MNI US MARKETS ANALYSIS - Tsys Chip Away at Friday Losses

Highlights:

- Treasuries work at erasing Friday losses, pressing 10y yield back below 4.12%

- Data schedule creeping back online, September payrolls due Thursday

- Scope for EURCHF bounce on bullish candle pattern

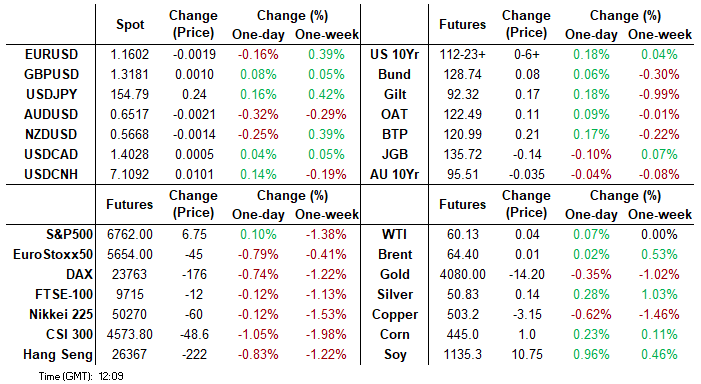

- Treasury futures extended the top end of the overnight range in the last 5 minutes, Dec'25 10Y tapped 112-24 before trading back to 112-23 (+6), 10y yield slips to 4.1173% low (-.0310). Treasuries last week challenged resistance at the 113-02 level, an area of congestion since Nov 5. This hurdle remains intact, however, a clear move above it would be a bullish signal and shift focus on resistance at 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme.

- The German 10Y Bund gained as well - but remains off overnight highs, Bbg US$ index firmer at 1217.70 (+1.42), stocks mildly higher (SPX eminis +19.75 at 6,775.00).

- Today’s schedule focus is likely on Fedspeak plus Trump headlines, with a quieter day for data before it builds into the week.

- Data: Empire Mfg Nov (0830ET), Construction spending Aug (1000ET), Federal budget data for Oct could be released between Nov 17-20 per Bloomberg scheduling

- Fedspeak: Williams (0900ET), Jefferson (0930ET), Kashkari (1300ET and Waller (1535ET) – see Fed bullet.

- Bill issuance: U.S. To Sell $86B 13-Wk and $77B 26-Wk bills (1130ET)

- Politics: Trump meets with WH task force on FIFA World Cup (1400ET), Trump delivers remarks at McDonald’s Impact Summit (1800ET)

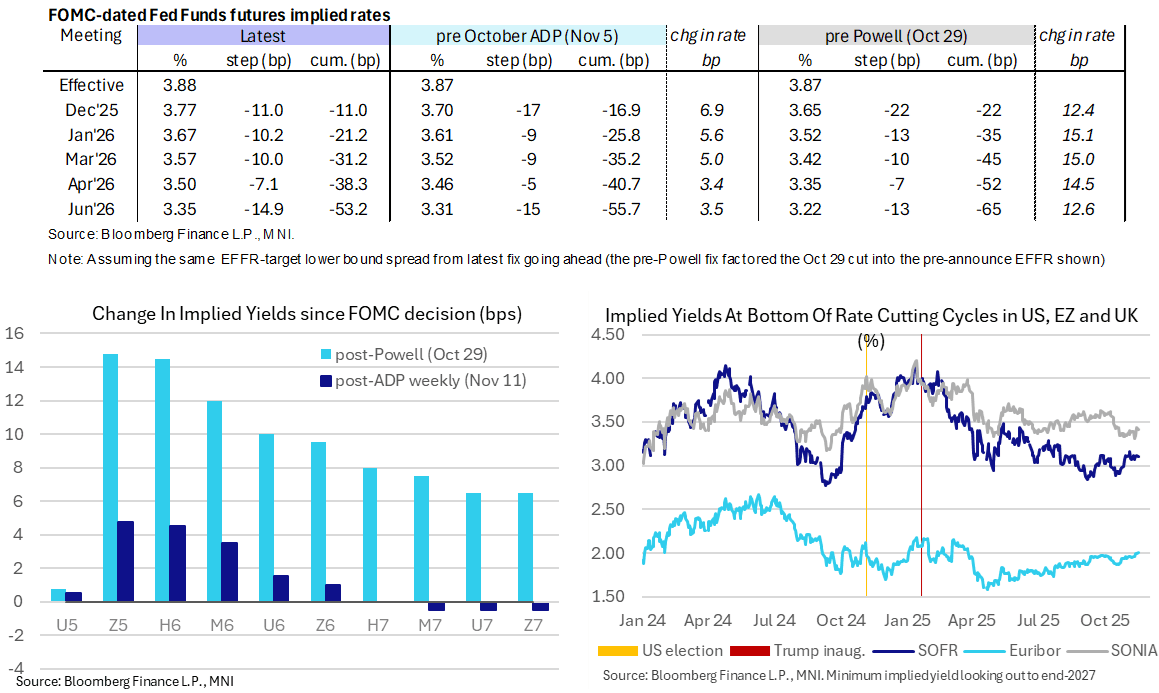

STIR: Fed December Pause Seen As ~50/50 Call As Official Data Resumes

- Fed Funds implied rates are unchanged from Friday’s close, holding last week’s push to a close call for December’s FOMC meeting between another 25bp cut or pausing.

- A pause is now seen as slightly more likely, supported by multiple Fed speakers with patient rhetoric.

- Cumulative cuts from an assumed 3.88% effective: 11bp Dec, 21bp Jan, 31bp Mar, 38.5bp Apr and 53bp Jun.

- SOFR futures are +0.005-0.025, with increases led by 2027 contracts.

- It sees the terminal implied yield remain within recent ranges, at 3.10% (SFRH7) between 3.06-3.16% that has been defined primarily by labor data and a strong ISM services report.

- Today’s data is light – Empire manufacturing for Nov and a delayed construction spending report for Aug – with some Fedspeak updates possibly more important (noted a little earlier). Nonfarm payrolls for September looms large on Thursday even if it is now two months old.

Fedspeak Highlighted By Updates From Jefferson And Waller

All of today’s Fedspeakers have spoken since the Oct 29 FOMC decision but we don’t rule out potential for reaction to comments from senior members Jefferson and Waller if there any tweaks in view. Waller in particular has driven by some gyrations in rates over the past six weeks, sounding a little more patient ahead of the October meeting before confirming a more dovish stance since then. However, surprises might be limited coming ahead of a official data releases resuming including Thursday’s nonfarm payrolls release for September.

- 0900ET - NY Fed’s Williams (voter) welcome remarks (no text or Q&A)

- 0930ET - VC Jefferson (voter) on economic outlook & mon pol (text + Q&A). He gave a speech on Nov 7 in which he described wanting to proceed slowly with policy easing as a result of being closer to a neutral level. He added “With respect to the path of the policy rate going forward, I will continue to determine policy based on the incoming data, the evolving outlook, and the balance of risks. I always take a meeting-by-meeting approach.”

- 1300ET – MN Fed’s Kashkari (’26 voter) moderates conversation (no text). As we noted in Friday’s MNI US Macro Weekly (link), Kashkari has tilted more hawkish recently, revealing he would have preferred to have held rates steady in October and is waiting and seeing for the December meeting.

- 1535ET – Gov. Waller (voter, dove) on economic outlook (text + Q&A). He made clear on Oct 31 that he still supports a rate cut in December. "The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and … the right thing to do with policy is to continue cutting."

SOFR: Mix Of Short Setting & Long Cover Seen In Futures On Friday

OI data points to net short setting dominating through the reds as most SOFR futures settled lower on Friday, with net long cover then coming to the fore in the greens and the blues.

| 14-Nov-25 | 13-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,367,543 | 1,356,564 | +10,979 | Whites | +73,025 |

SFRZ5 | 1,456,058 | 1,432,618 | +23,440 | Reds | +26,523 |

SFRH6 | 1,284,503 | 1,247,281 | +37,222 | Greens | -20,457 |

SFRM6 | 1,097,413 | 1,096,029 | +1,384 | Blues | -8,314 |

SFRU6 | 1,137,003 | 1,125,862 | +11,141 |

|

|

SFRZ6 | 1,208,633 | 1,190,808 | +17,825 |

|

|

SFRH7 | 849,528 | 853,156 | -3,628 |

|

|

SFRM7 | 817,182 | 815,997 | +1,185 |

|

|

SFRU7 | 768,228 | 775,279 | -7,051 |

|

|

SFRZ7 | 806,679 | 815,225 | -8,546 |

|

|

SFRH8 | 436,196 | 435,221 | +975 |

|

|

SFRM8 | 418,302 | 424,137 | -5,835 |

|

|

SFRU8 | 351,155 | 352,177 | -1,022 |

|

|

SFRZ8 | 318,633 | 326,743 | -8,110 |

|

|

SFRH9 | 201,660 | 201,225 | +435 |

|

|

SFRM9 | 188,233 | 187,850 | +383 |

|

|

EUROPE ISSUANCE UPDATE

EU-BOND SYNDICATION: 2.50% Oct-30 tap mandate

- The EU has mandated Goldman Sachs Bank Europe SE, HSBC, J.P. Morgan, Natixis and UBS as Joint Lead Managers for its upcoming Fixed Rate RegS Bearer increase of the EU 2.500% benchmark due 14 October 2030 (EU000A4EG021). No further group. The transaction will be launched tomorrow, subject to market conditions."

- Probably a smaller syndication than some had expected. Just a single line and only 5-year maturity (but we are coming to the end of the year).

FOREX: USDJPY Price Action Points Towards Renewed Test of 155.00

- The first session of the week provides some consolidation following Friday's volatility. The US dollar advanced against most others in G10 and SEK outperforms again, while the Euro and the likes of NZD and AUD weaken amid headline drivers remaining light.

- Amid reports on a fiscal easing package, price action in USDJPY points towards a renewed challenge to the 155.00 handle. The pair saw three highs around there recently ahead of Friday's temporary dip. Renewed upside would put sights on 155.53, a Fibonacci projection. Initial support to watch is 153.30, the 20-day EMA. Remember that Japanese authorities have recently stepped up their rhetoric on JPY valuations but stopped short of phrases historically associated with intervention for now.

- The extension of downward momentum in EURSEK is helping narrow the gap to an important support zone around 10.9000. A clear break of this level would expose 10.8000, which aligns closely with the April 4 low (10.7941). The case for continued SEK outperformance is largely tied to the growth differential channel. Recent domestic data have supported these arguments, with Swedish activity being supported by stimulative monetary policy, incoming fiscal stimulus and lower trade policy uncertainty.

- EURCHF closed last week at 0.9227, above a mid-term resistance zone after piercing 0.9200 for the first time since the withdrawal of the 1.20 floor in 2015. With today's price action lacking impetus following the weaker-than-expected Q3 Swiss flash GDP print, a few short-term signals suggest there may be scope for a bounce near-term for the cross.

- The trend is in oversold territory, and Friday's price pattern is a hammer candle - a potential short-term reversal signal. If the cross does recover, scope would be for a climb towards 0.9275, the 20-day EMA and 0.9298, the 50-day EMA. Key support lies at 0.9180, Friday's low and the bear trigger.

- Canada CPI, US empire manufacturing and construction spending highlight the data calendar for today alongside a set of Fed, ECB and BoE speakers.

CHF: Set Of Short-Term Signals May Suggest Scope For EURCHF Upside

EURCHF closed last week at 0.9227, above a mid-term resistance zone after piercing 0.9200 for the first time since the withdrawal of the 1.20 floor in 2015. With today's price action lacking impetus following the weaker-than-expected Q3 Swiss flash GDP print, a few short-term signals suggest there may be scope for a bounce near-term for the cross.

- The trend is in oversold territory, and Friday's price pattern is a hammer candle - a potential short-term reversal signal. If the cross does recover, scope would be for a climb towards 0.9275, the 20-day EMA and 0.9298, the 50-day EMA. Key support lies at 0.9180, Friday's low and the bear trigger.

- HSBC think the USD200bn Swiss investment announcement to the US "takes some shine off the reduction in the tariff rate" but "with a 15% rate, the hurdle for the CHF remains but has become lower to jump over". They continue to see the currency performing "resolutely" with risks over a deteriorating Swiss current account balance now reduced.

HUNGARY: MNI NBH Preview – November 2025

- The National Bank of Hungary is expected to keep the base rate on hold at 6.50% for the 14th consecutive month, sticking to its ‘cautious and patient’ approach to monetary policy as headline inflation continues to run above target.

- Additionally, pro-inflationary government measures and the possibility of sovereign ratings downgrades pose hawkish risks.

- All 20 analysts surveyed by Bloomberg expect the base rate to be left unchanged.

See our full preview, with a summary of sell-side analyst views, here.

EQUITIES: Eurostoxx Futures Trend Bullish Despite Latest Pullback

- A medium-term bull trend in Eurostoxx 50 futures remains intact and last week’s gains reinforce bullish conditions. However, the latest pullback suggests the start of a corrective phase. Price has traded through the 20-day EMA. Attention is on support at the 50-day EMA, at 5604.85, and 5599.00, the base of a bull channel drawn from the Aug 1 low. These two price points represent key support. A break would highlight a stronger reversal.

- The trend condition in S&P E-Minis remains bullish and the latest selloff appears corrective - for now. Support at the 50-day EMA, at 6730.32, has been pierced, however, price is once again trading above the average. The next key support to watch is 6655.50, the Nov 7 low. Friday’s price pattern is a doji candle - a reversal signal. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this level would be bullish.

COMMODITIES: Sell-Off in WTI on Nov 12 Strengthened a Bearish Theme

- A sell-off in WTI futures on Nov 12 strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- Gold is trading below last week’s high. The downleg between Oct 20 and 28, appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. Key support lies at the 50-day EMA, at $3927.5. Clearance of this EMA would signal scope for a deeper retracement. For bulls, a resumption of gains would pave the way for a test of $4381.5, the Oct 20 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 17/11/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 17/11/2025 | 1320/1320 | BOE Mann on DMP and MonPol | ||

| 17/11/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/11/2025 | 1330/0830 | *** | CPI | |

| 17/11/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/11/2025 | 1400/0900 | New York Fed's John Williams | ||

| 17/11/2025 | 1430/0930 | Fed Vice Chair Philip Jefferson | ||

| 17/11/2025 | 1445/1545 | ECB Lane Lecture on ECB MonPol | ||

| 17/11/2025 | 1500/1000 | * | Construction Spending | |

| 17/11/2025 | 1500/1000 | * | Construction Spending | |

| 17/11/2025 | 1600/1700 | ECB Cipollone at ECON Digital Euro Hearing | ||

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/11/2025 | 1800/1300 | Minneapolis Fed's Neel Kashkari | ||

| 17/11/2025 | 2035/1535 | Fed Governor Christopher Waller | ||

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1500 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders |