MNI US MARKETS ANALYSIS - Trump Meets With NATO

Highlights:

- UK inflation print raises risk of another rate cut this year

- Trump meets with NATO, comments on delayed Putin summit eyed

- Government still in shutdown, putting 20y reopening in focus

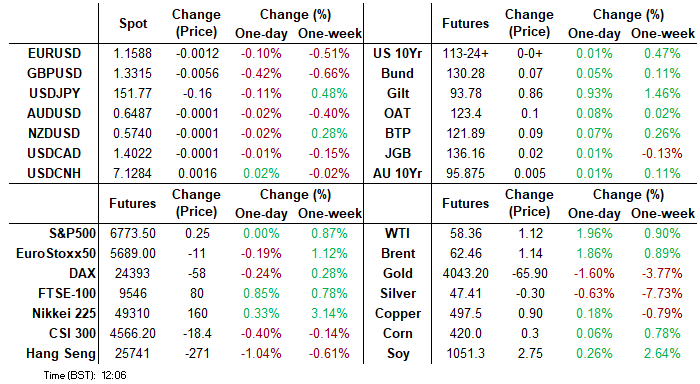

US TSYS: Yesterday’s Rally Consolidated, 20Y Auction Leads Calendar

- Treasuries are marginally firmer overnight, with intraday gains earlier helped by softer than expected UK in what’s otherwise seen little moves of note.

- Today’s 20Y re-open highlights an otherwise thin docket after last month’s solid auction.

- Trump’s NATO meeting will also be watched later on, as will his comments more broadly throughout the day. He yesterday urged Senate Republicans to hold the line on the government shutdown – now the second longest in history – whilst also floating that the meeting with China’s Xi maybe won’t happen albeit having said he expects to make a good deal with Xi just beforehand.

- Cash yields are 0.6-1.0bp lower across the curve.

- TYZ5 trades unchanged at 113-24 in what has been a particularly narrow range of 113-21 to 113-25 under subdued cumulative volumes of 200k.

- The bull cycle remains intact, with resistance seen at 114-02 (Oct 17 high) before 114-10 (Apr 7 high continuation), whilst support is seen at 113-03+ (20-day EMA).

- Data: Weekly MBA mortgage applications (0700ET)

- Coupon issuance: US Tsy $13B 20Y Bond re-open - 91210UN6 (1300ET). Last month’s 20Y auction saw a small 0.2bp trade through along with more encouraging internals, with a bounce in bid-to-cover and indirect take-up along with the lowest dealer take since mid-2024.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump in NATO meeting (1600ET)

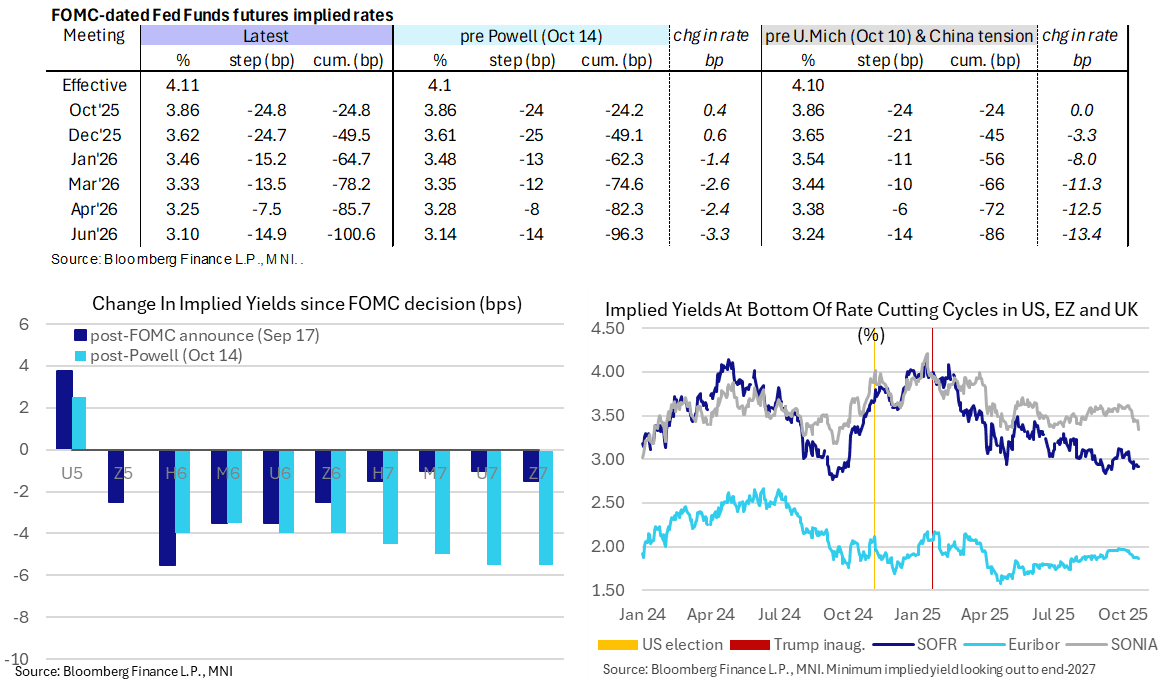

STIR: Back-to-Back Fed 25bp Cuts Still Eyed, Only Mild Impact From Soft UK CPI

- Fed Funds implied rates are little changed overnight, with back-to-back cuts seen for next week and December meetings before a quarterly pace thereafter to mid-2026.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49.5bp Dec, 64.5bp Jan, 78bp Mar, 85.5bp Apr and 100.5bp Jun.

- SOFR futures are little changed on the day, with only small intraday spillover from a sizeable rally in UK rates on softer than expected UK CPI inflation.

- The SOFR implied terminal yield of 2.915% (SFRH7) is unchanged on the day, close to last week’s lowest close of 2.89% in risk-off moves on regional bank fears. For context, cycle lows were 2.77% back in Sep 2024 in anticipation of an aggressive start to the Fed’s easing cycle at the time.

- It’s a particularly thin data docket today, with just MBA mortgage applications. More notable releases for the week are state-level jobless claims to be released from Thursday afternoon and then the highlight being the delayed September CPI report on Friday.

RUSSIA: Kremlin-'Budapest Summit Needs More Prep', Despite Trump Cancellation

State-run Tass reporting comments from Kremlin spox Dmitry Peskov regarding the apparent cancellation of the Budapest summit between President Vladimir Putin and his US counterpart Donald Trump (see 'RUSSIA: Budapest Conference Off, But Background Work Continues', 08:53BST). Peskov claims there is no news yet regarding the summit; "rumours and speculation" about the situation surrounding its preparations are largely inaccurate. Peskov claims that "The dates [for the summit] haven't been set; that's still to come. Thorough preparation is needed before then, and that takes time". Peskov repeats Trump's comments, saying that neither side wants to "waste time".

- Peskov takes the same line on the 'non-paper' supposedly passed to the US regarding Russia's stance on the conflict as Deputy Foreign Minister Sergei Ryabkov. Peskov says, "Russia has repeatedly stated its clearly formulated position on Ukraine."

- The 'non-paper', alleged to have reiterated Russia's maximalist demands for Ukraine to cede the entirety of the Donbas, is seen as one of the major factors behind the US' apparent cancellation of the summit and Trump's dismissal of the potential event as a "wasted meeting".

- Peskov claims that the idea of the Budapest summit came about due to “a mutual desire”. Says "the current pause [in the peace process] requires intervention at the highest level. But this intervention must be well-prepared."

- Separately, Peskov confirms that Putin will not attend the G20 summit in Johannesburg, South Africa, but that Russia will be represented at a 'decent' level.

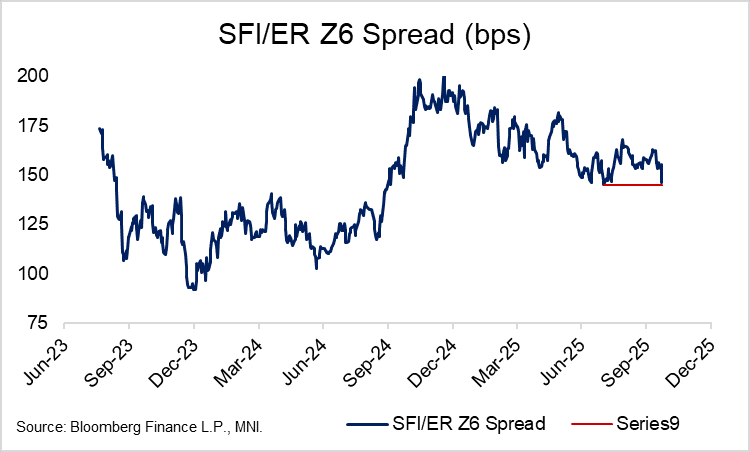

STIR: SONIA / Euribor Z6 Spread Could Narrow Further On Weak UK PMIs

Previously noted downside risks to the SONIA / Euribor Dec '26 spread are being realised this morning, following the soft UK September labour market data. The spread is currently down 9.5 ticks on the session at 146bps, narrowing the gap to the August 1 cycle closing lows of 145bps.

- A weak set of UK October flash PMIs on Friday could promote further narrowing in the spread. With ~60bps of cumulative BOE cuts priced across the next 12 months, there is still scope for additional dovish repricing.

- Meanwhile, a weaker-than-expected round of Eurozone flash PMIs is likely to exert greater influence on the distribution of implied ECB cuts (i.e. pulling cuts forward to December and March), rather than overall terminal rate expectations.

- Narrowing in the Z6 spread has supported a 0.3% bounce in EURGBP FX today. Spot is currently hovering just above 0.8700. The next area of interest on the topside is 0.8725, the October 10 and 17 high.

EUROPE ISSUANCE UPDATE

German auction results

- Weak demand again on that 2.50% Nov-32 Bund auction despite it being the only re-opening of the line in Q4.

- Bid-to-offer at 0.93x, below last month’s 1.13x.

- Lowest accepted price of 101.05 below the 101.062 pre-auction mid.

- The secondary price has fallen ~3 points briefly after the auction results were published.

- Very little spillover to Bund futures however (~5 ticks of downside in the minutes after the results release).

- E3bln (E2.284bln allotted) of the 2.50% Nov-32 Bund. Avg yield 2.33% (bid-to-offer 0.93x; bid-to-cover 1.22x).

UK DATA: Downside surprise to food in particular increases prospect of Q4 cut

- Food and non-alcoholic beverages are the biggest surprise here, down to 4.53%Y/Y and 0.48ppt below the BOE's forecast. That contributed 0.06ppt to the downside surprise to headline CPI. Alcohol and tobacco were also softer than expected. Overall FAT had been expected to contribute a positive 0.03ppt to headline CPI but it contributed negative 0.06ppt. So that accounts for around 0.09ppt of the 0.21ppt downside surprise.

- Cultural services contributed -0.06ppt to headline CPI (and around double that to services CPI). That wasn't expected to be as soft. Banking services also contributed -0.02ppt to headline CPI. They appear the biggest surprises in services.

- Note that air fares were marginally softer than expected at -28.8%M/M - it had been expected in the mid -20s so it's not the biggest driver of the softness here. There was also no upside from education, which came in a little softer than expected rising 7.2%Y/Y (down from 7.5%Y/Y in August).

- Still looking through the details but the food surprise is significant here.

- Some of the services downside might be a little reversed next month (through cultural services) but its hard to make a case for the weakness seen elsewhere.

- GBPUSD has fallen more than 50 points since pre-data levels now and the prospect of Bailey supporting a Q4 cut seems as though it would be higher.

- Recall how focused the MPC is on food inflation driving inflation expectations and leading to inflation persistence. If this is the peak, then those concerns can recede a little and combine with the softer wage data seen last week.

- We would expect to see SONIA rally on the open and probably take GBP FX weakness another leg.

FOREX: GBP Sinks as UK Markets Rush to Price Greater Cut Risk

- GBP is weaker against all others in G10 as markets rush forward BoE easing pricing after UK CPI surprised to the downside, notably on the back of lower food inflation. This means the prospect of Governor Bailey supporting a Q4 cut has risen, which is well reflected by SONIA pricing. Money markets now price 17bps of easing through year-end, up from 10bps yesterday. The MPC are particularly focused on food inflation driving inflation expectations and leading to inflation persistence. As such, if today's data marks the peak for the category, then those concerns can recede a little and combine with the softer wage data seen last week.

- Inflation numbers drove GBPUSD to lose around 70 pips to print 1.3316, strengthening the narrative that the recent recovery in the pair appears corrective. Key support and the bear trigger lies at 1.3249, the Oct 14 low. A break of it would resume the recent bear leg. There are no MPC appearances scheduled ahead of the November MPC meeting (although the blackout period doesn’t start for a while so there is plenty of time for unscheduled media appearances).

- After some potential profit taking in the early morning, EURUSD continues its downward trajectory seen during the last two sessions, narrowing the gap to the 1.1542 bear trigger in the pair. E1.47bln of EURUSD options expire today around the 1.1600 handle, which may act as a magnet for price action for the pair. French politics may move back into focus towards the end of the week, with the National Assembly set to begin debate on the 2026 budget on Friday.

- Ahead of tomorrow's inaugural SNB meeting minutes, EURCHF consolidates yesterday's bounce from key clustered support between 0.9206/21. Tomorrow's minutes will signal how far the SNB was away from cutting into negative territory in September, and we specifically look for any indication of whether Schlegel's decision not to mention of negative side effects of NIRP was a deliberate move, with potential commentary here posing two-way risks for Swiss STIR and subsequently EURCHF.

- More ECB speakers are on the schedule today but they are mostly expected to reiterate the previous "rates are in a good place" rhetoric. The data calendar is light given the continued US government shutdown until Friday's flash PMIs as well as the rescheduled US CPI.

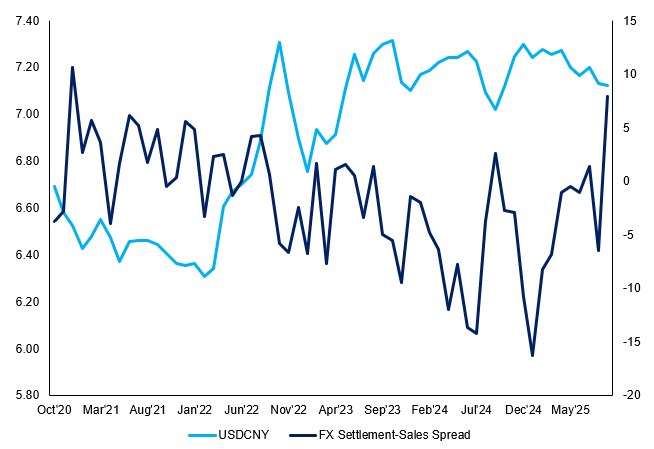

CHINA: SAFE Data Shows FX Settlement-Sales Spread at New High

Data on FX settlements from China's SAFE show the FX settlement ratio (a proxy for client willingness to settle FX) posting a sharp rise in September, to 71.2% from 61.2% in August. This is the highest level since August 2023 and is consistent with a sharp rise in exporters settling FX transactions in the month that covered USDCNY printing a new YTD low (Aug-Sept peak to trough was over 1.5%).

In contrast, the FX sales ratio (a proxy for client willingness to buy FX) was relatively stable at 63.3% (vs. August 67.7%), leading to a wider gap between settlement and sales in September. As a result, the FX settlement-sales spread has risen to a new 2025 high, and would be consistent with the weaker USD helping trigger the fastest pace of corporates closing out of FX positions relative to new FX exposure over the period.

Figure 1: FX Settlement/Sales Spread Highest of the Year

Source: MNI / SAFE / Bloomberg Finance L.P.

In addition, the SAFE data also shows an FX surplus totalling $51.1bln as a result of the rise of total FX purchases (up to $265bln from $212bln) outpacing the rise in FX sales (up to $214bln from $197bln).

SOUTH AFRICA: Steadier Rate Expectations Injects More Two-Way ZAR Risk

- The ZAR 3x6m FRA steadied on the back of today's CPI print, and may be signalling a bottoming-out of rate cut expectations through the turn of the year. The fading disinflationary impact of transport prices and accelerating food prices today will also be adding to steadier rates pricing, meaning CPI is likely to rise further in the coming months.

- This raises the focus on November 20th's SARB meeting (the last of the year), which sees pricing of a close to 60% chance for a 25bps cut. As such, two-way ZAR risk has risen on today's inflation data, particularly with the government's MTBPS likely in November - at which the Treasury may confirm a tighter, lower inflation target for the SARB.

- On the back of steadier rates pricing and the higher gold price (yesterday's corrective pullback notwithstanding), USDZAR and EURZAR could trade back toward early October lows (17.0683 and 19.8316 respectively) - although Trump's meeting with Xi in South Korea next week could be a key hurdle to further progress.

- News24 write on the inflation print: "Now it's chicken too [...] meat prices still red hot", in which they highlight the accelerating price rises for food staples, which clashes with the rise above the SARB's inflation target. While the rise in beef prices can be pinned on a recent outbreak of foot-and-mouth, higher pork, lamb and chicken prices are also contributing heavily. Housing costs also a key driver: September actual rentals rose on the quarter: 3.2% (Prev. 3.0%), with townhouse rentals up 5.4% (Prev. 4.1%).

OPTIONS: Expiries for Oct22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E732mln), $1.1595-00(E1.1bln), $1.1620-25(E586mln), $1.1640-50(E750mln) $1.1810-30(E1.1bln)

- USD/JPY: Y149.90-00($1.5bln), Y151.00($876mln), Y152.00($1.1bln)

- EUR/GBP: Gbp0.8740(E498mln)

- AUD/USD: $0.6535(A$516mln)

- NZD/USD: $0.5700(N$1.2bln)

- USD/CAD: C$1.3800($1.9bln), C$1.4085($551mln), C$1.4200($1.1bln)

- USD/CNY: Cny7.3000($749mln)

EQUITIES: FTSE-100 Stands Out in Soft Europe Trade

The trend condition in S&P E-Minis remains bullish and the contract is trading above support at the 50-day EMA. The average, currently at 6627.92, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. The trend direction in Eurostoxx 50 futures is up and This week’s gains reinforce this theme. The breach of 5689.00, the Oct 2 high and bull trigger, confirms a resumption of the uptrend.

COMMODITIES: Gold Pullback Deemed Corrective

A sharp pullback in Gold yesterday appears corrective - for now. Note that the trend is overbought and a deeper retracement would allow this condition to unwind. Support at the 20-day EMA, at $4031.4, has been pierced. A bearish theme in WTI futures remains intact and the move down last week reinforces current conditions. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend.

| Date | GMT/Local | Impact | Country | Event |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit | ||

| 22/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 22/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 22/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/10/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 23/10/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 23/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/10/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/10/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/10/2025 | - | ECB Lagarde at Euro Summit in Brussels | ||

| 23/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 23/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1330/1530 | ECB Lane Award Acceptance Speech | ||

| 23/10/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/10/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/10/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/10/2025 | 1425/1025 | Fed Governor Michael Barr | ||

| 23/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 23/10/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 23/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 23/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 23/10/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 24/10/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI |