MNI US MARKETS ANALYSIS - NATO Looks to Iron Out 5% Details

Highlights:

- NATO meeting begins in earnest, looks to iron out details of 5% spending deal

- Powell faces lawmakers for a second day after striking neutral tone yesterday

- TWD rallies to new highs on strong foreign equity buying

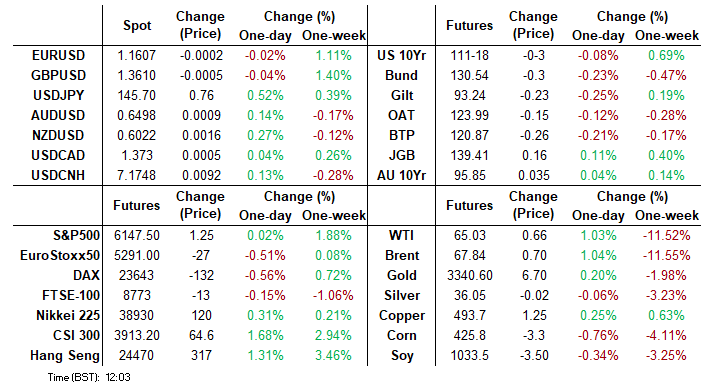

US TSYS: Mildly Lower; NATO Headlines, 5Y Supply And Housing Data Ahead

- Treasuries are inching lower as US desks filter in but are little changed on the day awaiting fresh drivers, having faded an earlier modest rally that came about with limited headlines.

- President Trump has disputed a Pentagon assessment that US airstrikes only had a limited impact by delaying the Iranian nuclear program by months.

- Trump is in the Netherlands today for a pared back NATO summit.

- Cash yields are 0.5-1bp higher on the day.

- 2s10s is mechanically steeper at 50.5bp (+3.2bp) after the new 2Y entered the benchmark after yesterday’s 2Y auction.

- 5s30s are little changed at 97.5bp (+0.3bp) having tested recent highs with 100.4bp yesterday.

- TYU5 deals at 111-18 (- 03) on modest cumulative volumes at 285k. An overnight high of 111-24 extended recent gains seen after Monday’s clearance of 111-14+.

- Resistance is eyed at 111-30 (76.4% of May 1-22 downleg) and 111-31+ (1.0% 10-dma envelope).

- Data: MBA mortgage applications (1200ET), New home sales May (1000ET), Building permits May revisions (tbd)

- Fedspeak: Goolsbee on podcast (0800ET), Powell testifies before Senate Committee (1000ET, text + Q&A)

- Coupon issuance: US Tsy $28B 2Y FRN Note re-open (1130ET), US Tsy $70B 5Y Note - 91282CNK3 (1300ET).

- Last month’s 5Y suction was strong, with a 0.4bp trade through (its sixth trade through in the past seven auctions) and record high indirect take-up at 78.4%. Yesterday’s 2Y auction meanwhile saw a small stop (0.2bp) and a bid-to-cover at 2.58x for almost identical to the 2.57x prior.

- Bill issuance: US Tsy $63B 17W bill auction (1130ET)

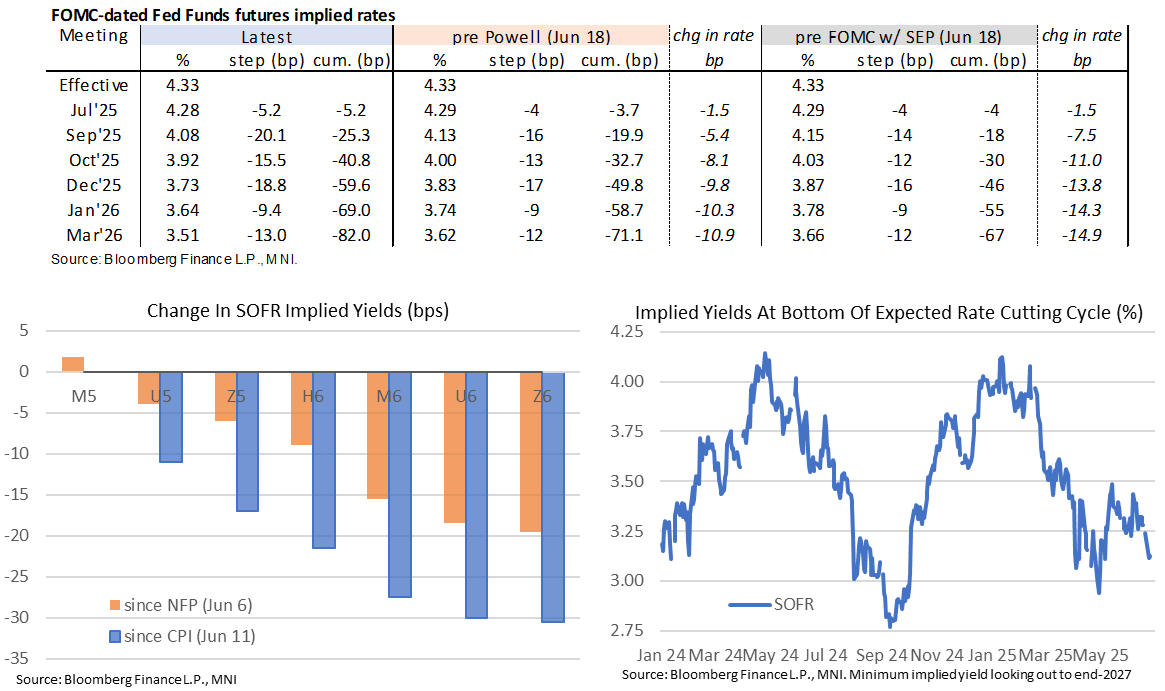

STIR: 20% Odds of Fed Cutting Next Month, Day Two Of Powell Testimony

- Fed Funds implied rates have softened a little further for the next two meetings but are broadly unchanged on the day for end-2025.

- Cumulative cuts from 4.33% effective: 5bp Jul, 25.5bp Sep, 41bp Oct, 60bp Dec, 69bp Jan and 82bp Mar.

- SOFR implied yields are up to 1.5bp higher on the day looking out to end-2027 contracts.

- The implied terminal yield of 3.125% (SFRZ6, -1bp) holds the week’s slide for closer to 5 rather than 4 cuts ahead, helped by a slide in oil prices and a surprisingly dovish Bowman on Monday (even if a variety of other FOMC members appear more patient).

- Today’s Fedspeak is unlikely to be as interesting as yesterday:

- 1000ET - Powell’s second day of Congressional testimonies, this time in front of the Senate committee. It follows yesterday’s House appearance where he noted many rate paths are possible although with somewhat selective headlines giving a dovish skew. As with last week’s FOMC presser, he implied that the September FOMC is the next ‘live’ meeting.

- 0800ET – Chicago Fed’s Goolsbee (’25 voter, dove) appears on a podcast. He’s already spoken this week, saying on Monday that the tariff impact hasn’t been as feared on inflation and that the Fed can cut rates if tariff inflation doesn't come. "Now we're trying to figure out is this all there is or is there about to be something showing up in the inflation data."

SOFR: Long Setting Most Dominant In Futures On Tuesday

OI data points to a mix of net long setting and short cover through most SOFR futures on Tuesday, with the former dominating in pack terms through the reds.

- The only exception to the wider theme came via modest net short setting in SFRM5.

| 24-Jun-25 | 23-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,297,037 | 1,293,133 | +3,904 | Whites | +12,281 |

SFRU5 | 1,138,586 | 1,146,262 | -7,676 | Reds | +39,217 |

SFRZ5 | 1,266,894 | 1,274,706 | -7,812 | Greens | +4,238 |

SFRH6 | 1,007,592 | 983,727 | +23,865 | Blues | +9,372 |

SFRM6 | 857,715 | 842,788 | +14,927 |

|

|

SFRU6 | 811,812 | 805,505 | +6,307 |

|

|

SFRZ6 | 927,790 | 917,288 | +10,502 |

|

|

SFRH7 | 696,763 | 689,282 | +7,481 |

|

|

SFRM7 | 632,989 | 633,197 | -208 |

|

|

SFRU7 | 448,421 | 443,572 | +4,849 |

|

|

SFRZ7 | 409,593 | 411,025 | -1,432 |

|

|

SFRH8 | 298,532 | 297,503 | +1,029 |

|

|

SFRM8 | 230,861 | 230,638 | +223 |

|

|

SFRU8 | 197,792 | 193,828 | +3,964 |

|

|

SFRZ8 | 176,490 | 172,310 | +4,180 |

|

|

SFRH9 | 140,844 | 139,839 | +1,005 |

|

|

US TSY FUTURES: Long Setting Dominated Again On Tuesday

OI data points to a second consecutive day of meaningful net long setting in curve-wide terms on Tuesday.

- Only WN futures bucked the wider trend, with modest net short cover seen there.

- TY futures accounted for roughly half of the ~$8.7mn DV01 of net longs added across the curve.

| 24-Jun-25 | 23-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,157,742 | 4,128,006 | +29,736 | +1,155,931 |

FV | 7,071,747 | 7,028,282 | +43,465 | +1,897,118 |

TY | 4,915,715 | 4,850,417 | +65,298 | +4,353,740 |

UXY | 2,377,445 | 2,375,560 | +1,885 | +166,033 |

US | 1,765,594 | 1,753,562 | +12,032 | +1,682,763 |

WN | 1,881,507 | 1,884,756 | -3,249 | -591,865 |

|

| Total | +149,167 | +8,663,720 |

IRAN: IAEA's Grossi-Inspectors' Return To Nuclear Sites "No. 1 Priority"

Reuters reports comments from International Atomic Energy Agency (IAEA) Director General Rafael Grossi in the aftermath of the US strikes on Iran and the Israel-Iran ceasefire. Says that IAEA inspectors' return to Iranian facilities is the "number one priority" at present. Grossi says that Iran informed him that they had taken "protective measures" with regard to its enriched uranium stock. On the nature of any inspections, Grossi says, "There is rubble, there could be unexploded ordnance, these are not normal inspections."

- Regarding reports that the Iranian nuclear programme is only set back a few months, Grossi says "I don't like this hourglass approach, it's in the eye of the beholder...In any case, the technological knowledge is there, the industrial capacity is there, that no-one can deny...Not important whether its two months or three months, we need a solution that will stand the test of time...There's a chance for a diplomatic solution, an opening, we shouldn't miss that opportunity."

- Says that "The non-proliferation treaty has served us well. Hard words are inevitable at times of war but we are working for diplomacy."

Grossi's comments come after the Iranian Parliament approved the country's suspension of its co-operation with the IAEA in a unanimous 221-0 vote earlier today. The legislation needs the sign-off from the 12-member Guardian Council, but this will prove a formality.

- As such, despite Grossi's comments, it remains to be seen whether the IAEA will be able to re-start its inspections at Iran's nuclear sites any time soon.

UK: i Paper-Gov't Considers Pulling Welfare Reform Bill Amid Growing Rebellion

The i Newspaper reports that PM Sir Keir Starmer could pull a controversial piece of legislation intended to save the gov't GBP5bln/year by 2030 by cutting a disability benefit, the Personal Independence Payment (PIP). This comes in the face of a growing rebellion among MPs from Starmer's centre-left Labour party, with over 120 putting their names to a 'reasoned amendment' that, if passed, would scupper the gov'ts reform plans.

- The gov't could look to continue with the reforms (as Starmer said he would earlier this morning). This would either need the number of rebels to decrease substantially, or rely on support from the main opposition centre-right Conservatives. The former seems unlikely given the groundswell of opinion among Labour backbenchers. Conservative leader Kemi Badenoch announced on 24 June that her MPs would back the legislation (enough to overcome the Labour rebels), before posting criticism of the potential withdrawal on X.

- The option of pulling the legislation (to be announced by the Leader of the Commons, Lucy Powell, on the morning of 26 June), would see it pushed back until the new parliamentary session in the autumn, when it would be reintroduced with rebels' views taken into account.

- Labour continues to trail the populist Reform UK in opinion polling, with Nigel Farage's party outflanking Starmer on the right on issues such as immigration, but on the left on welfare, leaving the gov't in a difficult position in terms of policy making.

EUROPE ISSUANCE UPDATE:

UK auction results

- Disappointing auction with the LAP (lowest accepted price) lower than the intraday low at the time of the auction. This is reflected in the wide 1.0bp tail seen at the auction.

- Price of the 4.375% Jan-40 gilt fell from around 95.11 (after the gilt had moved a bit higher post-bidding window close) to hit a low of 94.960.

- Gilt futures also hit on the auction and challenging the intraday lo of 93.34 seen around the time of the open at writing.

- GBP3.25bln of the 4.375% Jan-40 Gilt. Avg yield 4.850% (bid-to-cover 2.88x, tail 1bp).

Italy auction results

- E3bln of the 2.10% Aug-27 BTP Short Term. Avg yield 2.12% (bid-to-cover 1.49x).

- E3bln of the 1.10% Aug-31 BTPei. Avg yield 1.21% (bid-to-cover 1.46x).

FOREX: USD/JPY Bounces, But S/T Tech Drivers Still Point Lower

- Australian monthly CPI came in lower-than-expected, which could call into question the RBA's next inflation outlook round, however the currency is again firmer off lows and holding the bulk of the recovery off Monday's 0.6373. This price actions favours this week's weakness as a false break below the bottom-end of the multi-month trend channel, and a reversion higher here would make 0.6552, the June 16 high and bull trigger, the primary upside target.

- USD/CHF remains within range of cycle lows after the solid outperformance posted from the beginning of the week. Having initially benefited from haven flows on the exchange of fire between Israel and Iran, the CHF has held the rally, keeping 0.8035 in sight as the next downside level in USD/CHF.

- Meanwhile, USD/JPY is recouping a small part of the sharp losses posted off the 148.03 high, putting prices back above Y145.50 in what's likely a corrective rally off the pullback lows. This week's price action has formed a shooting star candle pattern - which argues in favour of further S/T losses in the pair. The 50-dma marks the next downside level at 144.25, but we see the 20-day EMA at 144.81 as more materially important in the short-term. The level has been pierced, but a clear break of it would strengthen a bearish threat.

- May new home sales data is the sole US release Wednesday. This should keep focus on the second appearance from Fed's Powell this week, this time in front of the Senate Finance Committee. He struck a balanced tone on policy yesterday, however a mention from the Fed chair that rate cuts could come faster on "lower inflation, weaker labor" still elicited interest from markets, despite the Fed chair again implying September is the next 'Live' meeting.

- The ongoing NATO meeting in the Netherlands will be carefully watched for cohesion around Trump's latest narrative that the US has secured firmer military commitments from Europe, despite remaining signs of dissention among countries including Spain. The US President remains in NATO sessions until 1040ET, at which time he is scheduled to return to the White House.

FOREX: Month-end Models Coalesce Around Moderate USD Sales for June

- Barclays project moderate month-end USD selling against most majors, with a weaker sign for EUR/USD. Their quarter-end model, however, indicates strong USD sales, with a weak sign for EUR/USD, and a moderate sign for USD/JPY.

- Citi see moderate USD sales this month, however the signal is weaker in GBP/USD due to outperformance in UK equities & bonds this month

TWD: FX Inflows Remain Key Driver, Could Heighten Importance of Dividends

- With the USD Index resuming the multi-month downtrend on the Iran-Israel ceasefire, USD/TWD has broken through to new pullback lows, with spot closing at 29.380, the lowest since June 2022. TWD strength is also playing a major part, with upside pressure stemming from increased foreign investor participation. Exchange data shows foreign investors were net buyers of $1.2bln Taiwanese stocks Wednesday, making for net purchases of ~$1.7bln this week alone.

- This comes despite the Taiwanese authorities looking to pressure speculators by dissuading foreign investors from using tools such as ETFs to garner larger long TWD positions. This week's price action, however, may provide a sign that this messaging is not yet working.

- The rally in TWD spot is also being felt in the front-end of the implied curve: 1-month USD/TWD vols were bid through 11 points today, meeting the levels seen in early May and the initial life insurer-driven spot rally and breakout in volatility.

- On foreign investor participation ahead, HSBC write that the peak of the local dividend season is forthcoming, and that may slow the pace of TWD appreciation ahead. The concentrated distribution of dividends through July & August has tended to increase FX outflow pressures in recent years - and they estimate 2025's season to be more concentrated to July (they see $8.3bln in payments to foreign investors this year, largely via TSMC, Hon Hai and MediaTek - all of which are in July).

OPTIONS: Solid Options Demand as Markets Reach for EUR Upside

- Yesterday's FX options volumes cleared $120bln - the busiest day for derivatives since June 12th and the second busiest since early May. Activity was led by a busier EUR/USD market, however EM FX was also in focus with much higher-than-usual activity across BRL, KRW and MXN.

- Given the post-ceasefire rally in EUR/USD spot, no surprise to see EUR calls dominating ($3 in EUR calls have traded for every $2 in puts so far this week). We note sizeable interest in $1.1700 calls, which see cumulative notional of over $4bln so far this week - a level spot hasn't traded above since 2021. Vol hedges have been a dominant theme so far Wednesday, with sizeable 1.1670 straddles (expiring late September) and 1.1430/1.1790 strangles (expiring early July) among the highlights.

- Where does this leave vol? The front end of the G10 FX vol curve remains under pressure. Implied vols across JPY, EUR, GBP, CHF and others are in the lower-end of the recent range, and through the bottom of the lower quartile in some instances. As a result, NZD and AUD are the G10 currencies maintaining a positive realised/implied vol ratio - and only just. This may signal a base in implied, which are holding despite the slide in realised volatility - as the expiry of the pause in Trump's Liberation Day tariffs on July 8th looms as the next potential driver of uncertainty.

OPTIONS: Expiries for Jun25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1395-00(E1.1bln), $1.1495-00(E4.0bln), $1.1600-10(E995mln)

- USD/JPY: Y143.98-00($1.0bln), Y144.50($1.6bln), Y145.00-10($1.1bln), Y146.00-20($1.3bln), Y148.00($1.0bln)

- GBP/USD: $1.3400(Gbp642mln)

- NZD/USD: $0.6265(N$757mln)

EQUITIES: Recovery in Eurostoxx 50 Futures Appears to Signal Potential Reversal

- A short-term bear cycle in Eurostoxx 50 futures remains intact, however, the recovery from Monday’s low appears to be a potential reversal. The contract has traded above the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme and signal scope for a stronger recovery. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of Monday’s 5194.00 low would reinstate a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle high reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. Sights are on the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5922.67. A clear break of it would signal a reversal.

COMMODITIES: Bullish Theme in Gold Remains Intact

- WTI futures maintain a softer tone following the reversal from Monday’s high. Support to watch is at the 50-day EMA, at $64.50. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- A bullish theme in Gold remains intact and the latest pullback is considered corrective - for now. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has recently been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3287.7, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf | ||

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 25/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 25/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/06/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 25/06/2025 | 1800/1400 | Federal Reserve Board Meeting | ||

| 26/06/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 26/06/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 26/06/2025 | 0830/0930 | BOE Breeden On UK Competetiveness Panel | ||

| 26/06/2025 | 0945/1145 | ECB De Guindos At Deutsch Bank Forum 2025 | ||

| 26/06/2025 | 0945/1045 | BOE Greene Chairs Panel On MonPol Communication | ||

| 26/06/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 26/06/2025 | 1100/1300 | ECB Schnabel At 'Wirtschaftsrat der CDU' Finanzmarktklausur | ||

| 26/06/2025 | 1100/1200 | BOE Bailey Keynote Speech At BCC Conference | ||

| 26/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 26/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 26/06/2025 | 1230/0830 | * | Payroll employment | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1230/0830 | *** | GDP | |

| 26/06/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1245/0845 | Richmond Fed's Tom Barkin | ||

| 26/06/2025 | 1300/0900 | Cleveland Fed's Beth Hammack | ||

| 26/06/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 26/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 26/06/2025 | 1430/1530 | BOE Lombardelli Chairs Panel On Communicating Uncertainty | ||

| 26/06/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 26/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 26/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 26/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/06/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 26/06/2025 | 1715/1315 | Fed Governor Michael Barr | ||

| 26/06/2025 | 1830/2030 | ECB Lagarde Opening Speech at Münchner Opernfestspiele | ||

| 26/06/2025 | 1900/1500 | *** | Mexico Interest Rate |