MNI US OPEN - House Rejects Trump’s Tariffs on Canada

EXECUTIVE SUMMARY

- PENTAGON PREPARES SECOND AIRCRAFT CARRIER TO DEPLOY TO THE MIDDLE EAST: WSJ

- TRUMP REBUKED OVER CANADA TARIFFS AS MIDTERM ANXIETIES GROW: BBG

- JAPAN’S FX CHIEF SAYS NOT LOWERING GUARD AT ALL AFTER YEN GAINS

- UK GDP DOWNSIDE RISKS REALISED; BUT LITTLE IMPACT LIKELY FOR MPC

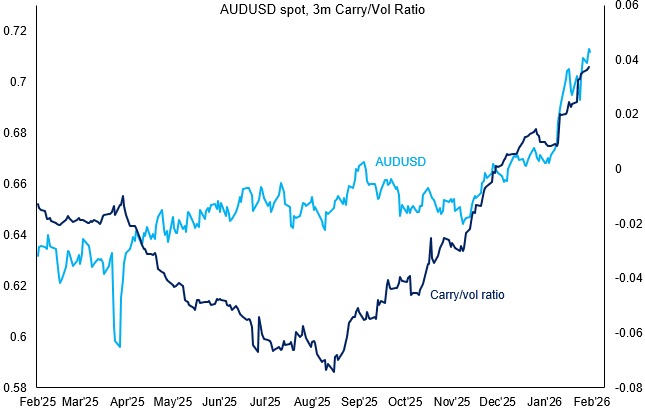

Figure 1: AUD/USD strength follows lead of rising carry/vol profile

Source: MNI / Bloomberg Finance L.P.

NEWS

US/MIDEAST (WSJ): Pentagon Prepares Second Aircraft Carrier to Deploy to the Middle East

President Trump said Tuesday that he was weighing sending a second carrier to the Middle East to prepare for military action if negotiations with Iran failed. The order to deploy could be issued in a matter of hours, one of the officials said. The officials cautioned that Trump hadn’t yet given an official order to deploy the second carrier, and that plans could change. The carrier would join aircraft carrier USS Abraham Lincoln that is already in the region. One of the officials said the Pentagon was readying a carrier to deploy in two weeks, likely from the U.S. East Coast. The aircraft carrier USS George H.W. Bush is completing a series of training exercises off the coast of Virginia, and it could potentially expedite those exercises, officials say.

US (BBG): Trump Rebuked Over Canada Tariffs as Midterm Anxieties Grow

Donald Trump’s tariff policies suffered their strongest political blow yet with the Republican-led US House passing legislation aimed at ending the president’s levies on Canadian imports. Wednesday’s vote represents an increase in political pressure to change course on Trump’s signature economic policy just months before the midterm elections, including by forcing swing-district Republicans affected by the tariffs to weigh when or if to cross the president by voting against his agenda. The vote also signals a growing anxiety over the White House’s economic agenda before elections that are expected to focus heavily on affordability.

US (Semafor): Republicans Suggest Senate, Not Justice Department, Investigate Powell

In a closed-door meeting with Senate Republicans Wednesday, Treasury Secretary Scott Bessent agreed with lawmakers who suggested the Senate Banking Committee could investigate Federal Reserve Chair Jerome Powell, instead of the Justice Department, people in the room told Semafor. One of the sources, a lawmaker, said they interpreted the exchange as “testing the waters” to see if the arrangement could get Sen. Thom Tillis, R-N.C., to lift his blockade on Fed nominees.

US (NBC News): Trump Administration Working to Expand Effort to Strip Citizenship From Foreign-Born Americans

The Trump administration is dramatically expanding an effort to revoke U.S. citizenship for foreign-born Americans as it works to curb immigration, according to two people familiar with the plans. Over the past several months, U.S. Citizenship and Immigration Services, the agency within the Department of Homeland Security that’s responsible for legal immigration, has been sending experts to its offices around the country or reassigning staff members to focus on whether some citizens processed through those offices could now be denaturalized, these people said.

US/INDIA (MNI): US Softens India Trade Agreement Amid Farm Protests

Indian Trade Minister Piyush Goyal told reporters that 90-95% of Indian farm products have been kept out of the pending US-India trade deal amid major nationwide protests today, per Reuters. Earlier, Goyal said negotiators are working to finalise and sign before the end of March. Goyal's comments come amid uncertainty over the final shape of the agreement, announced by US President Donald Trump on February 2. This week, a claim in a White House fact sheet that India "commits" to buy over USD$500 billion worth of US products has been softened to "intends to buy." The fact sheet now omits the term "agricultural" from the list of product categories covered by the pledge, and pulses, a critical agricultural product for Indian farmers, have been excluded entirely.

US/CHINA (MNI): China and U.S. Trade Teams Maintaining Communication

MNI (Beijing) China and the United States continue to maintain “close communication at various levels” through their economic and trade teams, Ministry of Commerce spokesperson He Yadong said on Thursday. He's remarks were in response to reporters’ questions about recent remarks by U.S. Treasury Secretary Scott Bessent, who stated that a working-level meeting was held in Beijing last week to prepare for talks with Vice Premier He Lifeng, ahead of an anticipated leaders’ meeting in April.

EU/CHINA (MNI): China Levies Countervailing Duties on EU Dairy

MNI (Beijing) China will impose a countervailing duty on EU dairy products, a Ministry of Commerce spokesperson said on Thursday. Effective from Feb 13, countervailing duty will be imposed for five years, at rates between 7.4% and 11.7%, the spokesperson said. Chinese authorities have made a final determination that imported dairy products from the EU are subsidised, and that China's dairy industry has in consequence suffered "material injury,” the Ministry stated.

EU (MNI): Macron & Merz Look to Downplay Rift on EU Preference at Leaders' Summit

Speaking alongside German Chancellor Friedrich Merz following a bilateral discussion on the sidelines of the informal meeting of EU leaders taking place in Belgium presently, French President Emmanuel Macron said that he shares Merz's "feeling of urgency" with regard to making the EU more competitive. Says "We must go quickly...We must have very concrete decisions by June, regarding how to make Europe more competitive." Politico reports "While agreeing on the need to cut red tape and diversify trade partners, France and Germany have been at odds on the rest of the bloc's economic agenda over the past days, from eurobonds to the definition of new "Made in Europe" measures." This chimes with reporting from MNI's Policy team earlier in the week.

ECB (BBG): Makhlouf Says Next ECB Move Could Be Interest-Rate Cut or Hike

European Central Bank Governing Council member Gabriel Makhlouf said policymakers’ next move could be to raise or lower borrowing costs. “I’m not ruling out further reductions, I’m not ruling out actually the possibility that interest rates could also go up,” the Irish central bank chief told Shannonside radio in an interview on Thursday. “What I’m saying is that at the moment it does look as if inflation is on track to deliver our target so we’re in a good place.”

UK (MNI): Brief Respite for PM as Parliament Enters Recess

At the end of today's sitting, the House of Commons goes on recess until 23 February. While this may provide a brief respite for PM Sir Keir Starmer, following an ill-tempered session of PMQs on 11 Feb, the speculation surrounding his knowledge or lack thereof of his former director of communications' links with a convicted sex offender before nominating him for a position in the House of Lords is unlikely to blow over any time soon. Political predictions market have noted something of a calming of the waters (at least in the short term). Data from Polymarket gives a 39% implied probability that Starmer is out of 10 Downing Street by 30 June. While this is much higher than the 22% recorded on 4 Feb, before the Mandelson-Epstein scandal broke, it is a sharp decline from the peak of 69% recorded on 9 Feb when Scottish Labour leader Anas Sarwar made his public call for the PM to step down.

JAPAN (BBG): Japan’s FX Chief Says Not Lowering Guard at All After Yen Gains

Japan’s top currency official said the government remains on high alert over foreign exchange movements in a week that’s seen gains in the Japanese currency. “We have not lowered our guard at all,” Atsushi Mimura, vice finance minister for international affairs, told reporters in Tokyo Thursday morning. “There’s been a lot of talk about yesterday’s jobs data and the market moves that followed, including speculation about whether there were rate checks and so on,” Mimura said, adding that he would not comment on such matters.

BOJ (MNI EXCLUSIVE): BOJ to Assess March Hike on Strong Market View

MNI discusses the BOJ's appetite for a March hike. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI EXCLUSIVE): China Gold Demand Robust, Despite Volatility

Local analysts provide insight into China's gold demand. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): PBOC Unveils CNY1 Trillion Outright Reverse Repo

MNI (Beijing) The People's Bank of China will conduct a CNY1 trillion outright reverse repo operation on Feb 13, according to a statement on its website on Thursday. With a term of six months, the operation will use a fixed-quantity, rate-bidding, multiple-price winning method, the statement said. It will be the largest monthly iteration of its six-month outright reverse repo since the Bank started the operation last October. The Bank operated a CNY800 billion three-month outright reverse repo early this month, which means it will inject as much as CNY1.8 trillion of liquidity through outright reverse repos in February.

RBA (MNI): RBA's Bullock Sees NAIRU at 4.6%

Reserve Bank of Australia has lifted its NAIRU estimate by around 10 basis points to 4.6%, Governor Michele Bullock told a Senate estimates hearing Thursday. "Our models' estimate of NAIRU have risen a bit, but we don't take a model approach only, we also use a bit of judgment," she said, noting the most recent set of forecasts showed how the Bank considered full employment. Her comments follow the Board’s decision last week to raise the cash rate 25bp to 3.85% and updated forecasts showing higher inflation and weaker potential growth.

ARGENTINA (BBG): Argentina Senators Pass Milei’s Labor Reform in Key First Step

Senators in Argentina passed President Javier Milei’s signature labor reform bill early Thursday, a key step forward for the libertarian’s ambitious agenda that could support his government’s return to international markets. In a 42-30 general vote, the Senate approved the sweeping bill, sending it to lower house for debate. Milei’s administration made 28 concessions Tuesday to win additional support from lawmakers and provincial governors. Among the changes, his administration removed an article that would have lowered employers’ income taxes because it would have reduced provincial revenue.

DATA

UK DATA (MNI): GDP Downside Risk Crystallised; Little Impact Likely for MPC

- UK DEC GDP +0.1% M/M, +0.1% 3M/3M, +1.0% 3M Y/Y

- UK DEC SERVICES INDEX +0.3% M/M, +0.0% 3M/3M

- UK DEC CONSTRUCTION OUTPUT -2.1% 3M/3M, +0.2% 3M Y/Y

- UK DEC IND PROD -0.9% M/M, +0.5% Y/Y

- UK DEC MANUF OUTPUT -0.5% M/M, +0.5% Y/Y

The downside risks to GDP that we highlighted were crystalised this morning with Q/Q GDP coming in at 0.1% Q/Q (lower than the 0.2% consensus and BOE forecast). It was a softer 0.1% too, with the unrounded at 0.06% Q/Q. Monthly GDP was in line with expectations, but there was a downside revision to November. Services was revised 0.2ppt lower in November (and the 0.2ppt upside surprise in December was not enough to quite offset this on the quarter). Industrial production was also soft in December. We don't think this will have much impact on the MPC. Voters are much more concerned about forward-looking growth prospects rather than backward looking data like this. On the margin it probably helps a little as it removes the possibility of a high print causing a headache, but next week's CPI and labour market data, as well as growth indicators such as the PMIs are much more important.

SWEDEN DATA (MNI): Mixed January PES Labour Market Data, Won't Change Riksbank Outlook

Public Employment Service data for January was a little mixed, but doesn't materially push back on Riksbank expectations for a stronger labour market this year. Although the unemployment claims rate remains on a downward trend, there was a fall in vacancies and a small rise in redundancy notices. The unemployment claims rate fell to a two-year low of 6.6%, now down from 7.1% in the middle of last year. This is expected to translate into a lower LFS unemployment rate in the coming months. The Riksbank projects the LFS rate to fall to 8.4% by December 2026 (vs 9.1% 3mma at present).

JAPAN DATA (MNI): Jan CGPI Rises 2.3% Y/Y; Import Price Rises

- JAPAN JAN CORP GOODS PRICE INDEX +2.3% Y/Y; DEC +2.4%

- JAPAN JAN CORP GOODS PRICE INDEX +0.2% M/M; DEC +0.1%

Japan's corporate goods price index rose 2.3% y/y in January, easing from 2.4% in December, while import prices increased for a second straight month, Bank of Japan data showed Thursday. The annual CGPI gain was driven lower by beverages and food (+4.7% vs. +4.8%) and petroleum and coal products (-12.9% vs. -8.3%), but partly offset by stronger nonferrous metals (+33.0% vs. +22.2%). The index rose 0.2% m/m, marking a fifth consecutive increase after a revised 0.1% rise in December.

FOREX: Bear Trigger Halts USDJPY Decline, For Now

- Given the magnitude of the moves since Sunday’s vote in Japan, it is perhaps unsurprising to see USDJPY generate some demand in the low 152’s, with the 3.5% decline in just four sessions falling just shy of 152.10 support, and the technical bear trigger. A solid turnaround from the 152.27 lows prompted a 153.55 session high just ahead of the European open, with the pair subsequently consolidating around the 153 mark. If the price action following yesterday’s US employment report is anything to go by, the pair’s inability to consolidate any meaningful upward momentum could be a sign that further downside is imminent.

- While moderately lower on the session, AUD extended its bullish cycle overnight, with 0.7147 coming within 11pips of the 2023 peak. “The overall picture of [labour market] persistent tightness is important because it is consistent with there still being some inflationary pressure in the economy”, RBA's Hunter said overnight. A renewed push higher for AUDUSD would put sights on 0.7208, a Fibonacci projection.

- Swiss Franc resilience has resumed today, with EURCHF seeing a renewed push back towards 0.9125. USDCHF also edges closer to cycle lows which are located 0.7605, with participants awaiting inflation data from both Switzerland and the US on Friday.

- In emerging markets, EURHUF briefly extended an intraday rally to 0.5%, with weakness for the forint stemming initially from the below-expectations CPI print and then from an EU Court opinion on frozen funds. We flag key short-term resistance at 383.04, the 50-day EMA.

- Today's US data calendar is rather light, with weekly claims and home sales scheduled. Fed's Logan and Miran are set to appear, while a set of ECB speakers is unlikely to move the needle.

EGBS: Tight Range for Bunds in Subdued Trading Session

It’s been a subdued session for global core FI markets, with Bunds trading in a tight 14 tick range on lower-than-average volumes. Markets have digested yesterday’s US labour market report, and are now waiting for tomorrow’s CPI report to assess the likely direction of Fed policy. Eurozone cues have been lacking this week, and tomorrow’s second Q4 GDP reading is unlikely to provide a meaningful impulse to EUR rates.

- Bund futures are +6 ticks at 128.73. A bull mode in Bund futures remains intact and the contract is holding on to its recent gains. The breach of 128.58, the Jan 19 high and a key short-term resistance, strengthens the short-term condition. This signals scope for an extension towards 128.89, a Fibonacci retracement.

- 10-year German yields are attempting once again to consolidate below the 2.80% figure, currently little changed on the session at 2.795%.

- Italian 3/7-year BTP supply was well digested. 10-year EGB spreads to Bunds are biased a little narrower, with the BTP/Bund spread 1bp narrower at 59.5bps.

- ECB’s Makhlouf continued to provide balanced rhetoric, noting that he was not ruling out a cut or hike to ECB rates.

GILTS: Risks to Bears Increases, Little Impact From Soft GDP

Gilts have firmed as European equity benchmarks edge away from highs, but the move has stalled.

- There was no lasting net impact from the softer-than-expected Q4 GDP data.

- Futures topped out at 91.30, last +19 at 91.22.

- The 20-day EMA was breached yesterday, increasing the risk to the bearish technical theme. Next resistance of note located at the Jan 22 high (92.13), as the contract extends the bounce from cycle lows. Fibonacci resistance (91.73) provides some intermediate interest.

- Yields flat to -1.5bp, curve flatter.

- A reminder that we had flagged downside risks to the GDP release ahead of time.

- BoE-dated OIS flat to 1bp more dovish through year-end, pricing 17.5bp of cuts for March, 23bp through April, 32bp through June and 45.5bp through November. Markets remain unwilling to fully discount 50bp of cuts at this stage, with political & fiscal risks probably providing some limit.

- We don't think this morning’s data will have much impact on the MPC. Voters are much more concerned about forward-looking growth prospects rather than backward looking data like this. On the margin it probably helps a little as it removes the possibility of a high print causing a headache, but next week's CPI and labour market data, as well as growth indicators such as the PMIs are much more important.

- Little of note on the UK calendar for the remainder of the day.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.551 | -17.6 |

Apr-26 | 3.498 | -22.9 |

Jun-26 | 3.410 | -31.7 |

Jul-26 | 3.344 | -38.3 |

Sep-26 | 3.311 | -41.6 |

Nov-26 | 3.272 | -45.5 |

Dec-26 | 3.275 | -45.2 |

EQUITIES: 6100 Handle Provides Next Resistance for EuroStoxx 50 Futures

The medium-term trend condition in EuroStoxx 50 futures remains bullish and this week’s fresh cycle high reinforces the bull theme. The move higher paves the way for an extension towards 6100.00, and 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5896.83. Clearance of this average would highlight a short-term top and signal scope for a deeper pullback. The firm reversal higher on Feb 6 in S&P E-Minis refocuses attention on the primary uptrend and the key resistance at 7043.00, the Jan 28 high. Clearance of this level would confirm a resumption of the trend and mark the end of a flat correction in the contract. Key short-term support has been defined at 6751.50, the Feb 6 low, where a break is required to highlight a top and a stronger short-term reversal.

- Japan's NIKKEI closed lower by 10.7 pts or -0.02% at 57639.84 and the TOPIX ended 26.88 pts higher or +0.7% at 3882.16.

- Elsewhere, in China the SHANGHAI closed higher by 2.035 pts or +0.05% at 4134.018 and the HANG SENG ended 233.84 pts lower or -0.86% at 27032.54.

- Across Europe, Germany's DAX trades higher by 302.67 pts or +1.22% at 25157.31, FTSE 100 higher by 28.65 pts or +0.27% at 10501.5, CAC 40 up 69.91 pts or +0.84% at 8383.15 and Euro Stoxx 50 up 42.58 pts or +0.71% at 6078.22.

- Dow Jones mini up 170 pts or +0.34% at 50374, S&P 500 mini up 20.5 pts or +0.29% at 6981, NASDAQ mini up 51 pts or +0.2% at 25338.25.

Time: 10:00 GMT (05:00 ET)

COMMODITIES: Bull Cycle in WTI Futures Remains Intact

A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.55. The 50-day EMA lies at $60.79. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger to watch has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend. The recent recovery in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high still highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude down $0.11 or -0.17% at $64.53

- Natural Gas up $0.05 or +1.46% at $3.205

- Gold spot down $11.82 or -0.23% at $5073.35

- Copper up $4.9 or +0.82% at $601.25

- Silver down $0.5 or -0.59% at $83.7816

- Platinum down $18.98 or -0.89% at $2118

Time: 10:00 GMT (05:00 ET)

| Date | GMT/Local | Impact | Country | Event |

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers Panel Talk on Productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR Existing Home Sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane at the World Ahead 2026 Gala Dinner | ||

| 12/02/2026 | 0000/1900 | Fed's Lorie Logan, Stephen Miran | ||

| 13/02/2026 | 0700/0800 | * | Wholesale Prices | |

| 13/02/2026 | 0730/0830 | *** | CPI | |

| 13/02/2026 | 0800/0900 | *** | HICP (f) | |

| 13/02/2026 | 1000/1100 | *** | EZ GDP (2nd Reading) | |

| 13/02/2026 | 1000/1100 | * | Employment | |

| 13/02/2026 | 1000/1100 | * | Trade Balance | |

| 13/02/2026 | 1000/1100 | ECB's de Guindos Lecture at Academia Europea Leadership | ||

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A at Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat at Santander Macro Event | ||

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | ** | US CPI Annual Revised | |

| 13/02/2026 | - | *** | New Loans | |

| 13/02/2026 | - | *** | Money Supply | |

| 13/02/2026 | - | *** | Social Financing |