MNI US OPEN - BOJ's Ueda Sees Gradual Hikes But No Timing Hint

EXECUTIVE SUMMARY

- BOJ’S UEDA SAYS RATE HIKES WILL COME; NO TIMING HINTS

- TRUMP, XI TO HOLD CALL AS TIKTOK, TARIFFS AND NVIDIA LOOM LARGE

- EU COMMISSION EXPECTED TO PRESENT 19TH ROUND OF SANCTIONS

- UK YTD GOVERNMENT BORROWING AT 5-YEAR HIGH IN AUGUST

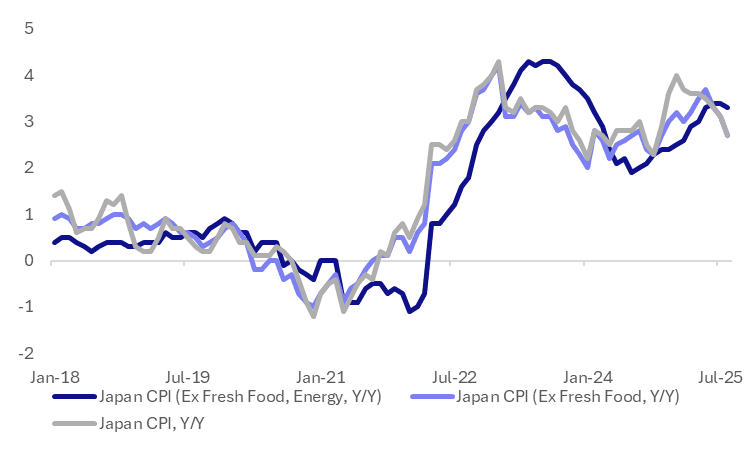

Figure 1: Japan CPI trends year-on-year - core ex fresh, energy still sticky above 3%

Source: MNI, Bloomberg Finance L.P.

NEWS

BOJ (MNI): Ueda Says Rate Hikes Will Come; No Timing Hints

Bank of Japan Governor Kazuo Ueda insisted that rate hikes remain in prospect but provided no further hints as to timing on Friday after the BOJ voted to keep the policy rate unchanged at 0.5% with two dissenters calling for a 25-basis-point hike. Uncertainty over the effects of U.S. trade policy and over the U.S. economy itself continues, and downside risks persist, Ueda told reporters. “Real interest rates stay at considerably low levels. We will raise the rate to adjust the degree of easy policy. We continue to carefully monitor the impact of trade policy on global economy without any preconditions,” he said, after the seven-two vote to hold, with calls for a hike by Naoki Tamura and Hajime Takata.

US/CHINA (BBG): Trump, Xi to Hold Call as TikTok, Tariffs and Nvidia Loom Large

The call Friday between US President Donald Trump and Chinese President Xi Jinping promises to determine the fate of TikTok — and potentially ease trade tensions between the world’s two biggest economies. Trump and Xi are due to speak at 9 a.m. Washington time, or 9 p.m. in Beijing about a framework agreement unveiled this week to shift control of TikTok’s US operations from its Chinese parent ByteDance Ltd. to a consortium of American investors.

US (WSJ): Trump's Team Explores Government-Backed Manufacturing Boost

President Trump's team is weighing a plan to spur the construction of factories and other infrastructure in a bid to jump-start the American manufacturing sector, according to documents and people familiar with the discussions. Under the plan, the administration would use money from a $550 billion investment fund established as part of trade negotiations with Japan to invest in the development of semiconductors, pharmaceuticals, critical minerals, energy, ships and quantum computing.

US (WSJ): Trump Administration Asks Supreme Court to Allow Removal of Fed Governor Lisa Cook

The Trump administration asked the Supreme Court on Thursday to let it remove Federal Reserve governor Lisa Cook from the central bank’s board while a lawsuit challenging the president’s effort to fire her proceeds. The emergency request came after a federal appeals court in Washington, D.C., rejected the administration’s bid to remove Cook ahead of the Fed’s meeting earlier this week. The 2-1 decision was handed down the night before the meeting began.

US (WaPo): Lawmakers Will Introduce Bill to Kill Tariffs on Coffee

Reps. Don Bacon (R-Nebraska) and Ro Khanna (D-California) plan to introduce a bill to exclude one everyday product from President Donald Trump’s tariffs: coffee. Their bipartisan legislation would exempt coffee products from any tariff imposed after Jan. 19, 2025 — the day before Trump came into office, according to draft legislation obtained by The Washington Post.

US (MNI INTERVIEW): Politics Already Influencing Path of Fed Policy

US/S.KOREA (BBG): US-Korea Talks Remain Stuck Over Auto Tariff, Visa Issues

South Korea remains in talks with the US over contentious issues, including visa restrictions and auto tariffs, the Asian nation’s top trade negotiator said, underscoring the economic stakes as Seoul works to ease frictions with Washington. Trade Minister Yeo Han-koo returned from Washington after meeting US Trade Representative Jamieson Greer and key members of Congress to press for progress in talks, he told reporters upon arriving in Incheon on Friday.

EU/RUSSIA (MNI): Commission Expected to Present 19th Round of Sanctions

The European Commission is set to announce its proposals for a 19th round of sanctions on Russia at some point today (19 September), with the main targets of the measures set to be Russia's hydrocarbon and banking sectors and its crypto markets.

EU/RUSSIA (BBG): EU Looking to Advance Russian Asset Plans Next Month, Lose Says

The European Union is looking to make progress in the coming weeks on plans to deploy billions of euros of frozen Russian assets to help fund Ukraine, according to Denmark’s economy minister. Speaking Friday in Copenhagen, Stephanie Lose said that securing financing for Ukraine is a top priority, and that a gathering of EU ministers next month is likely to yield more results toward that goal. “Hopefully we’ll advance question at the Ecofin in October,” Lose said before a meeting of European Union finance chiefs.

INDIA (BBG): India Presses Ahead With Russian Oil Buying as Modi, Trump Talk

Indian refiners have no plans to step away from Russian crude as domestic fuel demand picks up after the monsoon season, even as New Delhi resumes trade negotiations with Washington and both sides press for a deal. Instead, buying is expected to remain active for November and December delivery, though volumes may be below peaks seen in recent years, according to people with direct knowledge of procurement plans. They asked not to be identified as the matter is not public.

DATA

GERMANY DATA (MNI): August PPI Softer-Than-Expected; Disinflationary Forces Intact

- GERMANY AUG PPI -0.5% M/M, -2.2% Y/Y

German August PPI was softer-than-expected at -0.5% M/M, below the -0.1% consensus and prior reading. The pullback was mostly driven by the energy component, with PPI ex-energy falling -0.2% M/M (vs -0.2% prior). On a 3m/3m basis, PPI ex-energy fell for the fourth consecutive month to 0.1% (vs 0.3% in July). All major sub-components (investment goods, intermediate goods and consumption goods) have contributed to this move lower. Weaker momentum in pipeline pressures is also reflected in the EC's industry expected prices series, which remains at subdued levels.

UK DATA (MNI): UK YTD Government Borrowing at 5-Year High in August

- UK AUG PSNB GBP+17.96 BN

- UK AUG PSNB-X GBP+17.96 BN

- UK AUG PSNCR GBP10.16 BN

- UK AUG CGNCR GBP11.03 BN

UK government borrowing hit GBP18 billion in August, the second highest reading for the month on record, beaten only by the same period in 2020 at the height of the pandemic, the Office for Nartional Statistics said on Friday. Borrowing in the financial year to date was GBP83.8 billion, GBP16.2 billion more than in the same five-month period last year and the second-highest April-to-August borrowing since monthly records began in 1993. Public sector net debt excluding public sector banks was provisionally estimated at 96.4% of gross domestic product (GDP) at the end of August 2025; 0.5pp more than at the end of August 2024 at levels last seen in the early 1960s.

UK DATA (MNI): UK Retail Sales Enjoy Strong Summer Run

- UK AUG RETAIL SALES +0.5% M/M, +0.7% Y/Y

- UK AUG RETAIL SALES EX-FUEL +0.8% M/M, +1.2% Y/Y

UK retail sales volumes are estimated to have risen by 0.5% in August 2025, following an increase of 0.5% in July 2025, suggesting a strong start to the calendar Q3, the Office for National Statistics said Friday. Sales fell 0.1% in the months to August 2025 compared with the three months to May, the data showed. Clothing stores, butchers and bakers, and non-store retailing grew in August 2025, which, the ONS said, some retailers attributed to the good weather.

UK SEP GFK CONSUMER CONFIDENCE INDEX -19 (MNI)

FRANCE DATA (MNI): Fresh Post-Covid Low for INSEE Expected Employment

INSEE's September sentiment survey saw expected employment fall to a fresh post-covid low of 93.2, down from 94.8 in August and 95.9 in July. Against a backdrop of continued political and fiscal uncertainty, businesses appear reluctant to increase hiring and this will continue to weigh on economic activity. Broader business sentiment was steady at 95.9 (vs 96.2 prior) in September, with declines in manufacturing and retail offset by increases in services and construction confidence. All sectoral indicators remain below the neutral 100 level, though.

FRANCE SEP MANUF SENTIMENT 96 (MNI)

JAPAN DATA (MNI): Japan Aug Core CPI Rises 2.7% vs. July 3.1%

- JAPAN AUG CORE CPI +2.7% Y/Y; JULY +3.1%

- JAPAN AUG CORE-CORE CPI +3.3% Y/Y; JULY +3.4%

- JAPAN AUG SERVICES PRICES +1.5% Y/Y; JULY +1.5%

Japan’s annual core consumer inflation slowed to 2.7% y/y in August from 3.1% in July, the Ministry of Internal Affairs and Communications said Friday, as lower energy and food prices excluding perishables weighed on the index. The reading stayed above the Bank of Japan’s 2% target for the 41st straight month but fell below 3% for the first time since November 2024. Energy prices dropped 3.3% y/y after a 0.3% fall in July, while food prices excluding perishables rose 8.0%, easing from 8.3% the previous month.

FOREX: GBP Underperforming as DXY Probes Recovery Highs

- The dollar is trading on a firm footing Friday, broadly consolidating the solid post-Fed recovery and probing yesterday’s high in current trade around 97.60. Most of the action has been in the Japanese yen following the Bank of Japan, however, it’s sterling that is under the most pressure, after the latest round of UK PSNB data underscored the fiscal challenge that the UK faces at present.

- For USDJPY, the initial reaction was lower following BOJ board members Naoki Tamura and Hajime Takata wanting to raise the policy rate to 0.75%. The hawkish dissents saw USDJPY fall to a session low of 147.20. However, with the BOJ overall keeping its cautious economic view, leaving largely unchanged its assessment of private consumption, capital investment and exports, those initial USDJPY declines were pared steadily throughout the late APAC session and into the press conference.

- A bullish candle pattern on Tuesday - a hammer formation - provided an early reversal signal. Immediate resistance is at yesterday’s high of 148.27, and a continuation higher would open 149.14, the Sep 3 high.

- GBPUSD sits 0.52% in the red on Friday and has broken back below the 1.35 mark. Recent developments show no shift in the UK’s mix of sticky inflation and fiscal worry, resulting in the potential for higher for longer interest rates in the eyes of the market, yet providing no support for the pound.

- Initial firm support to watch at 1.3495, the 50-day EMA, has been pierced. A sustained break would pull into question the recent bullish theme. In similar vein, EURGBP is back above 0.8700, keeping bullish conditions intact. For bulls, a stronger resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high.

- Canadian retail sales is the final data release for the week.

EGBS: Bund Futures Off Session Lows, Supported by Crude and Equity Pullback

Bund futures have moved away from session lows over the last two hours, now -16 ticks at 128.35, seemingly supported by a pullback in European equity and brent crude futures. The September 4 low of 128.25 was pierced during this morning’s light selloff, but losses are still considered corrective for now.

- German paper lightly outperforms Gilts following this morning’s UK fiscal data. The 10-year Gilt/Bund spread is 0.5bps wider at 195.5bps.

- German yields are 0.5-1.5bps higher across the curve, with the belly lightly underperforming. That said, it’s long-end ASWs which are under the most pressure this morning.

- 10-year EGB spreads to Bunds are biased slightly tighter, with equities still up on the session despite the latest pullback.

- The Netherlands has set the coupon for next week’s DDA launch of the new 30-year DSL at 3.50%, while Italy has announced it will sell a new BTP Valore in October.

- This morning’s data saw German PPI come in below consensus (-0.5% M/M vs -0.1%) and France’s expected employment indicator reach a fresh post-covid low. Both are dovish developments on net, but the ECB will pay much more attention to next week’s September flash PMIs.

- Outgoing Bank of Portugal Governor Centeno struck an unsurprisingly dovish tone. We don’t pay much attention to his comments, with his replacement Pereira having already spoken this week.

GILTS: Away From Lows But Curve Still Steeper After PSNB Data

Gilts tick away from lows as oil markets soften and European equity benchmarks pull away from session highs.

- Gilt futures last -24 at 90.94 vs. session lows of 90.72.

- Yields now -1bp to +2bp, with the curve twist steepening.

- The September 5 high in 10-Year yields (4.716%) held, with that benchmark topping out at 4.715%, while the September 5 low in futures (90.65) went untested.

- Longer-dated UK paper continues to underperform Bunds in the wake of the higher-than-expected monthly PSNB figures that drove a sell off on the open, with the UK’s fragile fiscal situation underscored by the release.

- SONIA futures also off lows, last -2.5 to +0.5, while BoE-dated OIS shows ~6bp of easing through year-end after registering a fresh hawkish cycle extreme at ~5bp this morning.

- Outside of the PSNB release, retail sales data was in line to a touch firmer than expected (with negative revisions), while the IFS outlined the risks of a downgrade to the government’s productivity assumptions, which would provide fresh (but widely expected) fiscal headwinds.

- Not that the DMO confirmed that it will sell two lines (the 4.50% Sep-34 & 4.75% Dec-38 gilts) via PGT next week.

- Little of note on the UK calendar ahead of the weekend.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Nov-25 | 3.954 | -1.4 |

Dec-25 | 3.910 | -5.7 |

Feb-26 | 3.806 | -16.2 |

Mar-26 | 3.768 | -19.9 |

Apr-26 | 3.692 | -27.6 |

Jun-26 | 3.659 | -30.8 |

EQUITIES: Fresh Highs Keeps E-Mini S&P Bull Cycle Intact

Eurostoxx 50 futures recently traded through resistance around the 20-day EMA - a bullish development for now - and yesterday’s rally reinforces this theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high yesterday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6589.32, the 20-day EMA.

- Japan's NIKKEI closed lower by 257.62 pts or -0.57% at 45045.81 and the TOPIX ended 11.19 pts lower or -0.35% at 3147.68.

- Elsewhere, in China the SHANGHAI closed lower by 11.567 pts or -0.3% at 3820.089 and the HANG SENG ended 0.25 pts higher or +0% at 26545.1.

- Across Europe, Germany's DAX trades higher by 67.16 pts or +0.28% at 23740.28, FTSE 100 higher by 5.7 pts or +0.06% at 9233.61, CAC 40 up 67.32 pts or +0.86% at 7923.02 and Euro Stoxx 50 up 31.35 pts or +0.57% at 5488.5.

- Dow Jones mini up 18 pts or +0.04% at 46186, S&P 500 mini up 0.25 pts or +0% at 6635.25, NASDAQ mini up 1.5 pts or +0.01% at 24461.75.

Time: 10:00 BST

COMMODITIES: Trend Condition in WTI Futures Unchanged and Bearish

The trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low. Gold remains in a clear bull cycle and short-term weakness is for now, considered corrective. A fresh all-time high, once again this week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3705.2, a Fibonacci projection. Initial firm support lies at $3566.6, the 20-day EMA. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend.

- WTI Crude down $0.49 or -0.77% at $63.08

- Natural Gas down $0.01 or -0.48% at $2.925

- Gold spot up $11.14 or +0.31% at $3655.46

- Copper up $1.3 or +0.28% at $461.35

- Silver up $0.41 or +0.98% at $42.2442

- Platinum up $7 or +0.5% at $1393.56

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |