MNI US MARKETS ANALYSIS - US CPI in Focus, Earnings Begin

Highlights:

- US CPI in focus, market watches for clues on tariff passthrough

- Earnings season unofficially begins, with Citigroup set to follow JP Morgan, Wells Fargo today

- Moscow says will have assess Trump's statement on Ukraine talks

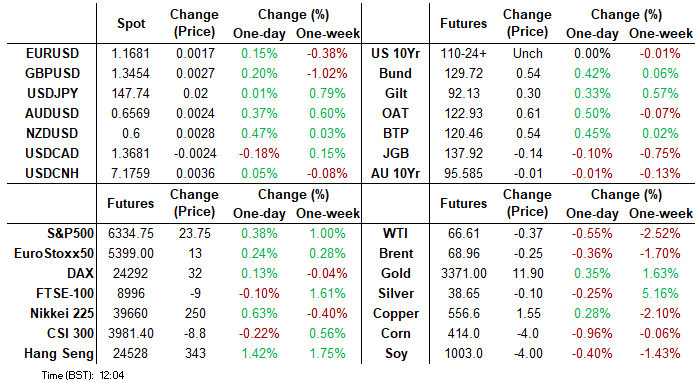

US TSYS: Mildly Bull Flatter Ahead Of CPI, TYA Support Watched

- Treasuries are bull flatter on the day, with the front end pinned ahead of the US CPI report for June at 0830ET but the long end gaining as it lags an EGB rally on no obvious drivers.

- Cash yields are unchanged to 2.5bp lower, with declines led by 20s.

- TYU5 sits a touch firmer at 110-25+ (+ 01) on light cumulative volumes of 235k, having remained within yesterday’s range throughout.

- Yesterday touched 110-20 in a further move closer to a key support at 110-17 (61.8% of May 22- Jul 1 bull leg). Further support would then be at 110-10+ (Jun 16 low) whilst resistance is seen at 111-13+ (Jul 10 high).

- Data: CPI June (0830ET), Real avg hourly earnings Jun (0830ET), Empire mfg Jul (0830ET)

- Fedspeak: Bowman (0915ET), Barr (1245ET), Barkin (1300ET), Collins (1445ET), Logan (1945ET) – see STIR bullet.

- Bill issuance: $70B 6W bill auction (1130ET)

- Bank earnings: BNY Mellon, JPM and Wells Fargo have recently reported, with Citigroup still to come (0800ET).

- Trump calendar per Roll Call: Departs White House en route to Pittsburgh (1230ET with open press), Participates in Inaugural Pennsylvania Energy and Innovation Event (1430ET with pre-credentialed media).

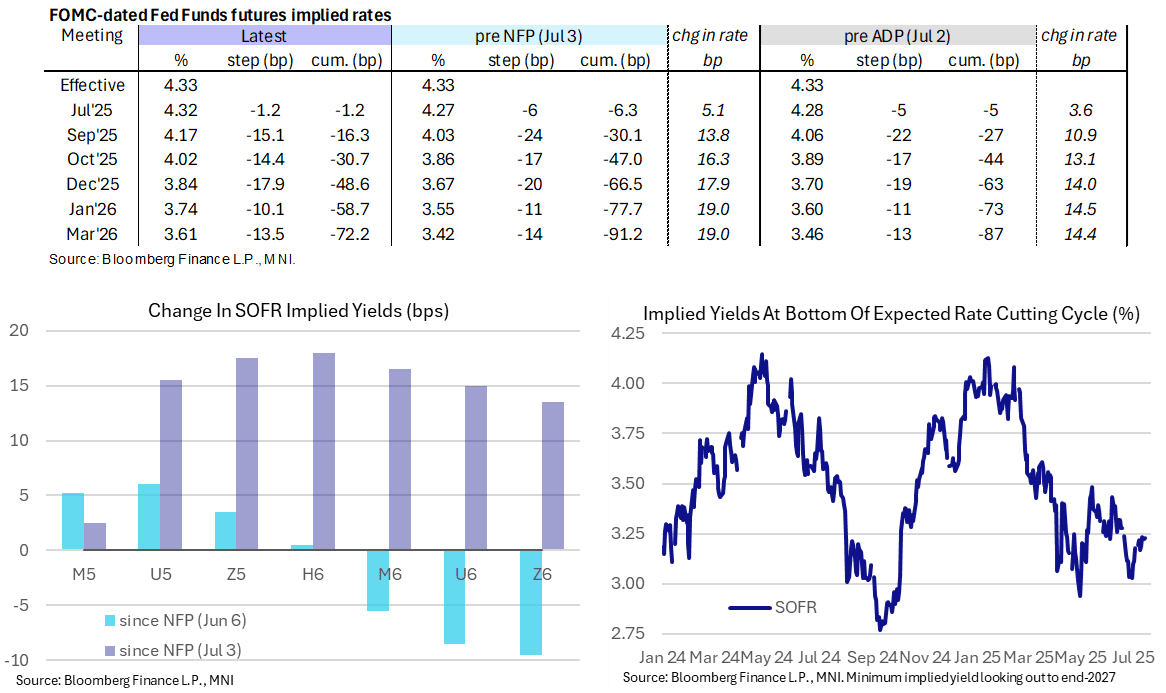

STIR: US CPI In Focus, Might Be A Wait To Hear FOMC Reaction

- Fed Funds implied rates are almost unchanged from yesterday’s close ahead of the June CPI report at 0830ET, with a next cut fully priced for the October FOMC.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Jul2025_07eaecc8d6.pdf

- Cumulative cuts from 4.33% effective: 1bp Jul, 16.5bp Sep, 30.5bp Oct, 48.5bp Dec, 58.5bp Jan and 72bp Mar.

- SOFR futures are also little changed, including terminal yields at 3.23% (SFRZ6, +0.5bp).

- There are multiple Fed appearances after the CPI release but we’ll likely have to wait until Barkin’s Q&A for the first reaction, at least from those scheduled to speak. After that, there’s a chance Collins will include some mention in her prepared remarks but we’re more likely to hear notable comments from Logan (hawk) after the close.

- 0915ET – VC Supervision Bowman (voter) welcoming remarks at Fed financial conference (text only). We’ll watch to see if she appears on newswires either side of this conference after her recent surprisingly dovish pivot saw her as probably one of the two dots looking for three cuts in what’s left of 2025.

- 1245ET – Gov. Barr (voter) on financial inclusion (text only)

- 1300ET – Richmond Fed’s Barkin (non-voter) repeats speech on “Forecasting beyond today’s data” (text + Q&A)

- 1445ET – Boston Fed’s Collins (’25 voter) closing keynote at NABE event (text only)

- 1945ET – Dallas Fed’s Logan (’26 voter) speaks on the economy (text + Q&A)

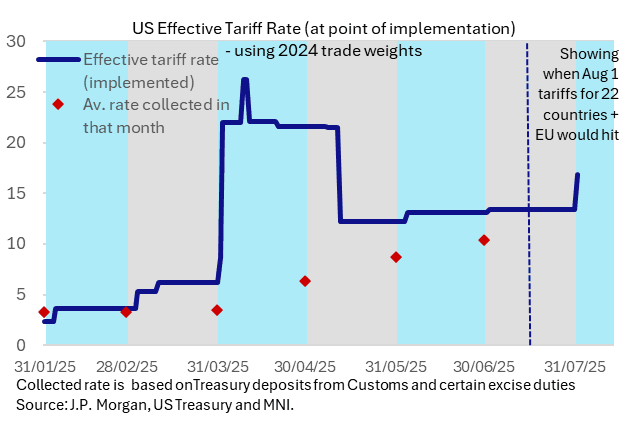

US OUTLOOK/OPINION: An Addendum To MNI US CPI Preview On Tariff Rates

- The below bullet is an addendum to the MNI US CPI Preview that was sent out yesterday (found here)

- It adds color to the section on the timing and magnitude of tariff hits, especially the remarks San Francisco Fed’s Daly made in a MNI webinar last week about the tariff collections data tracking below expected effective tariff rates.

- The static analysis takes effective tariff rates from J.P. Morgan calculations, in the chart below showing them at point of implementation rather than actual announcement, and compares them with average collection rates over the course of that month using US Treasury data for deposits from customs and certain excise duties.

- The latest message is similar to that from Daly: tariff collections data showed an average rate of ~10% in June after nearly 9% in May and 6% in April vs an effective rate of ~13% in June but one which could be 17% with new reciprocal tariffs slated for Aug 1; Daly referenced 8-9% collection rates vs an expected effective tariff rate of ~16%. The below also offers a useful look at how this has incrementally increased over time.

- It doesn’t however give insight into burden sharing across importers, businesses and consumers, something we go more into in the main preview.

SOFR: Mix Of Positoning Swings In Futures On Monday

OI data points to net short setting in SFRM5 on Monday, before a mix of net long setting and short cover came to the fore in SFRZ5 through SFRZ7.

- It is hard to provide any real inference outside of those moves, as the remainder of the strip (through the blues) was flat come settlement, in price terms.

| 14-Jul-25 | 11-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,297,183 | 1,295,120 | +2,063 | Whites | +60,956 |

SFRU5 | 1,253,866 | 1,204,748 | +49,118 | Reds | +25,676 |

SFRZ5 | 1,300,625 | 1,307,463 | -6,838 | Greens | -23,105 |

SFRH6 | 995,532 | 978,919 | +16,613 | Blues | -1,626 |

SFRM6 | 872,692 | 845,808 | +26,884 |

|

|

SFRU6 | 812,013 | 827,598 | -15,585 |

|

|

SFRZ6 | 899,723 | 880,570 | +19,153 |

|

|

SFRH7 | 726,375 | 731,151 | -4,776 |

|

|

SFRM7 | 666,734 | 668,925 | -2,191 |

|

|

SFRU7 | 475,402 | 478,554 | -3,152 |

|

|

SFRZ7 | 419,083 | 430,517 | -11,434 |

|

|

SFRH8 | 312,066 | 318,394 | -6,328 |

|

|

SFRM8 | 240,025 | 239,732 | +293 |

|

|

SFRU8 | 202,906 | 203,165 | -259 |

|

|

SFRZ8 | 206,629 | 209,350 | -2,721 |

|

|

SFRH9 | 140,493 | 139,432 | +1,061 |

|

|

US TSY FUTURES: Cover Dominated During Monday's Twist Steepening

OI data points to a mix of net short cover (TU, FV & TY), short setting (UXY & WN) & long cover (US) as the curve twist steepened on Monday.

- The instances of net cover comfortably outweighed any modest net short setting further out the curve when it came to the curve-wide positioning bias.

| 14-Jul-25 | 11-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,353,799 | 4,360,666 | -6,867 | -259,171 |

FV | 7,038,158 | 7,071,246 | -33,088 | -1,420,452 |

TY | 4,844,630 | 4,881,139 | -36,509 | -2,398,950 |

UXY | 2,436,011 | 2,434,574 | +1,437 | +124,591 |

US | 1,799,982 | 1,816,618 | -16,636 | -2,276,690 |

WN | 1,966,111 | 1,964,261 | +1,850 | +328,272 |

|

| Total | -89,813 | -5,902,400 |

EQUITIES: Wells Fargo Soft on NII, IB Fees, But Beats on Overall Revenues

Wells Fargo earnings:

• 2Q EPS $1.60

• 2Q NET INTEREST INCOME $11.71B, EST. $11.83B

• 2Q INVESTMENT BANKING FEES $696M, EST. $703.1M

• 2Q REV. $20.82B, EST. $20.75B

Presentation highlights:

- Average loans down $258mln Y/Y as declines in commercial real estate and residential mortgage loans were largely offset by higher commercial and industrial loans. Home lending down 5% from Q1 largely due to lower mortgage servicing income from portfolio run-off and sales

- Total average loan yield down 45bps to 5.95% as a result of lower interest rates

- Net gains from trading activities down 12%, driven by lower revenue in equities, partially offset by higher revenue in FX and rates products

- Credit card segment higher by 9% Y/Y on higher loan balances

- Sees 2025 NII "roughly" inline with 2024 at $47.7bln, but the absolute level of rates and the shape of the curve will be among determining factors

EQUITIES: JPM Earnings Mixed, Volatility in Share Price Pre-Market

- 2Q EPS $5.24

- 2Q ADJ. REV. $45.68B, EST. $44.05B

- 2Q FICC SALES & TRADING REV $5.69B, EST. $5.22B

- 2Q INVESTMENT BANKING REV. $2.68B, EST. $2.16B" - bbg

Highlights from the JPM results, which have seen the stock swing between gains and losses pre-market:

- Markets: "IB activity started slow but gained momentum as market sentiment improved, and IB fees were up 7% for the quarter.", "Markets revenue up 15%, with fixed income up 14%, equities up 15%."

- The economy: "US economy remained resilient. Finalization of tax reform and potential deregulation are positive for the economic outlook."

- On Tariffs: "Significant risks persist – including from tariffs and trade uncertainty"

- Home lending: "Home Lending net revenue was $1.3 billion, down 5%, predominantly driven by lower net interest income."

RUSSIA: Kremlin Assesses Trump's Announcement, Dismisses FT Report As "Fake"

State-run TASS reports comments from Russian Deputy Foreign Minister Sergei Ryabkov regarding US President Donald Trump's announcement that he will (indirectly) send 'top of the line' weaponry to Ukraine and his threat of '100%' and secondary tariffs on Russia if Moscow does not return to the negotiating table within 50 days. Ryabkov: "Russia is ready to negotiate, [the] diplomatic way is preferable." Says that "Russia does not accept any attempt to make demands, much less ultimatums." Ryabkov: "NATO countries are not interested in peace in Ukraine...Russia has a negative attitude towards NATO's coordinating role in arms deliveries to Ukraine."

- Separately, Kremlinx spox Dmitry Peskov says that Trump's statement is "serious, we need time to analyse it". Says that "If President Vladimir Putin deems it is necessary, he will surely make comments on this [Trump's statement]." Peskov: "Decisions taken in Washington and Brussels are seen by Ukraine as a signal to continue the war."

- Peskov dismisses the FT report claiming that Trump advocated for Ukrainian strikes on Russian cities as "fake" (see 'US-RUSSIA: FT-Trump Indicates Support For Ukrainian Strikes On Moscow', 10:21BST)

- Says that "Russia is ready for the next round of talks with Ukraine, [but] there were no proposals from the Ukrainian side so far." Regarding Ukrainian and NATO criticism that Russia has not sent senior delegations to past talks in Istanbul, Peksov says Vladimir Medinsky "is the president's aide, it's a higher rank than a federal minister."

US-EU: EU Spox-Not Moving Forward w/Trade Countermeasures Pre-Aug 1

Reuters reports comments from German Chancellor Friedrich Merz regarding the state of trade relations between the EU and US. Says that the "goal is a quick solution", and says he is in close contact with US President Donald Trump and Commission President Ursula von der Leyen. Says that the EU is refraining from countermeasures "for now", but that "the US should not underestimate [the EU's] willingness to respond." MNI's Policy team reported on 14 July that EU officials are targeting a series of mini trade deals for key industries, even if Trump's 30% tariffs are imposed from 1 Aug (see 'MNI: EU Hopes For Mini-Deals With US Despite Tariff Threat')

- Separately, a Commission spox says that Trade Commissioner Maros Sefcovic will hold a call with USTR Jamieson Greer this evening after talking with Commerce Secretary Howard Lutnick on 14 July. In line with Merz's comments, the spox that the EU "has no intention to move forward with any trade countermeasures before 1 Aug", and that a Commission team is en route to Washington, D.C., to continue working-level talks.

US-RUSSIA: FT-Trump Indicates Support For Ukrainian Strikes On Moscow

The FT reports that US President Donald Trump privately encouraged Ukrainian President Volodymyr Zelenskyy to strike Moscow if possible in a phone call on 4 July, according to people briefed on discussions. FT reports that in the call, Trump asked, “Volodymyr, can you hit Moscow? . . . Can you hit St Petersburg too?” Trump asked on the call, according to the people. They said Zelenskyy replied: “Absolutely. We can if you give us the weapons.” Trump signalled his backing for the idea, describing the strategy as intended to “make them [Russians] feel the pain” and force the Kremlin to the negotiating table, according to the two people briefed on the call."

- In recent weeks, despite Trump's increasingly aggressive rhetoric towards Russia, the Russian gov't has not criticised the US president, often talking up peace talks and Trump's deal-making capacities. Open US support for strikes on Russia's major cities could change this stance significantly.

- The story comes hours after Trump announced the provision of "top of the line" weapons that will be sold to NATO partners and, in turn, sent on to Ukraine. The US President also threatened major sanctions on Russia if they do not return to the negotiating table within 50 days.

- CNN: “A White House official clarified to CNN that when the president referred to “secondary tariffs,” he meant 100% tariffs on Russia and secondary sanctions on other countries that buy Russian oil. The US conducts very little trade with Russia, making the secondary sanctions the piece with potentially the most bite."

FOREX: Greenback Reversing Monday Gains Ahead of US CPI

- The USD index sits in moderate negative territory on Tuesday, taking the DXY back to unchanged levels on the week. Cautious sentiment precedes the June inflation report from the US, which will be the final input for the Fed and no doubt prompt some further commentary from President Trump.

- This dynamic has allowed AUD and NZD to outperform on the session, eroding the majority of the prior day’s declines. Bolstered sentiment in the equity tech space has been supportive, buoyed by early headlines that chip/AI bellwether Nvidia would resume sale of its H20 chip to China (with US government approval). Additionally, China’s Q2 GDP print was slightly better than forecast (y/y growth holding above 5%).

- The impressive USDJPY rally stalled overnight at 147.89, just 14 pips shy of the June highs of 148.03. The pair has since slipped back to unchanged on the day around 147.65. The key technical point for the pair remains at 148.65 as we approach the significant US data, the May 12 high and a reversal trigger.

- Markets remain cautious surrounding the upcoming upper house election on Sunday in Japan, with latest polls underlining the prospect that the governing bloc may struggle this weekend, with the focus remaining on the relentless rise in longer-dated JGB yields.

- GBP has been consolidating its relatively weak position this week, just below 1.3450. A UK jobs report from KPMG REC showed a particularly pessimistic/stagflationary set of figures on Monday, keeping markets on a pessimistic footing ahead of UK inflation and labour market data later this week. EURGBP reached a recovery high this morning at 0.8697, further narrowing the gap with the key bull trigger at 0.8738, the 2025 high and near-term upside target.

- Swiss Franc strength continues to be notable as CHFJPY rose to a fresh record high of 185.73 overnight. It is also worth highlighting that EURCHF dipped to a near 3-month low on Monday, slipping back below the 0.9300 mark.

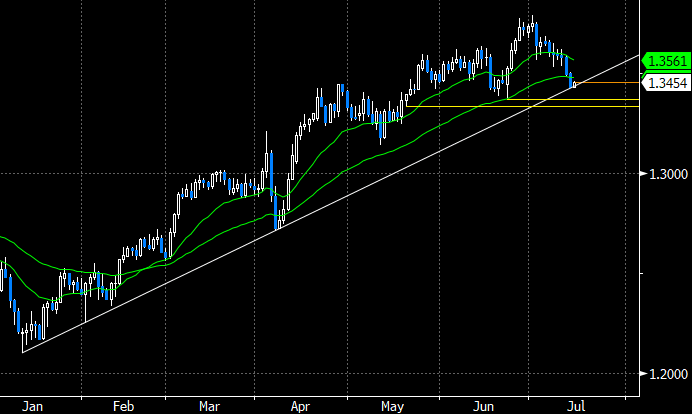

FOREX: GBPUSD at Significant Technical Juncture as US Data Awaited

- GBP has been consolidating its relatively weak recent position, hovering around 1.3450. A UK jobs report from KPMG REC showed a particularly pessimistic/stagflationary set of figures on Monday, keeping sterling on the back foot ahead of US data today and UK inflation & labour market data later this week.

- It is worth highlighting that GBPUSD (shown below) has exposed key trendline support at 1.3430, drawn from the Jan 13 low. The close proximity to this level promotes GBP as a noteworthy candidate to particularly suffer from firmer-than-expected inflation figures in the US. A clear break of the trendline would strengthen a bearish threat and expose 1.3371 initially, the Jun 23 low. Below here, the next target would be 1.3335, the May 20 low.

- Conversely, the Australian dollar may be in a heightened position to benefit from soft US data, as the backdrop of a hawkish RBA surprise and the ongoing resilience for major equity benchmarks fosters a supportive tone. Technical indicators also remain bullish for AUDUSD, and a break of the 0.66 handle would confirm a resumption of the ongoing uptrend. The US election related highs are located at 0.6688.

- Highlighting the above themes, GBPAUD has extended its recent weakness following a breach of trendline support to reach an important technical pivot just below 2.05. The next downside target comes in at 2.03, the Dec 19 high.

Source: Bloomberg Finance L.P. / MNI

EQUITIES: Stocks Boosted by NVIDIA Resuming H20 Chips Shipments

The trend condition in S&P E-Minis remains bullish and the contract is trading at its recent highs. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. A bull cycle in Eurostoxx 50 futures remains in play and the latest pullback appears corrective. Recent gains have exposed key resistance and the bull trigger at 5486.00, the May 20 high.

- Japan's NIKKEI closed higher by 218.4 pts or +0.55% at 39678.02 and the TOPIX ended 2.5 pts higher or +0.09% at 2825.31.

Elsewhere, in China the SHANGHAI closed lower by 14.651 pts or -0.42% at 3504.999 and the HANG SENG ended 386.8 pts higher or +1.6% at 24590.12. - Across Europe, Germany's DAX trades higher by 56.13 pts or +0.23% at 24215.81, FTSE 100 lower by 2.49 pts or -0.03% at 8995.35, CAC 40 up 6.7 pts or +0.09% at 7816.23 and Euro Stoxx 50 up 15.42 pts or +0.29% at 5387.93.

- Dow Jones mini down 56 pts or -0.13% at 44636, S&P 500 mini up 19.75 pts or +0.31% at 6331, NASDAQ mini up 128.75 pts or +0.56% at 23164.75.

COMMODITIES: Gold Holds Well Above 50-dma

A bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to its recent gains. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains still appear corrective. Support to watch is the 50-day EMA, at $65.46. The average has been pierced, a clear break of it would signal scope for a deeper retracement.

- WTI Crude down $0.21 or -0.31% at $66.73

- Natural Gas down $0.04 or -1.04% at $3.431

- Gold spot up $17.43 or +0.52% at $3361.14

- Copper up $0.05 or +0.01% at $555.2

- Silver up $0.12 or +0.32% at $38.2789

- Platinum up $7.89 or +0.58% at $1378.02