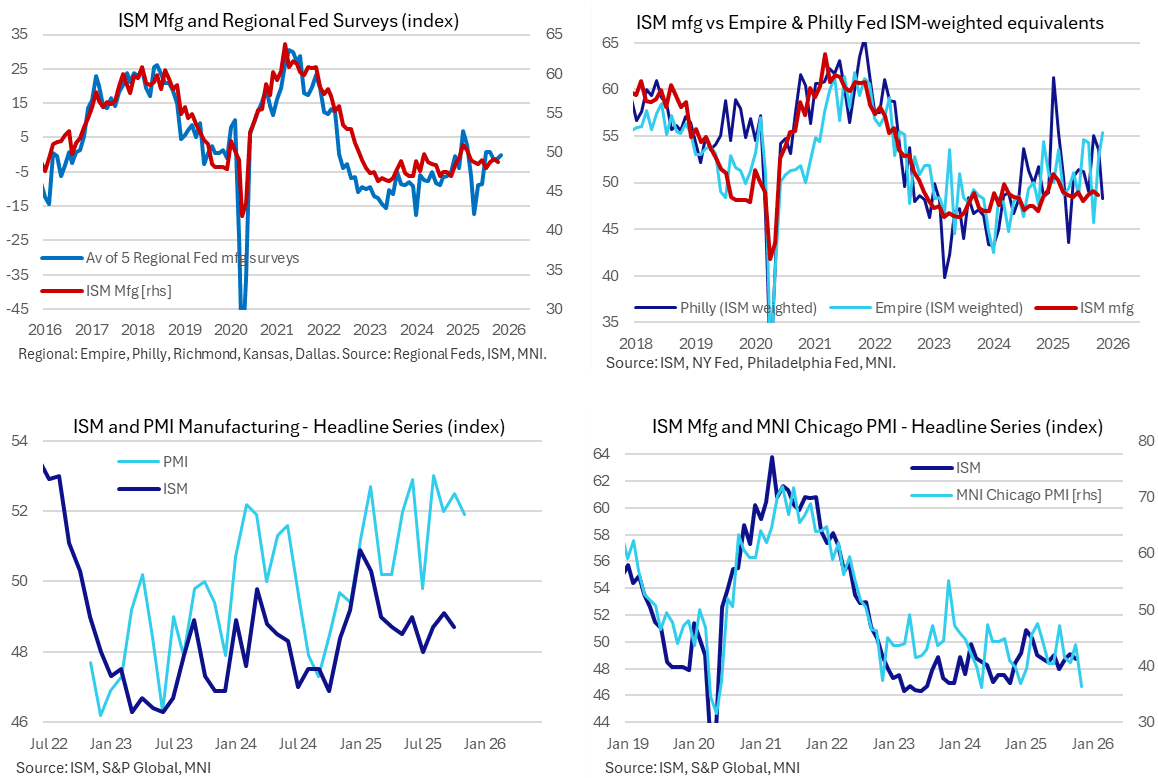

US OUTLOOK/OPINION: Two-Sided Risks For ISM Mfg, New Orders Look Softer

- Released at 1000ET today, the ISM manufacturing index is seen improving marginally to 49.0 in November having dipped 0.4pts to 48.7 in Oct.

- It has kept to a narrow range of 48.0-49.1 since March having eased back from Jan and Feb seeing the first months above 50 (i.e. in expansionary territory) since late 2022, with a high of 50.9 in Jan.

- Alternate indicators are mixed, justifying the limited improvement expected.

- Regional Fed surveys: mild upside. The average of the five regional Fed surveys increased from -1.0 to -0.1 although it’s essentially flatlined around its breakeven 0 line for six months now. The ISM equivalent readings of the Empire and Philly Fed surveys fell to 51.8 from 53.1 (highest since Feb) after a 5.2pt drop in the Philly version but continue to point to upside risk from a levels basis.

- S&P Global PMI: downside momentum, upside level. The flash survey eased from 52.5 to 51.9 in November to take it a little further away from the 53.0 in August that had been a multi-year high. It has averaged 2.6pts higher than the ISM survey so far this year, but by firmly differing amounts (between 0.3-4.3pts).

- MNI Chicago PMI: firm downside. It slumped 7.5pts to 36.3 in November for its second lowest since mid-2020 whilst new orders saw their largest one-month fall since Sep 2023.

- However, new orders indicators look a little more uniformly soft and could fall more materially below the 50-mark after 49.4 in Nov (its 51.4 in Aug was its highest since Jan). On top of that sharp drop in the MNI Chicago PMI, the regional Fed surveys reversed October’s improvement in contrast to their headline small improvement, whilst the S&P Global press release noted that “new order book growth weakened from October’s strong reading and therefore weighed on the PMI”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.670 @ 16:16 GMT Oct 31

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower Wednesday on the back of hotter-than-expected Australian inflation. This returned prices lower despite nascent signs of a technical recovery as recently as last week. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.375 @ 16:13 GMT Oct 31

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course Wednesday on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

FED: Gov Waller: Still Advocating For A December Rate Cut

Gov Waller, one of the FOMC's more prominent doves, makes clear in an appearance on Fox Business that he supports a follow-up rate cut in December. He makes reference to Chair Powell's press conference comment that the Fed could skip a cut at the December meeting due in part to a lack of official government data during the federal shutdown (Powell: “what do you do if you are driving in the fog? You slow down").

- Waller says today: "Right now, we know that the labor market has been weak... We know inflation is going to come back down. Inflation expectations are anchored, and in that world, the standard of central bank wisdom is to look through it and proceed with worrying about the labor market. So in my view, we should just look at what the data is telling us and proceed on policy that way.... So this is why I'm still advocating that we cut policy rates in December, because that's what all the data is telling me to do. The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and ... the right thing to do with policy is to continue cutting."

- This is of particular interest since he appeared to suggest he would have a more cautious outlook on further easing after cutting in October.