MNI US MARKETS ANALYSIS - JPY Sinks Despite BoJ Rate Hike

Highlights:

- JPY sinks as BoJ rate hike fails to stimulate bets for further tightening

- Fed chair saga continues - Waller, Rieder, Warsh still in the running with Hassett

- Final UMich sentiment data the data highlight, with Fed's Williams also due to speak

US TSYS: Treasuries Follow EGBs Lower, Williams and QCEW Update Ahead

Treasuries have bear steepened overnight, being dragged lower by EGBs with the ECB and Germany’s 2026 issuance plans now in the rear view. Today’s local focus should be on potentially important comments from NY Fed’s Williams at 0830ET along with 1000ET data including the delayed QCEW update. President Trump also makes an announcement at 1300ET, with the topic unknown but it following the Trump-Kennedy Center renaming vote.

- Cash yields are 1.5-3.3bp higher on the day, led by the long end, with 2s10s at 67.6bps having more than reversed the ~2.5bp flattening seen on CPI yesterday.

- TYH6 trades at session lows of 112-16+ (-07+) on modest cumulative volumes of 240k.

- A bull cycle is intact for now, with resistance seen at 113-00+ (61.8% retrace of Nov 25-Dec 10 bear leg) having fleetingly hit 112-31 on yesterday’s CPI release. Support is seen at 112-06 (Dec 16 low) before 111-29 (Dec 10 low and bear trigger).

- Data: Existing home sales Nov (1000ET), U.Mich consumer survey Dec final (1000ET), QCEW Q2 (1000ET), Kansas City Fed services Dec (1100ET).

- Note that QCEW update can help guide expectations for the size of the potential payrolls benchmark revision due with the January payrolls report. The preliminary benchmark estimate, based off Q1 QCEW data, showed a tentative -911k that is likely to not be as negative come the full benchmark revision. Powell last week said he sees monthly payrolls growth being overstated by 60k (Waller has since suggested 50-60k) compared to the ~75k that is tentatively implied by the preliminary estimate.

- Fedspeak: Williams on CNBC (0830ET) – see STIR bullet

- Politics: Trump makes an announcement (1300ET), Trump participates in Christmas reception (1745ET)

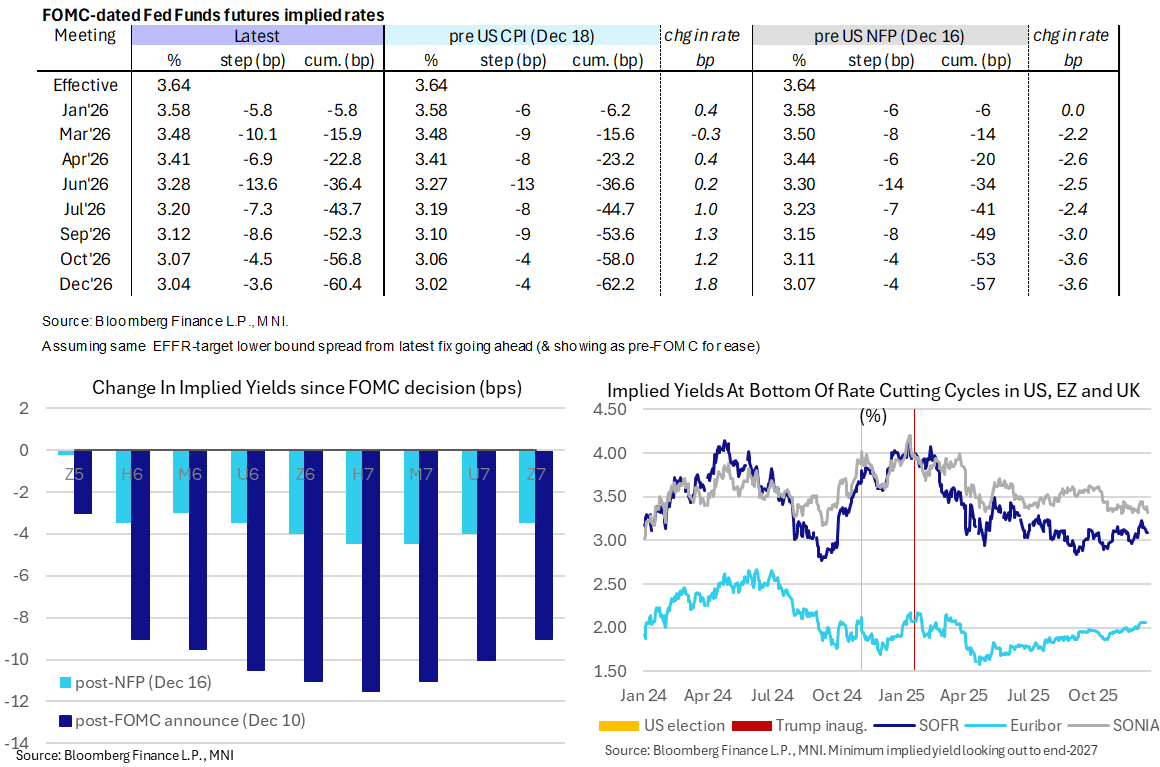

STIR: Similar Rate Path To Pre-CPI Levels, Williams Watched For Fed Reaction

- Fed Funds implied rates are 0.5-1bp higher overnight for meetings out to end-2026, leaving a rate path that is almost identical to pre-CPI levels for the next few meetings and then marginally higher in 2H26.

- Cumulative cuts from 3.64% effective: 6bp Jan, 16bp Mar, 23bp Apr, 36.5bp Jun, 52.5bp Sep and 60.5bp Dec.

- SOFR futures are up to 4 ticks lower in 2H27 contracts, with the terminal implied yield lifting to 3.09% (Z6, +2bp) as it remains within recent ranges seen over the past month.

- NY Fed Williams (voter) is set to speak on CNBC at 0830ET and could again have a sway on markets in giving an indication of how the FOMC might be thinking about yesterday’s extremely messy CPI report.

- There’s a general consensus that it will have to look through the large downside surprise due to being biased lower by technical distortions, so any comments of taking the data at face value would be notable.

- Note that speaking late yesterday, Chicago Fed’s Goolsbee (next voting ’27) didn’t sound too worried by potential distortions, saying there was a “lot to like” in the November report, adding that “I realize it’s just one month, and you never want to hinge too much on a single month, but that was a good month.” He did however add that he wants to see more economic data.

ECB VIEW: MS Delay Next Rate Cut Call, Still One Of Most Dovish Analysts

Morgan Stanley yesterday changed their ECB call and now expect a next rate cut in Jun 2026 vs March previously. They keep the terminal rate call at 1.5% but stronger data have increased the risk to their call. This leaves MS at the clear dovish end of analysts, with most expecting a 2% terminal rate and next moves generally viewed as hikes albeit some time away with the earliest we’ve seen being TD Securities looking for late 2026. We're still reviewing latest analyst views.

- “The new projections show stronger growth and higher inflation, more than we anticipated. Today's meeting, stronger data and stickier inflation have raised the bar for further easing.”

- “We now expect the first cut in June 2026 (instead of March), followed by another in September, contingent on weaker growth, faster inflation deceleration, and more euro appreciation.”

- “We maintain our view of a 1.5% terminal rate in 2026, but risks that the ECB will keep rates on hold for longer have clearly increased.”

- “With cuts basically not priced in, the market has little ability to reprice in the direction of “fewer cuts.” We continue to favour long positions at the short end of the curve and maintain Feb-Jun ECB flattening.”

US TSY FUTURES: Net Long Setting Dominated On Thursday

OI data points to net long setting dominating in Tsy futures as contracts settled higher on Thursday.

- The most meaningful net positioning swings came via net long setting in TU, FV & TY futures, while more modest net long setting was seen in US futures, along with small scale net short cover in UXY & WN contracts.

| 18-Dec-25 | 17-Dec-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,548,227 | 4,474,113 | +74,114 | +2,928,919 |

FV | 6,718,612 | 6,676,304 | +42,308 | +1,871,254 |

TY | 5,482,175 | 5,434,210 | +47,965 | +3,223,873 |

UXY | 2,513,958 | 2,516,267 | -2,309 | -209,066 |

US | 1,844,276 | 1,838,729 | +5,547 | +768,535 |

WN | 2,076,812 | 2,076,976 | -164 | -29,746 |

|

| Total | +167,461 | +8,553,768 |

SOFR: Mix Of Long Setting & Short Cover In Futures On Thursday

OI data points to net short cover in the SOFR white and green futures packs, while long setting was more prominent in the reds as the space reacted to the soft CPI data and central bank decisions in Europe on Thursday.

| 18-Dec-25 | 17-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,535,456 | 1,544,742 | -9,286 | Whites | -32,469 |

SFRH6 | 1,319,044 | 1,347,725 | -28,681 | Reds | +40,735 |

SFRM6 | 1,164,021 | 1,156,188 | +7,833 | Greens | -17,562 |

SFRU6 | 1,202,382 | 1,204,717 | -2,335 | Blues | +163 |

SFRZ6 | 1,145,941 | 1,129,570 | +16,371 |

|

|

SFRH7 | 869,724 | 853,766 | +15,958 |

|

|

SFRM7 | 765,553 | 762,411 | +3,142 |

|

|

SFRU7 | 815,731 | 810,467 | +5,264 |

|

|

SFRZ7 | 835,178 | 837,343 | -2,165 |

|

|

SFRH8 | 469,013 | 474,440 | -5,427 |

|

|

SFRM8 | 393,979 | 406,608 | -12,629 |

|

|

SFRU8 | 382,056 | 379,397 | +2,659 |

|

|

SFRZ8 | 326,093 | 329,908 | -3,815 |

|

|

SFRH9 | 207,196 | 203,886 | +3,310 |

|

|

SFRM9 | 209,705 | 211,603 | -1,898 |

|

|

SFRU9 | 176,907 | 174,341 | +2,566 |

|

|

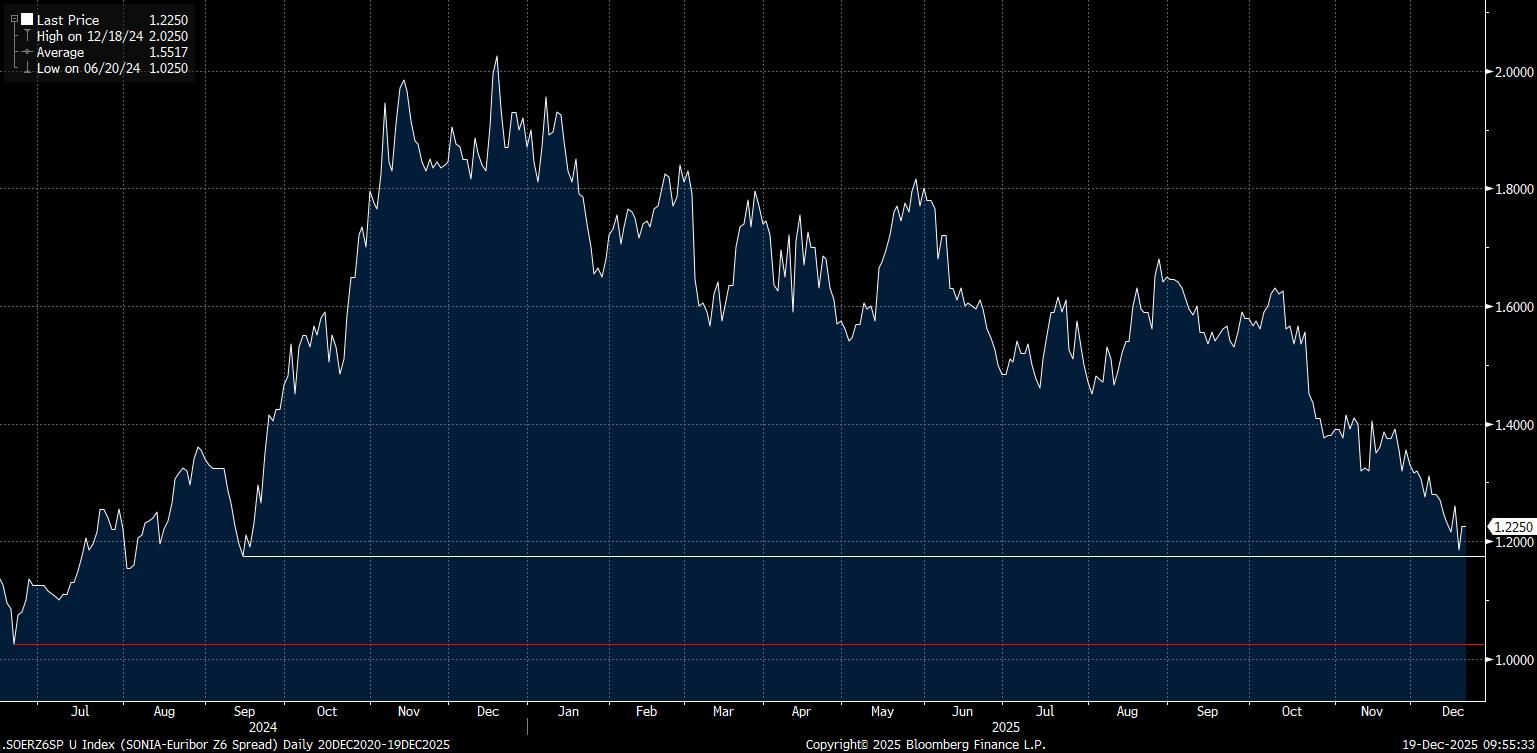

STIR: SONIA/Euribor Dec ’26 Spread Off Lows, Downside Risks Remain

Yesterday’s BoE decision pulled the SONIA/Euribor December ’26 spread off cycle lows after the combination of hawkish ECB repricing and soft UK CPI data drove the latest leg lower in recent sessions. Relative central bank outlooks may continue to drive fresh downside in the spread in the new year.

- Markets have taken the promotion of the language surrounding “closer call” decisions to the BoE’s statement as hawkish, although the ongoing easing bias in the communique alongside and since yesterday’s decision and slowing of UK CPI means that ~38.5bp of further is still priced into the GBP short end.

- This doesn’t seem particularly aggressive at this stage, with a full 25bp cut not fully discounted until the June MPC and inflation moving towards the Bank’s 2% target in a quicker than previously envisaged manner.

- Ongoing stickiness in UK wage growth presents a hawkish risk.

- Meanwhile, official ECB rhetoric continues to suggest that monetary policy settings are “in a good place”, stressing a meeting-by-meeting approach.

- The latest round of ECB source reports played down the odds of further easing, albeit with talks of rate hikes deemed premature (in the wake of the well-documented comments from Schnabel). While hikes still seem some way off, the bar to further ECB easing has definitely risen in recent weeks.

- Risks on this side of the spread come from the potential for slower-than-expected Eurozone growth (after an upgrade of the Bank’s projections) and lower-for-longer inflation (vs. ECB expectations).

- Support in the SONIA/Euribor December ’26 spread seen at the Sep 13 ’24 closing low (1.175%), which protects the June 20 ’24 closing low (1.025%).

Fig. 1: SONIA/Euribor Dec ’26 Spread

Source: MNI - Market News/Bloomberg Finance L.P.

FRANCE: Lecornu Will Have To Resort To Special Bill, OATs Widening A Little

With the Joint Committee unable to reach an agreement on the 2026 state budget (PLF) this morning, the French Government cannot pass its full budget before year-end. As such, the Government is expected to introduce a special bill to ensure the continuity of operations while budget negotiations restart/resume in the new year).

- The 10-year OAT/Bund spread has widened modestly (~0.9bps) since the news broke, now 0.5bps wider on the session at ~71bps. The 70bp figure continues to contain downside in the spread for now, and failure to pass a budget may keep this support intact into the start of next year.

- We have noted extensively in recent weeks that the prospect of getting the PLF passed was a much sterner test than the social security budget (PLFSS). As such, the failure of the Joint Committee to reach a compromise doesn’t come as a massive surprise.

- The special bill will allow the state to levy taxes and account for spending measures enacted in the previous budget (i.e. that which is 'already voted for').

- Although the special bill is essentially only choice facing Lecornu, Banque de France Governor Villeroy nonetheless said this morning that it “would lead us to a deficit significantly higher than what is desirable”, as it does not include “any savings measures ,”

FOREX: USDJPY Surges Through 157.00 On BoJ

- USDJPY is rallying well early Friday, rising over 1% to clear the 156.95 December 9 high as the lack of meaningful, hawkish guidance from BoJ Governor Ueda following the expected target rate hike weighs on JPY. The BoJ did signal it will continue raising rates in line with improvements in growth, wages and inflation, while maintaining accommodative conditions to support the economy - but this fell well short of any firmer commitment on tightening.

- Price action does strengthen bullish conditions in the pair, opening back up the 157.89 November 20 high and bull trigger. Above 158.00, the January 10 high and key resistance stands at 158.87. Speculative positioning may well prevail in terms of short-term drivers for spot as volumes remain high in recent trade.

- GBP meanwhile outperforms as markets digest yesterday's BoE meeting as well as follow-up comments from Governor Bailey this morning, in which he repeated that the Bank is getting nearer to the neutral rate. Despite this, GBPUSD is seeing only limited volatility as the JPY weakness spills over into USD markets. GBPUSD trades within range of resistance at the Dec 16 high of 1.3456 and support the Dec 17 low at 1.3312.

- NZDUSD pierces below its 20- and 50-day EMAs at 0.5748 as RBNZ hiking expectations have been pared to some extent this week. Some room for further adjustment remains, however.

- NY Fed's Williams is scheduled to appear on CNBC later. There are a host of Governing Council speakers scheduled today, where we don't expect meaningful departures from the ECB's central guidance, but will continue to monitor for nuances in view. Michigan inflation expectations and sentiment are on the data calendar.

OPTIONS: Expiries for Dec19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E3.0bln), $1.1600(E1.1bln), $1.1650(E1.2bln), $1.1675-80(E3.0bln), $1.1700-05(E2.0bln), $1.1750-60(E4.4bln), $1.1785-00(E4.8bln), $1.1850(E2.0bln), $1.1900(E2.0bln), $1.2000(E3.2bln)

- USD/JPY: Y153.00($2.8bln), Y154.00($1.4bln), Y155.00($2.2bln), Y156.00($1.4bln), Y157.00($1.3bln), Y158.00($1.9bln)

- GBP/USD: $1.3350-55(Gbp486mln)

- EUR/GBP: Gbp0.8800(E1.3bln), Gbp0.8825-30(E883mln), Gbp0.8850(E529mln), Gbp0.9000(E1.4bln)

- AUD/USD: $0.6600-05(A$943mln), $0.6625(A$551mln), $0.6650(A$842mln), $0.6675(A$1.3bln), $0.6700(A$1.6bln)

- AUD/NZD: N$1.1300(A$1.1bln)

- NZD/USD: $0.5630(N$594mln)

- USD/CAD: C$1.3800($940mln), C$1.3825($1.8bln), C$1.3900($1.7bln), C$1.3950($1.2bln), C$1.4000($1.5bln), C$1.4050($1.1bln), C$1.4200($1.6bln)

- USD/CNY: Cny7.2500($829mln), Cny7.3000($1.1bln)

EQUITIES: Eurostoxx 50 Futures Extend Recovery Off This Week's Low

- A bull cycle in Eurostoxx 50 futures remains intact and the latest pullback appears corrective. The first key support to watch lies at 5654.19, the 50-day EMA. A clear break of the average would highlight a potential short-term reversal. This would open 5594.00, the Nov 26 low. For bulls, a resumption of gains would refocus attention on key resistance at 5825.00, the Nov 13 high. Yesterday’s price pattern is a bullish engulfing candle - a reversal signal.

- A pullback in S&P E-Minis has resulted in a breach of both the 20- and 50-day EMAs. This strengthens a short-term bear threat and signals scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. Sights are on 6737.71, a Fibonacci retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls a resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

COMMODITIES: Gold Trend Structure Remains Unchanged and Bullish

- The trend condition in WTI futures remains bearish. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has been breached. Clearance of this level resumes the downtrend and opens $53.77, a Fibonacci projection. Key short-term resistance to watch is $61.25, the Oct 24 high. First resistance is at $58.83, the 50- day EMA.

- The trend structure in Gold is unchanged, it remains bullish. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4106.7. Clearance of this EMA would signal scope for a deeper retracement. Price is approaching key resistance and the bull trigger at $4381.5, the Oct 20 high. A break resumes the primary uptrend.

| Date | GMT/Local | Impact | Country | Event |

| 19/12/2025 | 1200/1300 | ECB Cipollone Remarks, Roundtable at Aspen Institute | ||

| 19/12/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 19/12/2025 | 1330/0830 | ** | Retail Trade | |

| 19/12/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 19/12/2025 | 1500/1000 | *** | NAR existing home sales | |

| 19/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 19/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 19/12/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 19/12/2025 | 1510/1610 | ECB Lane Lecture at Central Bank of Ireland | ||

| 19/12/2025 | 1630/1630 | BOE to announce APF Q4 Sales Schedule | ||

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |