MNI US MARKETS ANALYSIS - GBP Soft, Highest UK U/E Since COVID

Highlights:

- Stocks hold weekly gains, but momentum softens before any test on alltime highs

- GBP gaps lower as unemployment rate unexpectedly shoots higher, hitting highest since pandemic

- Weekly ADP series in focus, but shutdown progress may mean we get September NFP as soon as Friday

US TSYS: Light Volumes With Veterans Day, Weekly ADP Series To Headline

- Treasuries are little changed after thin overnight trading, with cash closed for Veterans Day.

- The Senate has passed a funding package to reopen the US government, with the package heading to the House of Representatives. We see the government on track to re-open on Wednesday.

- The weekly ADP series headlines today’s docket after last week’s clear sensitivity to alternate labor indicators.

- TYZ5 trades at 112-21 (-00+) having kept to narrow ranges in what has been a very quiet overnight session with cumulative volumes only just over 100k.

- A key near-term resistance is seen at at Friday's joint high of 113-02 (Nov 5 & 7 highs), but a bear threat is still present at 112-06 (Sep 25 low) before which lies 112-09+ (Nov 5 high) and other various support levels.

- Data: NFIB Oct (already released), ADP weekly (0815ET), Redbook retail weekly (0855ET)

- Fedspeak: Fed Gov. Barr on AI and innovation in Singapore (2225ET)

- No issuance with Veterans Day.

- Politics: Trump participates in Wreath Laying Ceremony and delivers remarks (1100ET)

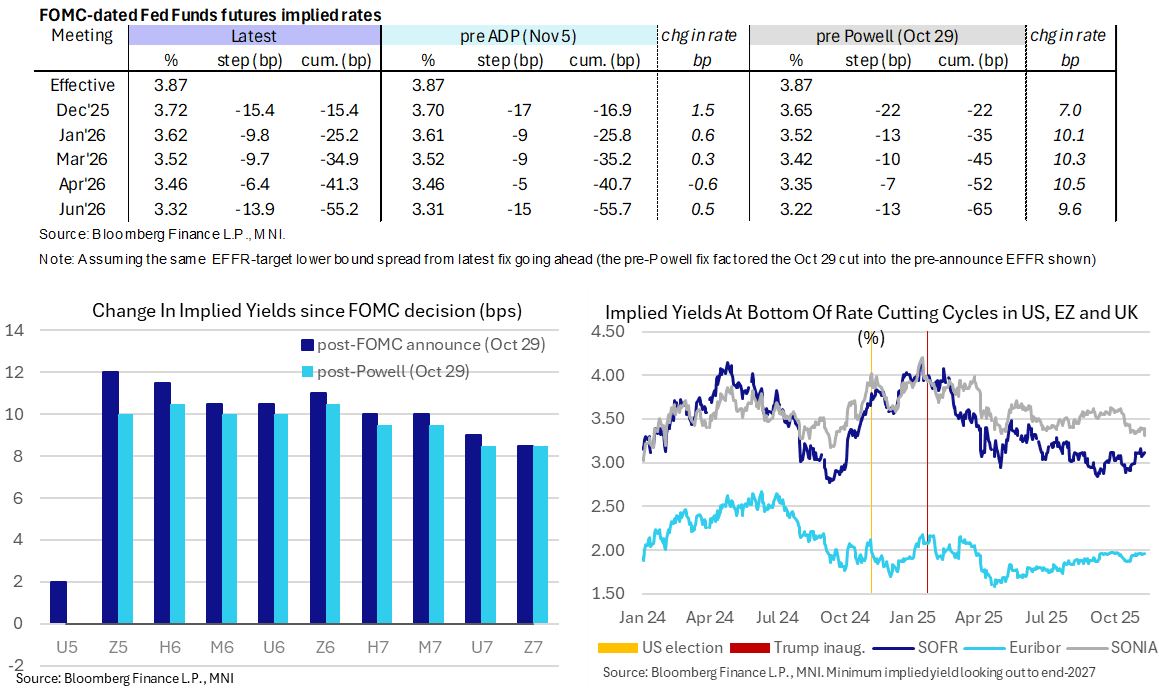

STIR: Weekly ADP Series A Potential Test Of Steady US Rates

- Fed Funds implied rates are little changed on the day, with today’s data focus likely on the first known-ahead-of-time publication of weekly ADP series at 0815ET.

- Cumulative cuts from 3.87% effective: 15.5bp Dec, 25bp Jan, 35bp Mar, 41.5bp Apr and 55bp Jun.

- SOFR futures are also little changed, between 1 tick firmer (Z5 and H6) and 1 tick lower (Z7).

- It leaves the terminal implied yield at 3.115% (H7) off last week’s multi-month high of 3.16% before being helped lower by soft alternative labor data.

- Today’s only scheduled Fedspeak comes overnight with Fed Governor Barr (voter) in Singapore, speaking on AI and innovation at 2225ET (text + Q&A). He said on Nov 6 that the Fed has made progress on inflation but there is still "work to do". Wealthier households are thriving in a two-speed economy whilst the Fed must pay attention to ensuring the job market is solid.

US TSY FUTURES: Short Setting Most Prominent On Monday

OI data points to instances of net short setting (FV, UXY & WN) outweighing more limited rounds of net long cover (TU, TY & US) as markets reacted to movement towards the end of the U.S. government shutdown on Monday.

| 10-Nov-25 | 07-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,647,222 | 4,653,405 | -6,183 | -231,751 |

FV | 6,902,050 | 6,872,863 | +29,187 | +1,250,488 |

TY | 5,422,840 | 5,428,848 | -6,008 | -401,164 |

UXY | 2,501,470 | 2,493,536 | +7,934 | +711,377 |

US | 1,850,463 | 1,851,368 | -905 | -114,986 |

WN | 2,168,566 | 2,160,748 | +7,818 | +1,458,385 |

|

| Total | +31,843 | +2,672,349 |

SOFR: Short Setting Dominated In Front End Of Futures On Monday

OI data points to net short setting in the white, red and blue SOFR futures packs on Monday, while net long cover was slightly more prominent in the greens.

- SOFR futures settled lower as the risk-positive impact stemming from movement towards the end of the U.S. government shutdown outweighed any increased confidence in Fed easing that the related resumption of U.S. official data releases may bring.

| 10-Nov-25 | 07-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,381,508 | 1,361,302 | +20,206 | Whites | +92,945 |

SFRZ5 | 1,435,021 | 1,439,176 | -4,155 | Reds | +19,922 |

SFRH6 | 1,231,752 | 1,181,065 | +50,687 | Greens | -1,181 |

SFRM6 | 1,105,233 | 1,079,026 | +26,207 | Blues | +3,203 |

SFRU6 | 1,108,727 | 1,100,480 | +8,247 |

|

|

SFRZ6 | 1,195,646 | 1,200,885 | -5,239 |

|

|

SFRH7 | 839,580 | 825,890 | +13,690 |

|

|

SFRM7 | 816,885 | 813,661 | +3,224 |

|

|

SFRU7 | 766,141 | 763,879 | +2,262 |

|

|

SFRZ7 | 804,365 | 803,121 | +1,244 |

|

|

SFRH8 | 429,602 | 438,003 | -8,401 |

|

|

SFRM8 | 410,600 | 406,886 | +3,714 |

|

|

SFRU8 | 356,837 | 352,745 | +4,092 |

|

|

SFRZ8 | 330,641 | 331,139 | -498 |

|

|

SFRH9 | 202,953 | 202,652 | +301 |

|

|

SFRM9 | 186,305 | 186,997 | -692 |

|

|

UK DATA: Labour data soft across the board

- Private regular pay is actually a bit softer than expected at 4.17%Y/Y in the 3-months to September (BOE forecast 4.23%). This still rounds to 4.2% in line with expectations, however.

- This is due to a soft single month figure of 3.79%Y/Y. At first glance the revision to August is very small (from 4.21% to 4.23%Y/Y).

- The unemployment rate was also higher than expected at 4.97% against the expected 4.87% from the BOE and 4.9% consensus.

- 3-month LFS employment change -22k (expected broadly flat).

- The revisions to PAYE payrolls are in a negative direction too (last September revised to -32k from -10k with the flash October number also at -32k (expected broadly flat). This puts the 3-month change at -54k (the 3-months to Sep revised to -23k from flat).

- PAYE median pay is also very soft at 3.13%Y/Y. That had been 5.86%Y/Y in the last print.

- There is nothing in this report that is not soft on a first read (other than public sector pay).

- GBPUSD down around 40 pips. This is encouraging for Bailey to vote for a cut (but we've still got one more labour print and 2 CPI prints before the decision).

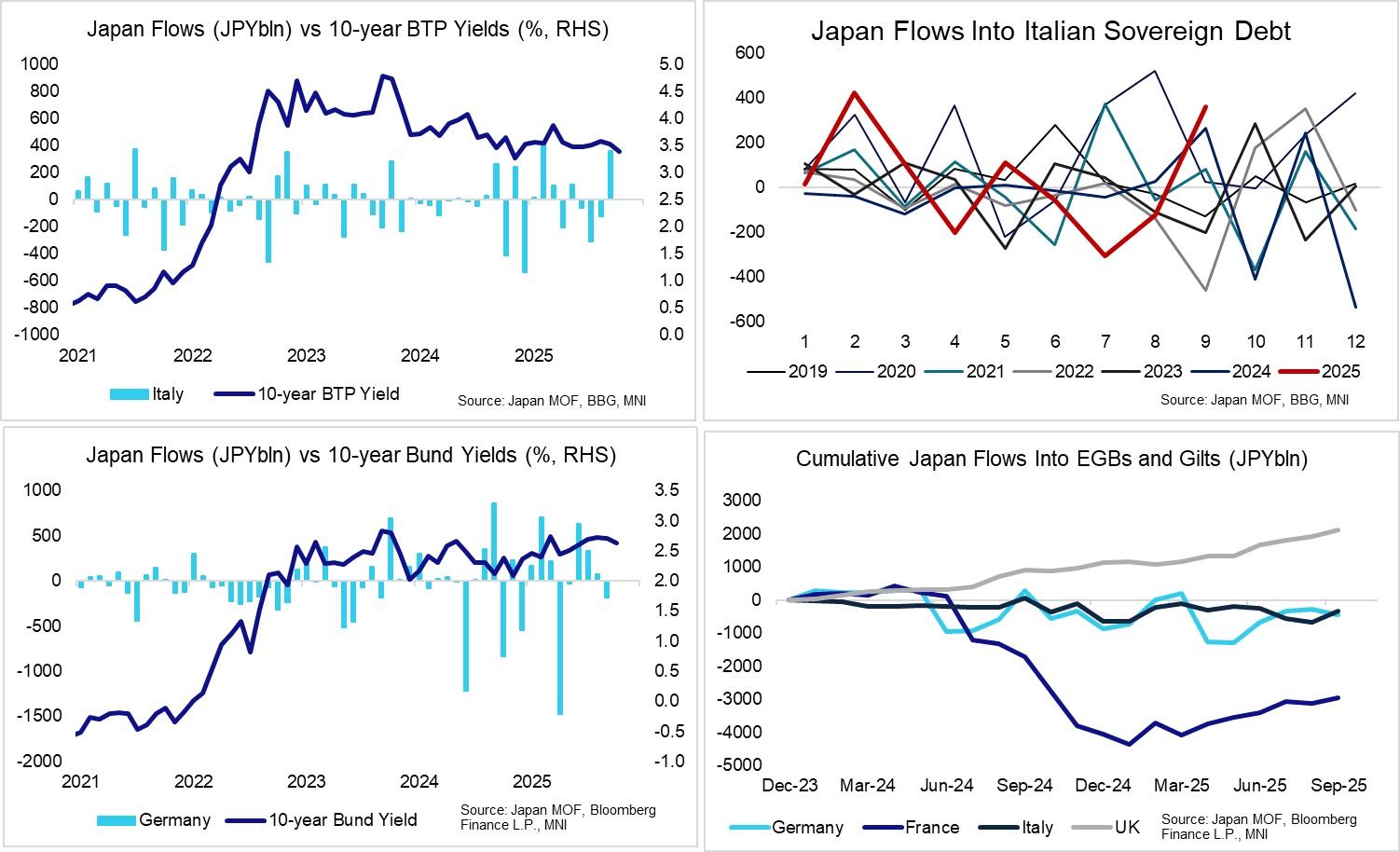

BONDS: Japanese Investors Were Large Net Buyers Of Italian Debt In September

Japanese investors net bought JPY361bln of Italian debt in September, according to domestic balance of payments data released overnight. This was the third largest single month net inflow since the start of 2021, after JPY423bln in February ’25 and JPY375bln in July ’21.

- After being subject to modest widening pressure in late-August/early-September, the 10-year BTP/Bund spread has resumed this year’s narrowing trend. BTP outperformance has been supported by relatively political stability in Italy versus the likes of France, improved domestic fiscal metrics and lower EUR rates vol. This combination of factors looks to have tempted Japanese investors back into BTPs in September, after a few months of net outflows in late Q2/early Q3.

- Japanese investors net bought JPY188bln of French debt in September, despite ongoing political uncertainty through the month amid the resignation of ex-PM Bayrou. It will be interesting to see aggregate net flows in October, with new PM Lecornu's budget negotiations dominating headline flow.

- There were JPY180bln of net sales in German bonds in September, while Gilts saw familiar net inflows.

- Meanwhile, Japanese investors net purchased JPY1,126bln of US Treasuries, bringing the year-to-date net inflow to JPY6,451bln.

- Our Asia-Pac team highlighted overnight that the larger-than-expected Japanese current account surplus was a combination of both the trade balance component and a surge in the primary income balance.

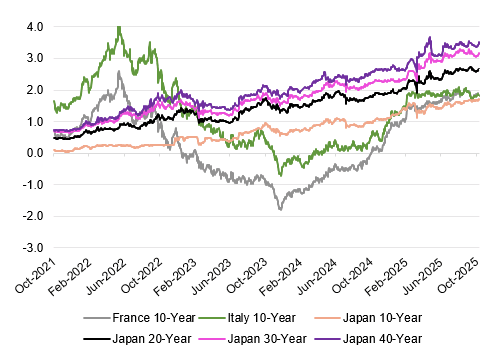

Note that both 10-Year Italian & French yields provide a modest 10-15bp pickup vs. 10-Year JGBs, when accounting for 3-month FX hedging costs from the perspective of a Japanese investor.

- This helps explain some of the demand, particularly given ongoing fiscal uncertainty in Japan.

- Those same FX hedging cost-adjusted yields are still some way below 20-, 30- & 40-Year JGBs, as seen in the chart below.

Fig. 1: JGB Yields Vs. 10-Year Italian & French Yields FX-Hedged From The Perspective Of A Japanese Investor (%)

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: GBP Pressured by UK Data, US-Swiss Trade Deal Buoys CHF

- The US Senate has passed a funding package to reopen the US government, sending it to the house which should allow for a reopening on Wednesday. The USD index has been consolidating around the 99.50 mark as details surrounding the release of US tier-one data is awaited. This left country-specific drivers in focus, with soft UK labour market data prompting GBP downside while CHF outperforms on optimism for a US-Swiss trade deal.

- A December BoE cut is now 80% and renewed downward pressure for GBPUSD looks set to snap a four-day winning streak for the pair. The bounce fell short of initial resistance at 1.3231, the 20-day EMA. Moving average indicators continue to signal a bearish trend, potentially strengthening the narrative that recent gains could be considered corrective.

- CHF outperforms following late yesterday's optimism on a potential Swiss trade deal with the US. While such a deal would be unlikely to sway SNB rates this year or the next, it should see a moderate upwards revision of 2026 GDP forecasts for the country. EURCHF sees downside pressure as a function of that at 0.9287. Key medium-term support for the pair remains at the clustered lows between 0.9206/22.

- Despite firmer consumer confidence data, AUD has reversed a touch lower this morning, eroding a small portion of the impressive gains Monday. This has allowed AUDNZD to edge lower, with the 2013 highs at 1.1586 broadly holding. Initial support for the cross moves up to 1.1513.

- Two ECB speakers as well as Norges Bank's Wolden Bache are scheduled for the rest of the day.

FOREX: EURGBP Bounces from Support Again After Weak Labour Market Report

- Softer-than-expected UK labour market data has prompted December BoE cut pricing to reach ~80%, and in tandem has provided some renewed pessimism for GBP which sits at the bottom of the G10 leaderboard.

- Downward pressure for GBPUSD (-0.33%) looks set to snap a 4-day winning streak, which saw the pair meaningfully correct from recent cycle lows of 1.3010 to 1.3191 highs on Monday. The bounce fell short of initial resistance at 1.3231, the 20-day EMA. Moving average indicators continue to signal a bearish trend, potentially strengthening the narrative that recent gains could be considered corrective.

- Sterling weakness even more notable in the cross, with EURGBP rising 0.45% to 0.8812 at typing. Once again, dips remain very well supported around the prior breakout level at 0.8769, highlighting the dominant uptrend. Topside targets remain at 0.8835 and 0.8875, the April 2023 high.

- It’s well documented that BoE Governor Bailey is viewed as the key swing vote and this morning’s data increases the odds of him opting to cut next month. However, it is worth noting there will be one more labour market print and two CPI releases before the next decision. With the other 8 MPC members having entrenched views, GBP volatility around non-Bailey speeches is likely to be much reduced ahead of the budget on Nov 26.

OPTIONS: Expiries for Nov11 NY cut 1000ET (Source DTCC)

- AUD/USD: $0.6450(A$644mln)

--------------------------------------------------------

Larger FX Option Pipeline

- EUR/USD: Nov12 $1.1500-05(E1.1bln), $1.1688-90(E1.3bln); Nov13 $1.1590(E1.5bln)

- USD/JPY: Nov13 Y147.00($1.6bln), Y152.96-00($1.1bln), Y155.00($1.1bln)

- GBP/USD: Nov12 $1.3100(Gbp1.9bln), $1.3225-30(Gbp1.3bln)

- AUD/USD: Nov12 $0.6500(A$1.2bln), $0.6530-50(A$1.2bln); Nov14 $0.6750(A$2.2bln)

- USD/CAD: Nov14 C$1.4025-35($1.2bln)

EQUITIES: Trend Condition in E-Mini S&P Bullish Despite Breach of 50-Day EMA

- A medium-term bull trend in Eurostoxx 50 futures remains intact and recent weakness appears to have been a correction. Price has managed to find support below two important price points; the 50-day EMA, at 5580.70, and 5577.00, the base of a bull channel drawn from the Aug 1 low. A clear break of both levels would strengthen a bear theme and highlight a stronger reversal. Sights are on the bull trigger at 5742.00, the Oct 29 high.

- The trend condition in S&P E-Minis remains bullish and the pullback since the Oct 30 high appears corrective. The contract has managed to find support below the 50-day EMA, currently at 6716.03 and a key support. Friday’s activity also highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. A continuation higher would signal the end of a correction and open 6953.75, Oct 30 high and bull trigger.

COMMODITIES: Recent Weakness in WTI Futures Appears to Be a Flag Formation

- Recent weakness in WTI futures appears to be a flag formation - a bullish continuation pattern. This suggests that an upward corrective cycle remains intact for now. Price has recently traded through the 50-day EMA, at $60.84, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low.

- The downleg in Gold since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains also suggest the correction is over. Price remains above a key support at the 50-day EMA, at $3890.0.0. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1200/1200 | BOE APF Quarterly Report | ||

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 11/11/2025 | 0325/2225 | Fed Governor Michael Barr | ||

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0900/1000 | * | Industrial Production | |

| 12/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | *** | Money Supply | |

| 12/11/2025 | - | *** | New Loans | |

| 12/11/2025 | - | *** | Social Financing | |

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins |

Note: US Government shutdown ongoing, meaning any Government-compiled US statistics will not be released.