MNI US MARKETS ANALYSIS - Sectors in Focus as NFP Seen Slowing

Highlights:

- Industries in focus for May payrolls, with markets expecting job gains to slow to +126k

- Treasuries sit a touch firmer, dragging USD to top end of the G10 table

- Trade headlines remain in focus following Merz' trip to Washington, shrugging off fallout from Musk/Trump break-up

US TSYS: A Touch Firmer With Thin Volumes Ahead Of Payrolls

- Treasuries are a little off yesterday’s lows seen after a Trump-Xi call and hawkish ECB press conference, with thin volumes ahead of today’s nonfarm payrolls report.

- MNI Preview found here.

- Fed Vice Chair for Supervision Bowman is the only FOMC member scheduled to appear today ahead of the media blackout starting 0001ET tomorrow.

- Cash yields are between 0.9-1.4bp lower on the day, with 2Y yields at 3.91% in the middle of the week's range.

- Curves consolidate yesterday’s flattening, with 2s10s at 47.3bp and 5s30s at 89.3bps having cleared 100bp early on Monday.

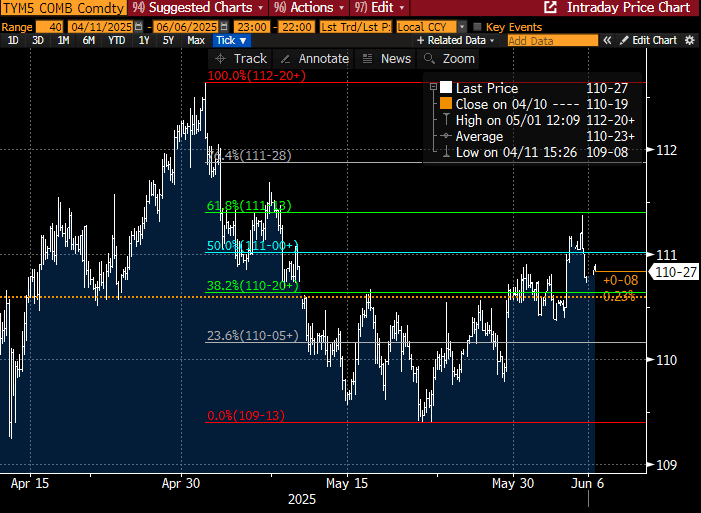

- TYU5 trades at 110-27 (+01+) having tentatively lifted off yesterday’s late low of 110-23+, with very low cumulative volumes of 205k.

- A bull cycle remains in play. Yesterday’s high of 111-14+ met resistance at 61.8% of the May 1-22 downleg, after which lies 111-19+ (1.0% 10-dma envelope), whilst support is seen at a key 110-11 (Jun 3 low).

- Data: Nonfarm payrolls May (0830ET), Consumer credit Apr (1500ET)

- Fedspeak: VC Supervision Bowman (1000ET) – see STIR bullet

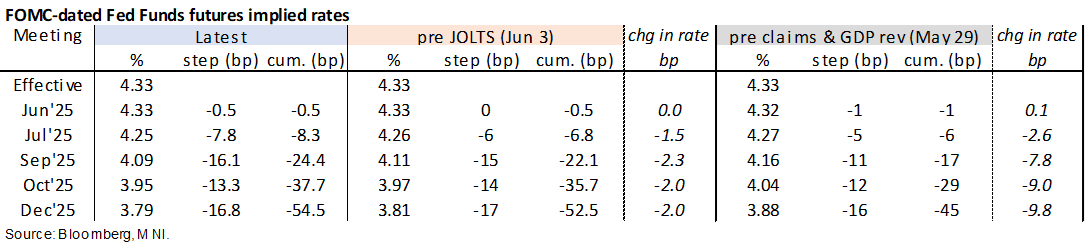

STIR: Next Fed Cut In September Priced Ahead Of Payrolls

- Fed Funds implied rates hold most of yesterday’s lift off the most dovish levels since May 12 following a Trump-Xi call.

- Focus is on the upcoming May nonfarm payrolls report at 0830ET. MNI Preview.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 9bp Jul, 24bp Sep, 38bp Oct and 54.5bp Dec.

- The SOFR implied yield of 3.28% is just -0.5bp lower on the day, back in its rough 100bp +/-5bp range of cuts mostly seen in recent weeks having dropped below it on Wednesday after weak ADP and ISM services data.

- Recently confirmed VC for Supervision, Bowman (voter) is the only Fed speaker set to appear after payrolls. She gives a speech on supervision and regulation at 1000ET and will be followed by Q&A. Having focused on financial stability for some time ahead of this week’s confirmation, we nevertheless watch the Q&A for any monetary policy implications from one of the most hawkish FOMC members.

STIR: Mix Of Short Setting & Long Cover As SOFR Futures Ticked Lower Thursday

OI data points to net long cover dominating through the greens as most SOFR futures ticked lower on Thursday. Some pockets of net short setting were seen in that area of the curve.

- Note the particularly modest OI swings in the very front end of the strip.

- Net short setting then moved to the fore in the blues.

| 05-Jun-25 | 04-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,069,487 | 1,069,372 | +115 | Whites | -15,758 |

SFRM5 | 1,407,171 | 1,407,973 | -802 | Reds | -10,605 |

SFRU5 | 1,129,921 | 1,130,000 | -79 | Greens | -1,280 |

SFRZ5 | 1,103,316 | 1,118,308 | -14,992 | Blues | +7,776 |

SFRH6 | 805,850 | 818,348 | -12,498 |

|

|

SFRM6 | 793,531 | 784,507 | +9,024 |

|

|

SFRU6 | 726,496 | 719,832 | +6,664 |

|

|

SFRZ6 | 850,716 | 864,511 | -13,795 |

|

|

SFRH7 | 681,005 | 685,122 | -4,117 |

|

|

SFRM7 | 592,542 | 593,616 | -1,074 |

|

|

SFRU7 | 414,504 | 416,322 | -1,818 |

|

|

SFRZ7 | 415,660 | 409,931 | +5,729 |

|

|

SFRH8 | 293,564 | 293,138 | +426 |

|

|

SFRM8 | 220,211 | 213,357 | +6,854 |

|

|

SFRU8 | 164,931 | 162,490 | +2,441 |

|

|

SFRZ8 | 170,961 | 172,906 | -1,945 |

|

|

JGBS: Futures Quickly Pare Uptick That Followed Latest BoJ Purchase Plan Report

JGB futures add just under 20 ticks to fresh overnight session highs of 139.64 after BBG sources report that the “BoJ is said to consider a smaller reduction in its bond buying”, before fading back towards pre-headline levels (~139.50 last).

- The BBG report suggests that the range of bond purchase reductions under consideration lies between JPY200-400bln per quarter, with a focus on JPY200bln.

- This is in line with general assumptions based on the current reduction pace (Y400bln) and official communique on dealer suggestions (JPY200bln)/prior source reporting.

- The lack of new information in the story helps explain the limited reaction in JGB futures and quick paring of the rally. USD/JPY reacts similarly, with spot pressuring the top-end of the daily range, but stopping short of any significant breakout.

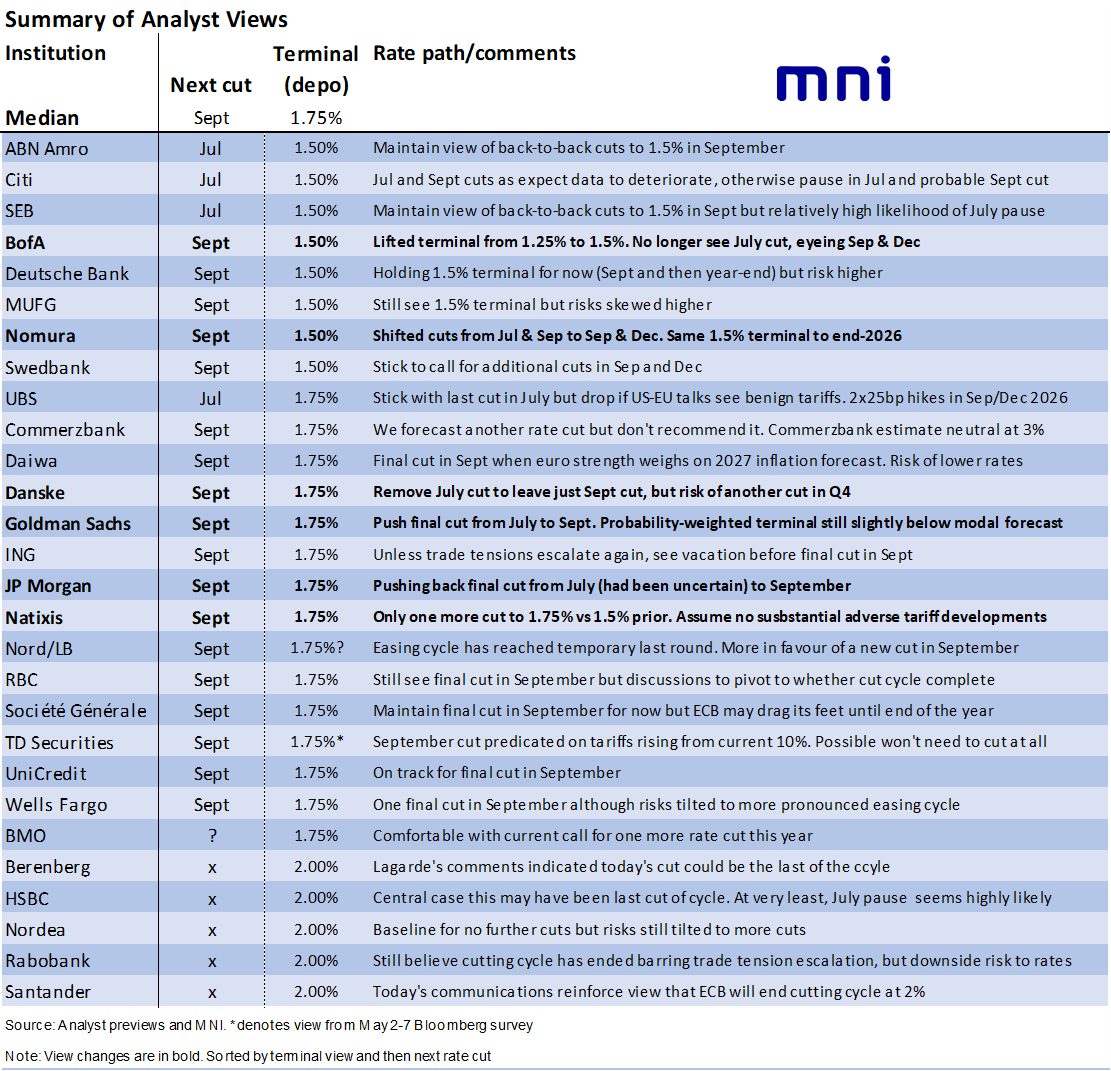

ECB VIEW: Summary Of Analyst Views Post-ECB Decision

- Yesterday’s hawkish ECB press conference from President Lagarde has seen 6 view changes across the 28 analysts reviewed below.

- Three lifted their terminal rate calls whilst the other three tweaked the timing of the next cut.

- The median analyst continues to eye a terminal rate of 1.75%, on balance seen coming with the September meeting.

- ECB-dated OIS currently prices 3.5bp of cuts for July and a cumulative 16bp for Sept and 26bp for year-end.

ITALY: Referendums Likely To Fail On Low Turnout

Voters go to the polls on Sunday, 8 and Monday, 9 June to vote in five 'abrogative' referendums. PM Giorgia Meloni's coalition gov't opposes the measures, and they are unlikely to pass. Their unexpected success would come as a blow to the government's prestige, but would not cause any lasting damage to the coalition's stability.

- As EurActiv reports, "Four of the five questions focus on labour law, ranging from reinstating unfairly dismissed workers and removing compensation caps in small firms, to curbing fixed-term contract abuse and restoring joint liability for workplace injuries. The fifth and most prominent referendum proposes reducing the residency requirement for non-EU citizens applying for Italian citizenship from 10 to five years."

- The gov't has largely avoided discussing the referenda, and this is an intentional move on its part. Rather than campaigning against the measures, the governing parties have instead advocated for boycotting the vote and not engaged in the debate.

- Under the Italian Constitution, popular referendums can take place to repeal or 'abrogate' existing laws. In order to get to the stage of a nationwide vote, a measure requires the backing of five Regional Councils or 500,000 Italian voters. In order to pass a simple majority is required. However, turnout must be at least 50% of all eligible voters or the measure fails.

- As such, Meloni's national conservative Brothers of Italy, Deputy PM Matteo Salvini's right-wing populist Lega, and Foreign Minister Antonio Tajani's centre-right Forza Italia all advocating a boycott is likely, alongside already widespread voter apathy on the issues, to see turnout fall well below the 50% mark.

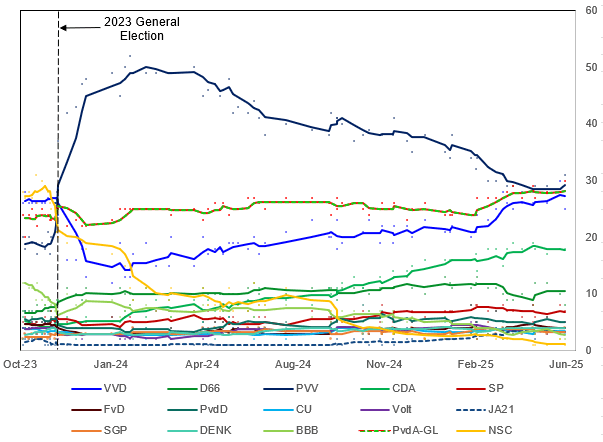

NETHERLANDS: Legislative Election To Be Set For 29 October

Interior Minister Judith Uitermark has confirmed that snap legislative elections will be set for 29 October, in line with recommendations from the electoral council. This follows the collapse of the governing coalition earlier this week, sparked by the withdrawal of Geert Wilders' right-wing nationalist Party for Freedom (PVV). Wilders claims that he withdrew his party due to the other coalition members' refusal to accept his 10-point plan for asylum reform, claims denied by the other parties.

- The election is too far away to make any concrete predictions, and indeed the plethora of parties means the political landscape will only become clear well after the 29 Oct vote as coalition negotiations take place.

- One of the main forces set to contest the election is the centre-left environmentalist GL-PvdA, an alliance between the GroenLinks (GreenLeft) and Labour (PvdA) parties, but it remains to be seen in what format. Members of both parties are currently voting on whether to formally merge or remain as an electoral alliance, with the result to be announced before a members' congress on 12 June. The merger is expected to pass, but there remains some unease.

- On the left of GL, there are concerns that joining with Labour will mean losing their 'radical' edge, while on the moderate wing of the PvdA some have argued joining with the environmentalists will turn off centrist voters and limit the party's prospects.

Chart 1. Legislative Election Opinion Polling, Projected Seats and 4-Poll Moving Average

Source: Peil.nl, Verian, Ipsos I&O, MNI

USDJPY Resilience Stands Out, 142.00/50 Support Gains Significance [1/2]

- Despite the Bloomberg dollar index falling 0.5% this week amid the prevailing trend that has been playing out across currency markets in 2025, USDJPY has been displaying relative resilience.

- Weaker-than-expected US ISM data in the lead up to today’s US employment figures have prompted multiple attempts back below 143.00, however, the firmer JOLTS data and the underlying bid for major US equity indices appear to be providing notable support. This could point to USDJPY being one of the better candidates to benefit from a robust set of US employment data later today.

- This has helped keep the key 142.12 level intact, the May 27 low, of which a clear break is needed to confirm a resumption of the bear leg. Better-than-expected data would enhance the significance of the cluster of recent lows, and signal scope for a more protracted recovery.

- Furthermore, while moving average studies have remained in a bear-mode position, they have continued to be tested in recent weeks. A close above the 50-day EMA, intersecting at 145.15, would bolster a bullish threat, while key short-term resistance has been defined at 146.28, the May 29 high.

USD: NZD and MXN Strong Candidates to Benefit From Soft Payrolls [2/2]

- Conversely, the resilience for equity benchmarks amid the cautious optimism surrounding US/China negotiations has been benefiting the likes of AUD and NZD, while the Mexican peso closed at its best level since September yesterday. Even the escalation of the Trump/Musk conflict and the associated nosedive for the Tesla share price had very little effect, and could signal that topside momentum could gather pace should the US employment figures disappoint.

- For AUDUSD, yesterday’s close above 0.6500 was the highest in 6 months, keeping trend signals bullish. The pair recently cleared a key short-term resistance at 0.6515, the May 7 high, confirming a resumption of the uptrend and signals scope for an initial climb to 0.6550, a Fibonacci retracement and the Nov 25 high. It is worth noting that US election related highs remain a medium-term target at 0.6688.

- The 1.1% rise this week for NZDUSD has seen the pair return to an important zone of resistance between 0.6025/40. Spot continues to threaten a daily close above the US election related highs, signalling scope for a more protracted recovery towards 0.6168, the 76.4% retracement of the Sep ’24 – Apr ’25 selloff.

- USDMXN has narrowed the gap to the September/October lows between 19.06-11, as bearish conditions have dominated following the significant range breakout in April. This comes despite the pessimism surrounding the Mexican growth trajectory and the heightened dovish profile of the central bank. Further USDMXN weakness would place attention on the Aug ’24 lows at 18.60.

FOREX: USD Off Lows, Shrugs Off Political Tumult

- After a tumultuous Thursday close, the greenback is recovering off lows, firming against all others in G10 ahead of the May jobs report. This has helped drag EUR/USD further off the post-ECB high at 1.1495, but losses at present are not sufficient to counter the underlying uptrend as defined by the 50-dma, which today highs 1.1259 - the highest since Q1 2022.

- Meanwhile, the recovery in equities overnight (e-mini S&P is higher by 0.4% at pixel time) is working further against the JPY, which keeps USD/JPY north of Y144.00 and EUR/JPY on track for a test of mid-May highs at Y165.21. The shape of the JGB yield curve remains a key driver here, with markets increasingly of the view that the finance ministry will tweak bond sale plans as soon as next month in order to compensate for stretched longer-end of the curve, and take advantage of the greater relative demand for shorter-dated securities.

- The recovering USD and stronger EUR post-ECB is putting GBP/USD on the backfoot. Moves look corrective at these levels, particularly as markets looked through the over-estimation of April UK CPI and the more dovish overtones from BoE Deputy Governor Breeden earlier in the week. As such, the technical picture remains bullish GBP/USD. Thursday’s climb resulted in a fresh cycle high, confirming a resumption of the uptrend and an extension of the price sequence of higher highs and higher lows.

- Markets expect job gains of 126k over the month and the industry breakdown will be watched for any weakness in trade & transportation after a strong April - likely on rapid inventory builds on tariff front-running - plus broader implications for discretionary demand. We expect greater sensitivity to a soft print in the event of a large surprise, although longer-term reaction would likely be capped by the FOMC not wanting a repeat of September’s (with hindsight) overreaction to a sharp but short-lived uplift in the u/e rate.

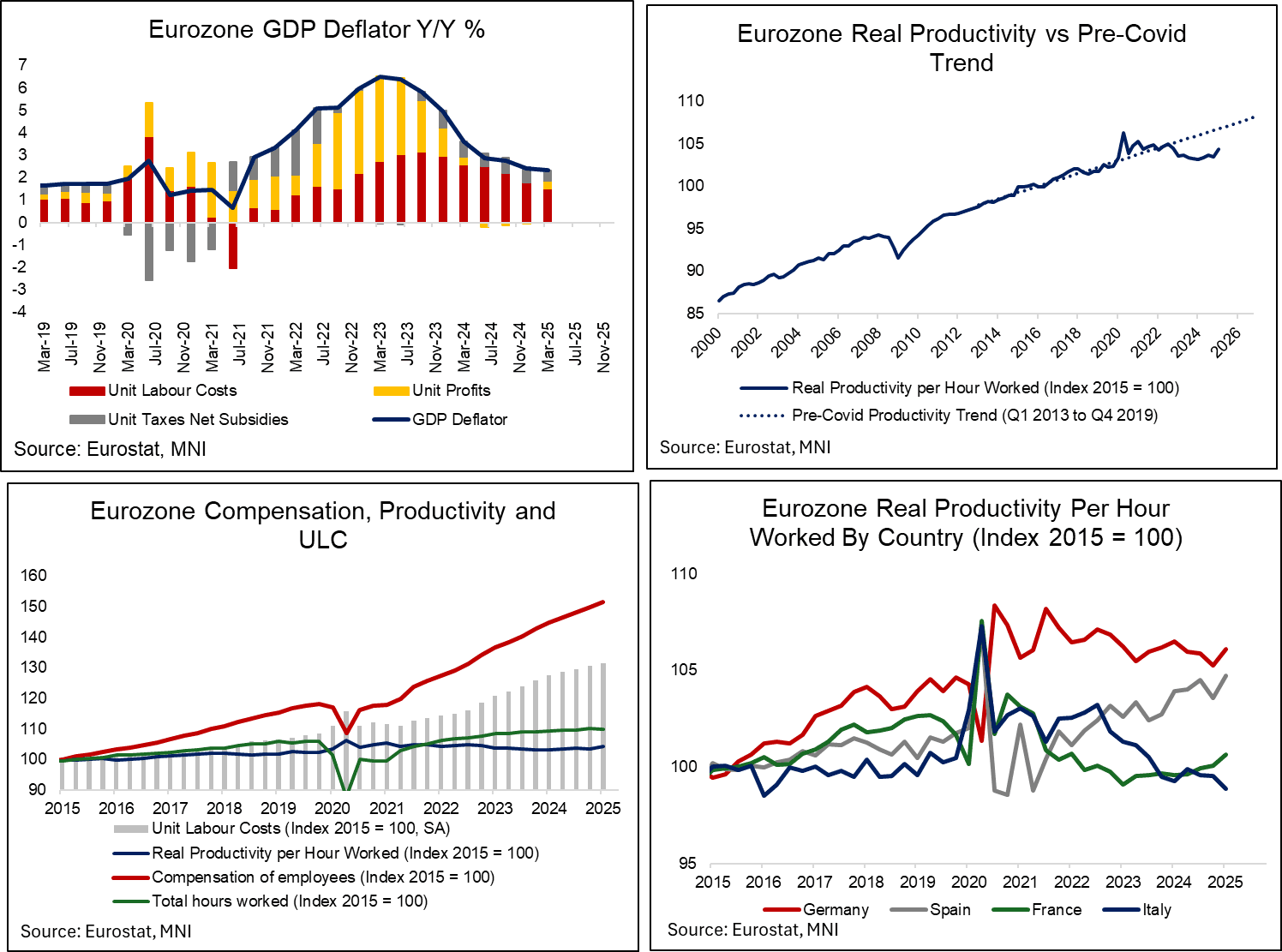

EUROZONE DATA: Moderating Unit Labour Costs Drive Further Deflator Easing In Q1

Eurozone GDP deflator growth eased a tenth to 2.3% in Q1, down from 2.4% in Q4 and a cycle high of 6.5% in Q1 2023. A moderation in unit labour costs continued to drive the deceleration, though unit profits provided some offset with the first positive Y/Y reading in a year. This was below the ECB’s 2.5% projection, seemingly a function of lower unit taxes growth than expected.

- In its June projections, the ECB noted that “overall domestic price pressures, as measured by the growth of the GDP deflator, are projected to continue decreasing in 2025 and to level off in the second half of the projection horizon, as declining unit labour costs allow profit margins to increase”.

- In Q1, unit labour costs rose 0.6% Q/Q (vs 0.8% prior) and 3.1% Y/Y (vs 3.7% prior, in line with the ECB’s projection), thus contributing 1.50pp to the annual GDP deflator rate. Compensation per employee growth softened to 3.8% Y/Y (vs 4.1% prior), but this was three tenths above the ECB’s projection. However, productivity per employee growth of 0.8% was four tenths higher than expected. The ECB writes that "growth in unit labour costs is projected to decline further over the projection horizon, on account of falling wage growth and increasing productivity growth."

- Worth noting that Eurozone-wide productivity was artificially skewed higher by increased tariff front-loading in countries such as Ireland and, to a lesser extent, Germany. Since employment growth (0.7% Y/Y) undershot real GDP growth of 1.2% Y/Y, productivity per employee by definition increased. Similar trends are seen on an hours-worked basis. At a country-level, Italian productivity growth stands out as weak.

- Unit profits fell 0.1% Q/Q (vs +0.8% prior) but rose 0.9% Y/Y (vs -0.1% prior), contributing 0.37pp to deflator growth. The ECB projected unit profit growth of 0.4% Y/Y in June, and noted that "as growth in unit labour costs moderates and other input cost dynamics remain contained, unit profit growth is expected to recover somewhat from 2025, aided by the economic recovery, strengthening productivity growth and a temporary accounting boost in 2027 related to the statistical treatment of ETS2".

- Taxes net of subsidies contributed the remaining 0.46pp, with annual growth of 4.3% Y/Y below the ECB’s 6.0% projection.

OPTIONS: Expiries for Jun06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E1.0bln), $1.1350(E656mln), $1.1400(E1.bln), $1.1450(E847mln), $1.1500(E1.4bln), $1.1550(E500mln)

- USD/JPY: Y142.00($1.6bln), Y142.50-60($744mln), Y142.90-05($684mln), Y143.50-65($584mln)

- EUR/GBP: Gbp0.8420-30(E510mln)

- GBP/USD: $1.3410(Gbp897mln)

- AUD/USD: $0.6300(A$1.5bln)

- USD/CAD: C$1.3600($626mln), C$1.3660($500mln), C$1.3745-60($1.1bln), C$1.4035-40($1.2bln), C$1.4180-85($1.6bln)

EQUITIES: Fresh Cycle Highs Bolster Bullish E-Mini S&P Trend Conditions

- The trend cycle in Eurostoxx 50 futures remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5274.35, the 50-day EMA. A clear break of this average would signal a possible reversal.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high yesterday. The recent break of 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5780.89, the 50-day EMA.

COMMODITIES: WTI Futures Still Close to Recent Highs But Bear Threat Present

- WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.56, the 50-day EMA. It has been pierced, however, a clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger.

- A bullish theme in Gold remains intact. Medium-term trend signals are bullish - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low. First support lies at 3313.2, the May 5 low.

| Date | GMT/Local | Impact | Country | Event |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit | |

| 07/06/2025 | 0730/0930 | ECB's Lagarde Speech In Monaco | ||

| 07/06/2025 | 0940/1140 | ECB's Schnabel in Dubrovnik panel discussion | ||

| 07/06/2025 | 0940/1040 | BOE Greene On Central Bank Decoupling Panel |