MNI US MARKETS ANALYSIS - STIRs Hold Powell Impact

Highlights:

- US STIR holds impact of less-than-hawkish Fed cut, next 25bps step fully priced by June

- Swiss National Bank keeps policy unchanged, hints that negative interest rates unlikely

- Weekly claims data in focus, curve sits bull steeper post-Powell

US TSYS: FOMC Bull Steepening Consolidated, Claims and 30Y Supply Ahead

Treasuries have seen two-sided flow overnight, especially at the long-end, but are back to little changed as they consolidate yesterday’s FOMC communications being less hawkish than expected. Today’s focus will be on jobless claims data after a surprise dip last week and then 30Y supply with four of the past five months tailing.

- Cash yields are 0.6-1.6bp lower on the day, with declines led by 5s and 7s.

- Curves also hold yesterday’s steepening, with 5s30s at 106.5bps vs ~101bp before the FOMC.

- TYH6 trades at 112-14+ (+07+) off an earlier high of 112-18+, on solid overnight volumes of 405k as regional markets react to yesterday’s FOMC announcements

- Yesterday’s push higher is deemed a corrective bounce, lifting off yesterday’s latest lows of 111-29 (which had started to eye Fibo projection support at 111-19) with clearance of resistance at 112-10+ (Nov 20 low). Next resistance is seen at 112-24 (20-day EMA).

- The biggest surprise at yesterday's Fed decision was the announcement of $40bln in monthly RMPs, starting Friday vs our expectation of 1H26.

- Data: Weekly jobless claims (0830ET), International trade Sep (0830ET), Wholesale sales/inventories Sep/Sep F (1000ET), State labor data Sep (1000ET), Dallas Fed Weekly economic index (1130ET)

- Coupon issuance: US Tsy $22B 30Y Bond action re-open - 912810UP1 (1300ET). Last month’s 30Y tailed by 1bp, a fourth tail in the last five, and saw mixed-to-weak peripheral stats including notably a second lowest bid-to-cover since Nov 2023.

- Bill issuance: US Tsy $85B 4W & $80B 8W bill auctions (1130ET)

- Politics: WH Press Sec Leavitt briefing (1300ET), Trump in signing ceremony (1645ET), Trump remarks at Congressional Ball (2015ET)

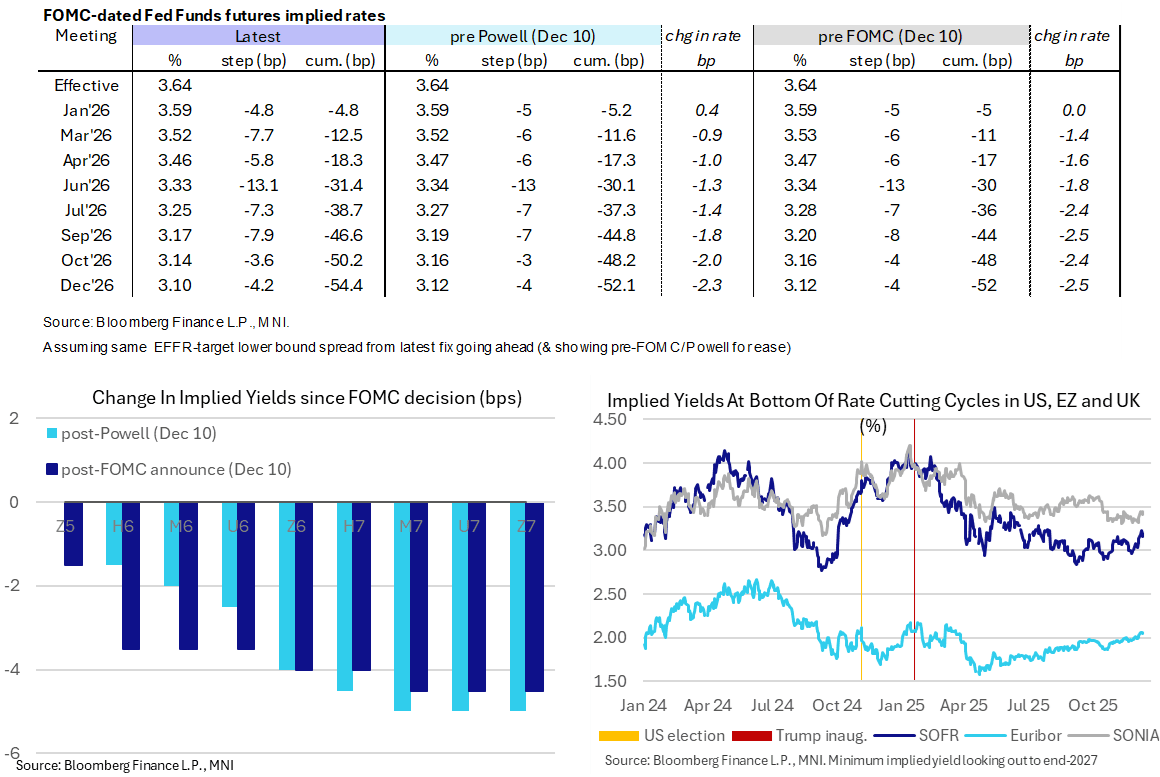

STIR: Holding Impact From A Not So Hawkish 25bp Cut

- Fed Funds implied rates are little changed overnight for 1H26 meetings and up to 1bp higher for 2H26 as they broadly consolidate the modest dovish reaction to yesterday’s 25bp cut communication leaning less hawkish than expected (MNI Review, link).

- Cumulative cuts from assumed 3.64% effective: 5bp Jan, 12.5bp Mar, 18.5bp Apr, 31bp Jun, 46.5bp Sep and 54bp Dec.

- SOFR futures are flat to +0.04 in most 2027 contracts, helping the terminal implied yield of 3.165% (Z6 and H7) pull back further from Tuesday’s 3.225% at what was the highest close since July. It's still more than 15bp higher than in late November after NY Fed's Williams had set up this week's cut.

- Today’s macro focus is on weekly jobless claims after initial claims slid in what was likely a distortion from difficulties in adjusting around Thanksgiving, whilst we also see catch-up for international trade and wholesale trade for September.

- The FOMC blackout remains in place today, as is customary, with tomorrow’s schedule set to start with three of those of who objected to Wednesday’s cut. Goolsbee dissented in favor of a hold and ’26 voters Paulson and Hammack were likely within the 6 “soft dissent” dots. Hammack was also likely one of the 3 dots who would have preferred to have kept rates on hold at previous levels through 2026 as well.

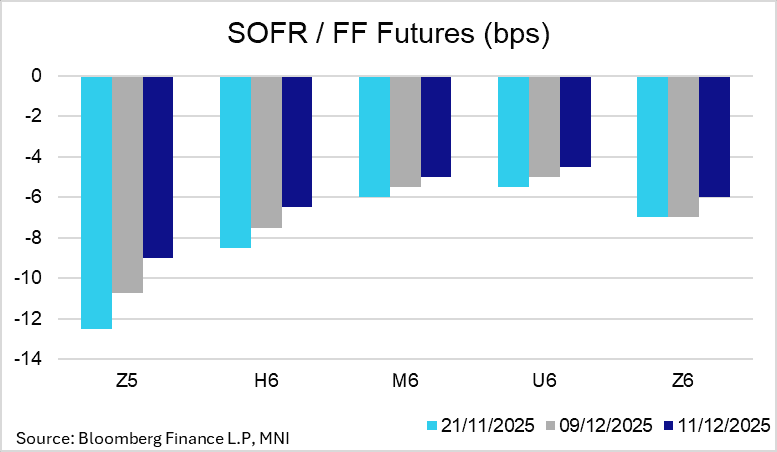

US TSYS/OVERNIGHT REPO: Fed RMP Announcement Drove Narrowing In SOFR/FF Basis

The biggest surprise at yesterday’s Fed decision was the announcement of $40bln in monthly reserve management purchases (RMPs), starting Friday. The decision spurred significant activity in SOFR/FF basis markets, and futures-implied spreads through the next year are now up 0.5-1.75bps relative to Tuesday’s close.

- Post-Fed activity was centred at the front of the curve, with the Fed intending to keep RMPs “elevated” for a few months to respond to anticipated pressures at year-end and during the April tax season.

- The NY Fed will publish a tentative schedule for the next 30-days of purchase operations today.

- CIBC caution that “$40bn per month does not eliminate year-end risks…we expect them to buy very aggressively in December in order to get some extra reserves in place. But even if they buy $30bn before year end, that is small relative to historical increases in the RRP on year-end.”

- Beyond April, analyst views on the scale of RMPs are mixed, ranging from $5-10bln (Danske) to $25bln (Wells Fargo). UBS expect regular purchases to reach a notable $60bln per month by 2027.

- On the markets side, TD write that “the announcement of RMP should remain a tailwind for swap spreads, and we remain positioned long 30y swap spreads. However, we believe RMP will be a swap spread curve flattener as front-end spreads lead the widening move”.

- Meanwhile, JP Morgan revise their "midyear swap spread targets, but we still look for a modest narrowing from current levels and we still look for a modest flattening of the spread curve”

- 2-year swap spreads have consolidated at around -17.5bps, just over 2bps wider than before the Fed decision. Meanwhile, 30-year spreads are just under 1bp wider relative to pre-Fed levels, currently at -70bps.

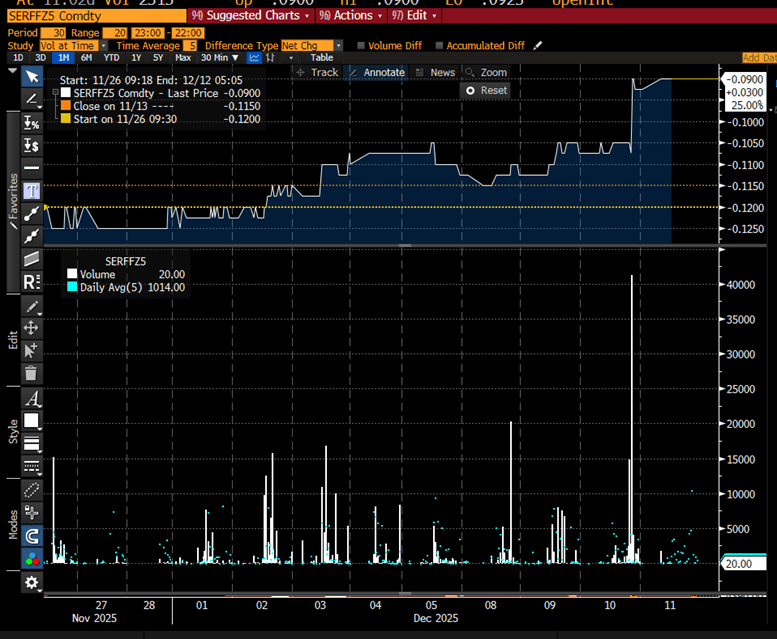

Figure 1: SOFR/FF Z5 Future Price and Volumes Through December (Source: Bloomberg Finance L.P)

Figure 2: SOFR/FF Futures Changes (Source: Bloomberg Finance L.P)

SOFR: Net Long Setting In The Reds Dominated In Futures On Wednesday

SOFR futures point to a mix of net long setting and short cover in SOFR futures as contracts settled higher in the wake of yesterday’s FOMC decision, with the former proving to be more prominent than the latter.

- A reminder that our macro team noted that with most of the main Fed communications having been well-anticipated (alongside the expected 25bp rate cut) - from the subtle shift in forward guidance in the Statement, to the unchanged Dot Plot rate forecast medians – overall the meeting outcome brought some slight dovish surprises and a concomitant market reaction.

- As a result, net long setting in SFRU6-H7 provided the most concentrated positioning swing.

| 10-Dec-25 | 09-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,304,459 | 1,303,034 | +1,425 | Whites | +20,749 |

SFRZ5 | 1,655,412 | 1,592,890 | +62,522 | Reds | +131,730 |

SFRH6 | 1,426,785 | 1,462,338 | -35,553 | Greens | +1,668 |

SFRM6 | 1,117,329 | 1,124,974 | -7,645 | Blues | +3,945 |

SFRU6 | 1,177,019 | 1,095,083 | +81,936 |

|

|

SFRZ6 | 1,173,327 | 1,128,700 | +44,627 |

|

|

SFRH7 | 865,333 | 849,826 | +15,507 |

|

|

SFRM7 | 770,831 | 781,171 | -10,340 |

|

|

SFRU7 | 808,756 | 808,399 | +357 |

|

|

SFRZ7 | 828,364 | 832,484 | -4,120 |

|

|

SFRH8 | 444,052 | 443,390 | +662 |

|

|

SFRM8 | 402,418 | 397,649 | +4,769 |

|

|

SFRU8 | 376,897 | 369,370 | +7,527 |

|

|

SFRZ8 | 323,911 | 328,615 | -4,704 |

|

|

SFRH9 | 196,537 | 195,353 | +1,184 |

|

|

SFRM9 | 205,604 | 205,666 | -62 |

|

|

CHINA: CEWC Statement Provides Some Detail on Policy, But Inline With Politburo

The Politburo held their December meeting on Monday - so to be expected the Central Economic Work Conference follows a few days later. We already got a readout from the Politburo earlier this week so this is shouldn't be many new details here - but is slightly more specific on policy measures (in particular, the reference to the "use of the RRR and interest rate cuts"), which should all be broadly inline with the fourth plenum.

- Further measures to help support the domestic housing market: "*CHINA ENCOURAGES BUYING EXISTING HOMES FOR SOCIAL HOUSING" - bbg

Worth noting there was no specific reference to stabilizing the real estate or stock market in the Politburo meeting readout (likely reflecting the sharp YTD rally in local equities) - but these headlines suggest there's still concern over stability housing markets, which will continue to receive policy support.

HUNGARY: Our Thoughts on the Orban Presidency Piece

- The possibility of pushing through the reform to a more dominant presidential system could be politically damaging – as the Bloomberg piece notes: “That path would be risky, though, if it was seen as going against the popular will.” Furthermore, Orban would need to use Fidesz’s current supermajority in parliament before April's election to push through the change.

- It is also worth noting that at least some of Bloomberg’s sources are from the Tisza party – “The possibility of Orban pushing through an overhaul of the presidency is one of many scenarios Tisza hasn’t ruled out, according to a person familiar with the thinking of the party’s leadership” – and therefore it would not be surprising to see Orban refute the report as political gamesmanship.

- Just last month, in response to a question about a presidential system, the head of the PM's Office, Gergely Gulyas, said the issue had been raised when the constitution was being redrawn after 2010 but it was decided that the parliamentary system was in line with Hungarian public law traditions and characteristic of functioning democracies in the region. "No change is expected, even in the event of a two-thirds victory," he said.

FOREX: USD Weakness Post ‘Not So Hawkish Cut’ Offset By Oracle Concerns

- The Dollar Index is holding onto the bulk of the post-Fed weakness, as the meeting outcome brought some slight dovish surprises and a concomitant market reaction. Notably, Chair Powell did not push back forcefully against a January cut, if anything sounding less cautionary about a follow-up cut than he sounded in October when the FOMC delivered an actual “hawkish cut”.

- After a solid bump lower yesterday, the DXY extended its 3-week pullback to 1.85%, printing a 98.54 low overnight. However, a warning from U.S. cloud computing giant Oracle about lower-than-expected profit and revenue outlooks has significantly dented risk-sentiment, providing an offsetting bid for the greenback, which tilts the DXY into positive territory ahead of the NY crossover.

- Alongside the softer risk tone, weaker-than-expected Australian employment data has hampered AUDUSD (-0.43%), which erased the entirety of the post-Fed advance by sinking to 0.6627 overnight. A net change of -21.3k jobs was concentrated among full time workers, however, a stable unemployment rate at 4.3% provided a silver lining to the release.

- From a near-term perspective, the AUDUSD trend is overbought, and a pullback would allow this condition to unwind. Key support to watch is at 0.6571, the 20-day EMA. AUDJPY’s pullback from the week’s high totalled 1% overnight amid the sensitivity to risk, however the cross remains comfortably above the recent 1.0240 breakout.

- Elsewhere, the Swiss National Bank kept rates unchanged, broadly maintaining their prior guidance. This has allowed yesterday’s theme of CHF outperformance to prevail, with USDCHF sliding further back below the 0.8000 mark, while EURCHF extends the week’s retreat from 0.9400 to around 60 pips.

OPTIONS: Expiries for Dec11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1595-00(E3.2bln), $1.1610(E3.9bln), $1.1710(E1.4bln), $1.1800(E1.7bln)

- USD/JPY: Y154.95-00($1.1bln), Y156.00($2.8bln)

- AUD/USD: $0.6550(A$1.6bln), $0.6640(A$732mln)

- USD/CAD: C$1.4000($968mln)

EQUITIES: Eurostoxx Futures Bull Cycle Intact, Key Resistance at 5825.00

- A bull cycle in Eurostoxx 50 futures remains intact and short-term weakness is considered corrective - for now. Price is trading above the 20- and 50-day EMAs, and sights are on 5742.40 next (pierced), 76.4% of the Nov 13 - 21 bear leg. A clear breach of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support to watch lies at 5632.90, the 50-day EMA.

- A bull cycle in S&P E-Minis remains intact and today’s pullback appears corrective - for now. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A resumption of gains would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support to watch is at 6815.09, the 20-day EMA.

COMMODITIES: Sustained Weakness for WTI Would Expose Bear Trigger at $55.99

- A bearish theme in WTI futures remains intact. Note that moving average studies are in a bear-mode position, highlighting a dominant medium-term downtrend. A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Gold is in consolidation mode. The trend set-up remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4051.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household debt-to-income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/12/2025 | 0430/1330 | ** | Industrial Production | |

| 12/12/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 12/12/2025 | 0700/0800 | ** | Unemployment | |

| 12/12/2025 | 0700/0700 | ** | Trade Balance | |

| 12/12/2025 | 0700/0700 | ** | Index of Services | |

| 12/12/2025 | 0700/0700 | ** | Index of Production | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0745/0845 | *** | HICP (f) | |

| 12/12/2025 | 0800/0900 | *** | HICP (f) | |

| 12/12/2025 | 0930/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/12/2025 | - | *** | Money Supply | |

| 12/12/2025 | - | *** | Social Financing | |

| 12/12/2025 | - | *** | New Loans | |

| 12/12/2025 | 1300/0800 | Philly Fed's Anna Paulson | ||

| 12/12/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 12/12/2025 | 1330/0830 | * | Building Permits | |

| 12/12/2025 | 1330/0830 | ** | Wholesale Trade | |

| 12/12/2025 | 1330/0830 | Cleveland Fed's Beth Hammack | ||

| 12/12/2025 | 1535/1035 | Chicago Fed's Austan Goolsbee | ||

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |