FOREX: GBP Soft on Clearest Signal Yet of "Unpopular" Tax Policy Ahead

- GBP traded softer on the back of another pre-Budget appearance from UK Chancellor Reeves. While not drawn into details on the Budget measures specifically - it was certainly her clearest signal yet that sizeable tax rises are incoming (suggested by the statement of working in the national interest, rather than political popularity), as well as indicating her intention to pave the way with fiscal policy to allow for further BoE rate cuts.

- What does this mean for GBP? GBPUSD has broken to a new pullback low - trading at comparable levels with the Liberation Day rally in April. This makes 1.3041, the Apr 14 low the area of interest ahead of 1.2971, the 1.382 proj of the Sep 17 - 25 - Oct 1 price swing.

- Outside of GBP, risk-off trade pervades after slippage in US equity futures held through overnight trade and remains the dominant theme into the crossover. Palantir is set to drop over 7% at the open as markets caution on extreme valuations and the scale of the recent rally - a move mirrored in South Korea's SK Hynix overnight - a key supplier to Nvidia.

- Resultantly, the best performing currency today is JPY, rallying against all others, will risk proxy currencies slide - namely the NZD. Initial support in USD/JPY comes in at 153.27, followed by 152.06. The technical trend structure in the pair remains bullish at this stage.

- JOLTs, trade balance and durable goods orders data were originally set for release today - but the extension of the government shutdown will keep focus on private sector data and corporate earnings as the best bellwether for the state of the economy. As such, tomorrow's ADP employment change, S&P Global final PMI and ISM services index are of utmost importance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle High

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4045 3.0% Upper Bollinger Band

- RES 2: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 1: 1.3989 200-dma

- PRICE: 1.3953 @ 16:02 BST Oct 3

- SUP 1: 1.3897/3825 Low Sep 30 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact and yesterday’s break above the late September’s high, firms the bullish theme. This move higher also maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3825, the 50-day EMA.

AUDUSD TECHS: Support Remains Intact For Now

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6603 @ 16:01 BST Oct 3

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at 0.6558. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

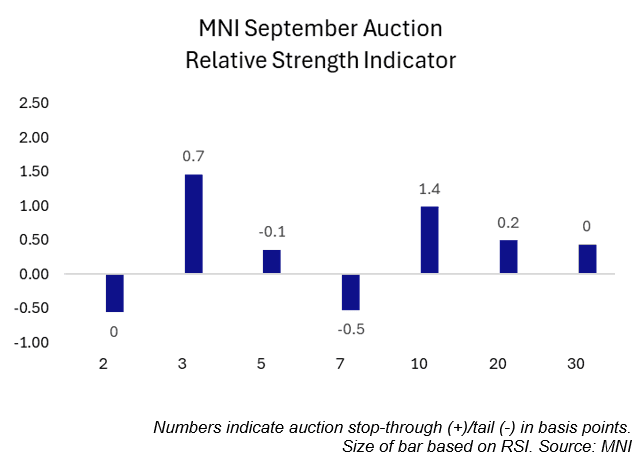

US TSYS/SUPPLY: September's Coupon Auctions Were Generally Solid (2/2)

September’s coupon auctions were generally solid, with three lines trading through, two coming out on the screws and two tailing slightly.

- Looking through the lens of MNI’s Relative Strength Indicator (RSI), five lines saw positive readings while two saw negative readings.

- The 3-year sale was the strongest auction of the month according to MNI’s RSI. The 3-year line traded through 0.7bps, the largest stop through in seven months. Meanwhile, the primary dealer take-up was just 8.4%, the lowest on record (data going back to 2003).

- The weakest sale of the month was the last – the 7-year line. This line saw the second consecutive 0.5bp tail, with the 12.0% primary dealer take-up above August’s 9.8% and July’s record low 4.1%.

September Auction Review:

- 2Y Note on-the-screws: 3.571% vs. 3.571% WI.

- 2Y FRN: 0.200% high margin vs. 0.195% prior

- 3Y Note trade-through: 3.485% vs. 3.492% WI.

- 5Y Note tail: 3.710% vs 3.709% WI.

- 7Y Note tail: 3.953% vs. 3.948% WI.

- 10Y Note trade-through: 4.033% vs. 4.047% WI.

- 10Y TIPS: 1.734% high yield vs. 1.985% prior

- 20Y Bond trade-through: 4.613% vs 4.615% WI.

- 30Y Bond on-the-screws: 4.651% vs. 4.651% WI.