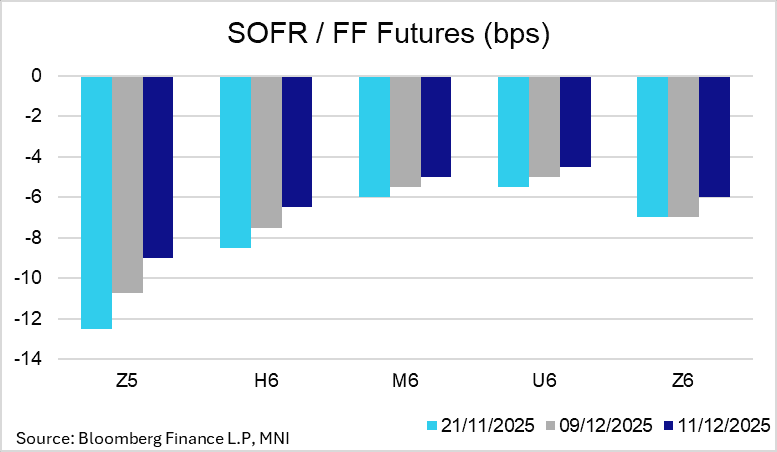

US TSYS/OVERNIGHT REPO: Fed RMP Announcement Drove Narrowing In SOFR/FF Basis

The biggest surprise at yesterday’s Fed decision was the announcement of $40bln in monthly reserve management purchases (RMPs), starting Friday. The decision spurred significant activity in SOFR/FF basis markets, and futures-implied spreads through the next year are now up 0.5-1.75bps relative to Tuesday’s close.

- Post-Fed activity was centred at the front of the curve, with the Fed intending to keep RMPs “elevated” for a few months to respond to anticipated pressures at year-end and during the April tax season.

- The NY Fed will publish a tentative schedule for the next 30-days of purchase operations today.

- CIBC caution that “$40bn per month does not eliminate year-end risks…we expect them to buy very aggressively in December in order to get some extra reserves in place. But even if they buy $30bn before year end, that is small relative to historical increases in the RRP on year-end.”

- Beyond April, analyst views on the scale of RMPs are mixed, ranging from $5-10bln (Danske) to $25bln (Wells Fargo). UBS expect regular purchases to reach a notable $60bln per month by 2027.

- On the markets side, TD write that “the announcement of RMP should remain a tailwind for swap spreads, and we remain positioned long 30y swap spreads. However, we believe RMP will be a swap spread curve flattener as front-end spreads lead the widening move”.

- Meanwhile, JP Morgan revise their "midyear swap spread targets, but we still look for a modest narrowing from current levels and we still look for a modest flattening of the spread curve”

- 2-year swap spreads have consolidated at around -17.5bps, just over 2bps wider than before the Fed decision. Meanwhile, 30-year spreads are just under 1bp wider relative to pre-Fed levels, currently at -70bps.

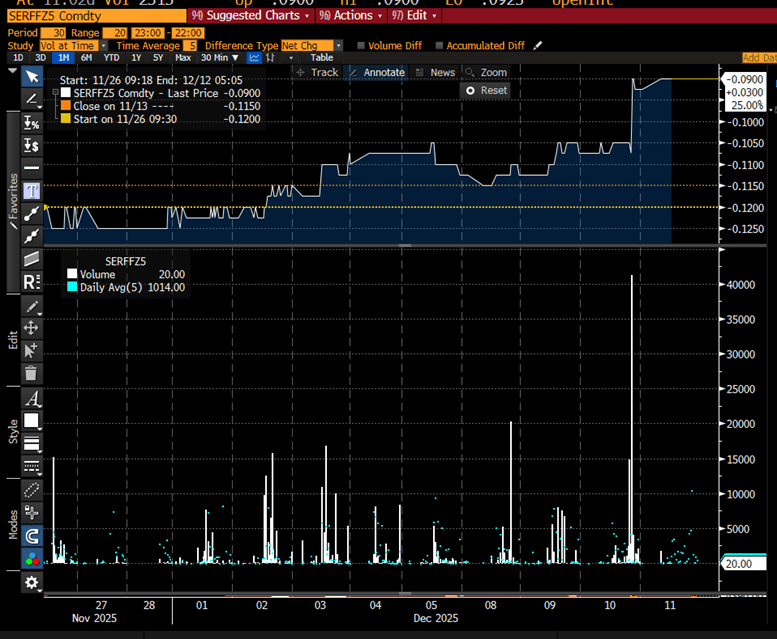

Figure 1: SOFR/FF Z5 Future Price and Volumes Through December (Source: Bloomberg Finance L.P)

Figure 2: SOFR/FF Futures Changes (Source: Bloomberg Finance L.P)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Weekly ADP Series A Potential Test Of Steady US Rates

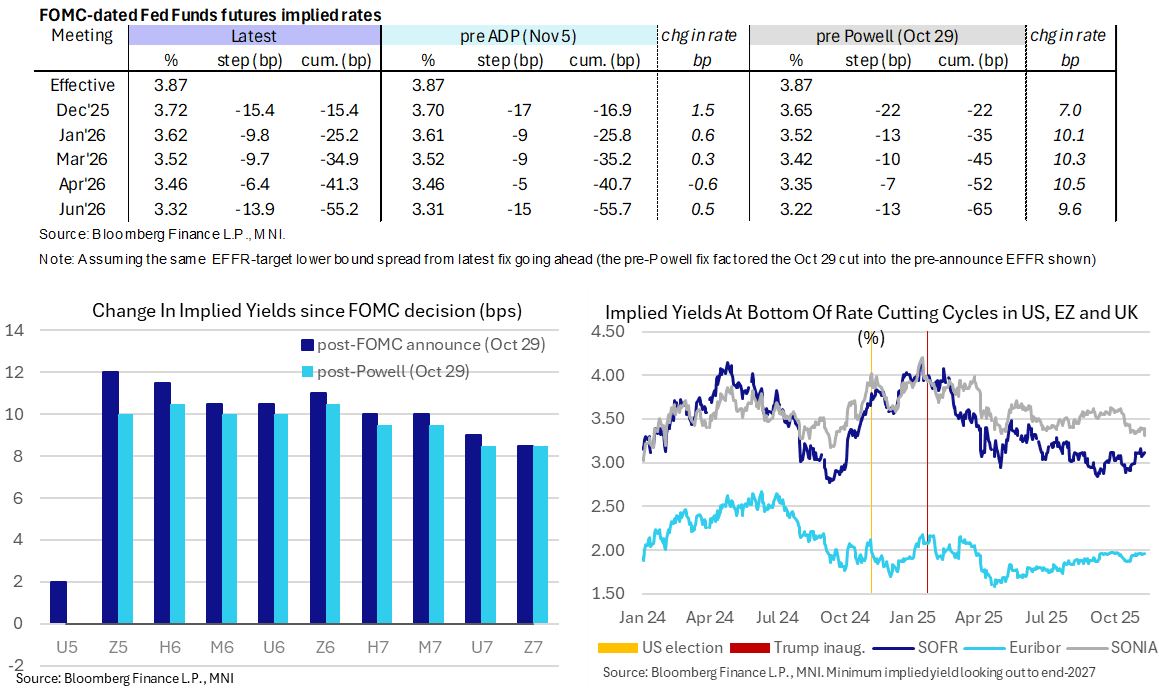

- Fed Funds implied rates are little changed on the day, with today’s data focus likely on the first known-ahead-of-time publication of weekly ADP series at 0815ET.

- Cumulative cuts from 3.87% effective: 15.5bp Dec, 25bp Jan, 35bp Mar, 41.5bp Apr and 55bp Jun.

- SOFR futures are also little changed, between 1 tick firmer (Z5 and H6) and 1 tick lower (Z7).

- It leaves the terminal implied yield at 3.115% (H7) off last week’s multi-month high of 3.16% before being helped lower by soft alternative labor data.

- Today’s only scheduled Fedspeak comes overnight with Fed Governor Barr (voter) in Singapore, speaking on AI and innovation at 2225ET (text + Q&A). He said on Nov 6 that the Fed has made progress on inflation but there is still "work to do". Wealthier households are thriving in a two-speed economy whilst the Fed must pay attention to ensuring the job market is solid.

OUTLOOK: Price Signal Summary - Resistance In GBPUSD Intact For Now

- In FX, EURUSD is holding on to its recent gains. The latest recovery is - for now - considered corrective and has allowed a recent oversold condition to unwind. Resistance to watch remains the 20-day EMA, at 1.1584. It has been pierced, a clear break of it would signal scope for an extension towards the 50-day EMA, at 1.1624. A reversal would refocus attention on the bear trigger at 1.1469, the Nov 5 low. Clearance of this level would resume the downtrend.

- A bear trend in GBPUSD remains intact and recent gains still appear corrective. The move higher is allowing an oversold trend condition to unwind. Firm short-term resistance to watch is at the 20-day EMA, at 1.3231. A break of this hurdle would signal scope for an extension towards the 50-day EMA, at 1.3334. For bears, a resumption of the downtrend would open 1.2971, a 1.382 projection of the Sep 17 - 25 - Oct 1 price swing. The bear trigger is 1.3010, Nov 4 and 5 low.

- The trend structure in USDJPY remains bullish and today’s marginal fresh cycle high reinforces bullish conditions. Moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. A clear break of the bull trigger at 154.48, the Nov 4 high, would confirm a resumption of the uptrend and open 154.80, the Feb 12 high. First important support to watch lies at 152.70, the 20-day EMA.

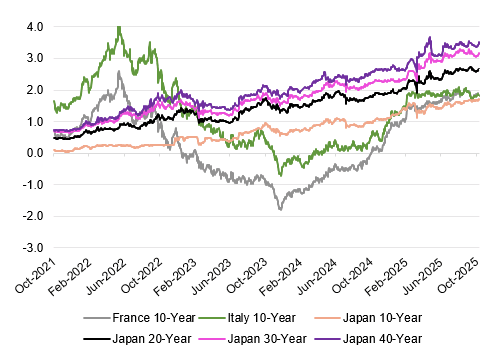

BONDS: OAT & BTP FX-Hedged Yields Top 10-Year JGBs In Japan, But Not Super Longs

Further to the above, not that both 10-Year Italian & French yields provide a modest 10-15bp pickup vs. 10-Year JGBs, when accounting for 3-month FX hedging costs from the perspective of a Japanese investor.

- This helps explain some of the demand, particularly given ongoing fiscal uncertainty in Japan.

- Those same FX hedging cost-adjusted yields are still some way below 20-, 30- & 40-Year JGBs, as seen in the chart below.

Fig. 1: JGB Yields Vs. 10-Year Italian & French Yields FX-Hedged From The Perspective Of A Japanese Investor (%)

Source: MNI - Market News/Bloomberg Finance L.P.