MNI US OPEN - EU Warns of Retaliation Against Trump Tariffs

EXECUTIVE SUMMARY

- EU WARNS A BASELINE TRUMP TARIFF WILL STILL SPUR RETALIATION

- US STRIKE SET BACK IRAN’S NUCLEAR PROGRAM BY ONLY A FEW MONTHS, REPORT SAYS

- FED’S SCHMID SUPPORTS WAIT-AND-SEE APPROACH, WATCHING PRICE DATA

- BOJ'S TAMURA SEES EARLY 2% TARGET HIT

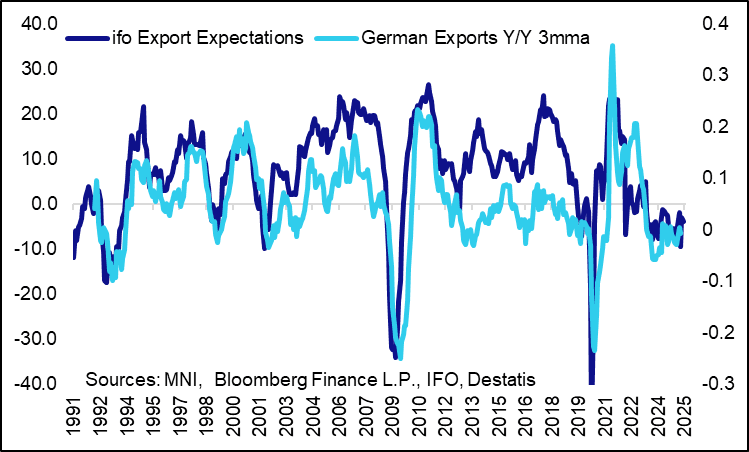

Figure 1: German ifo Export Expectations Fall in June

NEWS

US/EU (BBG): EU Warns a Baseline Trump Tariff Will Still Spur Retaliation

The European Union plans to impose retaliatory tariffs on US imports, including on Boeing Co. aircraft, if President Donald Trump puts a baseline levy on the bloc’s goods as many expect. EU officials expect the US to keep some duties in place, even after trade negotiations are concluded. Until now, the European Commission, which handles trade matters for the EU, hasn’t indicated if that would trigger retaliation from the bloc.

US/MIDEAST (NYT): Strike Set Back Iran’s Nuclear Program by Only a Few Months, U.S. Report Says

A preliminary classified U.S. report says the American bombing of three nuclear sites in Iran set back the country’s nuclear program by only a few months, according to officials familiar with the findings. The strikes sealed off the entrances to two of the facilities but did not collapse their underground buildings, the officials said the early findings concluded.

US (BBG): Trump Disputes Pentagon View, Says Iran Sites ‘Destroyed’

US President Donald Trump disputed an intelligence report that found the airstrikes he ordered on Iran had only a limited impact on its nuclear program, even though the assessment came from the Pentagon. “The nuclear sites in Iran are completely destroyed,” Trump said on Truth Social. He said CNN and the New York Times, which first reported the intelligence findings on Tuesday, “have teamed up in an attempt to demean one of the most successful military strikes in history.” Later, speaking to reporters at a NATO summit in The Hague on Wednesday, he said the report was “very inconclusive” but that he still believed the sites were demolished.

US/UKRAINE (AFP): Trump-Zelensky Talks Confirmed for Wednesday: Ukrainian Presidency Source

Ukrainian President Volodymyr Zelensky and US President Donald Trump will meet during the NATO summit in The Hague on Wednesday, a senior Ukrainian presidency source told AFP. The source said that both sides are expected to make brief statements ahead of the talks that are scheduled to start at around 13:30 local time (1130 GMT).

US (MNI): Trump Speaks on NATO & Iran-Israel Ceasefire

Speaking at the NATO summit, US President Donald Trump says, "We're with them all the way" when asked by reporters about the US' commitment to Article 5 (the collective defence clause). Adds that "NATO will be very strong". NATO Secretary General Mark Rutte praises Trump on getting NATO countries to increase defence spending, says that "Today we will decide to go to 5% [of GDP]." Trump says that the Iran-Israel ceasefire is "going well". Asked on Iran's uranium enrichment plans, Trump says, "We will not allow that militarily...Iran is not going to have a bomb...the last thing Iran wants to do is enrich anything." Says the US will have "somewhat of a relationship" with Iran.

NATO (MNI): Leaders Meet to Sign Off on 5% Spending Commitment

NATO leaders are delivering doorstep comments ahead of the main session of the alliance's summit in The Hague later this morning. Secretary General Mark Rutte is due to speak alongside US President Donald Trump shortly, followed by the welcoming ceremony and 'family photo' shortly. Rutte will hold a press conference after the Council meeting, at ~13:45CET (07:45ET, 12:45BST). He will then meet with the 'Indo-Pacific Partners' (Australia, Japan, New Zealand, South Korea) at 14:30CET (08:30ET, 13:30BST).

UK (The Times): British Jets to Carry Nuclear Warheads

Britain will buy a new squadron of fighter jets that can fire tactical nuclear weapons to match Russia and China in the biggest expansion of the deterrent since the end of the Cold War. Sir Keir Starmer, the prime minister, warned that “we can no longer take peace for granted” as he unveiled plans to buy 12 F-35As, which will carry American B-61 nuclear gravity bombs, capable of killing thousands.

US (WaPo): Cuomo Concedes to Mamdani in New York City’s Democratic Mayoral Primary

Zohran Mamdani, a 33-year-old state assemblyman and democratic socialist, took a lead Tuesday in the Democratic primary for mayor here after the first round of voting was tallied. His edge over former Democratic governor Andrew M. Cuomo positioned him for a seismic upset and signaled the enthusiasm his campaign engendered among voters eager for change. Because the primary is decided through ranked-choice voting, final results aren’t expected until July 1, according to the New York City Board of Elections. But Cuomo conceded defeat in remarks Tuesday night.

FED (BBG): Fed’s Schmid Supports Wait-and-See Approach, Watching Price Data

Federal Reserve Bank of Kansas City President Jeff Schmid said the US central bank should wait to see how tariffs and other policies impact the economy before adjusting interest rates. Schmid’s comments suggest he’s in no rush to lower borrowing costs, echoing what Chair Jerome Powell told lawmakers earlier Tuesday. “With all this uncertainty, the current posture of monetary policy, which has been characterized as ‘wait-and-see,’ is appropriate,” Schmid said Tuesday in prepared remarks for an event in Omaha, Nebraska. “The resilience of the economy gives us the time to observe how prices and the economy develop.”

RIKSBANK (MNI): Riksbank Minutes Show Wariness Over Further Cut

The June Riksbank Executive Board minutes showed that the five members were united in supporting both the 25 basis point policy rate cut to 2 per cent and the accompanying forecasts which put an even chance of a futher cut. First Deputy Governor Anna Seim said that although there were factors that could push up on inflation, such as supply chains shocks or a weaker krona, none of these had materialized and the risk was that weaker demand caused by uncertainty would create low inflation. This could lead to at least one more rate cut.

BOJ (MNI): BOJ's Tamura Sees Early 2% Target Hit

Bank of Japan board member Naoki Tamura signaled a more hawkish stance on Wednesday, suggesting the Bank’s 2% inflation target could be achieved earlier than expected and calling for a steady normalisation of monetary policy and the BOJ’s balance sheet. Speaking to business leaders in Fukushima City, Tamura said he does not view the 0.5% policy rate as a ceiling, citing both rising inflation and changes in bank lending rates compared to the previous rate-hike cycle.

JAPAN (MNI): Steady JGB Cut; Decisive Policy Change

A few Bank of Japan board members supported steadily reducing the Bank’s JGB holdings, though concerns over moving too quickly were also raised, according to the summary of opinions from the June 16-17 policy meeting released Wednesday. One member said the BOJ should normalise the amount of outstanding JGB holdings as soon as possible to “increase, at the earliest possible time, the capacity in financial markets to absorb shocks.” Another member noted that excess reserves remained abundant, making it appropriate for the Bank to “proceed steadily with the reduction of its purchase amount of JGBs, and thereby normalise its balance sheet.”

THAILAND (BBG): Thailand Holds Key Rate as Political Uncertainty Adds to Risks

The Bank of Thailand held its key interest rate unchanged, saving its limited policy space as political uncertainty at home compounds global risks ranging from US tariffs to the conflict in the Middle East. The central bank’s seven-member Monetary Policy Committee voted 6-1 to maintain the one day repurchase rate steady at 1.75% at Wednesday’s meeting. The hold was predicted by 15 of 21 economists surveyed by Bloomberg, with the rest forecasting a quarter-point cut. April saw the first back-to-back cut since 2020.

RUSSIA/CHINA (WSJ): Israel-Iran Conflict Spurs China to Reconsider Russian Gas Pipeline

The war between Israel and Iran has revived Chinese leaders’ interest in a pipeline that would carry Russian natural gas to China, according to people close to Beijing’s decision-making, potentially jump-starting a project that has been stalled for years. The Power of Siberia 2 pipeline project has been mired in disagreements over pricing and ownership terms, as well as Chinese concerns about relying too heavily on Russia for its energy supplies. But the recent war in the Middle East has given Beijing reason to reconsider the reliability of the oil and natural gas it gets from the region, the people said, even as a fragile cease-fire between Israel and Iran takes hold.

DATA

EUROZONE DATA (MNI): Indeed Wage Tracker Eases in May; Consistent With ECB Tracker

The May Indeed wage tracker, released yesterday, eased to 2.5% Y/Y (vs 3.2% prior) for the lowest rate since late 2021. The 3mma Y/Y rate was steady at 3.0%. Overall, the message from Indeed remains broadly consistent with the ECB's forward looking wage tracker. Wages for posted jobs in Germany eased to 3.3% Y/Y (vs 4.6% prior), with the 3mma rate steady at 3.8%. In France, which makes up a significant proportion of total observations in the Euro-area wide tracker, posted pay growth was unchanged at 2.0% Y/Y (3mma also unchanged at 1.9%).

GERMANY DATA (MNI): IFO Export Expectations Fall in June

IFO export expectations fell slightly in June to -3.9 points, down from -3.0 points in May. "The tariff threats from the US are still on the table. An agreement between the EU and the US has yet to be reached. This uncertainty is lowering exporters' expectations", IFO comments. "Beverage manufacturers took a major hit: After a very positive export outlook in the previous months, they do not expect any further impetus from international business in the coming months. Expectations among food manufacturers also plunged - they anticipate a decline in exports."

FRANCE DATA (MNI): Consumer Sentiment Weak; Political Uncertainty in Focus

- FRANCE JUN CONSUMER SENTIMENT 88

French June consumer confidence was steady at 88.4 (vs 88.3 prior), a touch below the 89.0 rounded consensus. There are likely downside risks to French sentiment ahead though, with political uncertainty set to ratchet higher again in the coming months. After the Bayrou government failed to reach an agreement on pension reforms with social partners yesterday, the Socialist party (supported by others on the left) have proposed a censure motion. While the far-right RN will not support censure at this stage, they have highlighted the 2026 budget as a key event to determine if they will continue to tacitly support (or at least, not bring down) Bayrou.

SPAIN Q1 FINAL GDP +2.8% Y/Y (MNI)

SPAIN Q1 FINAL GDP +0.6% Q/Q (MNI)

JAPAN DATA (MNI): May Services PPI Rises 3.3% vs. Apr 3.4%

Japan’s Services Producer Price Index (SPPI) rose 3.3% y/y in May, slightly easing from a revised 3.4% in April, indicating that firms are continuing to pass on higher costs, preliminary Bank of Japan data showed Wednesday. The slight slowdown was driven by softer gains in information and communications services (+2.4% vs. +2.6%) and real-estate services (+2.7% vs. +2.9%). However, advertising services accelerated sharply, rising 2.5% compared to 0.9% in April.

AUSTRALIA DATA (MNI): Monthly CPI Falls 20bp Below Expectations

- AUSTRALIA MONTHLY MAY CPI 0% MM, 2.1% YY

Australia’s monthly Consumer Price Index indicator rose 2.1% y/y in May, 20 basis points below expectations, while the annual trimmed mean measure fell 40bp to 2.4%, data from the Australian Bureau of Statistics showed Wednesday. The headline CPI result marked the lowest reading since October 2024, while the trimmed mean was at its lowest level since November 2021, potentially reinforcing expectations that inflationary pressures are easing more broadly. While the Reserve Bank of Australia monitors the monthly read, it prefers the more complete quarterly data.

FOREX: USD/JPY Bounces, But S/T Tech Drivers Still Point Lower

- Australian monthly CPI came in lower-than-expected, which could call into question the RBA's next inflation outlook round, however the currency is again firmer off lows and holding the bulk of the recovery off Monday's 0.6373. This price actions favours this week's weakness as a false break below the bottom-end of the multi-month trend channel, and a reversion higher here would make 0.6552, the June 16 high and bull trigger, the primary upside target.

- USD/CHF remains within range of cycle lows after the solid outperformance posted from the beginning of the week. Having initially benefited from haven flows on the exchange of fire between Israel and Iran, the CHF has held the rally, keeping 0.8035 in sight as the next downside level in USD/CHF.

- Meanwhile, USD/JPY is recouping a small part of the sharp losses posted off the 148.03 high, putting prices back above Y145.50 in what's likely a corrective rally off the pullback lows. This week's price action has formed a shooting star candle pattern - which argues in favour of further S/T losses in the pair. The 50-dma marks the next downside level at 144.25, but we see the 20-day EMA at 144.81 as more materially important in the short-term. The level has been pierced, but a clear break of it would strengthen a bearish threat.

- May new home sales data is the sole US release Wednesday. This should keep focus on the second appearance from Fed's Powell this week, this time in front of the Senate Finance Committee. He struck a balanced tone on policy yesterday, however a mention from the Fed chair that rate cuts could come faster on "lower inflation, weaker labor" still elicited interest from markets, despite the Fed chair again implying September is the next 'Live' meeting.

- The ongoing NATO meeting in the Netherlands will be carefully watched for cohesion around Trump's latest narrative that the US has secured firmer military commitments from Europe, despite remaining signs of dissention among countries including Spain. The US President remains in NATO sessions until 1040ET, at which time he is scheduled to return to the White House.

EGBS: Early Rally in Bunds Fades; Pullback From Jun 13 High Still Corrective

Early downward pressure in 10-year Bund yields stalled just above the 2.50% level, with yields across the curve now back to ~1bp lower on the day. There wasn’t a clear headline driver for the early rally in EGBs, with markets still digesting the de-escalation in the Middle East alongside yesterday’s German and Italian fiscal/issuance announcements.

- Bund futures are -4 ticks at 130.80, peaking at 131.12 earlier this morning. Bunds remain in consolidation mode, trading below the Jun 13 high. For now, the recent move down appears to be a correction. Key short-term support to watch lies at 130.12, the Jun 5 low.

- The 10-year BTP/Bund spread found support at the 90bp handle, with a pullback in European equities from session highs helping to spread back to 91.5bps. Italy sold E3.0bln of the new 2.10% Aug-27 BTP Short Term and E3.0bln of the new 1.10% Aug-31 BTPei this morning.

- In France, the Socialist party has submitted a censure motion against the Bayrou government. Although RN leader Bardella said his party would not support the current motion, he still signalled that a vote of no confidence could still be called in response to the 2026 budget, proposals for which will be detailed next month. The 10-year OAT/Bund spread is 1.5bps narrower today at 69bps despite the evident political risks.

- Today’s regional data calendar has been light (French consumer confidence was a little weaker-than-expected), with focus turning to the Spanish and French flash June inflation prints on Friday.

- There will be some interest in the outcome of today's NATO summit, with leaders expected to sign off on a much briefer communique than is usually the case at these events, due to its truncated nature. Commitments on the '3.5%+1.5%' of GDP on defence spending is likely to be agreed, although potentially with wording that allows Spain, still holding out on the 5% total, to accept.

GILTS: Off Highs, Soft 10-Year Auction Demand Noted

Gilts have ticked away from early session highs, with moves in core global FI peers and disappointing demand at the latest 10-Year auction factoring in.

- Futures pierce yesterday’s high before paring back from best levels, -9 at 93.38 last (93.33-57 range).

- The technical outlook in the contract remains bullish, next upside target is the June 13 high (93.68).

- Meanwhile, support is located at the 20-day EMA (92.51).

- Yields little changed to 2bp lower, curve bull steepens.

- Fundamentals point towards a steepening bias (further BoE cuts, with dovish risks, alongside limited fiscal headroom), although already crowded positioning, as well as a more activist approach from policymakers when it comes to containing spikes higher in long end yields, present risks to this idea.

- 10s spread vs. Bunds little changed at ~192.5bp.

- No headlines of note from the BoE’s CCBS conference as of yet.

- Modest dovish adjustments in GBP STIRs vs. closing levels.

- SONIA futures flat to +1.0, BoE-dated OIS pricing 52bp of cuts through year-end vs. ~51.5bp late yesterday.

- The June high in SFIZ5 remains unchallenged, as does the recent dovish extreme in Dec BoE-dated OIS (~55bp of cuts). However, SFIZ6 has registered a fresh multi-week high, switching bullish focus to the cluster of early May highs.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.013 | -20.3 |

Sep-25 | 3.952 | -26.5 |

Nov-25 | 3.784 | -43.3 |

Dec-25 | 3.696 | -52.0 |

Feb-26 | 3.572 | -64.4 |

Mar-26 | 3.539 | -67.8 |

EQUITIES: Recovery in Eurostoxx 50 Futures Appears to Signal Potential Reversal

A short-term bear cycle in Eurostoxx 50 futures remains intact, however, the recovery from Monday’s low appears to be a potential reversal. The contract has traded above the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme and signal scope for a stronger recovery. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of Monday’s 5194.00 low would reinstate a bearish theme. The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle high reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. Sights are on the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5922.67. A clear break of it would signal a reversal.

- Japan's NIKKEI closed higher by 151.51 pts or +0.39% at 38942.07 and the TOPIX ended 0.89 pts higher or +0.03% at 2782.24.

- Elsewhere, in China the SHANGHAI closed higher by 35.408 pts or +1.04% at 3455.974 and the HANG SENG ended 297.6 pts higher or +1.23% at 24474.67.

- Across Europe, Germany's DAX trades lower by 36.72 pts or -0.16% at 23605.84, FTSE 100 higher by 12.96 pts or +0.15% at 8771.86, CAC 40 up 9.62 pts or +0.13% at 7625.27 and Euro Stoxx 50 up 0.42 pts or +0.01% at 5297.24.

- Dow Jones mini up 6 pts or +0.01% at 43430, S&P 500 mini down 0.25 pts or 0% at 6146, NASDAQ mini up 10.25 pts or +0.05% at 22422.25.

Time: 10:00 BST

COMMODITIES: Bullish Theme in Gold Remains Intact

WTI futures maintain a softer tone following the reversal from Monday’s high. Support to watch is at the 50-day EMA, at $64.50. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. A bullish theme in Gold remains intact and the latest pullback is considered corrective - for now. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has recently been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3287.7, the 50-day EMA.

- WTI Crude up $1.01 or +1.57% at $65.38

- Natural Gas down $0.01 or -0.14% at $3.532

- Gold spot up $2.87 or +0.09% at $3327.29

- Copper up $2.8 or +0.57% at $495.15

- Silver down $0.07 or -0.19% at $35.8757

- Platinum down $7.49 or -0.57% at $1313.54

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf | ||

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 25/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 25/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/06/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 25/06/2025 | 1800/1400 | Federal Reserve Board Meeting | ||

| 26/06/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 26/06/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 26/06/2025 | 0830/0930 | BOE Breeden On UK Competetiveness Panel | ||

| 26/06/2025 | 0945/1145 | ECB De Guindos At Deutsch Bank Forum 2025 | ||

| 26/06/2025 | 0945/1045 | BOE Greene Chairs Panel On MonPol Communication | ||

| 26/06/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 26/06/2025 | 1100/1300 | ECB Schnabel At 'Wirtschaftsrat der CDU' Finanzmarktklausur | ||

| 26/06/2025 | 1100/1200 | BOE Bailey Keynote Speech At BCC Conference | ||

| 26/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 26/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 26/06/2025 | 1230/0830 | * | Payroll employment | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1230/0830 | *** | GDP | |

| 26/06/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1245/0845 | Richmond Fed's Tom Barkin | ||

| 26/06/2025 | 1300/0900 | Cleveland Fed's Beth Hammack | ||

| 26/06/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 26/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 26/06/2025 | 1430/1530 | BOE Lombardelli Chairs Panel On Communicating Uncertainty | ||

| 26/06/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 26/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 26/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 26/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/06/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 26/06/2025 | 1715/1315 | Fed Governor Michael Barr | ||

| 26/06/2025 | 1830/2030 | ECB Lagarde Opening Speech at Münchner Opernfestspiele | ||

| 26/06/2025 | 1900/1500 | *** | Mexico Interest Rate |