.204%.

- UK: The 2-Yr yield is down 1.2bps at 3.894%, 5-Yr is down 0.8bps at 4.067%, 10-Yr is down 1.4bps at 4.633%, and 30-Yr is down 1.3bps at 5.441%.

- Italian BTP spread down 0.7bps at 81bps / French OAT down 0.6bps at 65.6bps

MNI FOREX: Markets Build on USD Gains; EUR/JPY Sees Worst 2-day Return in Months

- Markets built on Monday's sharp dollar rally, tipping the greenback to a new monthly high in the process. The USD Index cleared 98.950 to print the best level since June 23rd as markets continue to absorb the details of the EU-US tariff agreement struck yesterday and the impending deadline for global reciprocal tariffs from Friday onwards.

- US and Chinese negotiators came to an agreement for an extension to the current deadline before reciprocal tariffs apply. The agreement still needs final approval from President Trump, however it does little to improve prospects of a trade deal in the very near-term.

- JPY traded well, prompting a second session of declines for EUR/JPY. The cross slipped well through Y172.00 as well as support seen into the mid-July lows of 171.37. Ishiba's leadership remains a key local focus. The governing LDP confirmed that its executive committee will call a General Assembly of members "in the near future". This could prove pivotal for the tenure of the PM, with markets pricing a more than likely chance that he will leave office before the end of the year. This raises the importance of the 171.53 20-day EMA for the near-term trend. A clear breach of this average would signal scope for a deeper correction and highlight potential for a move towards the 50-day EMA, at 168.89.

- Q2 Australian inflation data is the highlight of the Wednesday APAC session, and a cursory look at NZ developments given the high correlation between the two countries’ inflation rates suggests that Australia’s may also post a small decline. This result would still be above the RBA’s May Q2 forecast of 2.6%.

- The July Fed decision is also due. While markets see very little chance of a change in headline rates policy, much focus will be paid to any signals on the prospects of easing at the Fed ahead of year-end, particularly in the context of recent Trump criticism of Powell and his approach to policymaking.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/07/2025 | 0530/0730 | *** | GDP (p) | |

| 30/07/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/07/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 30/07/2025 | 0700/0900 | *** | HICP (p) | |

| 30/07/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | ECB Wage Tracker | ||

| 30/07/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/07/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP | |

| 30/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 30/07/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/07/2025 | 1430/1030 | BOC press conference | ||

| 30/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 30/07/2025 | 1800/1400 | *** | FOMC Statement | |

| 31/07/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/07/2025 | 2350/0850 | ** | Industrial Production | |

| 31/07/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/07/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/07/2025 | 0130/1130 | * | Building Approvals | |

| 31/07/2025 | 0130/1130 | ** | Retail Trade | |

| 31/07/2025 | 0130/1130 | *** | Retail trade quarterly | |

| 31/07/2025 | 0130/1130 | ** | Trade price indexes | |

| 31/07/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |