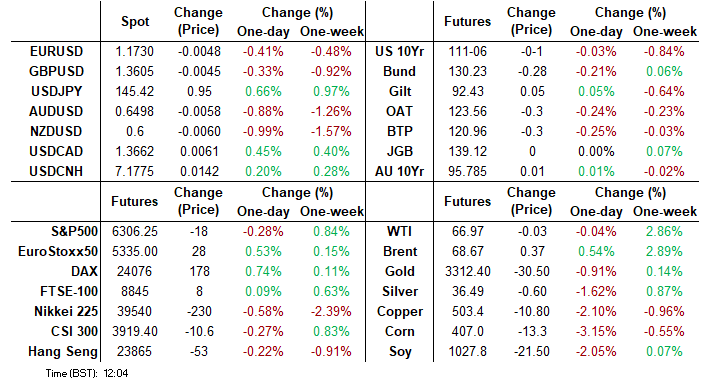

MNI US MARKETS ANALYSIS - Trump Waves BRICS Tariffs Threat

Highlights:

- Trump waves tariff threat against the "Anti-American" activities of BRICS

- USD firmer, pressing major pairs to post-NFP lows

- Treasuries return from long weekend under pressure

US TSYS: Back From Holiday, Bonds Under Pressure, Midweek FOMC Minutes

- Treasuries looking mixed as US markets resume after extended 4th of July holiday, curves steeper with 10s to Bonds weaker vs mildly higher 2s-5s at the moment (2s10s curve +2.023 at 47.984, 5s30s +2.475 at 94.849), Tsy 10Y yield +.0079 at 4.3537% (4.3201 Low / 4.3556 High).

- At the moment, Sep'25 10Y contract trades -2 at 111-05 - recent overnight low, above key technical support at 110-31, the 50-day EMA, and the Jul 3 low. A clear break of this average would signal scope for a deeper correction and highlight a possible reversal.

- For bulls, a resumption of gains would open 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off. Initial resistance is at 111-28, the Jul 3 high.

- No economic data or Fed speakers scheduled today, US Treasury will be auctioning $82B 13W & $73B 26W bills at 1130ET.

- Relatively light data calendar compared to last week, focus is on the release of FOMC minutes for the June 18 meeting this Wednesday at 1400ET.

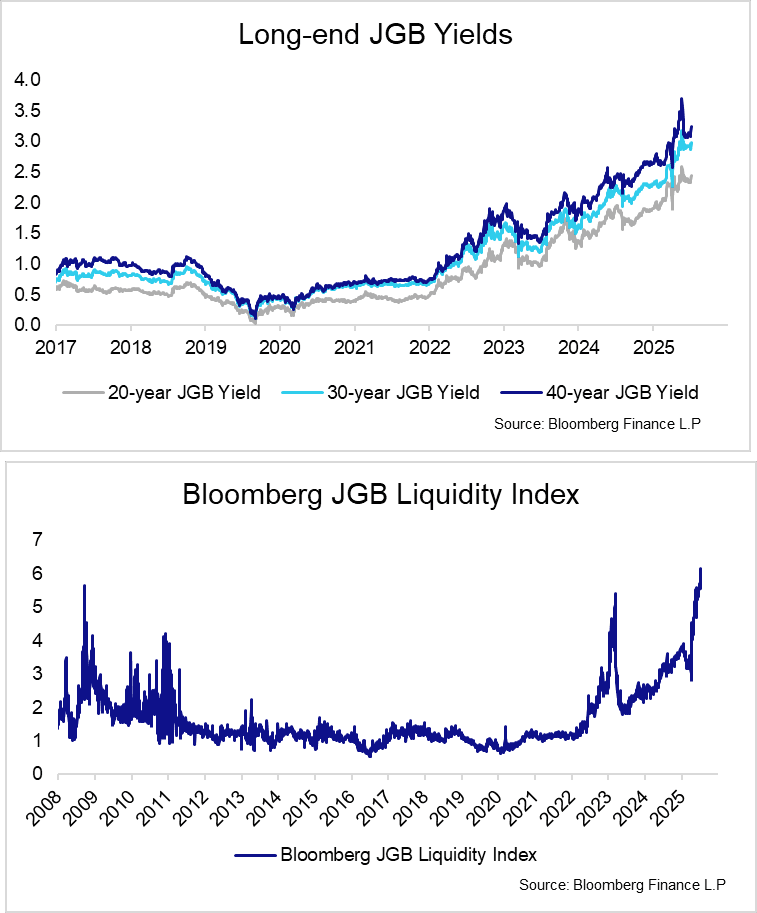

JGBS: Long-end Pressures Resumes Overnight As Election Comes Into View

Long-end JGB yields saw notable upward pressure overnight, with 20-year yields up 6.5bps and 30/40-year yields up 10bps. Yields remain comfortably below the late-May highs, but fiscal risks/concerns appear to be back in focus with the July 20 Upper House election coming into view. After falling by 7bps on Friday amid renewed tariff concerns, 30-year yields are back above last Thursday’s 2.970% high (which came following a mixed 30-year auction).

- May wage data overnight was much weaker-than-expected, with nominal earnings rising 1.0% Y/Y (vs 2.4% cons, 3.0% prior) and real earnings falling 2.9% Y/Y (vs -1.7% cons, -2.0% prior).

- With PM Ishiba’s LDP party already pledging cash handouts of JPY20k as part of its election campaign, the weak wage data may be increasing concerns of more fiscal loosening/household support pledges ahead of the July 20 vote. A reminder that Fitch noted earlier today that while Japanese fiscal risks are contained in the near-term, long-term risks are more significant given ageing-related costs.

- The latest seat projection opinion polling ahead election for the House of Councillors shows PM Shigeru Ishiba's conservative Liberal Democratic Party (LDP) on course to lose a significant number of seats, and potentially for the governing coalition (alongside the Komeito party) to lose its overall majority in the upper chamber of the Japanese National Diet.

- Despite yields remaining shy of year-to-date highs, liquidity at the long-end of the JGB market remains a concern. Bloomberg’s JGB liquidity index is currently at its highest since the series began in 2008 (indicating worse liquidity).

- See our earlier Political Risk post for more colour on current election polling figures.

EUROPE ISSUANCE UPDATE:

EU syndication: Mandate

- Dual-tranche Mandate: New 7-year Dec-32, tap 3.75% Oct-45 (ISIN: EU000A4EA8Y7)

- "The transaction will be launched tomorrow, subject to market conditions."

- We had thought there would be a good chance that the transaction was skewed to the shorter-end (although had thought a 5-year more likely than a 7-year here).

- We had also thought that a dual-tranche was likely to kick off H2 issuance for the EU.

- We pencil in E5-7bln for the new 7-year and E3-5bln for the 20-year tap.

Germany coupon size announcement

- DFA has announced its coupon for the new Oct-30 Bobl at 2.20%. E5bln of the line will be on offer tomorrow, July 8.

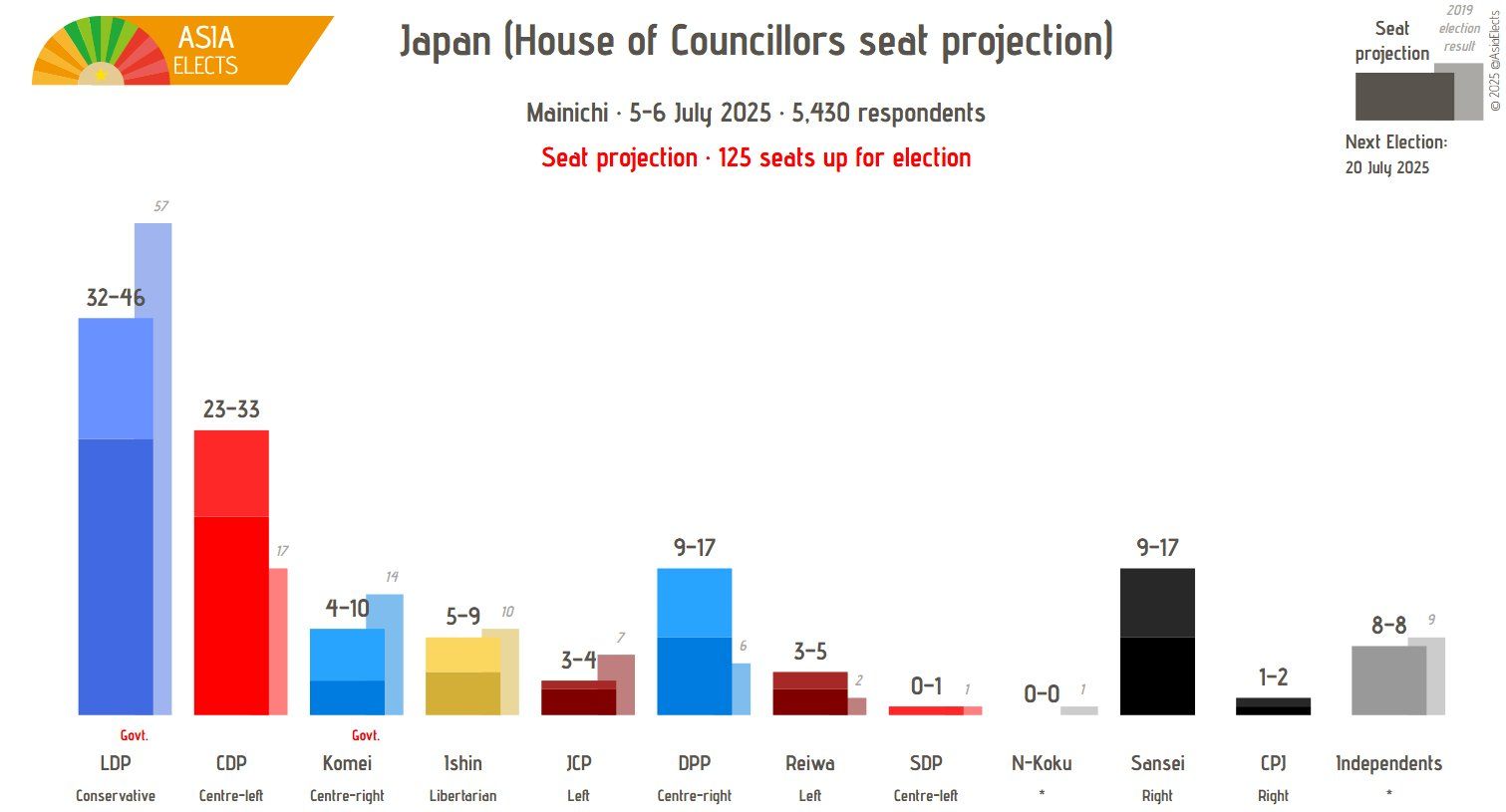

JAPAN: LDP-Komeito May Struggle To Hold Onto Upper House Majority-Poll

The latest seat projection opinion polling ahead of the 20 July election for the House of Councillors shows PM Shigeru Ishiba's conservative Liberal Democratic Party (LDP) on course to lose a significant number of seats, and potentially for the governing coalition (alongside the Komeito party) to lose its overall majority in the upper chamber of the Japanese National Diet.

- The poll for Mainichi Shimbun, carried out 5-6 July, projects the LDP to win between 34 and 46 of the 124 seats up for election. The House of Councillors has 248 seats in total, with half of the seats up for grabs every three years. In the previous election in which these seats were up, the LDP won 57 seats, meaning even at the higher end of the projection range, the party is on course to lose ground.

- Among the seats not up for election this round, the LDP and Komeito hold a combined 77 seats. As such, if the parties perform at the lower end of the projection range, they would come away with as few as 113 seats, short of the 125 needed for a majority. This would leave the gov't in the minority in both chambers of the Diet and could pose a threat to PM Shigeru Ishiba's position at the head of the LDP.

- The poll shows the right-wing populist Sanseito on course for significant gains, winning a projected 9-17 seats, up from one presently. After a strong performance in the Tokyo metropolitan assembly elections in June, an increased seat total in the upper chamber would cement the party's status as an opposition force rather than an upstart challenger.

Chart 1. House of Councillors Opinion Poll, Seat Projection

Source: @asiaelects, Mainichi

US-EU: German Gov't Spox: Merz Coordinating w/VdL, Meloni & Macron On Tariffs

Reuters reports comments from a German gov't spox stating that Chancellor Friedrich Merz is coordinating with European Commission President Ursula von der Leyen, Italian PM Giorgia Meloni, and French President Emmanuel Macron with regard to the situation vis-a-vis US tariffs. Adds that "time is money when it comes to tariff negotiations." Germany and France remain on different tracks in terms of response to US tariffs, with Berlin seeking a swift deal even if it is not perfect, while France has sought to avoid perceptions of EU 'weakness' at the risk of no agreement being reached.

- There has been significant uncertainty over the weekend as to the date of when 'reciprocal' tariff rates might kick back in. The initial date of 9 July supposedly remains, but both President Trump and Secretary of the Treasury Scott Bessent have said that 1 August will be the point at which the higher rates "boomerang back", (although denying this is a new deadline).

- In any case, there is little-to-no expectation of a deep trade deal being announced between the two sides, with a thin skeleton deal that includes the 10% baseline US tariff, seen as the best outcome in terms of avoiding friction in the short term.

- Bloomberg report comments from Portuguese Finance Minister Joaquim Miranda Sarmento, who said ahead of the EU economic affairs minsiters' meeting on 8 July, that “It’s possible to have an agreement with very low tariffs,” but added “If the terms of the deal are not favorable for the EU then there is no agreement,”

CHINA: PBoC Conducted Survey on USD Weakness, According to Sources

"EXCLUSIVE - CHINA'S CENTRAL BANK SURVEYED SOME FINANCIAL INSTITUTIONS ABOUT THEIR VIEWS ON RECENT U.S. DOLLAR WEAKNESS, SOURCES SAY" - Reuters

Piece writes that a survey was conducted last week, in which the PBOC asked questions related to the U.S. dollar's movements and the causes of its recent weakness and outlook for the Chinese yuan exchange rate, the sources said.

- One of the sources said he interpreted it as a sign authorities are concerned about a sharp appreciation of the yuan against the weakening dollar.

- Another source directly involved in the survey said it seemed to be an assessment of the dollar's outlook as trade negotiations with the U.S. progress.

GBP: USD Bounce Has Major Pairs Testing Key Levels

- The USD's bounce Monday is providing some relief for the USD Index, which now sits 1% above last week's cycle lows to put the currency on a surer footing. As a result, the major pairs are seeing pressure toward the the post-NFP lows - with EUR/USD and GBP/USD challenging 1.1718 and 1.3586 respectively.

- Rates markets are endorsing USD gains here: the US curve is steeper as the global long-end continues to underperform. This backdrop, allied with any deterioration in trade relations between the US and the RoW remains a key market focus, particularly with the fluidity around Trump's approach to tariffs and the suite of reciprocal trade tariff deadlines looming over markets this summer.

- A correction lower through 1.3563 would be consequential for GBP/USD, and raise the likelihood of a test on the 50-dma support in the near-term. This level has held well and helped define the rally over the course of 2025 - crossing at 1.3477 today. In trend terms, we note that the 50-dma now trades with the largest % premium over the 200-dma since the bounce off lows in 2009. The premium currently sits at ~4.2% vs. the 2009 peak of ~8.2%, mid-Global Financial Crisis.

AUD: Notable Weakness Ahead of RBA, EURAUD Extends Above 1.8000

- While the dollar is not exactly surging Monday, trepidation surrounding renewed tariff concerns have weighed significantly on the likes of AUD and NZD, comfortably the weakest currencies in G10. AUDUSD has seen a swift adjustment back below the 0.6500 handle, fading back into familiar territory for the pair across much of May and June.

- Price action is bolstered by the USD index continuing to respect its test of long-term trendline support and the subsequent grind to fresh recovery highs. The greenback stabilisation is underpinned by US nonfarm payrolls growth beating expectations in June and the impressive pullback in the unemployment rate, which at 4.117% unrounded was the lowest since January.

- AUD will remain in focus ahead of Tuesday’s RBA meeting (our preview here: https://mni.marketnews.com/4ldBNDE ), where most analysts expect a 25bp cut. With a minority calling for a hold, the confirmation of further easing could place pressure on the 50-day EMA for AUDUSD. The average currently intersects at 0.6471, and spot has not had a daily close below since April 10.

- Standing out even more on the chart is EURAUD, which has broken above 1.8000 convincingly this morning. This extends the bounce from the June lows to around 3.5%, signalling scope for further strength towards a cluster of daily highs between 1.8450-1.8550 from April. Initial Fibonacci resistance for the cross comes in at 1.8248.

OPTIONS: Expiries for Jul07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1640-50(E1.5bln), $1.1675(E600mln), $1.1690-00(E1.2bln), $1.1750-70(E4.1bln), $1.1800-10(E1.3bln), $1.1825(E837mln), $1.1850(E1.4bln)

- USD/JPY: Y143.50-60($531mln), Y143.85($550mln), Y144.30-50($876mln), Y144.75-90($725mln)

- GBP/USD: $1.3800(Gbp770mln)

- AUD/USD: $0.6600(A$885mln)

- USD/CNY: Cny7.1500($670mln), Cny7.2300($897mln)

EQUITIES: E-Mini S&P Trend Signal Unchanged and Bullish

- Short-term trend signals in Eurostoxx 50 futures remain bearish, however, the recovery from the Jun 23 low still appears to be a reversal and the contract is holding on to its most recent gains. Price has pierced both the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of 5194.00, the Jun 23 low, reinstates a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA - at 6000.73.

COMMODITIES: Gold Continues to Hover Just Above Support at 50-Day EMA

- WTI futures maintain a softer tone following the reversal from the Jun 23 high. Recent gains appear corrective. Support to watch is the 50-day EMA, at $64.84. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note that the latest recovery highlights a possible false trendline break. A resumption of gains would refocus attention $3451.3, the Jun 16 high. The bear trigger is $3248.7, the Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 07/07/2025 | - | ECB Lagarde and Cipollone In Eurogroup Meeting | ||

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/07/2025 | 2350/0850 | Balance of Payments | ||

| 08/07/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 08/07/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit |