MNI US MARKETS ANALYSIS - PPI to Add to Tariff Impact Views

Highlights:

- PPI, industrial production to add extra layer to tariff impact views

- Heavy session for Fedspeak keeps focus on White House - Fed relationship

- GBP stabilises on higher UK CPI, but August BoE cut is still the base case

US TSYS: Broadly Consolidating Yesterday’s CPI-Induced Breach Of TYA Support

- Treasuries trade modestly twist flatter on the day although broadly speaking consolidate yesterday’s sell-off on the June CPI report with its signs of increased tariff passthrough.

- Treasuries outperform Gilts across the curve owing to stronger than expected UK CPI, whilst they underperform EGBs at the front end but track in line further out the curve.

- Cash yields are 0.7bp higher (2s) to 1.8bp lower (30s).

- The 10Y yield, currently at 4.473%, saw an overnight high of 4.493%, having last cleared 4.50% on Jun 11.

- TYU5 trades at 110-11+ (+ 02+) on solid cumulative volumes of 375k, albeit keeping to narrowing ranges of 110-08+ to 110-13+.

- It consolidates yesterday’s push lower to that 110-08+, seen multiple times since then, in a move that breached an important support at 110-17 (61.8% of May 22 – Jul 1 bull leg). It has also traded through trendline support at 110-23+, strengthening a bearish theme and opening 110-03 (76.4% retrace of the same bull leg).

- Data: MBA mortgage applications (0700ET), PPI Jun (0830ET), NY Fed services Jul (0830ET), IP/Cap util Jun (0915ET)

- Fedspeak: Barkin repeats speech (0830ET, text + Q&A), Hammack on community development (0915ET, text only), Gov. Barr on financial regulation (1000ET, text + Q&A), Beige Book (1400ET), Bostic on fox business network (1530ET), NY Fed's Williams on economic outlook and policy (1830ET, text + Q&A).

- Bill issuance: US Tsy to sell $65bn 17-W bills (1130ET)

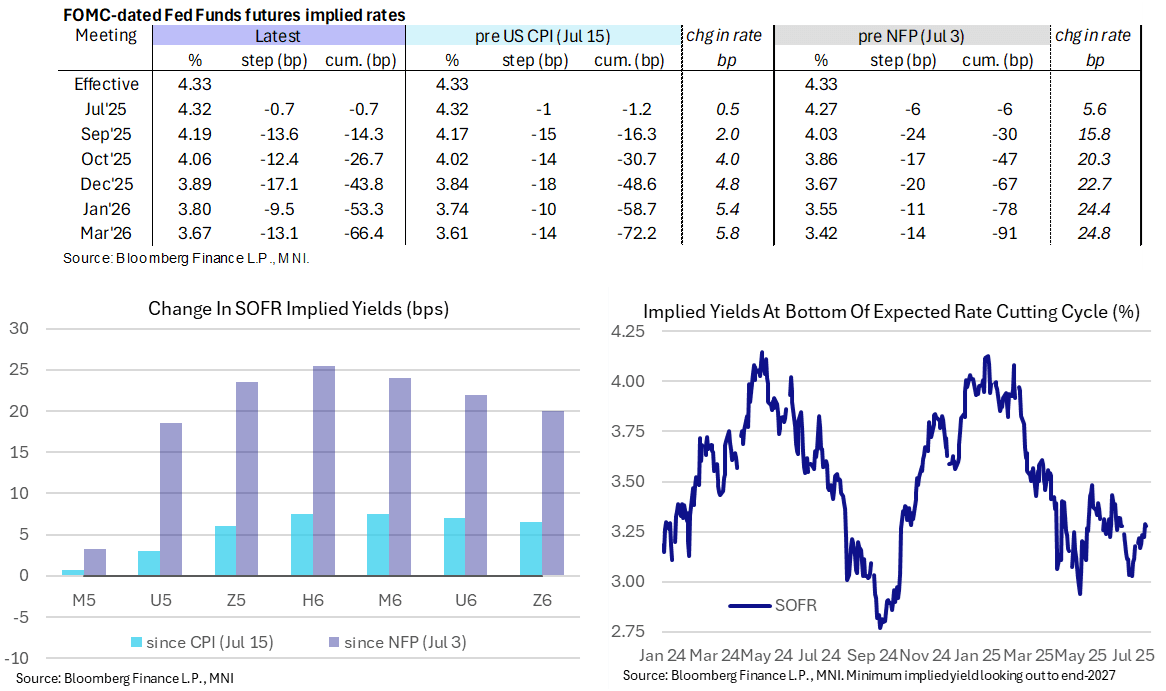

STIR: Less Than 60% Odds Of Sept FOMC Cut, PPI Eyed Before Fedspeak

- Fed Funds implied rates consolidate yesterday’s belated shift higher on signs of increased tariff passthrough in the June CPI report.

- Cumulative cuts from 4.33% effective: 0.5bp Jul, 14.5bp Sep, 26.5bp Oct, 44bp Dec, 53.5bp Jan and 66.5bp Mar. The 44bp of cuts through to year end compares with 67bp prior to payrolls less than two weeks ago.

- The SOFR implied terminal yield of 3.28% (SFRZ6) is 1bp lower on the day after its highest close since Jun 16.

- A typically hawkish Logan (’26 voter) said late yesterday that the base case calls for continued restrictive policy having been disappointed before after streaks of low inflation. She doesn’t think the tariff impact will be clear until at least the fall although it’s also possible a softer labor market could require cuts soon.

- Today’s macro focus is likely on the June PPI report – both the core PCE readthrough and broader input costs – along with further Fedspeak before the Beige Book (1400ET as usual) offers another useful update on regional Fed network monitoring.

- Aside from the Beige Book, NY Fed Williams (voter) at 1830ET is likely the pick for Fedspeak, talking on the economic outlook and policy with both prepared text and Q&A. It could be an important update from a senior Fed official who last spoke Jun 24, saying it’s appropriate to maintain the current policy stance whilst there are signs that inflation is affecting some categories of goods. He viewed the economy as remaining in a good place.

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen Tuesday

OI data points to a modest bias towards net short setting on Tuesday, as contracts sold off in the wake of the CPI data.

- The biggest net positioning swing came via short setting in TY futures, although the presence of net long cover across most of the rest of the curve (modest net short setting in TU futures being the exception) made for little net change in exposure in curve-wide DV01 terms.

| 15-Jul-25 | 14-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,356,744 | 4,353,213 | +3,531 | +132,941 |

FV | 7,025,845 | 7,037,494 | -11,649 | -498,349 |

TY | 4,890,176 | 4,843,970 | +46,206 | +3,021,244 |

UXY | 2,418,186 | 2,431,955 | -13,769 | -1,187,182 |

US | 1,796,835 | 1,798,339 | -1,504 | -204,002 |

WN | 1,961,786 | 1,966,204 | -4,418 | -789,050 |

|

| Total | +18,397 | +475,601 |

SOFR: Short Setting In The Greens Dominated On Tuesday

OI data points to meaningful net short setting in the SOFR greens on Tuesday (in net pack terms), as the market reacted to CPI data and signals that tariff increases were feeding into some core goods prices.

- A mix of more modest net long cover and short setting was seen across the remainder of the strip.

| 15-Jul-25 | 14-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,290,717 | 1,294,312 | -3,595 | Whites | -4,461 |

SFRU5 | 1,222,960 | 1,237,931 | -14,971 | Reds | +19,963 |

SFRZ5 | 1,291,654 | 1,291,473 | +181 | Greens | +101,520 |

SFRH6 | 1,001,973 | 988,049 | +13,924 | Blues | -16,711 |

SFRM6 | 868,458 | 864,627 | +3,831 |

|

|

SFRU6 | 817,110 | 811,448 | +5,662 |

|

|

SFRZ6 | 918,681 | 899,455 | +19,226 |

|

|

SFRH7 | 723,440 | 732,196 | -8,756 |

|

|

SFRM7 | 691,223 | 666,728 | +24,495 |

|

|

SFRU7 | 526,890 | 475,401 | +51,489 |

|

|

SFRZ7 | 446,185 | 419,083 | +27,102 |

|

|

SFRH8 | 310,500 | 312,066 | -1,566 |

|

|

SFRM8 | 228,677 | 240,025 | -11,348 |

|

|

SFRU8 | 201,739 | 202,622 | -883 |

|

|

SFRZ8 | 202,286 | 206,879 | -4,593 |

|

|

SFRH9 | 138,353 | 138,240 | +113 |

|

|

EUROPE ISSUANCE UPDATE:

30-year Bund Results:

- E1bln (E800mln allotted) of the 1.25% Aug-48 Bund. Avg yield 3.13% (bid-to-offer 3.69x; bid-to-cover 4.60x).

- E1.5bln (E1.129bln allotted) of the 2.90% Aug-56 Bund. Avg yield 3.22% (bid-to-offer 1.05x; bid-to-cover 1.40x).

Gilt Tender results:

- GBP1.5bln of the 4.50% Sep-34 Gilt. Avg yield 4.547% (bid-to-cover 3.32x, tail 0.4bp).

EQUITIES: Bank of America Macro Takeaways:

- "2Q NET INTEREST INCOME FTE $14.82B, EST. $14.84B - bbg

- 2Q NET INTEREST INCOME $14.67B, EST. $14.59B

- 2Q LOANS $1.15T, EST. $1.12T

- 2Q NET CHARGE-OFFS $1.53B, EST. $1.5B

- 2Q TRADING REVENUE EX. DVA $5.38B, EST. $4.94B"

- Markets: Record Q2 sales and trading revs, record Q2 equities sales and trading revs

- Consumer side: YTD consumer payment spend is up 4% Y/Y at $2.3tr

- Sectoral spending, they see increases in both volumes and transactions for travel & entertainment, food, retail and services (T&E, Services rising the fastest) however spending on gas declined by 6% in $ terms, on flat transaction numbers.

- Residential mortgage loans rose for the first time in 5 quarters, up to $118bln from $115bln in the prior quarter. Credit card and vehicle lending was broadly flat

EQUITIES: Big Banks Still Dominating Earnings Schedule; MS, BofA & GS All Due

Awaiting results from Bank of America in around 10 minutes times - continuing the theme of big bank earnings that should dominate this week. Highlights today include:

- 1145BST/0645ET: Bank of America

- 1230BST/0730ET: Morgan Stanley, Goldman Sachs

- Pre-Market: Prologis, Progressive Corp

- After-Market: United Airlines

Our full schedule including timings, EPS and revenue estimates here: Hidden PDF

SCANDIS: Weakness Through July Partly A Function Of Broader Dollar Correction

Scandi currencies are once again underperforming the G10, with EURNOK and EURSEK each up 0.3% on the session. This morning’s NOK weakness may be a function of the latest pullback in Brent crude futures, but it’s also worth viewing recent moves in the context of the broader USD rebound.

- As highlighted on several occasions this week, the DXY found support from the long-term trendline drawn from the 2011 low at the start of July. Yesterday’s US CPI data, which provided the first real signs of tariffs filtering through to consumer prices, helped the DXY pull further away from this support.

- NOK and SEK outperformed the G10 basket through Q1 and much of Q2, with early tariff fears contributing to a broader diversification away from US assets. NOK is seen as fairly insulated from tariffs given its low manufacturing share and commodity-heavy export mix. Meanwhile, SEK has benefitted from a repatriation/reallocation of fund flows into domestic equities alongside spillovers from increased German/European defence spending-related optimism.

- The corrective behaviour in the YTD dollar downtrend (alongside the resilience of US equities in the face of ongoing tariff/fiscal uncertainty) over the past few weeks has prompted a partial unwind of key FX themes from earlier this year. We have also previously highlighted a fading SEK-positive flow from Swedish Equity Investment fund data as of June.

- Monetary policy outlooks may also be playing a role. EURSEK has fully reversed the hawkish reaction to the July flash inflation data, suggesting FX markets do not consider the print a serious impediment to future Riksbank easing. Meanwhile, after surprising with a 25bp cut in June, expectations are now for Norges Bank to continue easing at a steady quarterly pace.

- EURNOK has pierced the July 2 high at 11.9156, narrowing the gap to the psychological 12.0000, which has provided soft resistance on several occasions since 2023. Meanwhile, EURSEK is just shy of 11.3203, the 76.4% retracement of the Feb – April selloff.

FOREX: Greenback Consolidating Tuesday Advance, GBP Contained Post CPI

- G10 currency ranges have been very contained early Wednesday, allowing the US dollar to consolidate the prior day’s broad-based advance following the release of US inflation figures. The recent USD index recovery has now extended to around 2.3% from cycle lows printed on July 01. The rally marks the cleanest evidence yet of a material break of the downtrend posted off the February high, bolstered by a clean break above the 20-day EMA.

- USDJPY moderately extended its significant upswing overnight, printing at the highest level since April 03 at 149.18. Bullish momentum was underpinned by the rising US yields and breaks above the June and May highs likely exacerbated the move. The May high around 148.65 has provided support this morning, keeping a short-term bullish theme prominent.

- the next focus will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- Despite headline and core CPI in the UK surprising to the upside, we think the BOE will largely describe inflation in the August MPR as broadly in line with their forecast. This explains the very limited reaction for GBP this morning, as markets assess the upcoming labour market data on Thursday and bearish technical developments for the pound.

- GBPUSD breached important trendline support below 1.3430 yesterday, drawn from the Jan 13 low. A clear break of the trendline strengthens a bearish threat and exposes 1.3335, the May 20 low.

- The data focus later today will be on US PPI, industrial production and the Fed’s beige book. There are also various FOMC speakers expected.

EQUITIES: Futures Extend Tuesday Weakness

- S&P E-Minis are trading in a range, closer to their recent highs. The trend condition remains bullish. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend.2

- A bull cycle in Eurostoxx 50 futures remains in play and the latest pullback still appears corrective. Recent gains have exposed key resistance and the bull trigger at 5486.00, the May 20 high.

COMMODITIES: Gold Finds Support at 50-dma

- A bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to the bulk of its recent gains. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend.

- WTI futures maintain a bearish tone. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower and this suggests that recent gains have been corrective.

| Date | GMT/Local | Impact | Country | Event |

| 16/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 16/07/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/07/2025 | 1230/0830 | *** | PPI | |

| 16/07/2025 | 1230/0830 | *** | PPI | |

| 16/07/2025 | 1315/0915 | *** | Industrial Production | |

| 16/07/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 16/07/2025 | 1400/1000 | Fed Governor Michael Barr | ||

| 16/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 16/07/2025 | 1800/1400 | Fed Beige Book | ||

| 16/07/2025 | 2230/1830 | New York Fed's John Williams | ||

| 17/07/2025 | 0130/1130 | *** | Labor Force Survey | |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller |