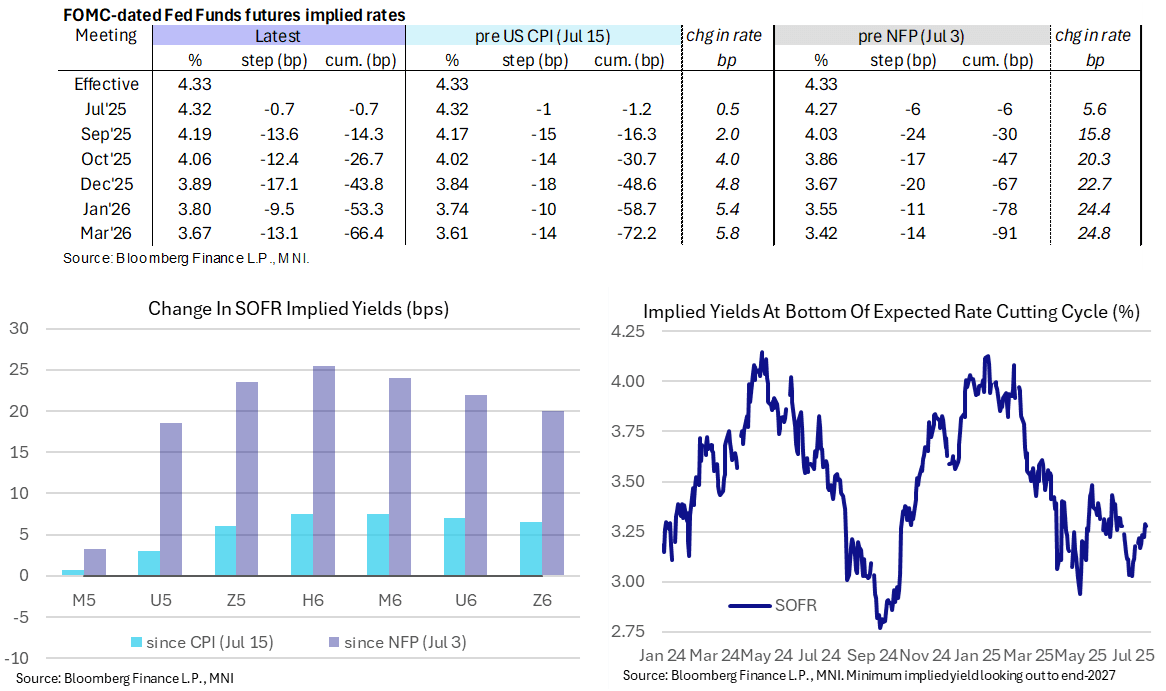

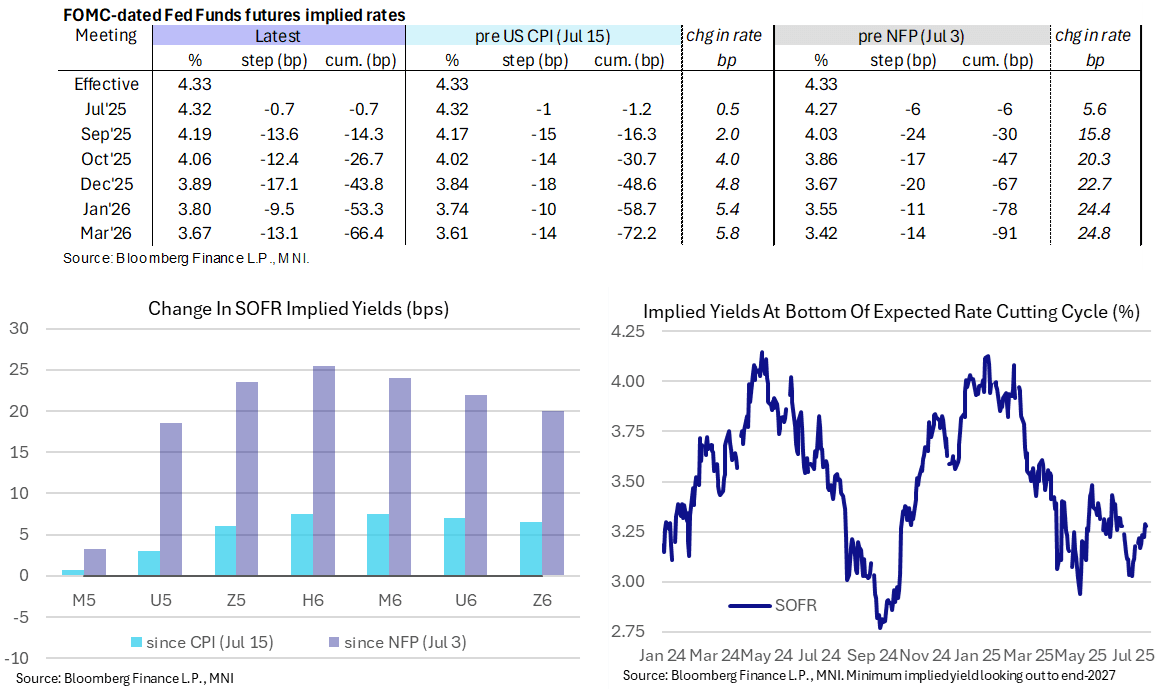

STIR: Less Than 60% Odds Of Sept FOMC Cut, PPI Eyed Before Fedspeak

Jul-16 10:35

- Fed Funds implied rates consolidate yesterday’s belated shift higher on signs of increased tariff passthrough in the June CPI report.

- Cumulative cuts from 4.33% effective: 0.5bp Jul, 14.5bp Sep, 26.5bp Oct, 44bp Dec, 53.5bp Jan and 66.5bp Mar. The 44bp of cuts through to year end compares with 67bp prior to payrolls less than two weeks ago.

- The SOFR implied terminal yield of 3.28% (SFRZ6) is 1bp lower on the day after its highest close since Jun 16.

- A typically hawkish Logan (’26 voter) said late yesterday that the base case calls for continued restrictive policy having been disappointed before after streaks of low inflation. She doesn’t think the tariff impact will be clear until at least the fall although it’s also possible a softer labor market could require cuts soon.

- Today’s macro focus is likely on the June PPI report – both the core PCE readthrough and broader input costs – along with further Fedspeak before the Beige Book (1400ET as usual) offers another useful update on regional Fed network monitoring.

- Aside from the Beige Book, NY Fed Williams (voter) at 1830ET is likely the pick for Fedspeak, talking on the economic outlook and policy with both prepared text and Q&A. It could be an important update from a senior Fed official who last spoke Jun 24, saying it’s appropriate to maintain the current policy stance whilst there are signs that inflation is affecting some categories of goods. He viewed the economy as remaining in a good place.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

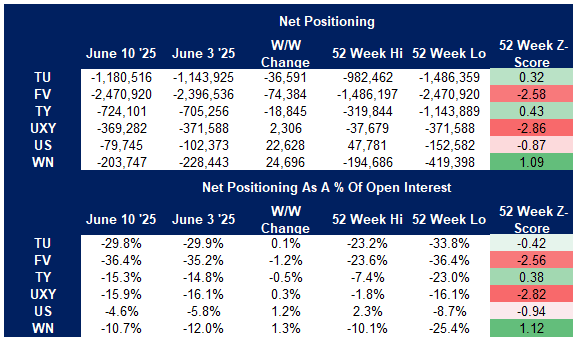

US TSY FUTURES: CFTC Shows A Managers & Leveraged Funds Trimming Net Exposure

Jun-16 10:34

The latest CFTC CoT report revealed cover of prevailing curve-wide positions amongst asset managers and leveraged funds in the week ending Tuesday June 10.

- Asset managers added to net longs in TU, UXY and WN futures, while trimming net longs in FV, TY & US futures. The cohort trimmed its curve-wide net long by ~$1.0mln DV01 but remains net long in all contracts.

- Leveraged funds covered some of their net short in TY, US & WN futures, while they extended net shorts in TU, FV & UXY contracts. The cohort trimmed its curve-wide net short by ~$4.2mln DV01 but remains net short in all contracts.

- The non-commercial cohort added to net shorts in TU, FV & TY futures, while they trimmed net shorts in UXY, US & WN futures. The cohort remains net short across the curve (more detail for that cohort available in the table below).

- Note that the cut off date means that initial reaction to the CPI data was captured, although PPI & UoM reaction was not.

- The data doesn’t capture the Israel-Iran developments later in the week.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

LOOK AHEAD: Monday Data Calendar: Empire Mfg, 20Y Bond Auction Re-Open

Jun-16 10:32

- US Data/Speaker Calendar (prior, estimate)

- 16-Jun 0830 Empire Manufacturing (-9.2, -6.3)

- 16-Jun 1130 US Tsy $76B 13W & $68B 26W bill auctions

- 16-Jun 1300 US Tsy $13B 20Y Bond auction re-open (912810UL0)

- Source: Bloomberg Finance L.P. / MNI

OUTLOOK: Price Signal Summary - USDJPY Bear Threat Remains Present

Jun-16 10:31

- In FX, a bullish EURUSD theme remains intact and the pair continues to trade closer to its recent highs. Last Thursday’s rally resulted in a breach of key resistance at 1.1573, the Apr 21 high. This strengthens the bullish theme and confirms a resumption of this year's uptrend. Sights are on 1.1696 next, a 1.618 projection of the Feb 28 - Mar 18 - 27 price swing. Initial firm support is at 1.1404, the 20-day EMA. The 50-day EMA lies at 1.1267. Short-term weakness is considered corrective.

- The trend condition in GBPUSD remains bullish and price is trading closer to its recent highs. A rising price sequence of higher highs and higher lows, together with a bull set-up in moving average studies, highlights a dominant uptrend. Sights are on 1.3681 next, the 1.500 projection of the Feb 28 - Apr 3 - 7 price swing. Support to watch lies at 1.3456, the Jun 10 low.

- USDJPY is trading in a range and remains below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend remains bearish - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend. A resumption of weakness would open 142.12, the May 27 low. Key short-term resistance is 146.28, the May 29 high. First resistance is 145.46, Jun 11 high.

Trending Top

Jun-26 16:22