MNI US MARKETS ANALYSIS - EUR Spooked by 20% Tariff Draft

Highlights:

- Markets still looking to get a measure of tariffs, with Wednesday event the focus

- Washington Post writes levy could be nearer 20%, according to draft proposals

- Equities already within range of yesterday's lows, keeping the near-term fragile

US TSYS: Steady Gains See TYA Take Another Step Closer To Bull Trigger

- Treasuries have slowly extended gains through both Asia and European hours and continue to probe recent highs.

- Modest gains over the past hour were helped by the Washington Post reporting around White House aides drafting a proposal for tariffs of around 20%.

- Cash yields are 2-4bp lower on the day, with 2s lagging declines ahead of some notable data releases including ISM manufacturing and JOLTS reports at 1000ET.

- 2Y yields at 3.865% for now remain above yesterday’s stabilization either side of the 3.85% level. 10Y yields meanwhile at 4.165% have easily pushed through yesterday’s 4.18-4.20%, with ytd lows seen at 4.104% on Mar 4.

- TYM5 trades close to a recent session high of 110-24+ ( + 17+) on solid overnight volumes of 455k.

- It has cleared tentative resistance at yesterday’s 111-22+ for another step closer to a bull trigger at 112-01 (Mar 4 high) after which lies 112-13 (Fibo projections).

- Data: S&P Global US mfg PMI Mar final (0945ET), ISM mfg Mar (1000ET), JOLTS Feb (1000ET), Construction spending Feb (1000ET), Dallas Fed services Mar (1030ET)

- Fedspeak: Barkin on policy and economic outlook (0900ET, text tbd)

- Bill issuance: US Tsy $70B 6W bill & $50B 14D CMB auctions (1130ET)

STIR: Fed Rate Path Towards Dovish End Of Recent Ranges

- Fed Funds implied rates are unchanged to a little lower on the day for late 2025 meetings (-2bp for Dec) with some contained risk off moves following the Washington Post reporting around White House aides drafting a proposal for tariffs of around 20%.

- Cumulative cuts from 4.33% effective: 5bp May, 20.5bp Jun, 37.5bp Jul, 54.5bp Sep and 78bp Dec.

- The 78bp of cuts priced for 2025 is off yesterday’s 81bp although still towards the dovish end of recent ranges.

- US data should receive attention today, especially March ISM mfg and February JOLTS at 1000ET, along of course with further headline watch ahead of Apr 2 tariff announcements.

- Scheduled Fedspeak looks unlikely to move the needle, with Richmond Fed’s Barkin (non-voter) speaking on policy and the economic outlook at 0900ET after yesterday’s CNBC appearance. His base case is that it will take a while for clarity around tariffs, and he’s nervous about inflation and employment. He’s in no hurry to cut rates and doesn’t see now being a time for forward guidance.

- NY Fed’s Williams (permanent voter) yesterday told Yahoo Finance that he wants to watch data to see the impact of tariffs on prices. The Fed needs to keep an open mind on how long tariff impacts will last with there definitely a risk of higher inflation, whilst pledging to keep long-term inflation expectations anchored. His baseline view is that inflation will be relatively stable but risks to growth and inflation are both very important.

US TSY FUTURES: Long Setting Further Out The Curve Dominates On Monday

OI data points to a mix of net long cover (TU), short setting (FV), short cover (TY) and long setting (UXY, US & WN) during yesterday’s twist flattening of the curve, with the long setting across UXY-WN providing the most meaningful adjustment.

| 31-Mar-25 | 28-Mar-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,914,900 | 3,913,083 | +1,817 | +69,993 |

FV | 6,530,172 | 6,547,779 | -17,607 | -769,392 |

TY | 4,900,059 | 4,939,314 | -39,255 | -2,539,454 |

UXY | 2,317,862 | 2,304,879 | +12,983 | +1,167,959 |

US | 1,824,574 | 1,800,971 | +23,603 | +3,127,842 |

WN | 1,803,402 | 1,789,617 | +13,785 | +2,694,283 |

|

| Total | -4,674 | +3,751,231 |

STIR: Net Long Cover Most Prominent In SOFR Futures On Monday, Some Shorts Set

OI data points to net long cover providing the most meaningful positioning swings through the SOFR greens on Monday, although some sizeable rounds of net short setting were also observed (most notably in SFRM5).

| 31-Mar-25 | 28-Mar-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,184,946 | 1,176,188 | +8,758 | Whites | -21,652 |

SFRM5 | 1,339,213 | 1,299,968 | +39,245 | Reds | -3,830 |

SFRU5 | 933,926 | 988,251 | -54,325 | Greens | -43,970 |

SFRZ5 | 1,084,708 | 1,100,038 | -15,330 | Blues | -2,701 |

SFRH6 | 650,227 | 643,893 | +6,334 |

|

|

SFRM6 | 690,706 | 680,632 | +10,074 |

|

|

SFRU6 | 628,954 | 637,794 | -8,840 |

|

|

SFRZ6 | 785,437 | 796,835 | -11,398 |

|

|

SFRH7 | 491,477 | 507,456 | -15,979 |

|

|

SFRM7 | 470,802 | 488,042 | -17,240 |

|

|

SFRU7 | 314,041 | 318,777 | -4,736 |

|

|

SFRZ7 | 427,353 | 433,368 | -6,015 |

|

|

SFRH8 | 230,364 | 232,386 | -2,022 |

|

|

SFRM8 | 191,123 | 190,300 | +823 |

|

|

SFRU8 | 128,687 | 130,602 | -1,915 |

|

|

SFRZ8 | 135,854 | 135,441 | +413 |

|

|

TARIFFS: Trump's Liberation Day Tariffs - What to Expect?

- What we know: Trump, with his cabinet in attendance, will announce the details of his reciprocal tariff plan at 1500ET/2000BST tomorrow, aiming to address "unfair" trade practices with "country-based" tariffs. Sectoral duties will still be implemented, but will not be the focus Wednesday - so don't expect details on Autos, copper, pharma, or otherwise. There will be "no exemptions at this time" - meaning there appears to be little room for bilateral negotiation at this stage.

- What we don't know: Which countries will be targeted, what the outright levies will be, and when they will be effective by. It is also not clear whether tariffs will 'stack' - e.g. whether Aluminium exports to the US from a tariffed country will be double charged. It is also unknown whether goods deemed compliant under USMCA, or other trade agreements, will be exempt, or subject to an outright tariff.

- What does the market expect? There is no real consensus on what the outright tariff % could be, however it's expected that those that maintain the largest relative trade surpluses with the US will be targeted most heavily (including, but not limited to, the EU, China, Mexico, Canada, Japan, South Korea). Average levies are expected to range between 10-20%, but outsized risk remains - particularly considering Trump's recent threats to charge as much as 50% tariffs on Canadian goods in the short-lived rift over Ontario's electricity surcharges.

TARIFFS: WaPo-WH Draft Proposal Has Tariffs ~20% On 'At Least Most Imports'

The Washington Post reports that "White House aides have drafted a proposal to impose tariffs of around 20 percent on at least most imports to the United States, three people familiar with the matter said,". While the looming 'reciprocal' tariffs to be imposed from April 2 have been top of the news cycle for some time, there has been very little concrete information about their nature. As such, these comments come as some of the first indications about what level the levies might settle at.

- WaPo: "Wilbur Ross, who served as commerce secretary during Trump’s first term, said the White House is considering setting one flat rate on imports of between 15 percent and 25 percent. He said administration officials are wrestling with the complicated question of how to change existing tariffs on countries that are higher or lower than that amount to align with the new target. "

- Ross adds that “there are some people in the White House who are undoubtedly more extreme” than Treasury Sec. Scott Bessent and Commerce Sec. Howard Lutnick, who are seen to support different rates for different countries. Highlights it is Trump who will make the undisputed final call.

- The story cautions that despite the draft proposal mentioned, there is no final decision yet. The main options remain either raising tariffs on almost all products from almost all countries in an effort to ramp up the quantity of funds brought in by such measures. The other is applying different rates to different countries, ensuring full reciprocity.

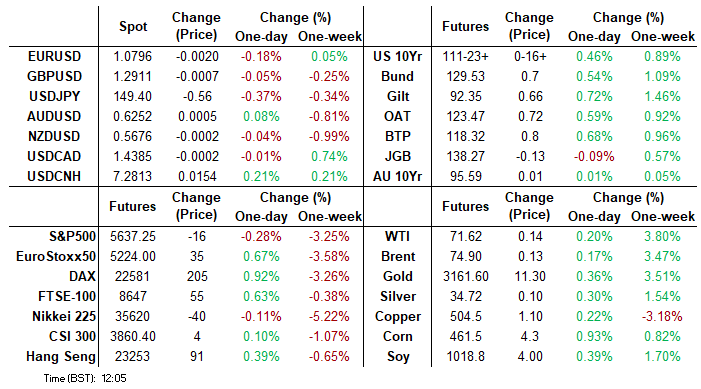

CROSS ASSET: Equities Slip Further on Washington Post Headline, Near Support

Stocks holds the entirety of the move lower triggered by the Washington Post story - the "around 20 per cent on at least most imports to the United States" is at the sharper end of expectations. We wrote earlier that while there is no real consensus on the tariff %, the average levy is expected between 10 - 20%, hence the market move (EUR, stocks lower) on that headline.

- E-mini S&P is falling further at typing: 5619.25 marks the first support and overnight low, ahead of the more major 5533.75 pullback low and bear trigger.

- EUR/USD, however, has bounced off headline-triggered lows, potentially stemming from the article's mention that "several options", potentially less extreme than a blanket tariff, remain on the table.

FRANCE: RN's Bardella Leads In 1st Round Poll Following Le Pen's Election Ban

A snap presidential election poll from Harris Interactive shows far-right Rassemblement National (RN, National Rally) leader Jordan Bardella leading in a hypothetical first-round if he becomes the RN candidate. This comes after presumptive RN presidential candidate Marine Le Pen was barred from seeking political office for five years as part of her sentence for misappropriation of funds, a ruling that has sparked outrage from Le Pen's supporters and contemporaries in France and abroad.

- Bardella has served as RN president since 2022 and has been viewed as the heir apparent to Le Pen. It was generally assumed that Le Pen would run in 2027, given that at that point Bardella will be just 31 years of age, before handing over the mantle.

- This first poll (which of course should not be taken as the indication of a trend) shows Bardella with 35-36% support compared to 23-25% for Edouard Philippe, the mayor of Le Havre, who is seen as the frontrunner to lead the centrist Ensemble coalition. Perennial far-left candidate Jean-Luc Melenchon sits far back on 13% in both polls.

- A separate poll from Elabe showed that among all French voters and RN supporters, Bardella is viewed as having as good as/a better chance of winning the presidency than Le Pen. Among all voters, 67% said Bardella has as good/a better chance of winning the presidency, compared to 30% saying only Le Pen could win for RN. This shifted to an 81%-18% split among RN voters.

Chart 1. Opinion Poll, "Regarding the impossibility of Marine Le Pen running in the 2027 presidential election and the possibility that she will be replaced by Jordan Bardella, which of the following opinions are you closest to?", %

Source: Elabe, MNI. Fieldwork: 31 March (after Le Pen conviction), 1,008 respondents.

FOREX: USD Index Holds Ground in Penultimate Pre-Liberation Session

- The USD Index holds above the 104.00 handle in the penultimate session before Wednesday's tariff announcement, with the near-term trajectory of the USD still subject to risk appetite and the market's inability to price the global trade picture. This leaves the greenback subject to the whims of equities - which are mixed so far Tuesday having bounced off the pullback lows. This still leaves the e-mini S&P within range of support layered between 5533.75-5559.75.

- Overnight FX vols are seeing some support - but the contracts won't fully capture Trump's tariff announcement until tomorrow - leaving markets still scratching their heads over quantifying the specific risks this week.

- Scandinavian currencies are modestly outperforming in early trade, undeterred by some uninspiring PMI manufacturing prints from Norway and Sweden. The single currency is off overnight lows, having found demand into the 1.0800 handle, but the bounce is shallow at this stage - contained by the slightly soft Eurozone Core CPI reading: 2.4% vs. Exp. 2.5%.

- US JOLTS job openings data is the Tuesday highlight, with the ISM Manufacturing release set to follow. Markets expect both metrics to deteriorate slightly over the month, and will be the final focus ahead of Wednesday's Rose Garden event, at which Trump is expected to unveil the full details of America's suite of tariffs to be used to rebalance global trade in the US' favour.

EQUITIES: E-Mini S&P Briefly Pierces Key Support and Bear Trigger

- Eurostoxx 50 futures traded lower Monday resulting in a breach of key support at 5229.00, the Mar 11 low. The print below this support undermines a bullish theme and signals scope for a deeper retracement. Note that the 5200 handle has also been cleared, opening 5079.00, the Feb 3 low. It is still possible that recent weakness is part of a broader correction. Initial firm resistance to watch is 5343.17, the 20-day EMA.

- S&P E-Minis maintains a softer tone following recent bearish price action. Attention is on key support and the bear trigger at 5559.75, the Mar 13 low. It has been pierced, a clear break of it would confirm a resumption of the downtrend that started Feb 19, and open 5483.30, a Fibonacci projection. MA studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term resistance has been defined at 5837.25, the Mar 25 high.

COMMODITIES: Sharp Move Higher for WTI Futures Monday Undermines Bearish Theme

- WTI futures traded sharply higher Monday. This undermines the medium-term bearish condition and instead signals scope for a continuation higher near-term. The rally has exposed the next key resistance at $72.91, the Feb 11 high. Clearance of this level would strengthen the bullish theme. On the downside, initial firm support to watch lies at $68.78, the 20-day EMA. A breach of this level would signal a potential reversal.

- The trend condition in Gold is unchanged, it remains bullish. The latest rally highlights a bullish start to this week’s session and confirms a continuation of the primary uptrend. The rally also once again, highlights fresh all-time highs for the yellow metal. Sights are on the $3151.5, a Fibonacci projection. Support to watch lies at $3004.9, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 01/04/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/04/2025 | 1230/1430 | ECB's Lagarde At AI Conference | ||

| 01/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 01/04/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 01/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/04/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/04/2025 | 1400/1000 | * | Construction Spending | |

| 01/04/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 01/04/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 01/04/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 01/04/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 01/04/2025 | 1630/1830 | ECB's Lane At AI Conference | ||

| 02/04/2025 | 0030/1130 | * | Building Approvals | |

| 02/04/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 02/04/2025 | 1030/1230 | ECB's Schnabel At SciencesPo Conference | ||

| 02/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 02/04/2025 | 1215/0815 | *** | ADP Employment Report | |

| 02/04/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/04/2025 | 1405/1605 | ECB's Lane At AI Conference | ||

| 02/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 02/04/2025 | 2030/1630 | Fed Governor Adriana Kugler | ||

| 03/04/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 03/04/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |