MNI US OPEN - Bullock's Tone Cautious Following RBA Pause

EXECUTIVE SUMMARY

- RBA’S BULLOCK STRIKES CAUTIOUS TONE FOLLOWING PAUSE

- UK'S REEVES DECLINES TO RULE OUT BREAKING TAX VOWS

- CHINA URGES US TO AVOID ‘RED LINES’ AFTER REACHING TRADE TRUCE

- SNB RATE CUT BELOW ZERO ISN’T WARRANTED FOR NOW, TSCHUDIN SAYS

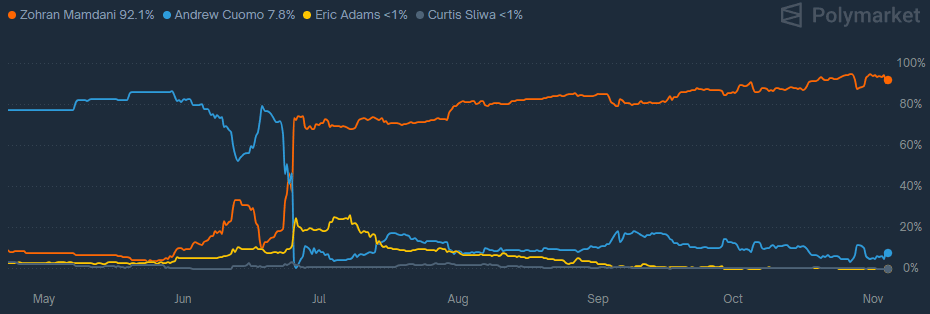

Figure 1: New York City Mayoral Election Odds

Source: Polymarket

NEWS

RBA (MNI): Bullock Strikes Cautious Tone Following Pause

The Reserve Bank of Australia may not need to ease as much as its peers, Governor Michele Bullock said on Tuesday after the Board unanimously decided to hold the cash rate at 3.6%. “We do see elevated inflation in the first 12 months because of the most recent numbers,” Bullock said, referring to the September quarter’s 3% trimmed mean result, which largely drove Tuesday’s widely-anticipated decision. “That’s baked in now, and then we see the quarterly numbers starting to come off and delivering an inflation rate of around 2.6% by the end of the period. But there’s a great deal of uncertainty.” While the RBA’s updated forecasts are based on at least one more cash rate cut, Bullock noted that keeping rates at 3.6% would push inflation toward the 2.5% target midpoint more quickly.

US/CHINA (WSJ): Trump Officials Torpedoed Nvidia’s Push to Export AI Chips to China

Shortly before President Trump met Chinese leader Xi Jinping in South Korea, an urgent issue emerged. Trump wanted to discuss a request by Nvidia Chief Executive Jensen Huang to allow sales of a new generation of artificial-intelligence chips to China, current and former administration officials said. Greenlighting the export of Nvidia’s Blackwell chips would be a seismic policy shift potentially giving China, the U.S.’s biggest geopolitical competitor, a technological accelerant. Huang—who speaks to Trump often—has lobbied relentlessly to maintain access to the Chinese market.

US/CHINA (BBG): China Urges US to Avoid ‘Red Lines’ After Reaching Trade Truce

China called on the US to avoid four sensitive issues so a trade truce sealed between Presidents Donald Trump and Xi Jinping can hold, highlighting the broad array of disagreements that will test ties. Ambassador to the US Xie Feng named Taiwan, democracy and human rights, China’s political system, and development rights as Beijing’s four red lines, adding that “the most important thing is to respect each other’s core interests and major concerns.”

US (NYT): The First Big Elections of the New Trump Era Are Today

Voters on Tuesday will deliver an early judgment on President Trump’s administration in the first set of coast-to-coast elections since he began his turbulent second term. Contests for mayor of New York, governor of New Jersey and Virginia, and a redistricting ballot measure in California have revolved to varying degrees around how the Democratic Party should rebuild itself and respond to Mr. Trump’s power play in Washington. The elections are predominantly in Democratic areas and battleground states, where the party’s candidates have sought to harness anger about Mr. Trump while deflecting discontent about the state of the Democratic brand.

UK (MNI): Reeves Prepares Ground For Tax Hikes; Voters Already Expecting Them

Chancellor of the Exchequer Rachel Reeves' speech earlier this morning, in which she talked about the UK's economic situation with regard to the 26 Nov udget, but not about the measures the budget would contain, was somewhat oddly timed. There has been significant speculation in recent weeks that Reeves intends to break the Labour manifesto promise of not raising income tax, VAT or National Insurance contributions. Given the language used in her speech, it is clear that the chancellor was attempting to prepare the ground for tax rises in the budget statement. However, by refusing to confirm or deny that the manifesto pledge will be breached, the main impact of the address will be to set up 3+ weeks of more media speculation, and ensure that headlines around looming tax hikes and 'Labour broken manifesto promises' remain prominent in the UK news cycle rather than only coming back to the fore in the direct run-up to the budget.

ECB (BBG): ECB’s Rehn Urges Rate Flexibility, Confirms Vice Presidency Bid

The European Central Bank must keep all its options open with both upside and downside risks to the inflation outlook, according to Governing Council member Olli Rehn, who confirmed he’ll run to become the institution’s vice president next year. While uncertainty has eased somewhat thanks to developments such as the ceasefire in the Middle East, it’s “still considerable,” the Finnish central-bank chief said in an interview on Tuesday.

ECB (BBG): ECB’s Lagarde Touts Euro’s Advantages to Skeptical Bulgarians

European Central Bank President Christine Lagarde sought to allay concerns among Bulgarians that adopting the euro will lead to prices rising more quickly. While acknowledging that “currency changeovers can produce a temporary uptick,” Lagarde said the switch — from January 2026 — will boost prosperity and security, and won’t necessarily lead to faster inflation.

EU/LATAM (BBG): EU Leaders Skip Latin American Summit to Avoid Annoying Trump

European leaders including German Chancellor Friedrich Merz and European Commission President Ursula von der Leyen will skip the EU’s summit with Latin American and Caribbean states due in part to concerns over angering US President Donald Trump. The European Union-CELAC summit is coming under scrutiny in Europe as the US targets countries including Colombia — which is hosting the summit — and Venezuela over drug trafficking claims, according to people familiar with the matter.

SNB (BBG): SNB Rate Cut Below Zero Isn’t Warranted for Now, Tschudin Says

The Swiss National Bank sees no reason to cut interest rates below zero at present but that can always change, policymaker Petra Tschudin said in a television interview. With price growth within the range targeted by the central bank, the current level of borrowing costs is appropriate, but it’s “hard to say” now what will happen at the next decision in December, she told Swiss TV station TeleZueri, according to a press release from the broadcaster on Tuesday.

BOJ (MNI EXCLUSIVE): Ueda Dec 1 Speech Crucial For BOJ Hike Timing

MNI looks at the BOJ's latest rates policy calculations. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Takaichi Says Japan Still Halfway Toward Achieving Stable Prices

Japanese Prime Minister Sanae Takaichi said the nation is still in the process of achieving stable inflation accompanied by wage increases, in a sign that she wants the Bank of Japan to proceed cautiously with its policy deliberations. “I recognize that we are still halfway to attaining stable and sustainable inflation with wage increases,” Takaichi said in parliament Tuesday afternoon. “I expect the BOJ to continue to take appropriate monetary policy” toward achieving its price target.

INDIA (BBG): RBI Intervenes Again, Lifting Indian Rupee From Near Record Low

The rupee gained sharply, pulling back from a near-record low after intervention by the Reserve Bank of India. The currency rose as much as 0.4%, the most since Oct. 15, to 88.3925 per dollar, before paring gains. The central bank stepped in with dollar sales in the offshore currency market just before the onshore trading commenced at 9 am local time, according to people familiar with the matter.

MNI NBP PREVIEW - NOVEMBER 2025: Cut on Cards After Soft CPI Print

The November meeting may be the last chance for the NBP to cut interest rates this year as an unwritten local convention dictates that the MPC sits on its hands in December. Although recent communications signalled continued vigilance amid lingering inflationary risks, another dovish CPI reading prompted a realignment of market consensus around a 25bp rate reduction. We too are inclined to think that the MPC will deliver an opportunistic cut before taking the next couple of months to reconsider its stance. Benign current inflation data and a revised macroeconomic projection should provide sufficient grounds to continue easing monetary policy. At the same time, we admit that it is a close call, with this MPC’s opaque reaction function fuelling uncertainty around the outcome.

DATA

JAPAN DATA (MNI): Japan Q3 GDP to Fall 0.7% Q/Q; Annualised -2.7%

Japan’s economy is expected to have contracted for the first time in six quarters in the July-September period, as weaker private consumption and capital investment offset earlier front-loaded gains, according to private economists. Preliminary estimates suggest GDP fell 0.7% quarter-on-quarter, or an annualised 2.7%, reversing from a 0.5% q/q (annualised 2.2%) expansion in the April-June quarter.

FOREX: GBP Soft on Clearest Signal Yet of "Unpopular" Tax Policy Ahead

- GBP traded softer on the back of another pre-Budget appearance from UK Chancellor Reeves. While not drawn into details on the Budget measures specifically - it was certainly her clearest signal yet that sizeable tax rises are incoming (suggested by the statement of working in the national interest, rather than political popularity), as well as indicating her intention to pave the way with fiscal policy to allow for further BoE rate cuts.

- What does this mean for GBP? GBPUSD has broken to a new pullback low - trading at comparable levels with the Liberation Day rally in April. This makes 1.3041, the Apr 14 low the area of interest ahead of 1.2971, the 1.382 proj of the Sep 17 - 25 - Oct 1 price swing.

- Outside of GBP, risk-off trade pervades after slippage in US equity futures held through overnight trade and remains the dominant theme into the crossover. Palantir is set to drop over 7% at the open as markets caution on extreme valuations and the scale of the recent rally - a move mirrored in South Korea's SK Hynix overnight - a key supplier to Nvidia.

- Resultantly, the best performing currency today is JPY, rallying against all others, will risk proxy currencies slide - namely the NZD. Initial support in USD/JPY comes in at 153.27, followed by 152.06. The technical trend structure in the pair remains bullish at this stage.

- JOLTs, trade balance and durable goods orders data were originally set for release today - but the extension of the government shutdown will keep focus on private sector data and corporate earnings as the best bellwether for the state of the economy. As such, tomorrow's ADP employment change, S&P Global final PMI and ISM services index are of utmost importance.

EGBS: Soft Risk Backdrop Helps Bunds Back Above 50-day EMA

Bund futures have found support from this morning’s deterioration of risk sentiment, but underperform Gilts. Today’s price action has allowed Bunds to move back above the 50-day EMA, which was pierced yesterday. For now, the selloff that started on October 17 is still considered corrective.

- Bunds are +18 ticks at 129.30 at typing. Initial resistance is the 20-day EMA at 129.42.

- German yields are 1.5 – 2.5bps lower across the curve. This morning’s Eurozone focus has been on supply, with the EFSF holding a dual tranche syndication, Austria selling 10-year RAGBs (which were well-received) and Germany set to sell E5bln of the 2.00% Dec-27 Schatz at 1030GMT.

- 10-year EGB spreads to Bunds are up to 1.5bps wider owing to the soft risk backdrop. European equity futures are down 1.65%.

- The French core state budget deficit in the year to September narrowed slightly versus August, as would normally be expected but at least an improvement compared to a rare monthly deficit in Sep 2024. The YTD deficit remains smaller than last year, helped by a further increase in revenues, and remains roughly on track to meet 2025 targets. Focus remains on ongoing 2026 budget negotiations.

- Bank of Finland Governor Rehn outlined his intention to run for ECB Vice President. He also maintained that uncertainty about future growth remains high, and that risks are skewed to the downside.

GILTS: Off Highs After Reeves But Still Outperforming Bunds

Gilts continue to outperform core global FI peers after the UK media signalled the increased likelihood pf meaningful fiscal tightening in the UK.

- Chancellor Reeves didn’t provide any fresh detail, which saw gilts trade away from session highs.

- Still, her choice of phrases and omissions of manifesto pledges (there was no mention of avoiding hiking the big 3 taxes and no increases of taxes on working people) left the door open to meaningful alterations in the Budget later this month.

- Elsewhere, wider risk-off price action stemming from equity weakness in a couple of meaningful global tech names (Palantir & SK Hynix) provided cross-market support.

- Gilt futures traded as high as 93.98 before trimming gains to ~93.70 (+33).

- Next resistance at 94.00.

- Yields 2.5-3.5bp lower, curve flatter. October closing lows intact at this stage.

- Long 3-Year supply passed smoothly.

- SONIA futures flat to +4.0. October highs in SFIZ6 remain untouched.

- BoE-dated OIS is flat to 2bp more dovish on the day, showing 7bp of easing for this week’s meeting (which we deem to be a 50/50 decision), 17bp through December (vs. ~19bp at one point today) and 30bp through February.

- BoE’s Breeden will speak at Santander’s International Banking Conference. Note that the BoE is in its pre-meeting quiet period, so don’t expect her to comment on monetary policy. She will focus on financial stability and there will not be a text release.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.903 | -6.6 |

Dec-25 | 3.807 | -16.2 |

Feb-26 | 3.668 | -30.1 |

Mar-26 | 3.602 | -36.7 |

Apr-26 | 3.490 | -47.9 |

Jun-26 | 3.460 | -50.9 |

Jul-26 | 3.397 | -57.2 |

Sep-26 | 3.379 | -59.0 |

EQUITIES: Short-Term Weakness for Eurostoxx Futures Considered Corrective

Short-term weakness in Eurostoxx 50 futures is considered corrective. The contract has breached the 20-day EMA, signalling scope for a deeper retracement towards support at the 50-day EMA, at 5567.19. Support below the EMA lies at 5549.50, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Key resistance and bull trigger is 5742.00, the Oct 29 high. The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Attention is on support at the 20-day EMA, at 6804.03. A clear break of this level average would signal scope for a deeper retracement and expose the 50-day EMA at 6698.11 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- Japan's NIKKEI closed lower by 914.14 pts or -1.74% at 51497.2 and the TOPIX ended 21.69 pts lower or -0.65% at 3310.14.

- Elsewhere, in China the SHANGHAI closed lower by 16.335 pts or -0.41% at 3960.186 and the HANG SENG ended 205.96 pts lower or -0.79% at 25952.4.

- Across Europe, Germany's DAX trades lower by 425.99 pts or -1.77% at 23708.36, FTSE 100 lower by 102.59 pts or -1.06% at 9598.75, CAC 40 down 127.82 pts or -1.58% at 7981.97 and Euro Stoxx 50 down 89.91 pts or -1.58% at 5589.34.

- Dow Jones mini down 414 pts or -0.87% at 47060, S&P 500 mini down 79 pts or -1.15% at 6803.75, NASDAQ mini down 385.5 pts or -1.48% at 25717.25.

Time: 10:00 GMT

COMMODITIES: WTI Futures Remain in a Corrective Cycle for Now

WTI futures remain in a corrective cycle for now. Note that price has recently traded through the 50-day EMA, currently at $61.05. The breach of this EMA signals scope for a stronger recovery. Note too that a resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low. Gold is unchanged. A fresh cycle low last week highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3864.7. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

- WTI Crude down $0.79 or -1.29% at $60.23

- Natural Gas down $0.02 or -0.54% at $4.243

- Gold spot down $7.98 or -0.2% at $3991.65

- Copper down $11.9 or -2.35% at $495

- Silver down $0.3 or -0.63% at $47.749

- Platinum down $16.14 or -1.03% at $1553.83

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 04/11/2025 | 1130/1130 | Chancellor Reeves at House of Commons | ||

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 1500/1000 | *** | JOLTS Jobs Opening Level | |

| 04/11/2025 | 1500/1000 | *** | JOLTS Quits Rate | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 2100/1600 | Canada Federal Budget, Release Expected Just After 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/11/2025 | - | Riksbank Meeting | ||

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/11/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/11/2025 | 0745/0845 | * | Industrial Production | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Composite PMI (f) | |

| 05/11/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Composite PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Composite PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Composite PMI (f) | |

| 05/11/2025 | 0900/1000 | * | Retail Sales | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (f) | |

| 05/11/2025 | 0930/0930 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/11/2025 | 1000/1100 | ** | EZ PPI | |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (f) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden at SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | Average Wages (p) |

Note: Due to U.S. government shutdown, some data may be unavailable.