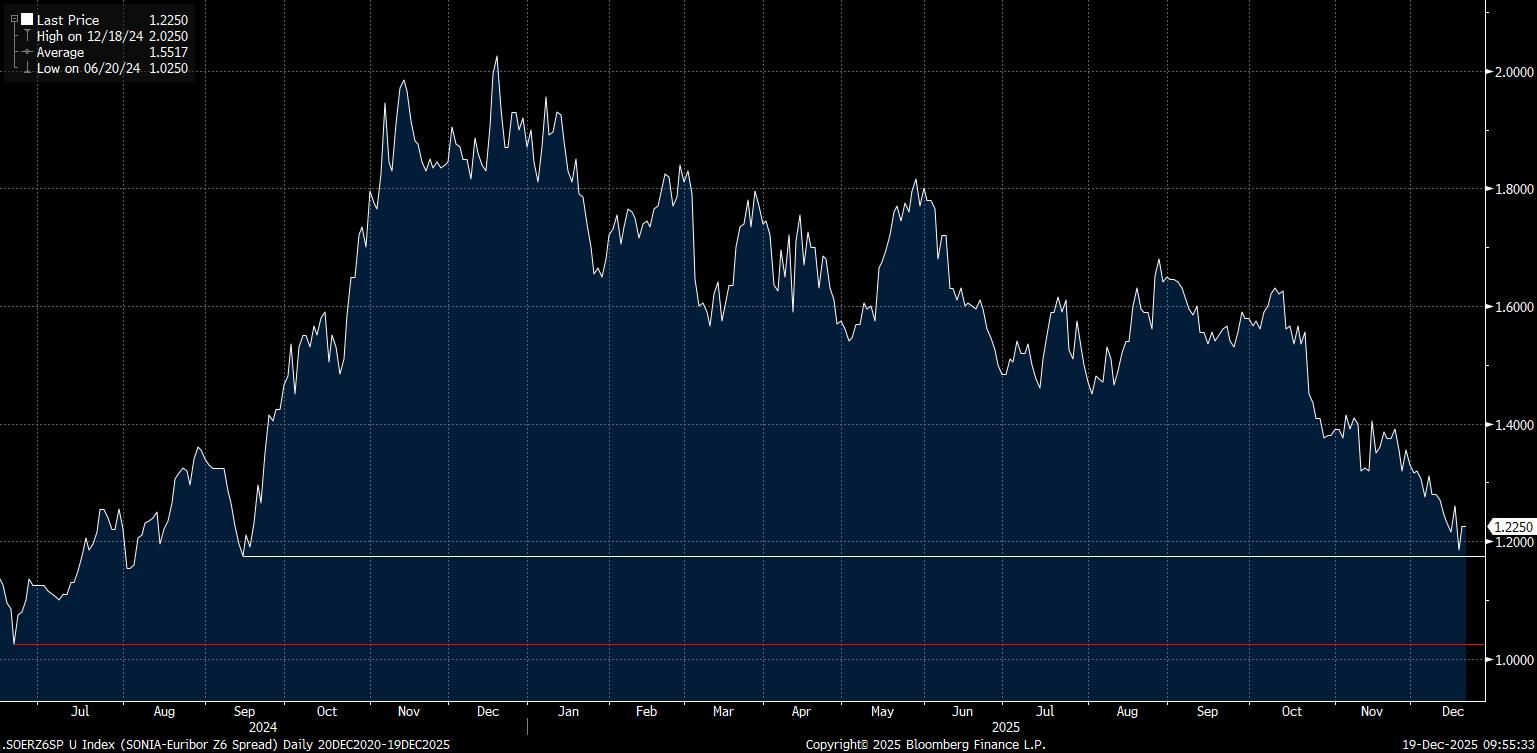

STIR: SONIA/Euribor Dec ’26 Spread Off Lows, Downside Risks Remain

Dec-19 10:21

Yesterday’s BoE decision pulled the SONIA/Euribor December ’26 spread off cycle lows after the combination of hawkish ECB repricing and soft UK CPI data drove the latest leg lower in recent sessions. Relative central bank outlooks may continue to drive fresh downside in the spread in the new year.

- Markets have taken the promotion of the language surrounding “closer call” decisions to the BoE’s statement as hawkish, although the ongoing easing bias in the communique alongside and since yesterday’s decision and slowing of UK CPI means that ~38.5bp of further is still priced into the GBP short end.

- This doesn’t seem particularly aggressive at this stage, with a full 25bp cut not fully discounted until the June MPC and inflation moving towards the Bank’s 2% target in a quicker than previously envisaged manner.

- Ongoing stickiness in UK wage growth presents a hawkish risk.

- Meanwhile, official ECB rhetoric continues to suggest that monetary policy settings are “in a good place”, stressing a meeting-by-meeting approach.

- The latest round of ECB source reports played down the odds of further easing, albeit with talks of rate hikes deemed premature (in the wake of the well-documented comments from Schnabel). While hikes still seem some way off, the bar to further ECB easing has definitely risen in recent weeks.

- Risks on this side of the spread come from the potential for slower-than-expected Eurozone growth (after an upgrade of the Bank’s projections) and lower-for-longer inflation (vs. ECB expectations).

- Support in the SONIA/Euribor December ’26 spread seen at the Sep 13 ’24 closing low (1.175%), which protects the June 20 ’24 closing low (1.025%).

Fig. 1: SONIA/Euribor Dec ’26 Spread

Source: MNI - Market News/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: UK and US Treasuries Roll Views (updated)

Nov-19 10:16

UK & Treasury Roll Views are mixed: Also be aware that next Week (27th Nov) is US Thanksgiving Day, so Pace could really pick up Post NFP Tomorrow.

JPM:

- WNA: Mildly Bullish.

- USA: Mildly Bullish.

- UXY: Neutral.

- TYA: Neutral.

- FVA: Neutral.

- TUA: Neutral.

- Gilt: Bullish.

MS:

- WNA: Mildly Bearish.

- USA: Neutral.

- UXY: Bearish.

- TYA: Mildly Bearish.

- FVA: Mildly Bearish.

- TUA: Neutral.

DB:

- WNA: Bearish.

- USA: Bullish.

- UXY: Neutral.

- TYA: Neutral.

- FVA: Bearish.

- TUA: Bullish.

Soc Gen:

- WNA: Mildly Bearish.

- USA: Neutral.

- UXY: Neutral.

- TYA: Mildly Bearish.

- FVA: Bearish.

- TUA: Mildly Bearish.

UBS:

- Gilt: Bearish. Their positioning CTA monitor sees moderate long positions in the Front Month. They see fair value in the G Z5/H6 spread at 152.

ITALY AUCTION RESULTS: Buyback Results

Nov-19 10:15

MEF has bought back:

- E1.181bln of the 3.50% Jan-26 BTP (ISIN: IT0005514473) at price 100.172.

- E0.825bln of the 0% Apr-26 BTP (ISIN: IT0005437147) at price 99.258,

- E1.294bln of the 3.80% Apr-26 BTP (ISIN: IT0005538597) at price 100.653.

- E0.667bln of the 3.85% Sep-26 BTP (ISIN: IT0005556011) at price 101.370.

- E1.033bln of the Apr-26 CCTeu (ISIN: IT0005428617) at price 100.209.

EUROPEAN INFLATION: Final HICP confirm services increase driven by transport

Nov-19 10:14

Looking into the details of the final Eurozone HICP print:

- The services increase in October from 3.24% to 3.36%Y/Y was largely due to services related to transport (as we expected) with that category rising from 3.32%Y/Y to 3.89%Y/Y. Air fares rose from -1.95%Y/Y in September to +1.66%Y/Y in October. Part of that stems for a soft September print, but there is also a strong October print in there that may well be partially reversed in November.

- Services related to communication also picked up from -0.10%Y/Y in September to +0.64%Y/Y in October - that has picked up from -1.70%Y/Y in August, so appear to be showing some more normalisation and we wouldn't really expect this to be reversed.

- Other services categories were broadly in line with their September Y/Y values. Package holidays doesn't look like a big contributor to the overall increase despite having picked up in some of the national prints. Some of the strength in accommodation seen in September was less pronounced in October.

- Clothing and footwear has reverted back to +0.62%Y/Y from the 1.08%Y/Y print seen in September and is now closer to the +0.53%Y/Y print seen in August. That, along with some softness in new motor sales, appears to be the largest single driver of the slowdown in NEIG (core goods) from 0.79%Y/Y in September to 0.62%Y/Y in October.

Related bullets

Related by topic

Euribor

SONIA

Bank of England

UK

European Central Bank

Eurozone

Trending Top

Apr-03 08:04

Apr-02 19:04