MNI BOE Review: Sep 2025 - Nothing to change Q4 expectations

Sep-22 06:34By: Tim Davis

UKFiscal PolicyGovernment Sovereign BondsEGBs

Hidden PDF

- With guidance unchanged, the 7-2 vote as expected and little new of note in the Minutes we think there should have been little to change the prospect of a Q4-25 cut in the September MPC meeting.

- However 10/21 sell side analysts that we track have pushed back their expectations of the timing of their next cut (albeit analysts still remain more dovish overall than market pricing).

- We think that markets under-price the prospect of both a November and a December cut.

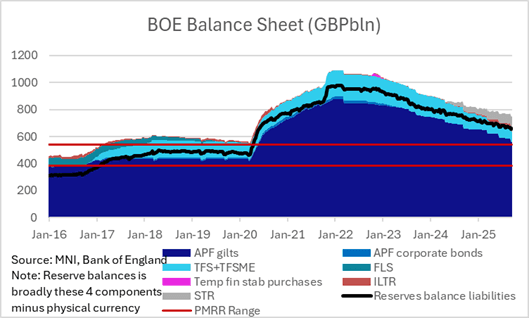

- We look at the implications of the decision to target a GBP70bln APF reduction over the next year and will be watching ILTR / STR operations closely in coming weeks as supply-led reserve balances move below the top of the Bank's PMRR (preferred minimum range of reserves).

Related stories

Related by topic

UK

Fiscal Policy

Government Sovereign Bonds

EGBs

Trending Top

Jun-26 16:22