MNI US MARKETS ANALYSIS - USDJPY Through Support on Ueda

Highlights:

- Treasury curve sits bear steeper on Japan spillover

- ISM manufacturing in focus as private stats still take lead over official numbers

- JPY rally pushes USDJPY through support as Ueda makes December meeting live

US TSYS: Bear Steeper On Japan Spillover, ISM Mfg Ahead

Treasuries trade bear steeper overnight primarily in spillover to JGBs under pressure on greater prospects of the BoJ hiking next month. The move also extends treasury losses seen during Friday’s particularly disrupted session with the sustained CME outage and early close.

- Cash yields are 0.5-4bp higher, with increases led by 20s and 30s.

- 5s30s are 109bps is back close to Nov 21 two-month highs that briefly cleared 110bps.

- TYH6 trades at 113-07+ (-04) on reasonable overnight volumes of 310k.

- It has shifted away from last week’s high of 113-22+ (Nov 25 high) in what’s seen as a corrective pullback, with support seen at 113-01 (20-day EMA).

- Data: S&P Global US mfg PMI Nov F (0945ET), ISM Mfg Nov (1000ET)

- Fedspeak: Fed Chair Powell gives brief remarks and is in a panel discussion (2000ET) – text and Q&A but within FOMC blackout and so won’t touch on the economic outlook or monetary policy.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump signs Congressional bills (1600ET)

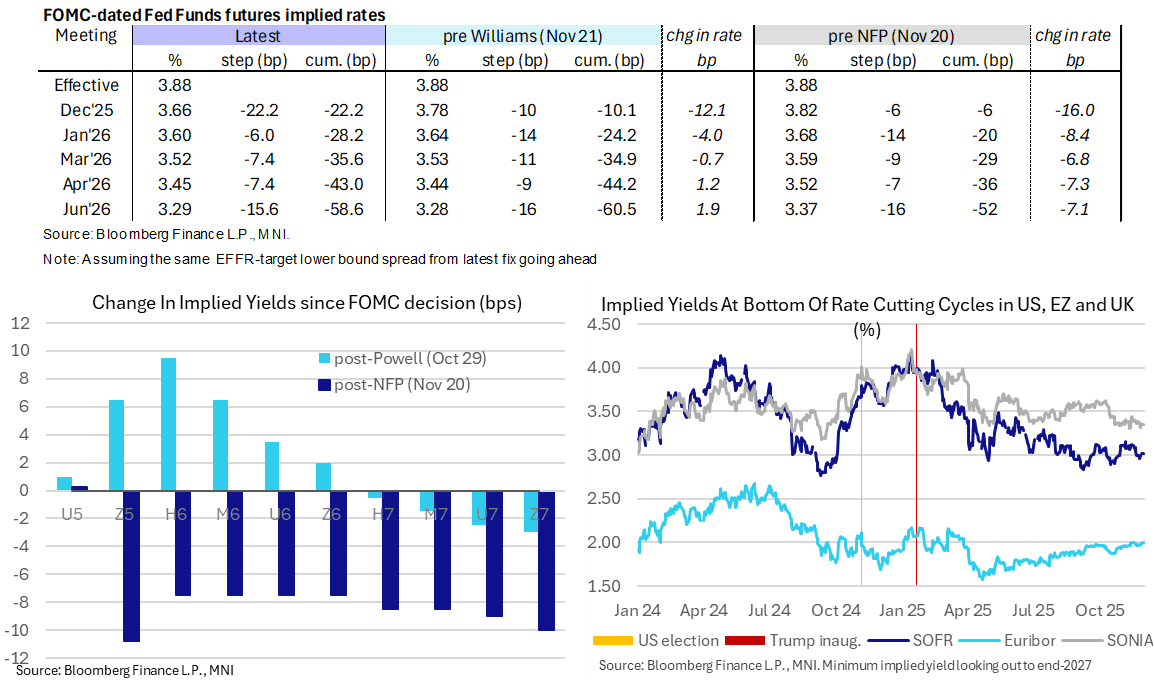

STIR: Fed 25bp Cut Increasingly Priced For Dec, Trump Has Decided On Fed Pick

- Fed Funds implied rates are 1bp lower for next month’s meeting, continuing to move closer to fully pricing a rate cut as time goes by without a countering argument, with little change further out.

- Today’s docket is headlined by manufacturing ISM/PMI surveys, with the FOMC now in media blackout.

- Trump yesterday said he has decided on his pick for the next Fed Chair role and that “we’ll be announcing it”. Bloomberg sources last week reiterated NEC’s Hassett as a front-runner and he’s since seen a further boost in betting markets to now 72% on Polymarket vs in the 50s late last week.

- Cumulative cuts from 3.88% effective: 22bp Dec, 28bp Jan, 35.5bp Mar, 43bp Apr and 58.5bp Jun.

- SOFR futures are between -0.01 to +0.005 on, with the terminal implied yield still holding around the 3.00% mark. A reminder that the 2.96% on Nov 25 was its lowest close since days shortly ahead of the hawkish Oct 29 FOMC press conference.

SOFR: Mix Of Limited Positioning Swings Seen In Futures Around Thanksgiving

OI data points to a mix of net positioning swings in the white pack of the SOFR futures strip between Wednesday’s close and Friday’s settlement

- SFRZ5 seemingly saw net short cover, while SFRH6 seemingly saw net short setting and SFRM6 saw net long cover.

- A mix of net short setting and long cover was then seen further out the strip.

- A reminder that volume was hampered by the presence of the Thanksgiving holiday and Friday’s technical issues at the CME, with the latter resulting in a further shortening of trading hours.

| 28-Nov-25 | 26-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,363,486 | 1,355,698 | +7,788 | Whites | -6,365 |

SFRZ5 | 1,690,713 | 1,709,755 | -19,042 | Reds | -496 |

SFRH6 | 1,351,866 | 1,343,237 | +8,629 | Greens | +4,814 |

SFRM6 | 1,126,543 | 1,130,283 | -3,740 | Blues | -4,571 |

SFRU6 | 1,099,480 | 1,106,614 | -7,134 |

|

|

SFRZ6 | 1,146,277 | 1,151,846 | -5,569 |

|

|

SFRH7 | 853,559 | 836,203 | +17,356 |

|

|

SFRM7 | 788,258 | 793,407 | -5,149 |

|

|

SFRU7 | 855,248 | 854,727 | +521 |

|

|

SFRZ7 | 864,928 | 855,845 | +9,083 |

|

|

SFRH8 | 432,490 | 438,271 | -5,781 |

|

|

SFRM8 | 407,543 | 406,552 | +991 |

|

|

SFRU8 | 374,486 | 374,061 | +425 |

|

|

SFRZ8 | 331,561 | 334,331 | -2,770 |

|

|

SFRH9 | 202,639 | 207,073 | -4,434 |

|

|

SFRM9 | 206,969 | 204,761 | +2,208 |

|

|

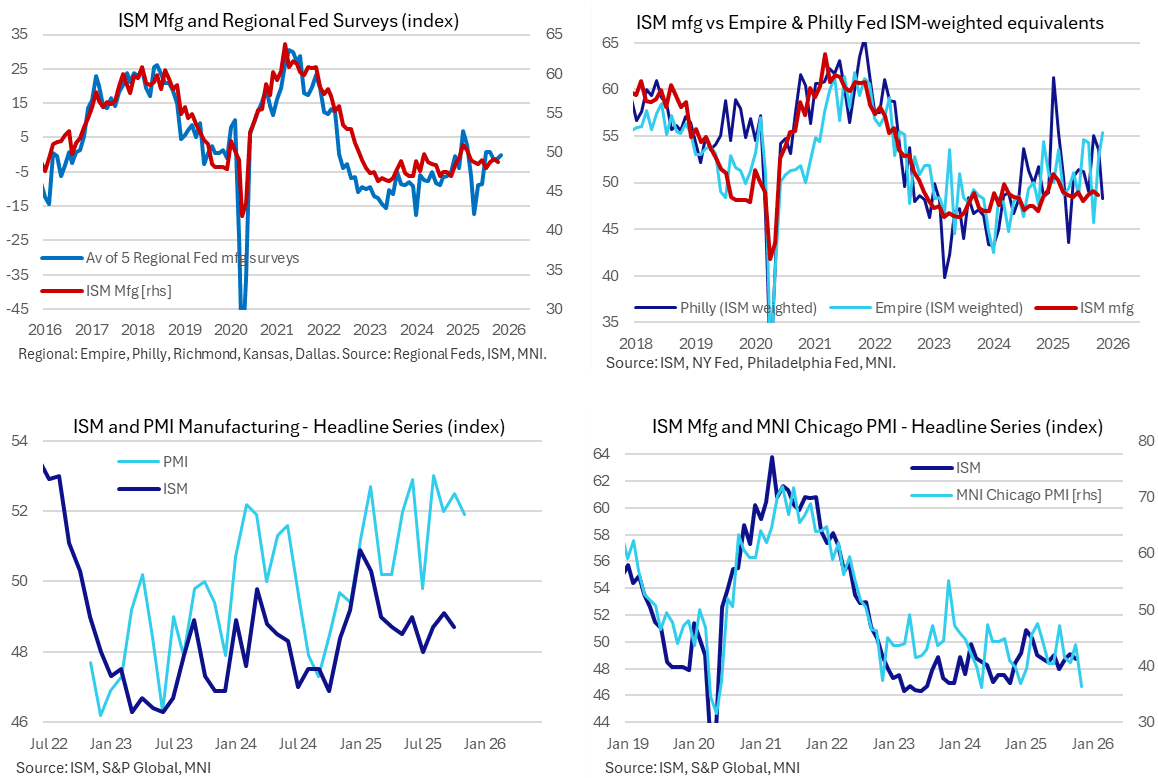

US OUTLOOK/OPINION: Two-Sided Risks For ISM Mfg, New Orders Look Softer

- Released at 1000ET today, the ISM manufacturing index is seen improving marginally to 49.0 in November having dipped 0.4pts to 48.7 in Oct.

- It has kept to a narrow range of 48.0-49.1 since March having eased back from Jan and Feb seeing the first months above 50 (i.e. in expansionary territory) since late 2022, with a high of 50.9 in Jan.

- Alternate indicators are mixed, justifying the limited improvement expected.

- Regional Fed surveys: mild upside. The average of the five regional Fed surveys increased from -1.0 to -0.1 although it’s essentially flatlined around its breakeven 0 line for six months now. The ISM equivalent readings of the Empire and Philly Fed surveys fell to 51.8 from 53.1 (highest since Feb) after a 5.2pt drop in the Philly version but continue to point to upside risk from a levels basis.

- S&P Global PMI: downside momentum, upside level. The flash survey eased from 52.5 to 51.9 in November to take it a little further away from the 53.0 in August that had been a multi-year high. It has averaged 2.6pts higher than the ISM survey so far this year, but by firmly differing amounts (between 0.3-4.3pts).

- MNI Chicago PMI: firm downside. It slumped 7.5pts to 36.3 in November for its second lowest since mid-2020 whilst new orders saw their largest one-month fall since Sep 2023.

- However, new orders indicators look a little more uniformly soft and could fall more materially below the 50-mark after 49.4 in Nov (its 51.4 in Aug was its highest since Jan). On top of that sharp drop in the MNI Chicago PMI, the regional Fed surveys reversed October’s improvement in contrast to their headline small improvement, whilst the S&P Global press release noted that “new order book growth weakened from October’s strong reading and therefore weighed on the PMI”.

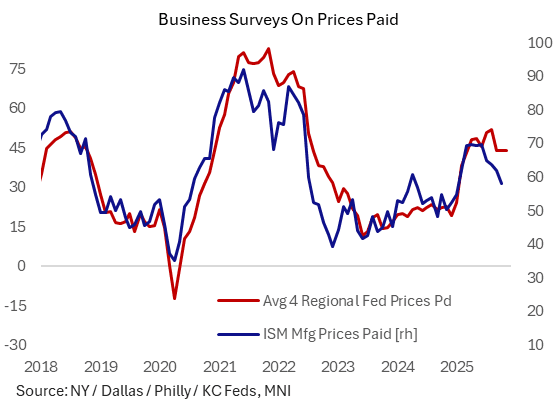

US OUTLOOK/OPINION: Net Upside Risks To ISM Mfg Prices Paid

- Bloomberg consensus sees the ISM manufacturing prices paid index slip 0.5pts to 57.5 after an almost 4pt drop in October and some large declines since 69.7 in June.

- It does however come from a typically small sample of just five responses (vs 42 responses for the headline manufacturing index) and we note that the regional Fed manufacturing surveys point to decent upside risk from a relative levels basis.

- Specifically, the prices paid average of four regional Fed surveys held steady around 44 for a third month in November (a level you can't directly translate to the ISM series). That’s down from 51.9 in August at what had been its highest since Jun 2022, but as the below chart shows there has seen less of a pullback in recent months although we're also cognizant of overshoots in the past.

- Elsewhere, the MNI Chicago PMI prices paid index increased nearly 6pts for its highest in four months although on the other hand the S&P Global PMI flash November release noted that “manufacturing input price inflation cooled to the lowest since February but remained well above the average seen over the past three years.”

UK FISCAL: Starmer claims government did not mislead on Budget runup

- Prime Minister Starmer has continued to argue that the government did not mislead regarding the fiscal black hole in the run up to the Budget. When asked about the OBR timeline, he pivots, pointing instead to the productivity downgrade costing GBP16bln, and that being a bad starting point. He does not acknowledge in his comments the total forecast adjustments.

- This appears to be a difficult claim. The OBR numbers are clear to see, and the timeline hasn't been denied by the government.

- It seems to leave four possible options: 1) Starmer genuinely believes he hasn't misled people (possibly difficult to argue given significant media coverage of the topic). 2) Starmer was complicit with Reeves and had planned this line all along. 3) Starmer feels he has no alternative to Reeves and has to protect her at all costs, and he thinks this will blow over. 4) Starmer and the media are arguing at cross purposes.

- The alternative would have been to communicate that there were two priorities: reducing child poverty and increasing fiscal headroom, and explaining that taxes would need to rise to do this. A clear outlining of this ahead of time could have saved significant political backlash, unless Starmer / Reeves are so worried about Reform UK that they did not want to risk any public backlash.

- It will be interesting to see whether there is any action taken over the allegations of misleading the market and breaches of the ministerial code. It seems as though Starmer and Reeves have opened themselves up to be vulnerable here for an unclear benefit.

FOREX: USDJPY Edges Through 20-day EMA Support

- USDJPY edges through the 155.26 20-day EMA support in recent trade after finding support at that level previously. Renewed pressure on the pair here would expose the 50-day EMA at 153.06 for direction - a level that could come into play should the pick-up in volumes at the NY crossover extend the hawkish JPY move.

- Ueda's comments overnight (namely his statement that raising rates should be seen as easing off the accelerator, rather than applying the brakes) keep December BoJ hike speculation in play, evident in market pricing for a hike rising to ~80% - up from around ~60% Friday. Perhaps notably, Ueda has also scheduled a speech to take place on December 25th - one week after the BoJ decision.

- The USD Index remains inside the S/T downtrend posted off the late November high (100.395), with support expected into the 98.992-99.063 area, which could contain any further decline in USDJPY.

- AUDUSD has pierced short-term trendline resistance at 0.6550, drawn from the Sep 17 high, after trading through its 20- and 50-day EMAs, undermining a recent bear theme. Current levels would mean the 7th consecutive session of gains for the pair. With the RBA cutting cycle likely over, AUD drivers ahead will be centred around global risk sentiment and the CNY - which continues to trade in a resilient fashion at fresh cycle highs against the dollar despite fresh property market woes reminding of concerns to the Chinese medium-term macro outlook.

- EUR meanwhile outperforms this morning after the November manufacturing PMIs highlighted renewed divergence between Germany/France and the rest of the region. EURUSD has breached both the 20- and 50-day EMAs, however, key short-term resistance to monitor is 1.1656, the Nov 13 high and a bull trigger.

- ISM Manufacturing will be the key datapoint today as private sector data remains more timely than the still-catching-up government stats. The USD Index remains inside the S/T downtrend posted off the late November high (100.395), with support expected into the 98.992-99.063 area, which could contain a further decline in USDJPY. BoE's Dhingra is also scheduled for today, and should be expected to remain with her dovish stance, while UK PM Keir Starmer is currently delivering a televised speech, addressing last week's Budget.

OPTIONS: Expiries for Dec01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E2.7bln), $1.1600(E1.5bln), $1.1795(E1.5bln)

- USD/JPY: Y155.00($744mln)

- GBP/USD: $1.2950(Gbp714mln)

- AUD/USD: $0.6550(A$522mln)

- USD/CAD: C$1.4025-30($1.1bln), C$1.4050($642mln)

EQUITIES: Move Lower for Eurostoxx Futures Last Week Undermines a Bearish Theme

- The move higher in Eurostoxx 50 futures last week undermines a recent bearish theme and the contract is holding on to most of its gains. Price has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5691.30 and 5742.40, Fibonacci retracement points. For bears, a reversal lower would instead expose the key S/T support and bear trigger at 5475.00, the Nov 21 low.

- S&P E-Minis are holding on to the bulk of their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

COMMODITIES: Trend Condition in Gold Remains Bullish, Key Resistance at $4381.50

- Recent weakness in WTI futures highlights a bearish theme. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. The contract has recovered from its latest low, resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. Note that the recovery since Oct 28 signals the end of the corrective cycle. Key support to watch lies at the 50-day EMA, at $3991.7. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 01/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 01/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/12/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 01/12/2025 | 1530/1530 | DMO to hold FQ4 consultations with investors / GEMMs | ||

| 01/12/2025 | 1530/1530 | BOE Dhingra Keynote at UK Trade Policy Observatory | ||

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 01/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/12/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 02/12/2025 | 0030/1130 | * | Building Approvals | |

| 02/12/2025 | 0030/1130 | Balance of Payments: Current Account | ||

| 01/12/2025 | 0100/2000 | Fed Chair Jerome Powell | ||

| 02/12/2025 | 0700/0700 | BOE Financial Stability Report | ||

| 02/12/2025 | 0745/0845 | Budget Balance | ||

| 02/12/2025 | 0900/1000 | Unemployment | ||

| 02/12/2025 | 1000/1100 | ** | EZ Unemployment | |

| 02/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 02/12/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 02/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 02/12/2025 | 1500/1000 | Fed Vice Chair Michelle Bowman | ||

| 03/12/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 03/12/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |