MNI US MARKETS ANALYSIS - Fallout Contained Despite Tensions

Highlights:

- Market fallout contained despite continued Israel - Iran escalation

- Central banks take focus this week with BoJ, Fed, BoE, SNB, Riksbank and Norges Bank all due

- EUR/JPY makes light work of resistance to retain underlying uptrend

US TSYS: Post-Weekend Losses Held; G7 Talks and 20Y Supply Watched Near-Term

- Treasuries have pared losses but remain lower on the day as part of broader moves consistent with a slight easing in Israel-Iran escalation fears compared to levels heading into the weekend.

- Aside from G7 deliberations, today sees the first regional Fed manufacturing survey for June and we also note a rare Monday 20Y auction due to a compressed week ahead of the Juneteenth holiday.

- Last week saw some reasonable duration demand. The 10Y stopped through by 0.9bp albeit with the bid-to-cover slipping from 2.60x to 2.52x whilst the 30Y stopped through by 1.5bps and the bid-to-cover increased from 2.31x to 2.43x. Last month’s 20Y auction was weak however, tailing by 1.2bps.

- Cash yields are 1.5-3bp higher on the day, with increases led by 7s.

- TYU5 trades near unchanged at 110-19 (- 00+) off an earlier low of 110-10+, on reasonable overnight volumes of 305k.

- The earlier low didn’t trouble support at 109-28 (Jun 6/11 low) whilst resistance also remains intact for now, with 111-13 (Jun 13 high) before 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg).

- Data: Empire mfg Jun (0830ET)

- Coupon issuance: US Tsy $13B 20Y Bond auction re-open - 912810UL0 (1300ET)

- Bill issuance: US Tsy $76B 13W & $68B 26W bill auctions (1130ET)

- Tariffs: Handelsblatt reports that the EU Commission is prepared to accept a flat-rate US tariff of 10% as part of trade talks in hopes to avoid higher tariffs on autos, pharma products and electronics.

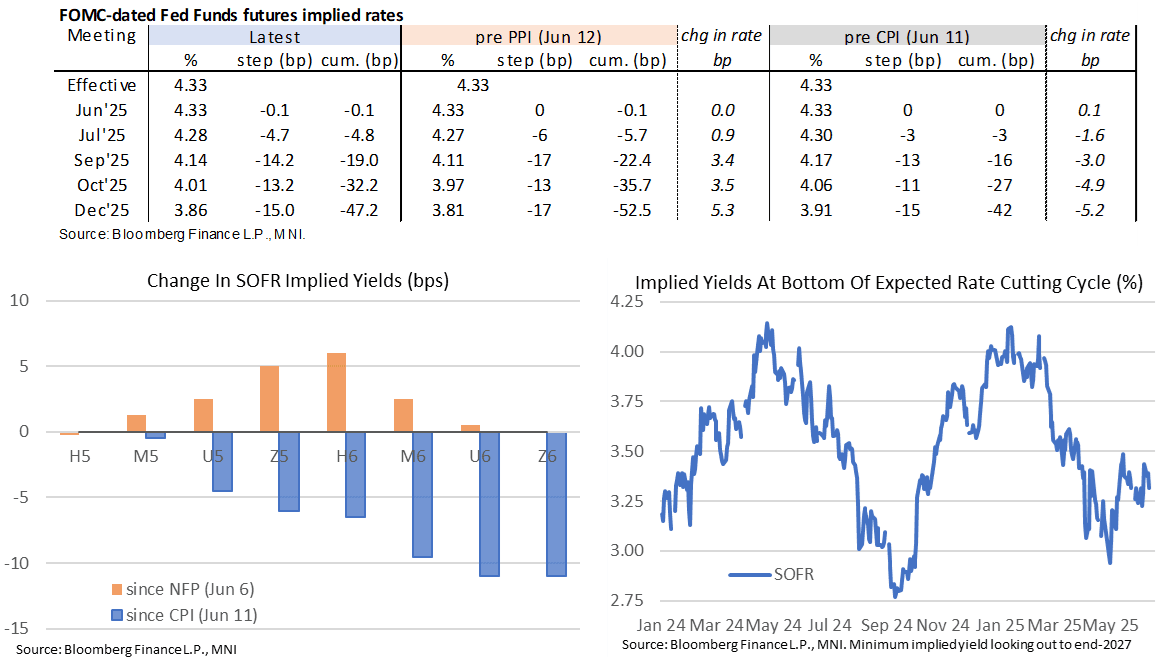

STIR: Next Fed Cut Seen In Oct With G7 and Wed FOMC Eyed

- Fed Funds implied rates are up to 3bp higher for 2025 meetings since Friday’s close despite modest losses for oil futures.

- The 47bp of cuts to end 2025 is off the 42bp seen before last week’s soft CPI report but remains one of the more hawkish levels in recent months.

- Cumulative cuts from 4.33% effective: 0bp for Wed, 5bp for Jul, 19bp for Sep, 32bp for Oct and 47bp for Dec.

- The SOFR implied terminal yield of 3.32% (SFRZ6, unch) points to ~100bp of cuts for what’s left of the easing cycle.

- Markets are focused on tariff and middle east discussions at G7 meetings this week before the FOMC decision on Wednesday.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Jun2025_ba372b9458.pdf

- The full analyst preview note will follow later today.

US TSY FUTURES: Mix Of Modest Long Cover & Short Setting On Friday

OI data points to a mix of modest net long cover (TU & US) and short setting (FV, TY, UXY & WN) as Tsy futures finished lower on Friday, with a sligh bias towards the latter in curve-wide net DV01 terms.

| 13-Jun-25 | 12-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,983,667 | 3,987,301 | -3,634 | -142,444 |

FV | 6,878,205 | 6,861,290 | +16,915 | +736,216 |

TY | 4,808,438 | 4,803,391 | +5,047 | +333,919 |

UXY | 2,348,245 | 2,345,800 | +2,445 | +213,104 |

US | 1,736,215 | 1,737,004 | -789 | -110,746 |

WN | 1,895,298 | 1,895,180 | +118 | +21,425 |

|

| Total | +20,102 | +1,051,474 |

STIR: Short Setting Dominated In SOFR Whites On Friday

OI data points to net short setting dominating in the SOFR whites on Friday, before a more balanced round of net short setting and long cover was seen further out the strip as contracts finished lower.

| 13-Jun-25 | 12-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,070,640 | 1,068,294 | +2,346 | Whites | +142,066 |

SFRM5 | 1,538,404 | 1,413,375 | +125,029 | Reds | -16,982 |

SFRU5 | 1,155,967 | 1,148,923 | +7,044 | Greens | +20,662 |

SFRZ5 | 1,188,604 | 1,180,957 | +7,647 | Blues | -8,505 |

SFRH6 | 929,118 | 926,768 | +2,350 |

|

|

SFRM6 | 876,419 | 877,743 | -1,324 |

|

|

SFRU6 | 781,911 | 786,849 | -4,938 |

|

|

SFRZ6 | 856,753 | 869,823 | -13,070 |

|

|

SFRH7 | 664,110 | 664,676 | -566 |

|

|

SFRM7 | 622,412 | 598,340 | +24,072 |

|

|

SFRU7 | 428,905 | 432,542 | -3,637 |

|

|

SFRZ7 | 403,985 | 403,192 | +793 |

|

|

SFRH8 | 300,772 | 306,747 | -5,975 |

|

|

SFRM8 | 200,233 | 211,254 | -11,021 |

|

|

SFRU8 | 177,371 | 171,103 | +6,268 |

|

|

SFRZ8 | 168,882 | 166,659 | +2,223 |

|

|

IRAN: Tasnim-Tehran Uses Hypersonic Missiles In Latest Strikes On Israel

Semi-official Iranian outlet Tasnim reports that the Islamic Revolutionary Guards Corps (IRGC) Aerospace Force is using hypersonic missiles in its attacks on Israel. Tasnim claims that "In this morning's operation, several images were recorded of hypersonic missiles hitting targets in Tel Aviv and Haifa, showing that these missiles easily passed through Israel's anti-ballistic defense systems and hit the target. [These missiles] are equipped with a solid-fuel spherical engine warhead with a movable nozzle and the ability to maneuver and change course." Previously, the Israeli military has denied that Iran possesses hypersonic missiles or manoeuvrable warheads.

- The Iranian press has claimed that the use of such missiles will limit Israel's ability or willingness to continue the escalating conflict. Security analyst Michael Horowitz writes on X that this may not be the case: "Notable development: Israel appears to have successfully used the "David's sling" air defense system to intercept Iranian ballistic missile. The system was not initially designed to intercept these types of missiles. The David's Sling is part of the "middle" tier out of a three tier system that goes from Iron Dome for low-altitude threats, to Arrow-2/3 for high-altitude/exo-atmospheric threats."

- It is also unclear what level of stockpiles Iran has of these advanced 'Fattah-1' missiles. While Iran's stockpile of conventional ballistic missiles is believed to be large (in the tens of thousands) capable of maintaining an aerial barrage for weeks, the high-tech nature and high cost of the hypersonic missiles are likely to limit their numbers.

FOREX: EUR/JPY Makes Light Work of Key Resistance as Geopol Spillover Limited

- The USD has been unable to benefit from the more fraught geopolitical backdrop, slipping against all others in G10 in contrast with the initial market reaction to the first exchanges of missiles between Iran and Israel on Friday.

- The underperformance for the USD today may be tied to the more benign energy market early Monday. WTI and Brent crude futures are holding last week's rally but have stopped well short of another impulsive leg higher - a possible signal that markets see the ramifications for energy supply as limited at this stage, despite evidence of attack on some Iranian oilfields.

- In a similar fashion, JPY is underperforming. The uptrend in EUR/JPY persists, and the cross has shown to a new high today to comfortably clear horizontal resistance at ~166.69, opening 167.40.

- The quiet data schedule Monday should keep focus on the option expiry pipeline today: sizeable strikes at 145.00 ($4.9bln) in USD/JPY and E4.6bln at 1.1700 in EUR/USD could keep spot vol contained into the Monday cut.

OPTIONS: Expiries for Jun16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.3bln), $1.1450-65(E2.0bln), $1.1500(E1.9bln), $1.1565-80(E1.6bln), $1.1600(E1.5bln), $1.1700(E4.6bln)

- USD/JPY: Y145.00($4.9bln)

- AUD/USD: $0.6503-05(A$500mln), $0.6560-63(A$1.0bln)

EQUITIES: E-Mini S&P Back Above 20-Day EMA, Pullback Considered Corrective

The latest pullback in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5297.58. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would highlight a short-term top and signal scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5365.98, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 5990.75, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5882.88. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

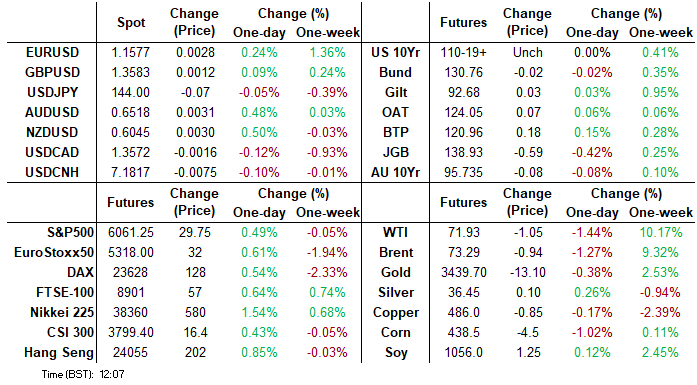

- Japan's NIKKEI closed higher by 477.08 pts or +1.26% at 38311.33 and the TOPIX ended 20.66 pts higher or +0.75% at 2777.13.

- Elsewhere, in China the SHANGHAI closed higher by 11.733 pts or +0.35% at 3388.729 and the HANG SENG ended 168.43 pts higher or +0.7% at 24060.99.

- Across Europe, Germany's DAX trades higher by 83.31 pts or +0.35% at 23599.84, FTSE 100 higher by 28.18 pts or +0.32% at 8878.8, CAC 40 up 51.83 pts or +0.67% at 7736.8 and Euro Stoxx 50 up 24.5 pts or +0.46% at 5315.14.

- Dow Jones mini up 197 pts or +0.47% at 42408, S&P 500 mini up 33.75 pts or +0.56% at 6013, NASDAQ mini up 141 pts or +0.65% at 21785.25.

COMMODITIES: Continuation Higher for WTI Futures Would Expose $80 Handle

WTI futures traded sharply higher last week and Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $68.49, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and this week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3262.2, the 50-day EMA.

- WTI Crude down $0.22 or -0.3% at $72.92

- Natural Gas up $0.11 or +2.99% at $3.687

- Gold spot down $16.91 or -0.49% at $3415.42

- Copper up $1.45 or +0.3% at $488.45

- Silver up $0.12 or +0.32% at $36.4139

- Platinum up $17.77 or +1.45% at $1245.79

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/06/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/06/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 17/06/2025 | 0600/0800 | ** | Unemployment | |

| 17/06/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note |