FED: What To Watch In Today’s Fedspeak & Position Deliberations

Sep-04 10:28

Today’s Fedspeak comes from members at the center to dovish end of the FOMC spectrum:

- 1205ET – NY Fed’s Williams (permanent voter) speaks on economic outlook and mon pol (text + Q&A). In a thorough CNBC interview on Aug 27, he views policy as currently “modestly restrictive” (citing neutral at 1% or a bit below) and that at some point will be appropriate to move rates down, with every meeting definitely live.

- He characterized the economy as slowing but not stalling and that he expects the recently softer GDP growth to continue. There have been a slowdown in the pace of hiring but the labor force is also growing more slowly, with the unemployment at 4.2% still historically very low.

- 1900ET – Chicago Fed’s Goolsbee (’25 voter, dove) in moderated Q&A (text tbd, Q&A). Whilst historically one of the more dovish members on the FOMC, said on Aug 21 that he thought the rise in July services inflation was a “dangerous” data point that he hopes is just a blip. He thinks the current tariffs don’t look “one and done” whilst economic data more broadly are sending mixed messages.

Other areas to watch:

- 1000ET – Fed Governor nominee Miran testifies before the Senate banking committee. His prepared testimony released yesterday (link) didn’t reveal anything about his views on current rate policy or even the current economic outlook. It instead focused heavily on the importance of the FOMC's "independence", no doubt in light of recent criticism of the Trump administration's approach to the Fed. We of course would expect his rate leanings to sway dovish once in the position, but it's unclear how much he will reveal in his confirmation hearing back-and-forth with Senators.

- Time unknown - a potential decision by US District Court Judge Cobb in Fed Governor Cook's lawsuit against her "firing" by President Trump (a judgment had been anticipated to come as soon as Tuesday but the judge gave the Justice Department until Thursday to file another brief). It appears increasingly likely that the Trump administration won’t be able to nominate a replacement for Cook while she disputes her firing. Politico quoted Republican Senator Tillis as telling reporters yesterday “I’m not going to consider anybody until that’s been adjudicated". Tillis is on the Senate banking committee on which the Republicans have a 13-11 majority, so without his support it is hard to see them confirming a new nominee. It's still unclear however whether Cook will participate in the September FOMC meeting that starts in just under 2 weeks' time.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Tuesday Data Calendar: Import/Export, PMIs, ISM Services, 3Y Sale

Aug-05 10:25

- US Data/Speaker Calendar (prior, estimate)

- 08/05 0830 Trade Balance (-$71.5B, -$61.0B)

- 08/05 0830 Exports MoM (-4.0%, --), Imports MoM (-0.10%, --)

- 08/05 0945 S&P Global US Services PMI (55.2, 55.2)

- 08/05 0945 S&P Global US Composite PMI (54.6, 54.6)

- 08/05 1000 ISM Services Index (50.8, 51.5)

- 08/05 1000 ISM Services Prices Paid (67.5, 66.5)

- 08/05 1000 ISM Services New Orders (51.3, --)

- 08/05 1000 ISM Services Employment (47.2, --)

- 08/05 1130 US Tsy $85B 6W & $50B 52W bill auctions

- 08/05 1300 US Tsy $58B 3Y Note auction (91282CNU1)

- Source: Bloomberg Finance L.P. / MNI

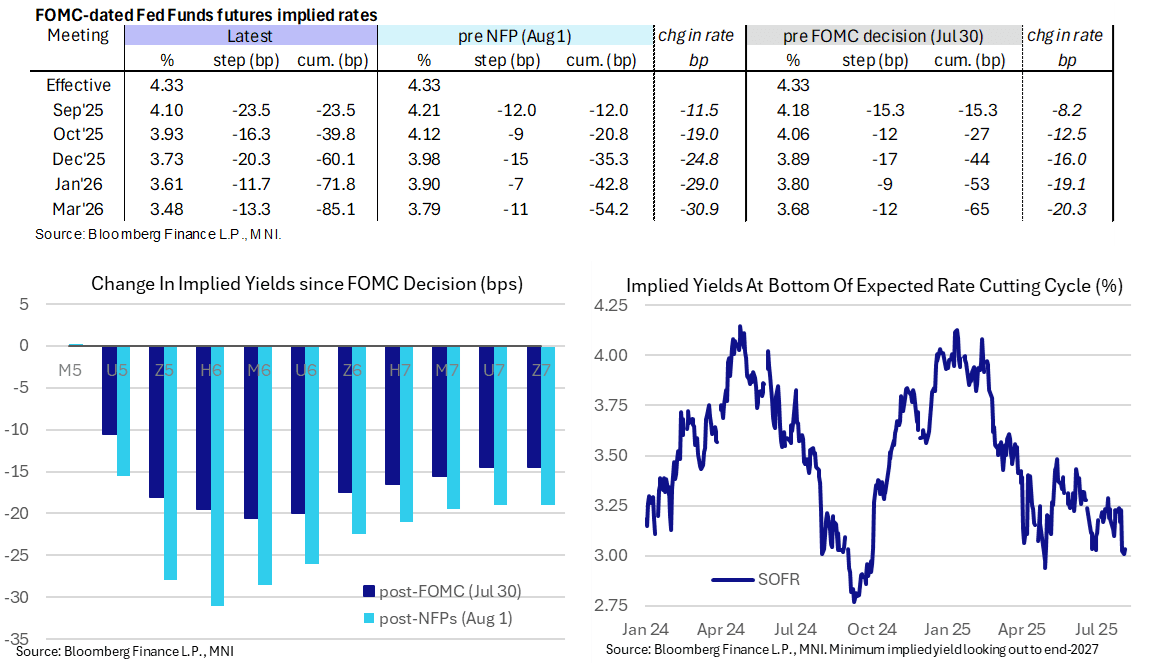

STIR: September Fed Cut Close To Fully Priced, ISM Services Headlines

Aug-05 10:25

- Fed Funds implied rates are 1.5-3bp higher on the day for nearer-term meetings having lifted off lows seen after a more dovish take from SF Fed’s Daly (non-voter) late yesterday to Reuters vs Friday’s more patient tone of Bostic and Hammack.

- They still hold all of Friday’s large dovish shift on the weak payrolls report and the helping hand from soft ISM mfg, with a cut close to being fully priced for the next meeting in September.

- Cumulative cuts from 4.33% effective: 23.5bp Sep (vs 12bp pre-NFP), 40bp Oct, 60bp Dec (vs 35bp), 72bp Jan and 85bp Mar.

- The SOFR implied terminal yield of 3.035% (SFRH7) is 2.5bp higher from yesterday’s lowest close since late April, still eyeing more than five cuts from current levels.

- Today sees main macro focus on ISM services plus any indication of potential contenders in for Fed Governor Kugler’s position and the new BLS commissioner.

- Daly said “I was willing to wait another cycle, but I can’t wait forever” [on rate cut prospects]. She still sees the two rate cuts pencilled in for this year as “an appropriate amount of recalibration”. “We of course could do fewer than two (rate cuts) if inflation picks up and spills over or if the labor market springs back”. However, “I think the more likely thing is that we might have to do more than two...we also should be prepared in my judgment to do more if the labor market looks to be entering that period of weakness and we still haven’t seen spillovers to inflation”

HONG KONG: Interbank Liquidity More Than Halved, But No Relief for HKD

Aug-05 10:22

- USD/HKD underwent a now-usual phase of sales at the local open in price action reminiscent of HKMA HKD buying (unlike other phases of USD/HKD downside e.g. On Jul28, which did not match the pattern of intervention).

- As such, a further step lower of ~HKD 6.5bln in the HKMA Aggregate Balance is expected this week, pressing interbank liquidity down to HKD72.5bln and closer to the pre-HKD rout levels of early May (circa HKD 45bln). This leaves interbank liquidity at less than half the prevailing level in May - however there has been minimal relief in USD/HKD spot which, again, is pressuring 7.85.

- Persistent HKD pressure comes as the carry trade dynamics remain highly favourable: overnight and one-week HKD swap rates remain heavily supressed (0.35% and 0.31$ respectively) which is limiting the advance in HIBOR (1m has failed to rise materially above 1%) and, in turn, keeping long USD/HKD a favourable carry trade.

- This leaves a material lag between falling interbank liquidity, the side effect of higher local rates, and a stronger spot HKD. Low demand for HK securities and still-low levels of corporate activity are largely responsible here - meaning narrowing US-HK rate spreads via Fed easing will likely be required to pull USD/HKD lower barring a material improvement in the HK IPO pipeline.