MNI US OPEN - French Crisis Extends as PM Lecornu Resigns

EXECUTIVE SUMMARY

- LECORNU RESIGNS AFTER NAMING LARGELY UNCHANGED GOVERNMENT

- TAKAICHI ELECTED LDP'S 1ST FEMALE HEAD

- TRUMP PUSHES FOR ISRAEL, HAMAS DEAL AHEAD OF MONDAY TALKS

- ECB’S GUINDOS SAYS PRICE STABILITY COULD BE GUARANTEED

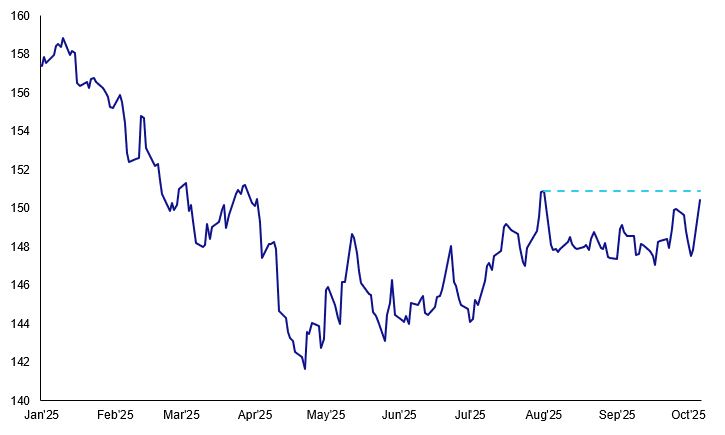

Figure 1: USD/JPY spikes 2%, approaches key resistance on Takaichi win (chart shows high price)

Source: MNI, Bloomberg Finance L.P.

NEWS

FRANCE (MNI): Lecornu Resigns After Naming Largely Unchanged Government

French Prime Minister Sebastien Lecornu has presented his resignation to President Emanuel Macron after a broadly unchanged government Lecornu named on Sunday

evening was criticised by party leaders from both the right and the left. Politico described Lecornu's government as "a sign that the political forces represented in Macron's successive administrations remain broadly the same, despite Lecornu's being the French president's fifth prime minister in less than two years." Lecornu's resignation comes after a Friday move to rule out using Article 49.3 of the French constitution to pass a budget without a parliamentary vote, and a parallel bid to agree on a 'non-aggression pact' between competing parties failed to ease concerns with Socialists.

FRANCE (MNI): Oct.13 Budget Draft Deadline Looms w/No Clear Route to Functional Govt

French Minister for Public Accounts Amelie de Montchalin warned in an interview with Le Monde last month that the government must submit a draft budget to parliament by October 13 or enact a special law to avoid a shutdown, as it will no longer be possible to pass a budget by January 1. De Montchalin said a special law was used earlier this year, "There was no catastrophe because it only lasted six weeks." However, she added, "France cannot go an entire year without a budget: It's a context in which revenues and expenditures are frozen. Political choices and priorities would give way to a purely accounting form of management."

JAPAN (MNI): Takaichi Elected LDP's 1st Female Head

Japan’s ruling Liberal Democratic Party on Saturday elected Sanae Takaichi as its new president in a runoff against Agriculture Minister Shinjiro Koizumi, paving the way for her to become Japan’s first female prime minister. Opposition parties, which together control a majority in both chambers of parliament, are unlikely to agree on a unified candidate due to policy differences. In her first speech as LDP president, Takaichi said tackling the cost-of-living crisis would be her top priority. She noted that small and medium-sized enterprises, as well as those in the agriculture and fisheries sectors, have been hit hard by rising costs and “need to be helped.”

US/MIDEAST (BBG): Trump Pushes for Israel, Hamas Deal Ahead of Monday Talks

President Donald Trump is pressing Israel and Hamas to seal a settlement to the two-year conflict that’s devastated Gaza and destabilized the Middle East as the warring sides are set to begin mediated talks on Monday. The first sign of whether the negotiations, being hosted by Egypt, are serious will be whether Hamas follows through on Trump’s demand to release all the remaining hostages, including those who died, in return for Israel releasing Palestinian prisoners.

ECB (BBG): Race for ECB’s No. 2 Job to Shape Search for Lagarde Succession

The European Central Bank is heading into a two-year shake-up that will replace two-thirds of its top leadership — including President Christine Lagarde. Plans to overhaul of the six-strong Executive Board — shaped as much by politics as personal qualifications — could kick off this week when euro-zone finance ministers meet in Luxembourg, providing the opportunity to start discussing a successor to Lagarde’s No. 2, Luis de Guindos.

ECB (MNI): Price Stability Could Be Guaranteed - de Guindos

The European Central Bank’s 2% price stability target could already be guaranteed with interest rates at current levels given incoming data on services inflation, wages evolution and the overall economic outlook, Luis de Guindos said at an event in Madrid on Monday. “Inflation risks are balanced and our projections are being met”, the ECB's Vice President said, while adding that uncertainty is still high and things could change quickly.

UK (BBG): British Lender Shawbrook Unveils IPO, Adding to LSE Momentum

British specialty lender Shawbrook Group Plc said it’s planning an initial public offering on the London Stock Exchange, making it one of the largest UK companies to go public in the City since 2021 and adding to momentum for the bourse after years of muted volumes. The banking firm backed by BC Partners and Pollen Street said the offering would consist of new and existing shares, in a statement on Monday. The firm could seek a valuation of about £2 billion ($2.7 billion), Bloomberg News previously reported.

BOJ (MNI): Mixed Wages, Prices May Cloud Rate Hike - BOJ

The Bank of Japan reported mixed views on wage hikes for fiscal 2026 and on corporate price-setting behaviour, key areas of focus for policymakers, in its quarterly Regional Economic Report released Monday. Regional firms expressed differing views on wage and price policies. A transportation company plans to maintain high wage levels in fiscal 2026, similar to this year, while a food and beverage firm in the same area intends to limit pay increases amid falling profits.

CZECHIA (MNI): Election Winner ANO on Track to Lead Next Administration

Andrej Babiš's ANO is on track to form a coalition or minority government after Czech voters handed it a clear victory in parliamentary elections held over the weekend. The party garnered 34.5% of the vote and immediately proceeded to coalition talks with right-wing Motorists for Themselves (AUTO) and Freedom and Direct Democracy (SPD). The governing Spolu alliance (ODS, KDU-ČSL and TOP09) took 23.4% of the vote, finishing in a distant second place, as expected. Its result was marginally better than suggested by opinion polls, but insufficient to hold onto power and should prompt the alliance's leaders to rethink future cooperation. The Civic Democratic Party (ODS) brought forward its leadership election to January amid reports that outgoing Prime Minister Petr Fiala was considering stepping down.

DATA

EUROZONE AUG RETAIL SALES +0.1% M/M, +1.0% Y/Y (VS -0.4% M/M, +2.1% Y/Y JUL)

SPAIN DATA (MNI): Another Small Decline in IP, But Underlying Signals Remain Positive

Spanish industrial production fell 0.1% M/M SA in August, the second consecutive sequential decline. Only three analysts had submitted forecasts for the print, with estimates ranging from -0.2% to +0.7% M/M. Though sequential growth rates have been negative for two months now, 3m/3m and Y/Y comparisons remain in positive territory. Furthermore, signals from the manufacturing PMI suggests underlying IP momentum remains positive.

SWISS SEP UNEMPLOYMENT RATE 3.0% (MNI)

AUSTRALIA DATA (MNI): Data Continue to Signal Stall in Disinflation

The Melbourne Institute's inflation gauge for September picked up 0.2pp to 3.0% with Q3 averaging 2.9% up slightly from Q2's 2.8%. It also has a trimmed mean measure which also rose 0.2pp to 2% in September to be 1.9% in Q3 up from Q2's 1.5% and may be trending higher again. Monthly CPI inflation is also higher over Q3 and RBA Governor Bullock sounded cautious last week as the central bank is concerned that there are signs a few key components are rising, especially market services which have also been sticky overseas. The key quarterly CPI data are released 29 October and are likely to determine the outcome of the 4 November RBA meeting.

FOREX: EUR and JPY Slide on Political Risks, USD Main Beneficiary

- The EUR is weaker in early Europe, following the resignation of the French PM Lecornu - and bedding markets in for an extended period of political risk and budget brinkmanship. French equities also see weakness - with the CAC40 easily the underperformer in Europe. Next major support in EURUSD crosses at 1.1646, the late Sept low. Weakness through here snaps the weak uptrend posted off the August 1st low.

- Lecornu's resignation opening up more criticism from other parties: National Rally's Bardella says the government have shown they have understood

"nothing" regarding the country's problems. - Meanwhile, the JPY is lower against all others in G10, helping trigger a new all-time high for EURJPY, after the surprise victory of Takaichi in the LDP leadership race. This was no doubt a surprise to the market given market odds, with most bettors favouring Koizumi winning the race. An extraordinary session of the Diet will be held around Oct to choose a new PM.

- Takaichi's policy bias around pro-fiscal policy may mean the coalition could expand to incorporate more like-minded parties, and she is expected to focus on cash handouts and tax rebates for households to reduce cost of living pressures. While she toned down her criticism of the BoJ during the leadership campaign, her well known views around BoJ rate hikes (she previously deemed them "stupid") is weighing on the currency. USD/JPY rallied to touch 150.44, paving the way for a test of the key medium-term resistance at 150.92, the Aug 1 high. A break of this hurdle would confirm a resumption of the bull leg that started Apr 22. Today's intraday low at 149.05 is the first support.

- The US government remains in shutdown, leaving official data on the sidelines for now. As such, market focus remains on central bank speak. ECB members due today include ECB's Escriva & Lagarde, Fed's Schmid and BoE's Bailey.

EGBS: OATs Underperform After Lecornu Resigns; Curves Steepen

Steepening pressures have re-asserted themselves in EGB curves this morning, with OATs in the spotlight following French PM Lecornu’s resignation. OAT yields are flat to +8bps, with German counterparts -2bps (Schatz) to +3bps (30-year Bund) at typing. That sees the 10-year OAT/Bund spread up 5.5bps to 86.5bps, after briefly piercing the December 2024 high of 87.8bps in the immediate aftermath of Lecornu’s resignation.

- There is once again no clear route to a functional French Government, with the EC’s October 13 budget deadline nearing.

- OAT futures traded to a knee-jerk session low of 120.61 on the Lecornu news (piercing the Sep 25 low of 120.63), but have since recovered to 120.99. Volumes are unsurprisingly very strong.

- Bund futures have settled towards the middle of today’s 45 tick range, currently -12 ticks at 128.55.

- The EU is scheduled to hold a syndication this week, with conventional auctions set to begin tomorrow. This week sees heavy redemptions from Germany totalling E36bln.

- External steepening forces include Sanae Takaichi’s success in the LDP leadership election over the weekend, alongside ongoing US Government shutdown risks.

- Eurozone August retail sales were in line with consensus at 0.1% M/M, with July’s reading revised up a tenth to -0.4%. The October Sentix survey was slightly stronger than expected (-5.4 vs-7.7 cons, -9.2 prior).

- ECB Chief Economist Lane re-iterated the bank’s data dependent approach, while de Guindos noted again that rates are appropriate at current levels. We don’t expect any surprises from Escriva and Lagarde later today.

GILTS: Bear Steepening on Global Cues

Gilts trade lower as steepening impetus from Japan (in the wake of the LDP Party naming a new leader & PM) and heightened political risk in France (as PM Lecornu steps down) weigh.

- Futures break Thursday’s low, basing at 90.48 before a recovery to 90.60.

- Bears remain in technical control at this stage, particularly with UK fiscal risks lingering.

- Initial support and resistance in futures still located at 90.26 & 91.28, respectively.

- Yields 1.5-5.0bp higher, curve steeper.

- 10s still comfortably within their recent 4.60-4.80% range, last 4.73%. Broader benchmark yields fail to test recent highs.

- 2s10s and 5s30s stick within their respective multi-week ranges, trading ~7bp and ~11bp below their cycle closing highs. Steepening trends intact.

- BoE-dated OIS still shows ~5bp of easing through year-end and is not discounting the next 25bp cut until the end of the April MPC.

- We continue to believe that markets underprice the odds of a Q4 rate cut.

- Comments from BoE Governor Bailey are due today.

- They will be closely scrutinised (even though he spoke as recently as Friday), particularly after Deputy Governors Ramsden & Breeden failed to push back against the idea of rate cuts last week.

- We have previously suggested that Bailey and those two Deputies would probably have to join dovish dissenters Dhingra & Taylor if we were to see a cut in Q4.

- Also note that the BoE will sell GBP775mln of short bucket gilts from its APF (3- to 7-Year) this afternoon.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.963 | -0.5 |

Dec-25 | 3.923 | -4.5 |

Feb-26 | 3.818 | -14.9 |

Mar-26 | 3.788 | -17.9 |

Apr-26 | 3.707 | -26.0 |

Jun-26 | 3.683 | -28.4 |

Jul-26 | 3.634 | -33.3 |

Sep-26 | 3.623 | -34.4 |

EQUITIES: EuroStoxx 50 Futures Maintain a Bullish Theme Following Recent Climb

Eurostoxx 50 futures maintain a bullish theme. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high. A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 66.84.22. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6566.78.

- Japan's NIKKEI closed higher by 2175.26 pts or +4.75% at 47944.76 and the TOPIX ended 96.89 pts higher or +3.1% at 3226.06.

- Across Europe, Germany's DAX trades lower by 2.76 pts or -0.01% at 24377.13, FTSE 100 lower by 16.19 pts or -0.17% at 9475.19, CAC 40 down 149.89 pts or -1.85% at 7931.65 and Euro Stoxx 50 down 30.18 pts or -0.53% at 5621.53.

- Dow Jones mini up 60 pts or +0.13% at 47091, S&P 500 mini up 18.5 pts or +0.27% at 6782.75, NASDAQ mini up 113.5 pts or +0.45% at 25107.

Time: 10:00 BST

COMMODITIES: WTI Futures Remain in a Bear-Mode Condition

WTI futures remain in a bear-mode condition. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains in play and today’s fresh cycle high, reinforces current conditions. This maintains the bullish price sequence of higher highs and higher lows and note too that corrections, when they do occur, are shallow. Furthermore, moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3987.33 next, a Fibonacci projection. Support to watch lies at $3715.0, the 20-day EMA.

- WTI Crude up $0.97 or +1.59% at $61.85

- Natural Gas up $0.15 or +4.45% at $3.475

- Gold spot up $57.43 or +1.48% at $3944.61

- Copper down $5.05 or -0.99% at $505.95

- Silver up $0.7 or +1.45% at $48.6983

- Platinum up $11.84 or +0.74% at $1616.6

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 06/10/2025 | 1500/1600 | BOE Bailey Keynote at Scotland Global Investment Summit | ||

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 06/10/2025 | 1700/1900 | ECB Lagarde at ECON Hearing, European Parliament | ||

| 06/10/2025 | 2100/1700 | Kansas City Fed's Jeff Schmid | ||

| 07/10/2025 | 2330/0830 | ** | Household spending | |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran |

Note: Due to U.S. government shutdown, some data may be unavailable.