MNI US MARKETS ANALYSIS: USD Off Highs Ahead Of Fedspeak

Highlights:

- USD index eases off recovery highs

- European equities tick lower

- Fedspeak & comments from BoE's Pill eyed

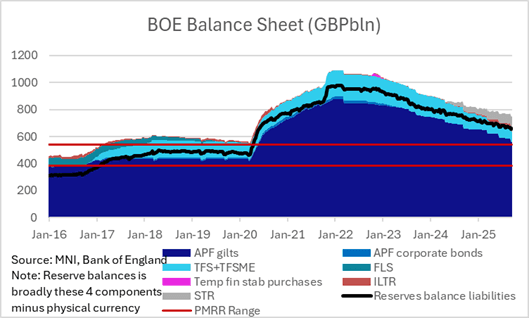

MNI BOE Review: Sep 2025 - Nothing to change Q4 expectations

For the full MNI BOE Review, including updated summaries of over 20 sell side analysts click here.

- With guidance unchanged, the 7-2 vote as expected and little new of note in the Minutes we think there should have been little to change the prospect of a Q4-25 cut in the September MPC meeting.

- However 10/21 sell side analysts that we track have pushed back their expectations of the timing of their next cut (albeit analysts still remain more dovish overall than market pricing).

- We think that markets under-price the prospect of both a November and a December cut.

- We look at the implications of the decision to target a GBP70bln APF reduction over the next year and will be watching ILTR / STR operations closely in coming weeks as supply-led reserve balances move below the top of the Bank's PMRR (preferred minimum range of reserves).

US TSYS: Inside Friday Range, Several Fed Speakers on Light Data Docket

Treasuries drifting near the top end of a narrow overnight range - near the middle of Friday's range

- TYZ5 trades at 112-25.5 (+1.5) on thin cumulative volumes of 217k. 10Y yield +.0019 at 4.1293%.

- The pullback in Treasury futures from their recent highs appear corrective. Price has moved through the 20-day EMA, at 112-28+. The break signals scope for a deeper retracement and attention turns to the 50-day EMA, at 112-08+ and the next key support. Resistance well above at 113-29, Sep 11 high and the bull trigger.

- Data: Limited to Chicago Fed National Activity Index at 0830ET, Bbg survey estimate -0.16 est from -0.19 prior.

- Fedspeak: NY Fed Williams on monetary policy (0945ET), StL Fed Musalem on economy & policy from Brookings Inst (1000ET), Cleveland Fed Hammack on banks & economy (1200ET), Richmond Fed Barkin (1200ET), Fed Gov Miran moderated Q&A from Economic Club/NY (1200).

- Politics: Congress has departed for a week-long recess without a plan to fund the federal government (Senate blocked a CR bill Friday after the House passed the measure. Senate Majority Leader Thune (R-SD) is expected to delay a second CR vote until September 29, exerting as much pressure on Democrats as possible.

- At 1300ET, Press Briefing by the White House Press Secretary Karoline Leavitt.

- At 1600ET, President Trump expected to make an announcement on Significant Medical and Scientific Findings for America's Children.

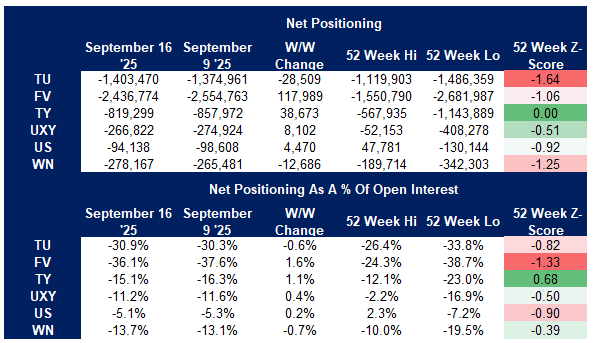

US TSY FUTURES: CFTC CoT Points to Reduction In Positioning Across Funds & AMs

Aggressive net long cover in US futures (~$9.6mln DV01) meant that asset managers reduced their curve-wide net long position by a little over $7mln on the week, with net long cover also seen in FV & TY futures, while there was net long setting in TU, UXY & WN futures. The cohort remains net long across all contracts.

- Leveraged funds lightened their curve-wide net short by ~$3.1mln DV01, with instances of net short cover (FV, TY & US) comfortably outweighing instances of net short setting (TU, UXY & WN). The cohort remains net short across the curve.

- Non-commercial accounts added to net shorts in the wings (TU & WN), while they covered some of their existing short position across the remainder of the curve. The cohort remains net short across all contracts. See table below for more details on the cohort’s positioning.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen Friday

OI data points to a mix of net long cover (FV, UXY, US & WN) and short setting (TU & TY) during Friday’s downtick in Tsy futures, with the curve-wide net DV01 ultimately little changed on the day.

- Net short setting in TU futures provided the most prominent move on the curve (~$2mln DV01).

| 19-Sep-25 | 18-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,549,540 | 4,499,244 | +50,296 | +2,019,481 |

FV | 6,736,872 | 6,745,323 | -8,451 | -373,445 |

TY | 5,396,507 | 5,396,323 | +184 | +12,516 |

UXY | 2,373,804 | 2,378,248 | -4,444 | -402,855 |

US | 1,820,922 | 1,826,004 | -5,082 | -719,076 |

WN | 2,014,280 | 2,018,444 | -4,164 | -771,952 |

|

| Total | +28,339 | -235,332 |

SOFR: Short Setting & Long Cover In Futures On Friday, No Notable Themes

OI data points to a mix of net long cover and short setting in SOFR futures on Friday, as contracts finished flat to lower.

- There wasn’t much in the way of meaningful themes to highlight, with most positioning swings proving to be fairly limited.

| 19-Sep-25 | 18-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,468,061 | 1,460,339 | +7,722 | Whites | +42,602 |

SFRZ5 | 1,570,799 | 1,564,152 | +6,647 | Reds | -22,359 |

SFRH6 | 1,169,874 | 1,152,319 | +17,555 | Greens | +5,845 |

SFRM6 | 1,044,435 | 1,033,757 | +10,678 | Blues | -4,148 |

SFRU6 | 938,525 | 940,105 | -1,580 |

|

|

SFRZ6 | 1,034,680 | 1,043,224 | -8,544 |

|

|

SFRH7 | 743,217 | 756,465 | -13,248 |

|

|

SFRM7 | 813,709 | 812,696 | +1,013 |

|

|

SFRU7 | 662,156 | 657,465 | +4,691 |

|

|

SFRZ7 | 709,833 | 708,883 | +950 |

|

|

SFRH8 | 438,357 | 434,949 | +3,408 |

|

|

SFRM8 | 354,151 | 357,355 | -3,204 |

|

|

SFRU8 | 269,667 | 272,951 | -3,284 |

|

|

SFRZ8 | 296,047 | 294,487 | +1,560 |

|

|

SFRH9 | 186,977 | 189,131 | -2,154 |

|

|

SFRM9 | 176,221 | 176,491 | -270 |

|

|

EUROPEAN ISSUANCE UPDATE

EU-Bond Auction Results:

- E2.1bln of the 3.125% Dec-28 EU-bond. Avg yield 2.302% (bid-to-cover 1.33x)

- E1.659bln of the 3.375% Dec-35 EU-bond. Avg yield 3.189% (bid-to-cover 1.43x)

- E1.317bln of the 2.625% Feb-48 Green EU-bond. Avg yield 3.883% (bid-to-cover 1.26x)

OLOs Auction Results:

E933mln of the 0.10% Jun-30 OLO. Avg yield 2.525% (bid-to-cover 2.23x).

E952mln of the 3.10% Jun-35 OLO. Avg yield 3.248% (bid-to-cover 2.20x).

E726mln of the 2.75% Apr-39 Green OLO. Avg yield 3.595% (bid-to-cover 2.03x).

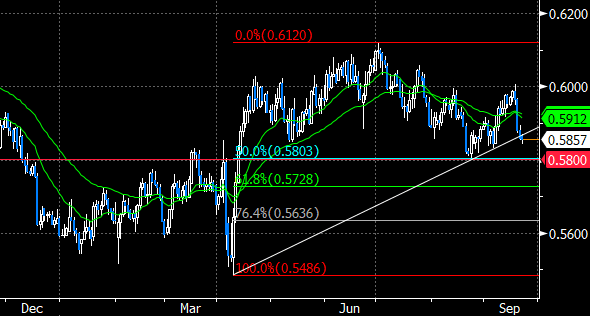

FOREX: Latest NZDUSD Leg Lower Renews Focus on 0.5800

NZDUSD tracks a 0.07% lower to start the week, relatively underperforming its G10 peers as the likes of EUR and GBP trade on a surer footing. Kiwi weakness was well documented last week following the much weaker-than-expected GDP figures that have raised the odds of the RBNZ more aggressively easing in Q4.

- Notably, Kiwibank now expect a 50bp cut in October followed by a 25bp cut in November so that the cash rate ends the year at 2.25%. They note "It has become crystal clear that the Kiwi economy is not recovering" and "the Reserve Bank needs to do more." Additionally, ongoing leadership woes add to urgency for kiwi dollar and rates traders to closely scrutinize the changing of the guard at RBNZ, according to TD.

- For NZDUSD, the sharp reversal from 0.6000 to current spot levels renews the focus on a significant pivot point at 0.5800, which coincides with the 50% retracement of the year’s range. Furthermore, the pair is currently trying to break a trendline drawn from the year’s lows, which may bolster the bearish momentum in coming sessions. Below 0.5800, 0.5728 and 0.5636 would be the most obvious targets for a deeper selloff.

- A lot of focus in recent weeks has been on the impressive breakout for AUDNZD, emboldened last week by the cross breaking to near 3-year highs above 1.1180, despite softer Australian jobs data. Since then, spot has been consolidating around 1.1250. Resistance appears scant until the 2022 highs, located at 1.1491.

- The domestic calendar is light this week, with ANZ consumer confidence for September due Friday.

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: USD Index Eases Off Recovery Highs, Fed Speakers Awaited

The USD index tracks moderately lower on Monday, easing around 30 pips from the overnight peak that saw the index print a fresh recovery high at 97.82. Markets are trading with a subdued tone amid a lighter economic calendar to start the week, with central bank speakers dominating the schedule later today.

- The likes of EUR and GBP trade on a surer footing, rising around 0.15%. Large option expiries for EURUSD between the 1.17/18 mark might define the short-term range, following the post-Fed volatility last week that saw the pair reverse from 1.1919 cycle highs. Support to watch is 1.1667. the 50-day EMA.

- GBPUSD is broadly consolidating its solid bump lower last week, struggling to get back above the 1.35 mark. Fiscal concerns continue to be front and centre following last Friday’s borrowing data. The next support to watch lies at 1.3441, a trendline support drawn from the Aug 1 low.

- For NZDUSD, the sharp reversal from 0.6000 to current spot levels renews the focus on a significant pivot point at 0.5800, which coincides with the 50% retracement of the year’s range. Furthermore, the pair is currently trying to break a trendline drawn from the year’s lows, which may bolster the bearish momentum in coming sessions. Below 0.5800, 0.5728 and 0.5636 would be the most obvious targets for a deeper selloff.

- There are five Fed speakers in the calendar on Monday, with markets most likely to focus on further comments from Fed’s Miran, who is speaking at the Economic Club of New York. We may also have comments from Bank of England’s Bailey and Pill. Governor Bailey has a fireside chat on supervision culture.

FOREX OPTIONS: Expiries for Sep22 NY cut 1000ET (Source: DTCC)

- EURUSD: 1.1700 (583mln), 1.1720 (626mln), 1.1730 (630mln), 1.1745 (559mln), 1.1770 (461mln), 1.1775 (260mln), 1.1780 (245mln), 1.1790 (465mln), 1.1800 (1.14bn)

- GBPUSD: 1.3500 (393mln)

- USDJPY: 148.35 (350mln)

- USDCAD: 1.3800 (519mln)

- AUDUSD: 0.6600 (547mln)

EQUITIES: S&P Bull Cycle Remains In Play

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Friday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a 1.236 projection of the Aug 1 - 15 - 20 price swing. Initial support to watch lies at 6602.01, the 20-day EMA.

- EUROSTOXX 50 futures recently traded through resistance around the 20-day EMA - a bullish development - and the subsequent rally reinforces a bullish theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. First support lies at 5405.03, the 20-day EMA.

COMMODITIES: Bear Threat In Oil Futures Remains Present

Gold remains in a clear bull cycle. A fresh all-time high once again, today, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3744.2, a 1.500 projection of the May 15 - Jun 16 - 30 price swing. Initial firm support lies at $3577.9, the 20-day EMA.

- The trend condition in WTI is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 22/09/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/09/2025 | 1230/1330 | BOE Pill At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/1545 | ECB Lane At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/0945 | New York Fed's John Williams | ||

| 22/09/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 22/09/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/09/2025 | 1600/1200 | Cleveland Fed's Beth Hammack | ||

| 22/09/2025 | 1600/1200 | Richmond Fed's Tom Barkin | ||

| 22/09/2025 | 1715/1315 | BOC Sr Deputy speaks at LSE panel on supervision | ||

| 22/09/2025 | 1800/1900 | BOE Bailey Fireside Chat On Supervision | ||

| 22/09/2025 | 1945/1545 | BOC Deputy Kozicki speaks at BIS panel on central bank frameworks | ||

| 23/09/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 23/09/2025 | - | Riksbank Meeting | ||

| 23/09/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/09/2025 | 0900/1000 | BOE Pill Fireside Chat At Pictet Research Institute Symposium | ||

| 23/09/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/09/2025 | 1230/0830 | * | Current Account Balance | |

| 23/09/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/09/2025 | 1300/0900 | Fed Governor Michelle Bowman | ||

| 23/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/09/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/09/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 23/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/09/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 23/09/2025 | 1420/1620 | ECB Cipollone In Bloomberg Fireside Chat | ||

| 23/09/2025 | 1635/1235 | Fed Chair Jay Powell | ||

| 23/09/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 23/09/2025 | 1815/1415 | BOC Governor Macklem speech in Saskatoon |