MNI US MARKETS ANALYSIS - Gov Shutdown in the Balance

Highlights:

- US government shutdown becoming more likely still, Trump set to meet lawmakers

- UK Chancellor Reeves looks to reassure at Conference speech

- USD/JPY erases large part of last week's strength, re-aligns with 200-dma

US TSYS: US Gov Shutdown Looms, Trump Meets Cong'l Leaders, Israel's Netanyahu

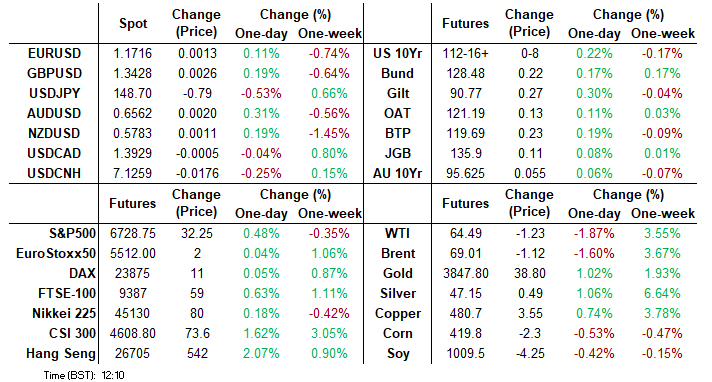

- Treasuries are climbing higher this morning as a US Government shutdown looms - Pres Trump to meet with congressional leaders at 1500ET in an attempt to avert a shutdown as Federal agencies to run out of money at midnight Tuesday. Aside from shutdown risks, market focus is on Friday's employment report for September.

- Back to early Thursday levels - the Dec'25 10Y contract (TYZ5) currently trades at 112-16.5 (+8) on light cumulative volumes of 195k. 10Y yield at 4.1426% (-.0330). Curves flatter: 2s10s -1.465 at 51.583, 5s30s -.363 at 97.829.

- Treasury futures traded lower last week and remain in retracement mode. Thursday’s sell-off has resulted in a print below the 50-day EMA, at 112-10. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. Initial firm resistance to watch is 113-00, the Sep 24 high.

- Economic Data: Pending Home Sales (1000ET), Dallas Fed Mfg Activity (1030ET)

- Treasury Auctions: $82B 13W & $73B 26W bills at 1130ET.

- Fedspeak: (0730ET) Fed Gov Waller on payments from Germany (text, no Q&A), (0800ET) Cleveland Fed Hammack policy panel at ECB w/ BOE Ramsden & ECB Lane, (1330ET) StL Fed Musalem moderated panel w/ former Fed Pres Bullard, (1800ET) Atlanta Fed Bostic moderated discussion (no text, Q&A).

- Politics: In addition to meeting with congressional leaders Thune, Johnson, Schumer and Jeffries at 1500ET, President Trump's schedule includes signing executive orders (1015ET), bilateral meeting with Israel's Netanyahu (1135ET) with presser at 1315ET, President Trump participates in a Gold Star Families Reception (1730ET).

SOFR: Mix Of Long Setting & Cover Most Prominent In Futures On Friday

OI data points to net long setting being most prominent through the reds on Friday, before net long cover came to the fore in the greens and blues as the SOFR futures strip twist steepened

| 26-Sep-25 | 25-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,444,055 | 1,449,448 | -5,393 | Whites | +22,562 |

SFRZ5 | 1,514,329 | 1,522,050 | -7,721 | Reds | +41,376 |

SFRH6 | 1,216,258 | 1,182,195 | +34,063 | Greens | -20,591 |

SFRM6 | 1,031,498 | 1,029,885 | +1,613 | Blues | -1,628 |

SFRU6 | 936,267 | 902,448 | +33,819 |

|

|

SFRZ6 | 1,041,486 | 1,055,171 | -13,685 |

|

|

SFRH7 | 758,297 | 742,132 | +16,165 |

|

|

SFRM7 | 775,915 | 770,838 | +5,077 |

|

|

SFRU7 | 669,626 | 676,518 | -6,892 |

|

|

SFRZ7 | 727,476 | 727,951 | -475 |

|

|

SFRH8 | 415,766 | 421,828 | -6,062 |

|

|

SFRM8 | 359,660 | 366,822 | -7,162 |

|

|

SFRU8 | 266,461 | 275,015 | -8,554 |

|

|

SFRZ8 | 298,631 | 295,455 | +3,176 |

|

|

SFRH9 | 188,448 | 185,308 | +3,140 |

|

|

SFRM9 | 177,800 | 177,190 | +610 |

|

|

US TSY FUTURES: Cover Most Prominent On Friday

OI data points to a mix of net short cover (TU), long setting (FV), long cover (TY, US & WN) and short setting (UXY) as the Tsy futures curve twist steepened on Friday.

- The curve-wide bias was tilted towards cover.

| 26-Sep-25 | 25-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,561,246 | 4,578,816 | -17,570 | -596,677 |

FV | 6,729,900 | 6,708,903 | +20,997 | +921,522 |

TY | 5,467,351 | 5,484,173 | -16,822 | -1,096,393 |

UXY | 2,414,482 | 2,403,972 | +10,510 | +919,388 |

US | 1,807,227 | 1,817,470 | -10,243 | -1,452,421 |

WN | 2,003,714 | 2,011,180 | -7,466 | -1,393,545 |

|

| Total | -20,594 | -2,698,127 |

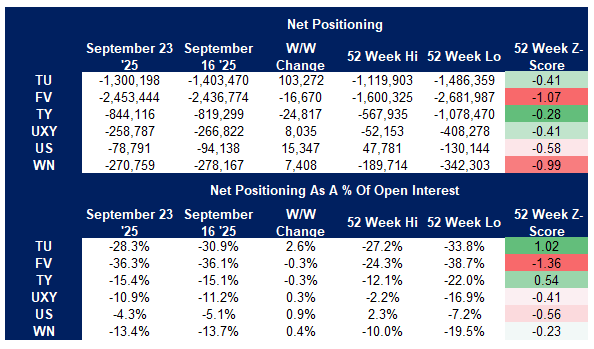

US TSY FUTURES: CFTC CoT Shows Funds & Asset Mangers Trimming Exposure

The latest CFTC CoT report pointed to relatively aggressive trimming of exposure in Tsy futures on the part of both asset managers and leveraged funds in the week ending September 23.

- Asset managers trimmed net longs in all contracts outside of FV futures, adding modestly to longs in the latter. This meant that the cohort trimmed its curve-wide net long position by $13.6mln DV01 equivalent but remained net long in all contracts.

- Leveraged funds covered net shorts in TU, FV & TY futures, while they added to shorts in UXY, US & WN futures at the margins. This meant that the cohort reduced their curve-wide net short exposure by $8.2mln DV01 equivalent but remained net short across the curve.

- Meanwhile, broader non-commercial accounts trimmed net shorts in TU, UXY, US & WN futures, while they added to net shorts in FV & TY futures. The cohort remains net short across the curve (see table below for more granular detail on non-commercial positioning).

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

UK FISCAL: VAT increase impacts on fiscal, CPI, monetary policy (1/2)

- Chancellor Reeves seemed to commit a little more firmly against a VAT rise this morning in her Sky News interview (we will be watching closely her language at the Labour party conference where she is due to speak at midday - but probably with a more friendly audience).

- In terms of the fiscal revenues, the Treasury's illustrative effects of a change indicate that a 1ppt increase in VAT would raise GBP8.8bln in 2026/27, GBP9.2bln in 27/28 and GBP9.55bln in 28/29.

- As we noted last week, although the natural response is to think of VAT as a retail tax, it is much broader than that, also applying to hospitality and construction as well as across a number of other sectors.

- Looking at the impact on CPI, the standard rate of VAT is not paid on "essential" goods or household energy. It does apply to vehicular fuels (although this could be offset by a VED reduction) and also does apply to non-essential foods (confectionary, crisps, ice cream) as well as mineral waters and soft drinks.

- We estimate that around 60% of that CPI basket would be directly impacted by a VAT increase. So a 1ppt increase in VAT from 20% to 21% would increase headline inflation by around 0.5ppt if fully passed through.

- The last increase in VAT was implemented in January 2011 (2.5ppt increase from 17.5% to 20%). The timing of this - just after the Global Financial Crisis - makes it hard to use this as a basis for comparison (and VAT eligibility has changed somewhat since then too) but we note that Y/Y CPI rose from 3.26% in October 2010 to 4.35% by February 2011 (an increase of 1.09ppt), and continued to rise to a peak of 5.18% in September 2011.

UK FISCAL: VAT increase impacts on fiscal, CPI, monetary policy (2/2)

- We do not think that the MPC would be able to fully look through a VAT increase and continue to cut Bank Rate. It would likely lead to a pause, in our view, and even by placing a question mark over the feasibility of a VAT hike over the weekend might be enough to spook the MPC's swing voters to vote to keep Bank Rate on hold in November (albeit there is not much priced for this prospect by markets anyway - and we still think the chance is under-priced even given the weekend's news).

- The MPC is very focused on where headline CPI goes in the short-term and its impact on to inflation expectations. Particularly with food prices having increased notably and with continued commentary that the weekly supermarket shop, household energy and petrol prices have an outsized impact on inflation expectations it is important to note that of the "food and non-alcoholic beverages" category around 20% is subject to VAT. For the broader "food, alcohol and tobacco" category this rises to 40%.

- So if there was a VAT increase the MPC may want to wait to see how higher CPI data in Q1 filter through to inflation expectations and potentially even wait for more hard data on wage settlements in Q1 / April 2026. This could potentially even push a cut even later than April (as a lot of the wage data will not be fully available until June). Terminal rates may not be impacted, but timing almost certainly would be, in our view.

- The MNI Markets team thinks that an increase to the basic rate of income tax would be more appropriate for the economy than an increase in VAT. And despite this increasing tax on "working people" it would likely be better than the alternative of constant tinkering around the edges and only leaving another small c. GBP10bln of fiscal headroom, which would be vulnerable to more speculations over more tax increases next year.

- Chancellor Reeves may make more media appearances this morning ahead of her midday Labour Party Conference address.

FOREX: Reeves Looks to Reassure at Conference Speech

- The USD is slipping against most others in G10 early Monday, keeping the USD Index closely glued to the 50-dma of 98.038 - a level that's helped dictate price action well since the beginning of August. The inability of the USD to build on last week's gains does suggest those looking for a near-term greenback bounce may need more support before progress toward a more sustained recovery. This leaves the stress evident in the labor market as the key near-term driver, however resilient inflationary pressures continue to provide the counter, a topic raised by Fed's Hammack today, who stated inflation may stay above target out to 2028.

- The JPY, AUD are the firmest performers in G10 - with the JPY adding to gains as the Japanese government confirm an upgraded near-term view on the economy and economic conditions. This has helped USD/JPY revert back to key support of the 148.44 200-dma to erase a large part of last week's strength in the pair.

- Much market focus on UK Chancellor Reeves' appearance at the Labour Party Conference later today, at which she'll defend the government's record on the economy and potentially set out further clues for her intentions into the Autumn Budget as pressure grows on how to close the fiscal gap without breaching manifesto commitments of higher income tax, VAT or national insurance. Into the conference speech, GBP remains mixed, however traded lower last week, marking an extension of the current bear cycle that started Sep 17. The move down has resulted in a break of 1.3491, a trendline support drawn from the Aug 1 low. This undermines a recent bullish theme.

- Outside of the conference appearance, pending home sales and Dallas Fed Manufacturing data are due today, while Eurozone CPI data and the MNI Chicago PMI are the focus for the rest of the week.

FOREX: Notable USDJPY Weakness, Pullback Technically Corrective (1/2)

- On Friday, USDJPY rose to within 4 pips of the 150 mark, and it was notable that the recovery had outpaced that of the DXY, rallying 3.07% to its peak. Subsequently, the pair has retraced a solid portion of this advance, extending this morning amid US government shutdown concerns. President Trump will meet senior figures in congress at the White House in a last-ditch attempt to avert a shutdown.

- With USDJPY moving average studies highlighting a dominant uptrend, today’s pullback appears technically corrective. Sights are on 150.92, the Aug 1 high and key resistance, while pivot support remains much further out at 145.49, Sep 17 low.

- Some market participants have sighted BOJ board member Asahi Noguchi’s comments as potentially assisting the yen bid. Noguchi said the Bank's monetary policy is entering a phase requiring careful assessment, adding that Japan will eventually need a new policy perspective addressing upside risks, while also facing downside pressures from U.S. tariff policies.

- Separately, a former BOJ Executive Director told MNI that markets are watching Bank of Japan communications more closely than economic data for signals on policy moves. They added there is no reason for the BOJ to refrain from raising the policy rate while underlying CPI inflation remains below 2%.

- Japan’s government slightly tweaked its economic assessment in September, upgrading views on private consumption and capital investment for the first time in over a year, though leaving its overall judgment largely unchanged, the Cabinet Office said Monday.

FOREX: JPY Crosses Might Take Focus Given US Employment Related Risk (2/2)

- With such focus on the dollar and the impending US employment report this week, it is worth looking at some of the key Yen crosses and their significant chart points, especially considering that uncertainty surrounding Japanese politics and the LDP leadership remains high. Fiscal dove and well-positioned LDP contender Sanae Takaichi hinted at a review of Japan’s $550 billion investment fund that was part of its pact with the US.

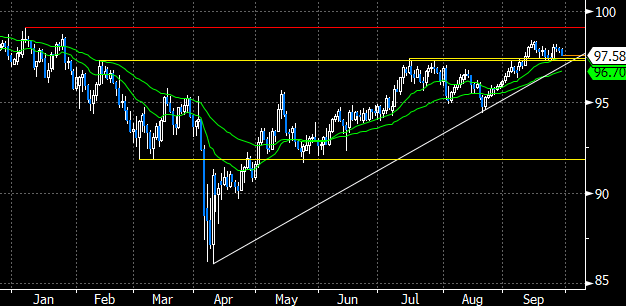

- Given the proximity to tomorrow’s RBA decision, it’s worth noting that AUDJPY (shown below) remains in a strong uptrend, with the 20-day EMA acting as very strong support in recent weeks amid the firm price action for major equity indices. Additionally, an area between 97.25-45 continues to hold, while the uptrend from the April lows remains intact.

- Should we move higher, the year’s highs reside at 99.17, before the psychological 100 mark. A move back below the 50-day EMA at 96.70 would be required to alter the trend.

- Today’s EURJPY price action has taken spot back to the prior breakout level, just below the 174 handle. However, after trading to a fresh cycle high last week, a bullish theme remains prevalent. The overnight high fell just short of 175.43, the Jul 11 ‘24 high and a key medium-term resistance.

- One cross that has failed to garner much topside momentum above 200.00 is GBPJPY, and the cross has today slipped below the 20-day EMA. While noting that GBPUSD had broken some important trendline supports last week, GBPJPY might be most vulnerable to a further upward yen correction. The 50-day EMA remains key here having not meaningfully closed below this average apart from the fleeting test below in early August. The average intersects at 198.98, and the next downside target would be 195.04, the August low.

Source: Bloomberg Finance L.P. / MNI

EQUITIES: EuroStoxx 50 Futures Breach Key Resistance and Bull Trigger at 5525.00

- Eurostoxx 50 futures have started the week on a bullish note. Today’s gains have resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5433.67, the 20-day EMA.

- A bull cycle in S&P E-Minis remains intact and the latest pullback is considered corrective. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, the contract has recently pierced initial support at the 20-day EMA, currently at 6640.59. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6526.11.

COMMODITIES: WTI Futures Holding Onto Recent Gains, Key Resistance at $68.43

- WTI futures are holding on to their recent gains. The contract has breached resistance at $65.43, the Sep 2 high and this has improved the short-term condition for bulls. However, the next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on key support at $60.85. A break of this level would reinstate a bearish theme.

- The trend condition in Gold is unchanged and a bull cycle remains in play. The yellow metal has started the week on a bullish note, trading to a fresh cycle high, confirming a resumption of the primary uptrend. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3831.4, a Fibonacci projection. On the downside, support to watch lies at $3646.3, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 29/09/2025 | 1130/0730 | Fed Governor Christopher Waller | ||

| 29/09/2025 | 1200/1400 | ECB Lane In Policy Panel At Inflation Conference | ||

| 29/09/2025 | 1200/0800 | Cleveland Fed's Beth Hammack | ||

| 29/09/2025 | 1200/1300 | BOE Ramsden On ECB Inflation Panel | ||

| 29/09/2025 | 1330/0930 | NY Fed's Roberto Perli | ||

| 29/09/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/09/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 29/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 29/09/2025 | 1730/1330 | St. Louis Fed's Alberto Musalem | ||

| 29/09/2025 | 1730/1330 | Ex-St. Louis Fed's James Bullard | ||

| 29/09/2025 | 1730/1330 | New York Fed's John Williams | ||

| 29/09/2025 | 2200/1800 | Atlanta Fed's Raphael Bostic | ||

| 30/09/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 30/09/2025 | 2350/0850 | ** | Industrial Production | |

| 30/09/2025 | 2350/0850 | * | Retail Sales (p) | |

| 30/09/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/09/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 30/09/2025 | 0130/1130 | * | Building Approvals | |

| 30/09/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 30/09/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/09/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/09/2025 | 0645/0845 | *** | HICP (p) | |

| 30/09/2025 | 0645/0845 | ** | PPI | |

| 30/09/2025 | 0645/0845 | ** | Consumer Spending | |

| 30/09/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/09/2025 | 0755/0955 | ** | Unemployment | |

| 30/09/2025 | 0800/1000 | ** | PPI | |

| 30/09/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/09/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/09/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/09/2025 | 0900/1100 | *** | HICP (p) | |

| 30/09/2025 | 1000/0600 | Fed Vice Chair Philip Jefferson | ||

| 30/09/2025 | 1100/1300 | ECB Cipollone In Panel At Sibos | ||

| 30/09/2025 | 1150/1250 | BOE Lombardelli Panel On MonPol, Bank of Finland | ||

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1250/1450 | ECB Lagarde Keynote at MonPol Conference, Bank of Finland | ||

| 30/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 30/09/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/1500 | ECB Elderson In Panel On Climate Action | ||

| 30/09/2025 | 1300/0900 | Boston Fed's Susan Collins | ||

| 30/09/2025 | 1325/1425 | BOE Mann Fireside Chat At FT | ||

| 30/09/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/09/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 30/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 30/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 30/09/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 30/09/2025 | 1530/1630 | BOE Breeden Speech At Cardiff University | ||

| 30/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 30/09/2025 | 1600/1200 | ** | USDA GrainStock - NASS |