HUNGARY: Our Thoughts on the Orban Presidency Piece

- The possibility of pushing through the reform to a more dominant presidential system could be politically damaging – as the Bloomberg piece notes: “That path would be risky, though, if it was seen as going against the popular will.” Furthermore, Orban would need to use Fidesz’s current supermajority in parliament before April's election to push through the change.

- It is also worth noting that at least some of Bloomberg’s sources are from the Tisza party – “The possibility of Orban pushing through an overhaul of the presidency is one of many scenarios Tisza hasn’t ruled out, according to a person familiar with the thinking of the party’s leadership” – and therefore it would not be surprising to see Orban refute the report as political gamesmanship.

- Just last month, in response to a question about a presidential system, the head of the PM's Office, Gergely Gulyas, said the issue had been raised when the constitution was being redrawn after 2010 but it was decided that the parliamentary system was in line with Hungarian public law traditions and characteristic of functioning democracies in the region. "No change is expected, even in the event of a two-thirds victory," he said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: BLOCK/Screen: Feb'25 SOFR Call Condor

- Total 4,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 0.75 at 0612:07ET

US 10YR FUTURE TECHS: (Z5) Bear Threat Remains Present

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02 High Nov 5& 7 and a key near-term resistance

- PRICE: 112-21+ @ 11:10 GMT Nov 11

- SUP 1: 112-09+ Low Nov 5

- SUP 2: 112-08+ 38.2% retracement of May - Oct Upleg

- SUP 3: 112-08/06 100-dma / Low Sep 25 and a reversal trigger

- SUP 4: 112-02 Trendline support drawn from the May 22 low

A short-term bear theme in Treasuries remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low. Resistance to watch is 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.

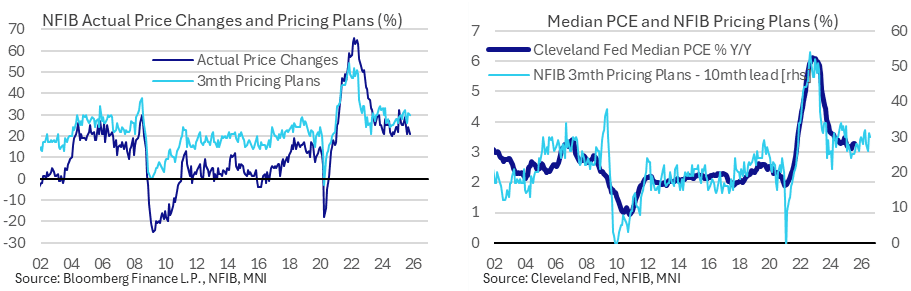

US DATA: NFIB Pricing Plans Cool Slightly But Still Stubbornly High

Pricing plans within the NFIB survey for October were softer than in September but hold at a level that points to median PCE inflation remaining stubbornly above the 2% target. Elsewhere in the survey, weaker profit trends drove an admittedly small decline in optimism, with the largest attributing factor from weaker sales followed by the cost of materials.

- The NFIB small business survey for October saw its optimism index broadly as expected at 98.2 (Bloomberg consensus 98.3) for a mild dip from 98.5 in September.

- “Optimism among small businesses declined slightly in October as owners report lower sales and reduced profits. Additionally, many firms are still navigating a labor shortage and want to hire but are having difficulty doing so, with labor quality being the top issue for Main Street.”

- As usual, our focus here is on the non-labor side of the survey with its jobs report already published, with particular attention on pricing plans which this month were a little softer than in September.

- A net 21% of firms raised their average selling prices compared to three months ago, back to a joint low since Aug 2024 having increased to 24% in September. This series has seen a recent high of 32% in February although it remains above the ~12% seen in immediate years ahead of the pandemic.

- A net 30% of firms plan to increase average selling prices over the next three months, down marginally from the 31% in September. It saw a recent high of 32% in June (down from the 50s in late 2021/early 2022 for comparison) but remains above the ~22% pre-pandemic average.

- Back to optimism more broadly, “The frequency of reports of positive profit trends fell 9 points from September to a net negative 25% (seasonally adjusted). This component contributed the greatest to the decline in the Optimism Index. Among owners reporting lower profits, 33% blamed weaker sales, 16% cited the rise in the cost of materials, 9% cited price change for their product(s) or service(s), and 9% cited labor costs.”