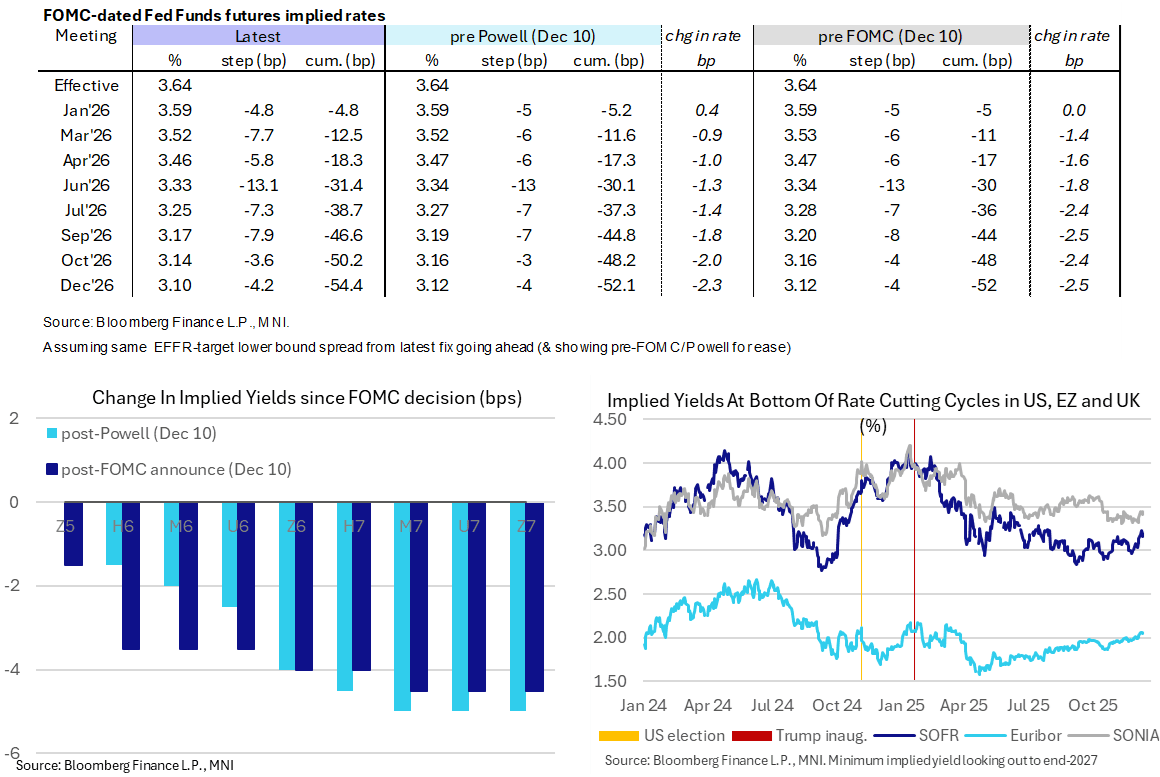

STIR: Holding Impact From A Not So Hawkish 25bp Cut

Dec-11 11:31

- Fed Funds implied rates are little changed overnight for 1H26 meetings and up to 1bp higher for 2H26 as they broadly consolidate the modest dovish reaction to yesterday’s 25bp cut communication leaning less hawkish than expected (MNI Review, link).

- Cumulative cuts from assumed 3.64% effective: 5bp Jan, 12.5bp Mar, 18.5bp Apr, 31bp Jun, 46.5bp Sep and 54bp Dec.

- SOFR futures are flat to +0.04 in most 2027 contracts, helping the terminal implied yield of 3.165% (Z6 and H7) pull back further from Tuesday’s 3.225% at what was the highest close since July. It's still more than 15bp higher than in late November after NY Fed's Williams had set up this week's cut.

- Today’s macro focus is on weekly jobless claims after initial claims slid in what was likely a distortion from difficulties in adjusting around Thanksgiving, whilst we also see catch-up for international trade and wholesale trade for September.

- The FOMC blackout remains in place today, as is customary, with tomorrow’s schedule set to start with three of those of who objected to Wednesday’s cut. Goolsbee dissented in favor of a hold and ’26 voters Paulson and Hammack were likely within the 6 “soft dissent” dots. Hammack was also likely one of the 3 dots who would have preferred to have kept rates on hold at previous levels through 2026 as well.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

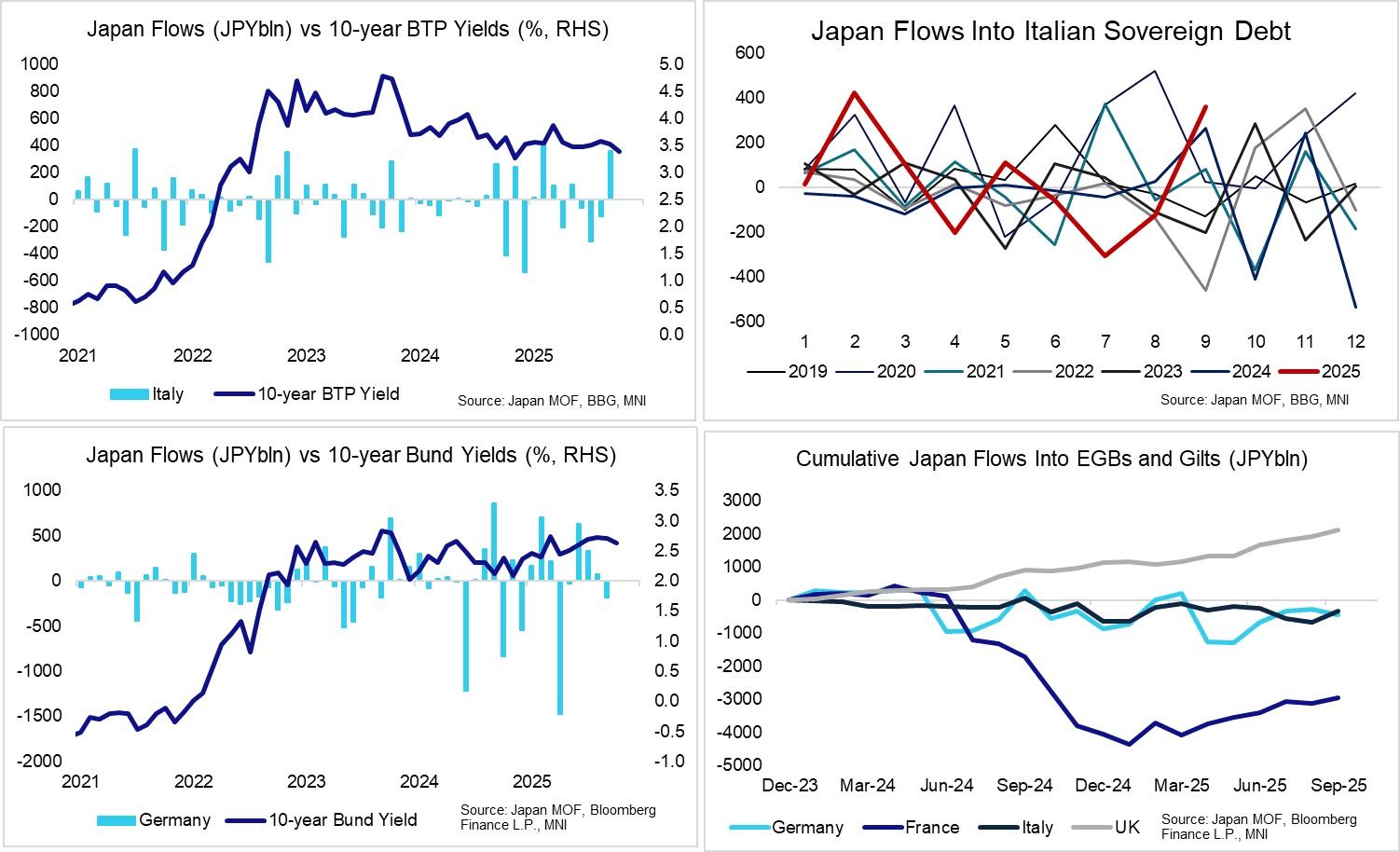

BONDS: Japanese Investors Were Large Net Buyers Of Italian Debt In September

Nov-11 11:28

Japanese investors net bought JPY361bln of Italian debt in September, according to domestic balance of payments data released overnight. This was the third largest single month net inflow since the start of 2021, after JPY423bln in February ’25 and JPY375bln in July ’21.

- After being subject to modest widening pressure in late-August/early-September, the 10-year BTP/Bund spread has resumed this year’s narrowing trend. BTP outperformance has been supported by relatively political stability in Italy versus the likes of France, improved domestic fiscal metrics and lower EUR rates vol. This combination of factors looks to have tempted Japanese investors back into BTPs in September, after a few months of net outflows in late Q2/early Q3.

- Japanese investors net bought JPY188bln of French debt in September, despite ongoing political uncertainty through the month amid the resignation of ex-PM Bayrou. It will be interesting to see aggregate net flows in October, with new PM Lecornu's budget negotiations dominating headline flow.

- There were JPY180bln of net sales in German bonds in September, while Gilts saw familiar net inflows.

- Meanwhile, Japanese investors net purchased JPY1,126bln of US Treasuries, bringing the year-to-date net inflow to JPY6,451bln.

- Our Asia-Pac team highlighted overnight that the larger-than-expected Japanese current account surplus was a combination of both the trade balance component and a surge in the primary income balance.

SOFR OPTIONS: BLOCK/Screen: Feb'25 SOFR Call Condor

Nov-11 11:23

- Total 4,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 0.75 at 0612:07ET

US 10YR FUTURE TECHS: (Z5) Bear Threat Remains Present

Nov-11 11:21

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02 High Nov 5& 7 and a key near-term resistance

- PRICE: 112-21+ @ 11:10 GMT Nov 11

- SUP 1: 112-09+ Low Nov 5

- SUP 2: 112-08+ 38.2% retracement of May - Oct Upleg

- SUP 3: 112-08/06 100-dma / Low Sep 25 and a reversal trigger

- SUP 4: 112-02 Trendline support drawn from the May 22 low

A short-term bear theme in Treasuries remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02. The trendline is drawn from the May 22 low. Resistance to watch is 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal.