MNI US MARKETS ANALYSIS: USD Softer With Fed Positions Watched

Highlights

- USD softens ahead of NY trade, Fed personnel matters remain in focus

- US fixed income markets await a busy mid-week with a Fed cut fully priced

- Sino-U.S. tension surrounding Nvidia noted, Empire manufacturing & ECB's Lagarde due.

FED: MNI Fed Preview-September 2025: A Reluctant Return To Easing

We've published our preview of the upcoming FOMC meeting - Hidden PDF

- The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The Statement will downgrade the description of the labor market to reflect a rise in the unemployment rate and poor payrolls growth, and is likely to include at least one dissent to the rate decision.

- But with a Committee that is fairly divided on the way forward, Powell will be noncommittal on future action, reiterating that policy is not on a preset course, and upcoming decisions will be data-dependent.

- A key undercurrent is an increasingly activist approach to Fed personnel management from the White House, which leaves the composition of the FOMC uncertain not just over the medium-term but also at this meeting.

- MNI’s separate preview of sell-side analyst summaries to follow later today.

US TSYS: Back Little Changed, Politics Including Fed Positions In Focus Today

- Treasuries are on balance little changed from Friday’s close, with cash having firmed through European trading are opening a little lower following a Japan holiday.

- Cash yields are 0.5bp lower (3s) to 0.7bp higher (7s).

- Curves for now holds last week’s flattening, including 5s30s at 105.7bps vs fresh multi-year highs of ~127bps after the August payrolls report two weeks ago.

- TYZ5 trades at 113-07+ (-01+) on thin volumes only just approaching 200k, having eased back from a session high of 113-10.

- Some might look to initial resistance at 113-15+ but a firmer level is seen at 113-29 (Sep 5 high), with a bullish trend sequence in play. Support meanwhile is seen at 112-23+ (20-day EMA).

- Data: Empire Mfg Sep (0830ET)

- Fed positions: Miran confirmation votes (~1730/2000ET) and Cook case – see STIR bullet

- Bill issuance: US Tsy $82B 13W & $73B 26W bill auctions (1130ET)

- Politics: Trump meets Ecumenical Patriarch Bartholomew (1400ET), Trump signs Presidential Memorandum (1600ET). Today also sees a second day of Bessent-He talks in Madrid, with a press conference potentially in the European afternoon

STIR: Fed Personnel Deliberations Watched Later On

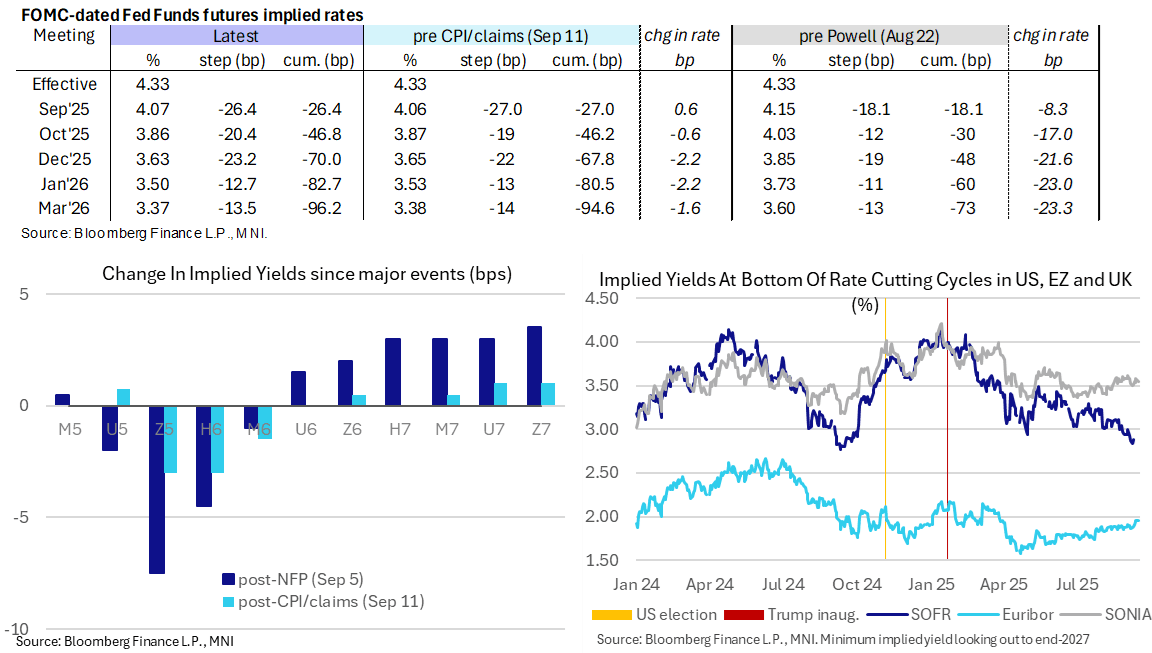

- Fed Funds implied rates for near-term meetings are near unchanged since Friday’s close.

- Two Fed personnel deliberations today:

- Senate cloture vote on CEA’s Miran nomination as a Fed Governor at ~1730ET before full confirmation voter ~2000ET. Expected to pass having already passed 13-11 in the Senate Banking Committee.

- Watching for a reaction after the Trump administration on Sunday filed an appeal for a stay on a lower court block on Gov Cook's firing, a long-shot bid to remove Cook ahead of the FOMC meeting. The administration previously asked for a ruling by today. While unlikely, the Trump administration is targeting an emergency ruling from the Supreme Court on the so-called 'shadow docket'.

- Data picks up tomorrow with retail sales whilst the FOMC decision of course looms large on Wednesday.

- Cumulative cuts from 4.33% effective: 26.5bp Sep, 47bp Oct, 70bp Dec, 82.5bp Jan and 96bp Mar.

- SOFR futures see minor twist flattening, 1 tick lower in the U5 to 1.5 ticks firmer through 2027 contracts.

- The SOFR implied terminal yield of 2.915% (SFRH7, -1.5bp) remains off last Monday’s close of 2.84% (lowest since Sep 2024 and one of the lowest for the cycle) but still points to more than 140bp of cuts ahead.

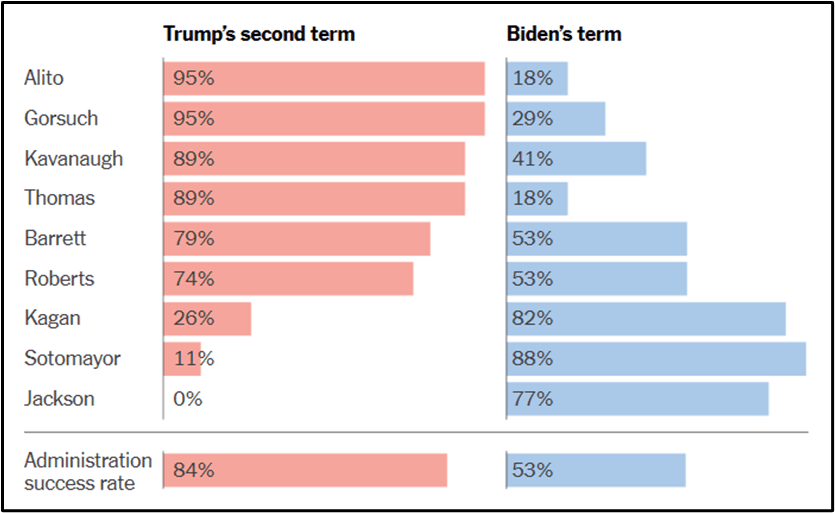

US: Miran Set For Fed Confirmation Tonight, Trump Eyes Final Push To Remove Cook

The Senate is on track to confirm Stephen Miran to the Federal Reserve Board this evening, seating the CEA Chair in time for the Fed’s two-day rate-setting meeting that kicks off on Tuesday.

- The Senate will hold a cloture vote on Miran’s nomination at around 17:30 ET 22:30 BST, with a full confirmation vote likely to take place at roughly 20:00 ET 01:00 BST. Despite some reservations from institutionalist Senate Republicans, there is not expected to be any GOP opposition.

- Meanwhile, on Sunday, the Trump administration filed an appeal for a stay on a lower court block on Governor Lisa Cook’s firing, a long-shot bid to remove Cook ahead of the FOMC meeting.

- While unlikely, the Trump administration is targeting an emergency ruling from the Supreme Court on the so-called ‘shadow docket’. For this to play out, the three-judge appeals panel would need to deny the DOJ’s request, allowing Trump to immediately call on the Supreme Court to intervene.

- The New York Times writes in an analysis of the ‘shadow docket’, “In their public appearances, the justices try to counter the perception that they favor the agenda of the party of the president who appointed... The emergency docket presents a different portrait of the court, one in which partisan affiliations map onto voting patterns quite closely…”

Figure 1: Emergency Docket Rulings by Justice

Source: New York Times

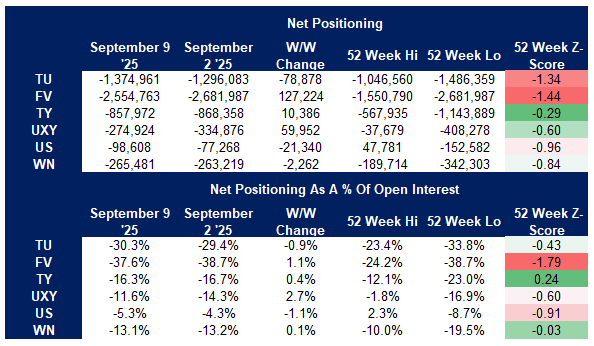

US TSY FUTURES: CFTC Shows Asset Managers & Funds Build On Existing Positioning

The latest CFTC CoT report showed asset managers building on their net long position in the week ending September 9, with net long setting in FV, TY, US & WN futures comfortably outweighing net long cover in TU & UXY futures. The cohort added a net ~$8.6mln DV01 of risk across the curve and remains net long all contracts.

- Leveraged funds added modestly to their existing net short, with net short setting in TU, FV, TY & WN futures mostly cancelled out by short cover in UXY & US futures. This meant that the cohort added ~$1.2mln of fresh curve-wide risk on the week and remains net short across the curve.

- Broader non-commercial investors added to net shorts in the wings (TU, US & WN futures), while they trimmed net shorts in the belly and intermediates (FV, TY & UXY).

- Greater details covering non-commercial positioning moves can be found in the table below.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

US TSY FUTURES: Net Long Cover Most Prominent On Friday

OI data points to a mix of net long cover (TU, FV, UXY, US & WN) and short setting (TY) as Tsy yields pulled away from recent lows on Friday. Net long cover was comfortably more prominent in curve-wide terms.

| 12-Sep-25 | 11-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,485,334 | 4,494,228 | -8,894 | -360,593 |

FV | 6,819,380 | 6,841,853 | -22,473 | -999,406 |

TY | 5,372,837 | 5,367,855 | +4,982 | +341,293 |

UXY | 2,365,713 | 2,372,134 | -6,421 | -586,746 |

US | 1,807,094 | 1,818,959 | -11,865 | -1,697,898 |

WN | 2,011,771 | 2,016,360 | -4,589 | -864,949 |

|

| Total | -49,260 | -4,168,298 |

SOFR: Mix Of Short Setting & Long Cover In Futures On Friday

OI data points to a mix of net short setting (in the whites) and net long cover (in the reds, greens & blues) as SOFR futures ticked lower on Friday.

| 12-Sep-25 | 11-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,231,643 | 1,225,409 | +6,234 | Whites | +28,291 |

SFRU5 | 1,487,469 | 1,473,429 | +14,040 | Reds | -13,380 |

SFRZ5 | 1,670,579 | 1,666,022 | +4,557 | Greens | -18,268 |

SFRH6 | 1,200,040 | 1,196,580 | +3,460 | Blues | -21,589 |

SFRM6 | 1,005,633 | 1,015,971 | -10,338 |

|

|

SFRU6 | 910,870 | 889,115 | +21,755 |

|

|

SFRZ6 | 1,014,912 | 1,033,649 | -18,737 |

|

|

SFRH7 | 709,949 | 716,009 | -6,060 |

|

|

SFRM7 | 823,158 | 849,677 | -26,519 |

|

|

SFRU7 | 692,056 | 690,088 | +1,968 |

|

|

SFRZ7 | 690,926 | 686,161 | +4,765 |

|

|

SFRH8 | 447,757 | 446,239 | +1,518 |

|

|

SFRM8 | 362,224 | 357,038 | +5,186 |

|

|

SFRU8 | 251,991 | 273,387 | -21,396 |

|

|

SFRZ8 | 259,301 | 260,820 | -1,519 |

|

|

SFRH9 | 182,320 | 186,180 | -3,860 |

|

|

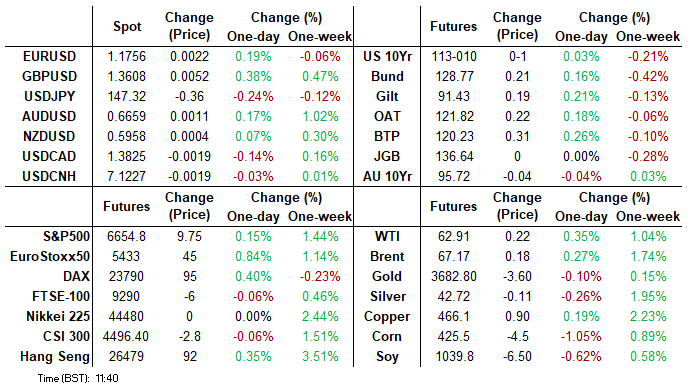

FOREX: Dollar Index Tilts Lower, GBPUSD Rises Above 1.3600

- The dollar index has been edging lower heading into the NY crossover on Monday, as markets await a stacked data and central bank calendar this week, headlined by the Fed. Amid the moves, GBP is a clear outperformer, with cable rising above 1.3600 to a fresh two-month high.

- Bullish conditions for GBPUSD have been bolstered this morning, following the break of the bull trigger located at 1.3595, the August 14 high. The rally that started Sep 3 has retraced the steep Sep 2 sell-off and highlights a stronger bullish development. This suggests the corrective cycle between Aug 14 - Sep 3 is over.

- Immediate resistance is found at 1.3636, the 76.4% retracement of the Jul 1 - Aug 1 downleg, before 1.3681, the Jul 4 high.UK Labour market figures, CPI data and the BOE decision will place a huge amount of attention on sterling this week.

- Softer dollar dynamics have also allowed AUDUSD to rise back towards cycle highs. Last week’s gains plus the breach of 0.6625, the Jul 24 high and bull trigger, confirmed a resumption of the technical uptrend, and the pair has narrowed the gap substantially to the US election related highs at 0.6688.

- In similar vein, EURUSD has edged higher above 1.1750 in recent trade. While underlying bullish conditions remain intact for EURUSD, this week’s Fed decision could be a pivotal moment for the pair, with the 1.1829 bull trigger and the 50-day EMA (intersecting at 1.1639) remaining the key short-term parameters.

- US Empire State manufacturing data headlines a relatively quiet economic calendar on Monday. No surprises are expected from ECB President Lagarde, due to speak at Montaigne Institute’s 25th anniversary event, in Paris.

FOREX OPTIONS: Expiries for Sep15 NY cut 1000ET (Source DTCC)

- EURUSD: 1.1650 (794mln), 1.1690 (967mln), 1.1700 (538mln), 1.1735 (266mln), 1.1750 (553mln), 1.1800 (731mln)

- GBPUSD: 1.3500 (776mln)

- USDJPY: 147.50 (265mln), 147.70 (541mln)

- USDCAD: 1.3850 (323mln)

EQUITIES: EUROSTOXX50 Recovery Extends

- A bull cycle in S&P E-Minis remains intact and last week’s fresh cycle highs reinforce current conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6685.25, a 1.00 projection of the Aug 1 - 15 - 20 price swing, and the 6700.00 handle. Initial support to watch is 6547.03, the 20-day EMA. A corrective bear cycle in EUROSTOXX 50 futures remains in play. Recent weakness resulted in a breach of 5370.21, the 50-day EMA. A clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development for now. A stronger rally would expose 5522.0, the Aug 26 high.

COMMODITIES: Gold Bulls Remain In The Driver's Seat

- Gold remains in a clear bull cycle and continues to trade at its recent highs. The yellow metal traded to a fresh all-time high once again, last week. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a 2.382 projection of the Dec 30 ’24 - Apr 3 - 7 price swing. Initial firm support lies at $3504.1, the 20-day EMA. Initial firm support lies at $3504.1, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 15/09/2025 | 1130/1330 | ECB Schnabel At EIB Chief Econ Meeting | ||

| 15/09/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/09/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/09/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/09/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 15/09/2025 | 1810/2010 | ECB Lagarde at Institut Montaigne Paris | ||

| 15/09/2025 | - | FOMC Meetings with S.E.P. | ||

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0800/1000 | *** | HICP (f) | |

| 16/09/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/09/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond |