MNI US MARKETS ANALYSIS - Treasuries Press to New Highs

Highlights:

- Treasuries extend to new cycle highs ahead of busy session for data

- FX options gear for most consequential payrolls print of Trump's second term

- Trump set to host business and tech leaders at the White House today

US TSYS: TYZ5 Sees Fresh Cycle Highs Ahead Of A Busy Docket

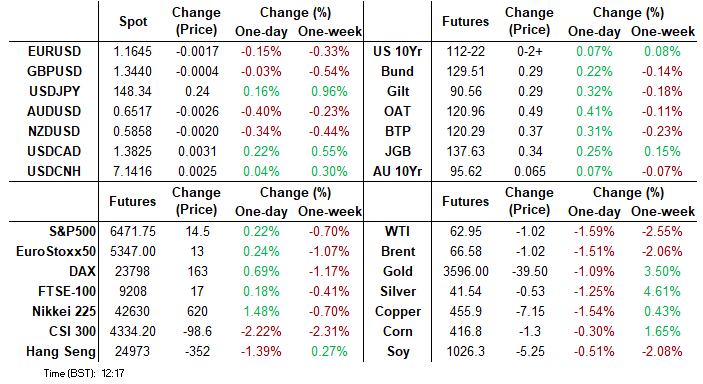

- After somewhat muted Asia trade, Treasuries have extended yesterday’s JOLTS-driven gains for new recent highs.

- It’s been assisted by firmer EGBs, with gains extended after the smooth passing of Spanish and French supply.

- Today sees many potential risk events, including ADP employment, jobless claims, ISM services, Miran’s nomination hearing, broader Fedspeak and potential Cook lawsuit headlines.

- Cash yields are 2-3bp lower on the day, with declines led by 7s.

- 30Y yields are now down to 4.8715% (-2.5bp) after yesterday’s failed clearance of 5.00% having last been higher on Jul 18.

- Curves mostly consolidate yesterday’s bull flattening, a move that continued right up to the close. That includes 5s30s at 120.8bp after fresh cycle highs of 124.6bp seen Tue/Wed.

- TYZ5 trades close to session and fresh short-term cycle highs of 112-23+ (+04), extending the mid-week shift away from Tuesday lows of 111-31. Volumes are thin at 215k ahead of a busy docket.

- It confirms a resumption of the uptrend and paves the way for an extension towards 112-28+ (Fibo projection) before the round 113-00.

- Data: Challenger jobs report Aug (1230ET), ADP report Aug (0815ET), Weekly jobless claims (0830ET), Productivity/ULCS Q2 final (0830ET), Trade balance Jul final (0830ET), S&P Global serv/comp PMI Aug final (0945ET), ISM services Aug (1000ET)

- Fedspeak: Williams on economic outlook and mon pol (1205ET, text + Q&A), Goolsbee in Q&A (1900ET, text tbd but Q&A) – see STIR bullet

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1130ET)

- Politics: President Trump hosts tech leaders for a dinner in the Rose Garden (1930ET)

FED: What To Watch In Today’s Fedspeak & Position Deliberations

Today’s Fedspeak comes from members at the center to dovish end of the FOMC spectrum:

- 1205ET – NY Fed’s Williams (permanent voter) speaks on economic outlook and mon pol (text + Q&A). In a thorough CNBC interview on Aug 27, he views policy as currently “modestly restrictive” (citing neutral at 1% or a bit below) and that at some point will be appropriate to move rates down, with every meeting definitely live.

- He characterized the economy as slowing but not stalling and that he expects the recently softer GDP growth to continue. There have been a slowdown in the pace of hiring but the labor force is also growing more slowly, with the unemployment at 4.2% still historically very low.

- 1900ET – Chicago Fed’s Goolsbee (’25 voter, dove) in moderated Q&A (text tbd, Q&A). Whilst historically one of the more dovish members on the FOMC, said on Aug 21 that he thought the rise in July services inflation was a “dangerous” data point that he hopes is just a blip. He thinks the current tariffs don’t look “one and done” whilst economic data more broadly are sending mixed messages.

Other areas to watch:

- 1000ET – Fed Governor nominee Miran testifies before the Senate banking committee. His prepared testimony released yesterday (link) didn’t reveal anything about his views on current rate policy or even the current economic outlook. It instead focused heavily on the importance of the FOMC's "independence", no doubt in light of recent criticism of the Trump administration's approach to the Fed. We of course would expect his rate leanings to sway dovish once in the position, but it's unclear how much he will reveal in his confirmation hearing back-and-forth with Senators.

- Time unknown - a potential decision by US District Court Judge Cobb in Fed Governor Cook's lawsuit against her "firing" by President Trump (a judgment had been anticipated to come as soon as Tuesday but the judge gave the Justice Department until Thursday to file another brief). It appears increasingly likely that the Trump administration won’t be able to nominate a replacement for Cook while she disputes her firing. Politico quoted Republican Senator Tillis as telling reporters yesterday “I’m not going to consider anybody until that’s been adjudicated". Tillis is on the Senate banking committee on which the Republicans have a 13-11 majority, so without his support it is hard to see them confirming a new nominee. It's still unclear however whether Cook will participate in the September FOMC meeting that starts in just under 2 weeks' time.

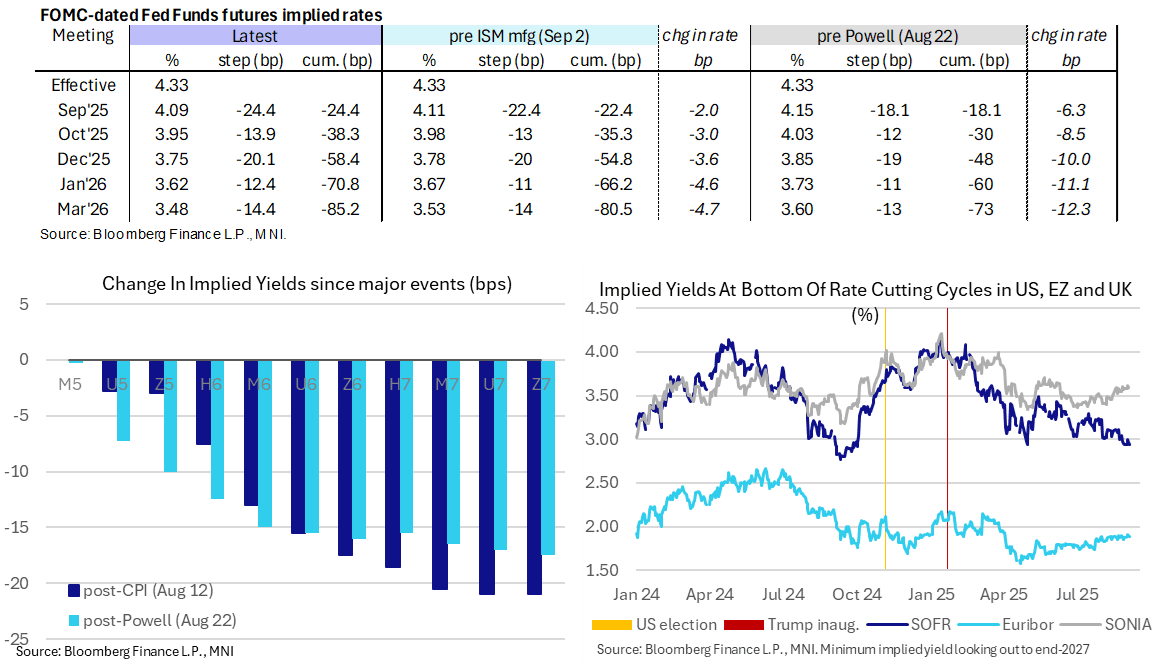

STIR: Holding Dovish Shift Ahead Of A Solid US Docket

- Fed Funds implied rates are holding yesterday’s dovish shift after a soft JOLTS report ahead of multiple labor releases between 0730-0830ET (prior to NFPs tomorrow) plus ISM services at 1000ET.

- There’s also various Fedspeak appearances plus possible headlines from the Cook case, to be discussed in a following bullet.

- Cumulative cuts from 4.33% effective: 24.5bp Sep, 38.5bp Oct, 58.5bp Dec, 71bp Jan and 85bp Mar.

- SOFR futures are broadly at session and yesterday’s highs, up to 2 ticks higher out to end-2027 contracts.

- The SOFR implied terminal yield of 2.945% (SFRH7, -1.5bp) is back probing last week’s lowest closes since late April and before that Oct 2024. It eyes close to 140bp of cuts from current levels.

Yesterday saw mostly patient Fedspeak before a Beige Book with a marked weakening in labor discussions.

- Musalem (’25 voter, hawk) thinks rates are currently at the right level given economic conditions. While he seems prepared to ease policy at some point in the future, and he recognizes that the balance of risks is tilting a little more toward missing on the employment mandate, he is comfortable with keeping policy "modestly restrictive" for now.

- Kashkari (’26 voter) said inflation is still too high and he is not yet in the camp that tariff-driven inflation will be a short-term phenomenon.

- Bostic (non-voter) still sees a single 25bp rate cut this year, with the September meeting in play. Rising inflation presents a greater risk to the dual mandate than a deteriorating labor market even as hiring has slowed.

- The Beige Book pointed to a slightly improved assessment of current economic activity in August versus the prior edition in July, with selling price pressures remaining modestly/ moderately to the upside. However, expectations were for future price increases (in part due to tariffs), and the latest edition suggests that labor market conditions have weakened. After a solid July Beige Book for labor, this was the weakest Beige Book report in terms of employment dynamics in at least the last year.

SOFR: Net Long Setting Dominated In Futures On Wednesday

OI data points to net long setting dominating in SOFR futures during Wednesday’s rally, with only fairly isolated instances of net short cover seen.

| 03-Sep-25 | 02-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,164,853 | 1,168,892 | -4,039 | Whites | +16,096 |

SFRU5 | 1,424,358 | 1,446,293 | -21,935 | Reds | +51,543 |

SFRZ5 | 1,572,634 | 1,532,299 | +40,335 | Greens | +12,811 |

SFRH6 | 1,141,852 | 1,140,117 | +1,735 | Blues | +1,153 |

SFRM6 | 952,541 | 922,707 | +29,834 |

|

|

SFRU6 | 895,879 | 890,564 | +5,315 |

|

|

SFRZ6 | 975,921 | 962,038 | +13,883 |

|

|

SFRH7 | 726,983 | 724,472 | +2,511 |

|

|

SFRM7 | 810,834 | 816,550 | -5,716 |

|

|

SFRU7 | 640,704 | 636,704 | +4,000 |

|

|

SFRZ7 | 653,759 | 642,178 | +11,581 |

|

|

SFRH8 | 417,856 | 414,910 | +2,946 |

|

|

SFRM8 | 333,277 | 336,559 | -3,282 |

|

|

SFRU8 | 224,231 | 220,697 | +3,534 |

|

|

SFRZ8 | 245,408 | 246,786 | -1,378 |

|

|

SFRH9 | 164,303 | 162,024 | +2,279 |

|

|

EUROPE ISSUANCE UPDATE

Spain auction results

- E1.555bln of the 1.40% Jul-28 Obli. Avg yield 2.204% (bid-to-cover 2.10x).

- E1.919bln of the 3.10% Jul-31 Obli. Avg yield 2.734% (bid-to-cover 2.08x).

- E1.48bln of the 4.20% Jan-37 Obli. Avg yield 3.425% (bid-to-cover 1.92x).

- E536mln of the 1.00% Nov-30 Obli-Ei. Avg yield 0.877% (bid-to-cover 2.83x).

France auction results

- Overall, no major alarm bells regarding demand for French debt at today’s auction. The top of the E9.5-11.0bln range was sold, with the sale unsurprisingly skewed towards the new 3.50% Nov-35 OAT. The 10-year OAT/Bund spread didn’t move much following the publication of the results, but has since tightened a touch to 79.3bps (-0.5bps today).

- The 10-year launch attracted a 2.18x bid-to-cover ratio for the E7.261bln issued. That’s below the 2.32x seen at the last re-opening of the previous on-the-run 10-year OAT (the 3.20% May-35 line), where E7.674bln was sold.

- It’s also slightly softer than the launch of the 3.20% May-35 OAT back in February, where a 2.23x cover was seen for the E8.641bln issued.

- The 15- and 30-year lines saw decent results. The stop prices were comfortably above pre-auction mid prices, even if the bid-to-cover ratios were a little weaker than the previous outing.

- E7.261bln of the 3.50% Nov-35 OAT. Avg yield 3.57% (bid-to-cover 2.18x).

- E1.93bln of the 3.60% May-42 OAT. Avg yield 4.04% (bid-to-cover 2.73x).

- E1.809bln of the 3.75% May-56 OAT. Avg yield 4.43% (bid-to-cover 2.66x).

UK auction results

- Nominal 10s30s flatten further post strong linker auction:

- It was a strong 20-year linker auction with a bid-to-cover of 3.91x and an average price of 72.277 notable above the secondary market pricing which prior to the auction hadn't exceeded 71.810.

- The strong auction has had knock on effects to nominal 20-year gilts and broader long-end gilts.

- 10s30s has already been flattening on the day but post-10am the flattening has accelerated and a further 0.9bp of flattening has taken place (2.0bp flatter soon after on the day at 83.3bp). This is now around 7bp off the steepest levels seen yesterday morning and approaching the flattest level since 14 August.

- The market is seeing the strong auction results as less concern regarding the UK long-end.

- GBP0.8bln of the 0.625% Mar-45 Linker. Avg yield 2.412% (bid-to-cover 3.91x).

US: Trump To Host Tech And Business Leaders At White House

US President Donald Trump is expected to host around two dozen tech and business leaders for an event in the newly-renovated White House Rose Garden at 19:30 ET 00:30 BST. According to an invite list, attendees include Meta founder Mark Zuckerberg, Apple CEO Tim Cook, Microsoft founder Bill Gates, and OpenAI founder Sam Altman. Former Trump advisor Elon Musk is not on the invite list. The dinner will follow an AI event in the White House hosted by First Lady Melania Trump.

- White House Press Secretary Karoline Leavitt told reporters on August 19 that the Rose Garden would soon host “what will be the best event in the history of the White House.”

- The event comes after Trump announced that the US government has taken a 10% ‘passive’ share of US chipmaker Intel, and promised more similar-such deals in the future. Much of the Intel deal was financed via re-purposed funds from the 2022 CHIPS and Science Act. Today’s event will provide a forum for tech leaders to gauge Trump’s plans to take similar stakes in other US companies in 'critical industries'.

- Bloomberg notes that the White House has signaled that it’s “looking to support leading AI chipmakers Nvidia Corp. and Advanced Micro Devices Inc. Those companies have said they plan to resume the sale of some AI chips in China after securing US government assurances that the transactions would be approved, a reversal from Trump’s earlier stance seeking to block those shipments in a bid to rein in China’s AI ambitions.”

SECURITY: 'Coalition Of Willing' Meeting In Paris Underway

A hybrid in-person and virtual meeting of the so-called Coalition of the Willing group of Ukraine-backers is underway in Paris. Several European leaders and Ukrainian President Volodymyr Zelenskyy will call US President Donald Trump to discuss the outcome of the meeting at 08:00 ET 13:00 BST 14:00 CET. Details of the call likely to hit wires at around 09:00 ET 14:00 BST 15:00 CET.

- The Elysee said the primary focus of today’s meeting is specific security guarantees that will be provided to Kyiv to ensure a peace agreement with Russia can hold.

- French President Emmanuel Macron announced yesterday, alongside Zelenskyy, that after months of work by military planners, Europe was finally ready to provide the guarantees and would politically endorse their plan at the meeting today, per the Guardian.

- The broad understanding is that any Ukrainian security guarantee will require a US backstop. It is unclear if Trump is willing to put US troops in Ukraine as part of an international peacekeeping force, but has appeared open to providing logistical support.

- Trump told reporters yesterday alongside Polish President Karol Nawrocki that the US will maintain its troop presence in Poland, nixing speculation that Trump could drawdown US force posture in Central and Eastern Europe.

- Trump said he’s ‘not happy’ with Russian President Vladimir Putin, but was ambiguous about pursuing new measures against Moscow. "I’ll be speaking to him over the next few days and we’re going to see... If we are unhappy about [Putin’s response], you will see things happen” he said.

FOREX: Steady Trade into Key US Datapoints

- Markets are generally quiet headed into the NY crossover, with an early phase of USD buying through the open broadly matching the price patterns we've seen so far this week. Volumes are lighter than average despite the minor move higher in the dollar, with EUR, JPY and GBP futures volumes ~30% below average for this time of day - although the roll into Z5 may be clouding this picture somewhat.

- Bucking the recent trend, GBP is seen firmer. Newsflow and fresh headlines are few and far between, with markets narrowing in on November 26th for the UK Budget announcement, which marks the next major macro event. For now, the bear threat in GBPUSD remains present following Tuesday’s sell-off. The pair has traded through a key support at 1.3391, the Aug 22 low. This signals scope for a deeper retracement and exposes 1.3315 next, a Fibonacci retracement. Clearance of this level would strengthen a bearish threat.

- Headlines suggesting that Japan and the US are in the final stages of talks to implement lower tariffs on Japanese automobile imports provided a moderate boost to the yen, allowing USDJPY to decline around 20 pips off the 148.41 session highs. Overall, the pair is operating within a relatively contained 60 pip range as investors await the plethora of US data this afternoon which includes ADP employment, weekly jobless claims and the ISM Services PMI. While all

important data points, a decisive breakout for USDJPY is unlikely ahead of tomorrow's employment report. - Larger FX options rolling off today include decent interest in and around 1.1629-80 (totalling close to E5bln) in EURUSD, while the interest in USDJPY is seen lower; $1.4bln is set to roll off at the Tuesday lows of Y147.00-15. The most sizeable AUD strike is north of yesterday's highs at 0.6595-00.

- ECB speakers today include Cipollone, who appears in EU Parliament and marks the likely last ECB speaker before the media blackout period into next week's rate decision - so is unlikely to deter markets from their current path at this stage. Fed's Williams is set to follow at the midpoint of the US session, speaking on the economic outlook and monetary policy.

OPTIONS: Markets Gear for Most Consequential Payrolls of Trump's Term So Far

- Overnight USD vols are well bid Thursday, helping markets quantify the market risk into Friday's NFP print. The vol premium added is sizeable: an average 3.9 point vol premium across G10 FX is close to double that seen for the July, June and May NFP prints.

- As such, the vol premium into this week's NFP is the largest since January, and the largest of Trump's second Presidential term so far. Both EUR and AUD overnight vols have cleared 15 points, hitting multi-month highs in the process.

- Given recent intraday vol in JPY, no surprise to see USD/JPY isolated by options markets into tomorrow - overnight vol of ~18.5 points blows out the break-even on a USDJPY straddle to just over 100 pips, double that of the same option struck earlier in the week.

- In our payrolls preview, we highlight the focus on the potential “breakeven” rate of payrolls growth, as well as the skew towards 4.2% evident in the unemployment rate this month: it wouldn’t take much from the 4.25% in July.

FOREX: Clustered Options Interest Could Define Today's EUR Range

Larger FX options rolling off today include decent interest in and around 1.1629-80 (totalling close to E5bln) in EURUSD, while the interest in USDJPY is seen lower; $1.4bln is set to roll off at the Tuesday lows of Y147.00-15. The most sizeable AUD strike is north of yesterday's highs at 0.6595-00. Full list here:

- EUR/USD: $1.1590-00(E2.9bln), $1.1629-30(E590mln), $1.1640-50(E1.9bln), $1.1670-80(E2.3bln), $1.1700(E1.3bln), $1.1720(E563mln), $1.1750(E1.3bln)

- USD/JPY: Y146.00($611mln), Y147.00-15($1.4bln), Y147.90-00($520mln)

- EUR/GBP: Gbp0.8670-90(E520mln)

- AUD/USD: $0.6475(A$574mln), $0.6595-00(A$1.7bln)

- USD/CAD: C$1.3755-65($978mln)

EQUITIES: Primary Trend Set-Up in Eurostoxx Futures is Bullish

- The primary trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective. However, the contract has breached 5371.32, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5387.15, the 20-day EMA.

- A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6340.81. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

COMMODITIES: Fresh All-Time Highs for Gold Reinforces Current Conditions

- A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. Yesterday’s move down highlights a possible early reversal signal and the end of the corrective phase. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle and the metal is trading closer to its recent highs. This week’s gains resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3600.00 handle. Initial firm support to watch lies at $3411.8, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams | ||

| 04/09/2025 | 2300/1900 | Chicago Fed's Austan Goolsbee | ||

| 05/09/2025 | 2330/0830 | ** | average wages (p) | |

| 05/09/2025 | 2330/0830 | ** | Household spending | |

| 05/09/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/09/2025 | 0600/0700 | *** | Retail Sales | |

| 05/09/2025 | 0645/0845 | * | Foreign Trade | |

| 05/09/2025 | 0800/1000 | * | Retail Sales | |

| 05/09/2025 | 0900/1100 | * | Employment | |

| 05/09/2025 | 0900/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |