Fig. 1: Canadian unemployment seen returning to post-COVID highs

Source: MNI - Market News/Bloomberg

NEWS

FED (MNI): Trump Missed Window For Significant Fed Change

The Trump administration is unlikely to score any major reforms of the Federal Reserve because there is no clear effort to pressure Capitol Hill for the kind of legislative changes that would be needed, Gary Richardson, the Fed system's first official historian, told MNI.

U.S. (BBG): Trump Signs Order Easing Path for Private Assets in 401(k)s (1)

President Donald Trump signed an executive order easing access to private equity, real estate, cryptocurrency and other alternative assets in 401(k)s, a major victory for industries looking to tap some of the roughly $12.5 trillion held in those retirement accounts.

U.S.-CHINA (BBG): Bessent: China Tariffs ‘Could Be On The Table’ Over Russia Oil

Treasury Secretary Scott Bessent says the US may impose tariffs on China at some point, when asked about President Trump’s promise to impose tariffs on countries that buy Russian oil.

JAPAN (NYT): Japan Says Trump to Correct ‘Extremely Regrettable’ Error in Tariff Order

The Trump administration has agreed to correct an “extremely regrettable” blunder in the execution of its trade agreement with Japan, the country’s top trade negotiator said in Washington on Thursday.

BOJ (MNI): BOJ Opinions: Price Risk; May Exit From Waiting Mode

Some Bank of Japan board members acknowledged upside risks to prices but saw no need to rush a rate hike at the July 30-31 meeting, the summary of opinions showed Friday.

A former BOJ official shares his policy rate outlook -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA (MNI): China's Interest Bond Tax To Inject Yield Volatility

Advisors share their view on China's new bond interest income tax -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.

RUSSIA (Guardian): Trump says he will meet Putin despite Kremlin’s refusal to talk to Kyiv

Donald Trump has said he is ready to meet Vladimir Putin despite the Russian leader’s refusal to meet Ukraine’s Volodymyr Zelenskyy – dispelling speculation that direct talks between the two warring presidents were a precondition of a high-level US-Russia summit.

INDIA (Business Standard): Trump Rules Out Trade Talks With India Until Tariff Dispute Resolved

US President Donald Trump has ruled out any possibility of trade negotiations with India until the two countries resolve the ongoing dispute over tariffs.

ISRAEL (BBC): Israel Approves Plan To Take Control Of Gaza City, Signalling Major Escalation

Israel's security cabinet has approved a plan to take control of Gaza City, Prime Minister Benjamin Netanyahu's office has confirmed.

EQUITIES (BBG): Intel CEO Says Has Board Support As Trump Calls For Resignation

Intel Corp. Chief Executive Officer Lip-Bu Tan said he’s got the full backing of the company’s board, responding for the first time to US President Donald Trump’s call for his resignation over conflicts of interest.

GOLD (FT): U.S. Hits One-Kilo Gold Bars With Tariffs In Blow To Refining Hub Switzerland

The US has imposed tariffs on imports of one-kilo gold bars, in a move that threatens to upend the global bullion market and deal a fresh blow to Switzerland, the world’s largest refining hub. The Customs Border Protection agency said one-kilo and 100-ounce gold bars should be classified under a customs code subject to levies, according to a so-called ruling letter dated July 31, which was seen by the Financial Times.

OIL (BBG): Russia Boosts Oil Processing, Fuel Output To Meet Demand At Home

Russia’s oil producers are boosting crude processing, deploying spare refinery capacity and accelerating unplanned repairs to meet domestic fuel demand, the nation’s Energy Ministry said Friday in a Telegram statement.

DATA

GERMAN DATA (MNI): Truck Toll Index Points Towards July IP Recovery

Destatis has released its monthly data for July for its truck toll index, which printed +2.3% on a sequential comparison to the weak June (-0.8% prior). This tentatively points towards some recovery in industrial production last month after the IP print notably surprised to the downside yesterday (at -1.9% M/M amid a May downward revision).

GBP has extended the spell of post-BoE decision strength. GBP/USD edged to a new recovery high overnight at 1.3453, signalling markets are still buying into the view that the split vote yesterday has restricted the room with which the BoE can cut rates later this year. For now, S/T momentum is still pointed higher, with the Jul 24 high of 1.3589 the next notable upside level.

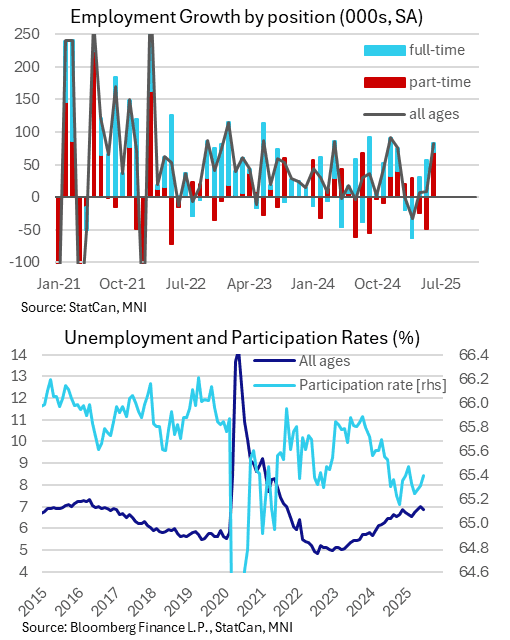

Canada's July jobs report is due Friday, and with markets expecting job gains to slow sharply to +10k from +83.1k previously, the unemployment rate is seen ticking moderately higher. Ahead of the print, USD/CAD is holding toward the lower-end of the weekly range, with yesterday's 1.3722 low and the 1.3692 50-dma the next notable downside levels.

JPY is among the poorest performers on the day. Speculation continues to mount over the future of the LDP leadership. Speaking today, Ishiba noted he is not intending to change the cabinet lineup for now, but has vowed to stay on in his role despite party pressure to accelerate succession. Conviction in the weaker is low, however, with volumes holding below the average for this time of day.

BoE's Pill and Fed's Musalem are the sole central bank speakers. Speculation remains over the possible make-up of the FOMC into 2026, with CEA head Miran set to step in for the remainder of Kugler's term, while reports earlier in the week suggested current FOMC member Waller was being pushed to take over from Powell next year. Any further reports or headlines here will be carefully watched by markets.

Today also marks the supposed expiry of Trump's deadline by which Moscow must strike a ceasefire with Ukraine to avoid secondary tariffs. Presumably the week's developments and potential meeting with Putin as early as next week will prompt relief here, but further White House commentary on this topic will be carefully watched.

Gilts hold lower looking to cues from Tsys after yesterday’s soft 30-Year U.S. auction.

Futures as low as 92.14.

The 20-day EMA (92.11) and yesterday’s low (92.00) remain untouched, leaving the recent bullish cycle intact. Initial resistance located at the 5 August high (92.84).

Yields 1-3bp higher, curve steeper, but major spreads still comfortably flatter than pre-BoE levels.

Spread to Bunds 0.5bp wider, trading 192bp, 200bp remains untested in August.

The DMO has announced that the next syndication will be the launch of a new 10-year conventional gilt maturing on 22 October 2035. The transaction will take place in the W/C 1 September subject to market conditions

We had already pencilled in a 10-year gilt for that week - so this is not a huge surprise. We pencil in Tuesday 2 September but Wednesday 3 September is also possible.

17bp of BoE easing priced through year-end, with the next cut fully discounted through the end of the Feb MPC.

SONIA futures little changed to -2.0.

SFIZ5 broke its July low during yesterday’s sell off but failed to test June lows before recovering. Meanwhile, SFIZ6 failed to challenge its August base.

We have seen a couple of hawkish sell-side BoE view changes, but most still lean towards a cut at the next MPR meeting in November.

Comments from BoE’s Pill are due later today, but the chief economist’s hawkish stance has been underscored by yesterday’s dissenting vote. Comments surrounding his dissent are eyed as a result. Expect him to remain relatively hands off when it comes to the timing of any potential future policy moves and ongoing focus on the uncertain outlook the UK faces.

BoE Meeting

SONIA BoE-Dated OIS (%)

Difference vs. Current Cut-Adjusted SONIA Rate (bp)

Bund futures have weakened 15 ticks today on below average volumes, currently at 130.08. Downside pressure has been fairly steady since the European open, with desks potentially reacting to yesterday evening’s weak US 30-year auction. Headline flow has been light, with no major regional data released either.

This week’s light weakness in Bunds is considered corrective from a technical perspective. Initial support is around the 129.80 level, with key support and the bear trigger not seen till 128.84 (Jul 25 low).

German yields are 2-3bps higher, while 10-year EGB spreads to Bunds are up to 0.5bps tighter. The BTP/Bund spread is gradually narrowing the gap to support around 75bps, the 2010 low.

EQUITIES: Eurostoxx50 Futs Extending Bounce

While the e-mini S&P faded into the Thursday close, the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact for now. The index holds above support at the 20-day EMA, at 6336.50. The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA into the Thursday close.

Japan's NIKKEI closed higher by 761.33 pts or +1.85% at 41820.48 and the TOPIX ended 36.29 pts higher or +1.21% at 3024.21.

Elsewhere, in China the SHANGHAI closed lower by 4.539 pts or -0.12% at 3635.128 and the HANG SENG ended 222.81 pts lower or -0.89% at 24858.82.

Across Europe, Germany's DAX trades lower by 48.02 pts or -0.2% at 24142.51, FTSE 100 higher by 3.22 pts or +0.04% at 9104.82, CAC 40 up 13.07 pts or +0.17% at 7722.05 and Euro Stoxx 50 up 3.61 pts or +0.07% at 5335.2.

Dow Jones mini up 49 pts or +0.11% at 44128, S&P 500 mini up 14.5 pts or +0.23% at 6381, NASDAQ mini up 61.5 pts or +0.26% at 23557.75.

COMMODITIES: WTI Futures Extend Spell of Weakness

Gold continues to benefit from the soft NFP print on Friday and broad USD weakness across the week. This returns prices toward the top-end of the recent range and supports the view that short-term weakness is corrective. WTI futures trade poorly early Friday, having cracked the 50-day EMA and extended losses on the week. This keeps S/T momentum pointed lower. Support at the 50-day EMA has been cleared.