MNI US MARKETS ANALYSIS - Curve Twist Steeper into Payrolls

Highlights:

- US curve sits twist steeper ahead of payrolls

- Markets expect job gains of 104k over July, unemployment rate expected to rise 0.1ppts

- First Fed dissenters expected to issue statements arguing in favour of cuts

US TSYS: Twist Steeper Ahead Of Payrolls and ISM Manufacturing

- Treasuries trade twist steeper although with the pivot from 5s onwards as only 2s sits firmer on the day in contained moves ahead of the July nonfarm payrolls report.

- There don’t appear to be fresh catalysts for the steepening over the past hour, in moves that appear more likely flow-driven, with curves still on net flatter since Wednesday’s patient Fed rhetoric.

- President Trump yesterday announced new tariffs, including a 10% global minimum and 15% or higher duties for countries with trade surpluses with the US for smaller countries without specific trade deals. He will also impose a 35% tariff on Canadian non-USMCA goods.

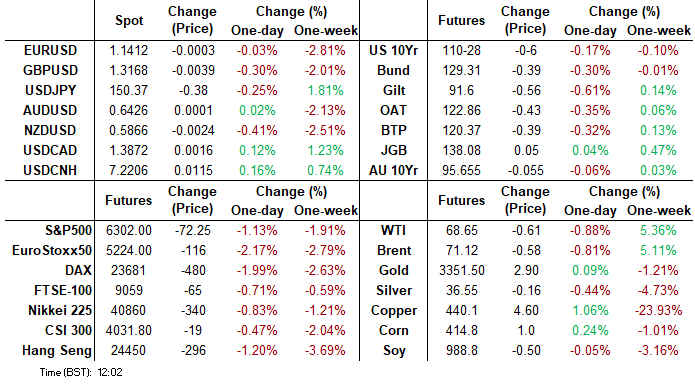

- Cash yields range from 0.5bp lower (2s) to 3bps higher (20s/30s).

- 2s10s at 44.7bp (+2.6bp), further away from yesterday’s low of 40.3bp but still below pre-FOMC levels of ~47bp.

- 5s30s at 95.3bp (+2.2bp), above yesterday’s low of 92.1bp but also below pre-FOMC levels of 96-97bps.

- TYU5 trades at 110-28 (-06) vs an earlier low of 110-26+, extending yesterday’s losses but holding above Tuesday’s low of 110-24. Cumulative volumes are moderate at 295k.

- A patient Powell on Wednesday helpeda sizeable move away from a key resistance at 111-14+ (Jul 22/30 highs), bringing closer to support at 110-19+ (Jul 24 low) after which lies 110-08+ (Jul 14/16 lows).

- Data: Nonfarm payrolls Jul (0830ET), S&P Global US mfg PMI Jul final (0945ET), ISM mfg Jul (1000ET), U.Mich consumer survey Jul final (1000ET), Construction spending Jun (1000ET)

- Fedspeak: Hammack on Bloomberg TV (0910ET), Bostic on CNBC (1030ET) & Bowman/Waller dissent statements at some point – see STIR bullet

- There’s little reaction to Trump’s latest attack on Fed Chair Powell in an early morning Truth Social post but it clearly doesn’t detract from the recent steepening: “Jerome “Too Late” Powell, a stubborn MORON, must substantially lower interest rates, NOW. IF HE CONTINUES TO REFUSE, THE BOARD SHOULD ASSUME CONTROL, AND DO WHAT EVERYONE KNOWS HAS TO BE DONE!”

STIR: Payrolls Looms Large Plus First Post-FOMC Fedspeak Including Dissents

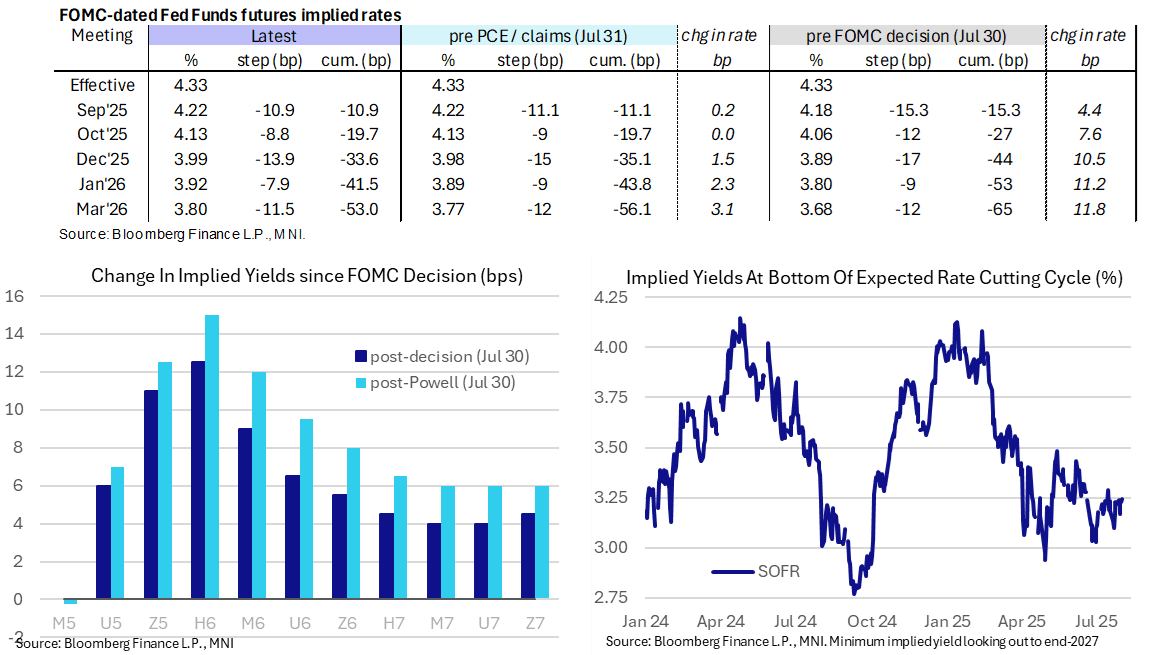

- Fed Funds implied rates are only 0.5bp lower overnight for near-term FOMC meetings, holding the week’s shift higher driven by Fed Chair Powell’s patient rhetoric in Wednesday’s press conference.

- Cumulative cuts from 4.33% effective: 11bp Sep (vs 15.5bp pre FOMC), 19.5bp Oct, 34bp Dec (vs 44bp), 42bp Jan and 53.5bp Mar (vs 65bp).

- The SOFR curve has steepened modestly overnight but doesn’t materially change the post-FOMC flattening.

- The SOFR implied terminal yield of 3.245% (SFRH7, +1.5bp on the day) last closed higher on Jul 15 but remains within the 3.1-3.3% range seen through July.

- Front rate moves are contained ahead of the July nonfarm payrolls report at 0830ET which is also followed by ISM manufacturing for July at 1000ET. We see greater sensitivity to a dovish NFP report – see the MNI Payrolls Preview: Hidden PDF

- Cleveland Fed's Hammack (’26 voter, hawk) is the first scheduled post-FOMC speaker at 0910ET on Bloomberg TV before Atlanta Fed’s Bostic (non-voter) on CNBC at 1030ET.

- We also expect dissent statements from Bowman and Waller. There is no set time here although for reference Waller's March statement came at 1000ET and Bowman's September statement at 1300ET. However, Waller’s in particular shouldn’t be a surprise, his speech on July 17 (The Case For Cutting Now) explicitly laid his arguments out, and Bowman’s dissent was also widely expected since her speech on Jun 23 (Unintended Policy Shifts and Unexpected Consequences).

SOFR: Fresh Position Setting Dominated In Futures On Thursday

OI data points to a mix of net long (greens & blues) and short (whites & reds) setting dominating across the SOFR futures strip on Thursday, with only 4 rounds of net cover detected through the blues.

| 31-Jul-25 | 30-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,264,162 | 1,255,816 | +8,346 | Whites | +69,722 |

SFRU5 | 1,327,485 | 1,291,339 | +36,146 | Reds | +48,867 |

SFRZ5 | 1,326,273 | 1,342,563 | -16,290 | Greens | +45,513 |

SFRH6 | 1,091,519 | 1,049,999 | +41,520 | Blues | +2,819 |

SFRM6 | 894,208 | 862,852 | +31,356 |

|

|

SFRU6 | 847,985 | 835,151 | +12,834 |

|

|

SFRZ6 | 925,329 | 932,881 | -7,552 |

|

|

SFRH7 | 723,222 | 710,993 | +12,229 |

|

|

SFRM7 | 710,806 | 692,888 | +17,918 |

|

|

SFRU7 | 532,979 | 516,894 | +16,085 |

|

|

SFRZ7 | 476,762 | 462,754 | +14,008 |

|

|

SFRH8 | 330,044 | 332,542 | -2,498 |

|

|

SFRM8 | 250,177 | 248,494 | +1,683 |

|

|

SFRU8 | 201,107 | 199,537 | +1,570 |

|

|

SFRZ8 | 206,749 | 207,355 | -606 |

|

|

SFRH9 | 145,091 | 144,919 | +172 |

|

|

US TSY FUTURES: Full range Of Positioning Swings During Thursday's Twisting

OI data points to a variety of positioning adjustments on Thursday:

- Net short setting in TU.

- Net long cover in FV.

- Net short cover in TY, US & WN.

- Net long setting in UXY.

- The net short cover across TY, US & WN futures provided the most meaningful DV01 equivalent adjustment.

| 31-Jul-25 | 30-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,532,570 | 4,451,292 | +81,278 | +2,983,872 |

FV | 6,959,364 | 6,975,185 | -15,821 | -671,682 |

TY | 4,931,325 | 4,953,659 | -22,334 | -1,459,321 |

UXY | 2,425,392 | 2,424,893 | +499 | +43,166 |

US | 1,740,124 | 1,765,130 | -25,006 | -3,436,179 |

WN | 1,949,093 | 1,953,917 | -4,824 | -861,072 |

|

| Total | +13,792 | -3,401,215 |

INDIA: US Team To Visit For FTA Talks 24 Aug As 25% Tariffs Confirmed By Trump

Reuters reports that according to an unnamed gov't source, the Indian gov't has engaged with the US for further trade talks, with a US delegation set to visit Delhi on 24 August. These will be the sixth round of talks on a formal bilateral trade agreement, with NDTV reporting in late July that an announcement on an interim deal could be announced as soon as September or October.

- Reuters source also claims that the gov't expects around USD40bln of Indian exports to be hit by the US' 25% 'reciprocal' tariffs confirmed by President Donald Trump on 31 July, and set to come into force by 7 August. The Trump administration has also indicated an "unspecified penalty" on India for continuing its purchases of Russian hydrocarbons.

- The scale of the reciprocal tariffs puts the US-Indian relationship in a tricky position. PM Narendra Modi was the first foreign leader to visit the White House following Trump's second inauguration, with Minister for External Affairs S. Jaishankar saying in March that “our relations with the US are probably at the best ever that they have been.”

- However, New Delhi may have been caught off guard by the hardline transactional nature of the US' stance on trade talks. The significant political power of India's agricultural sector, combined with the US viewing dairy imports as a particular sticking point (according to the Washington Post) could limit the prospect of a swift agreement being reached.

SWITZERLAND: Gov't Does Not Expect 39% Tariffs To Hit Pharma Sector

A spox for the Federal Department of Economic Affairs has told Reuters that the gov't does not expect the 39% 'reciprocal' tariffs to come into effect from 7 August on Swiss exports to the US to include the pharmaceuticals sector. The 39% rate puts Switzerland among the most heavily-penalised nations worldwide under the 'reciprocal' tariff regime, behind only Brazil (with whom's leader US President Donald Trump is involved in a bitter verbal spat), Syria, Laos and Myanmar.

- This comes after the Federal Council posted on X that the tariffs come despite Switzerland's "very constructive stance", adding that Bern "continues to seek a negotiated solution" and "will analyse the new situation and decide on the next steps."

- The US accounted for 18.6% of total Swiss exports in 2024, with the large majority (60%) of this being pharmacueticals, followed by machinery and metalworking (20%) and watches (8%).

- The expectation of a separate agreement on pharma does not necessarily mean a major reduction in tariffs. Speaking to CNBC earlier in the week, US Commerce Secretary Howard Lutnick said, "Basically, if you are not building your plant in America where we pay for pharmaceuticals, you are going to pay a massive tariff, because why should we pay for your drugs? And you make them overseas and you make your money overseas? At least if we’re going to pay for your drugs, you’re going to build them in America." Lutnick claimed that a plan would be announced within two weeks.

USD: The EUR is the early mover

- A mixed picture for the Dollar overnight against G10s, the CHF was down 0.21% at one point following reports that the US will be putting a 39% Tariffs on imports from Switzerland.

- USDCHF edged higher to print a 0.8146, but this Weeks high and the July high of 0.8151 remains untested.

- AUD was the early best performer, some overnight Desks reported some exporter demand, but the AUDUSD printed low overnight was its lowest since the 23rd June, after Market participants and Investors fully price a cut for the August meeting, on the back of the last Inflation Data.

- The September RBA meeting sees around 31% odd of a cut versus 42% at one point this Week.

- The Early mover has actually been the EUR, which is now the best performer, but the Currency is also seeing some small broader buying, testing intraday high against the CNH, AUD, NOK, USD, CAD and the NOK.

- CEEs seems to somewhat benefit, PLN, CZK and HUF hover at session high vs the EUR.

OPTIONS: Expiries for Aug01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400-05(E1.7bln), $1.1425-30(E956mln), $1.1440-60(E2.2bln), $1.1500(E845mln)

- USD/JPY: Y146.00($1.4bln), Y147.00($1.6bln), Y148.15-35($729mln), Y149.00($574mln), Y150.00($932mln), Y151.00($627mln)

- USD/CAD: C$1.3450-70($1.2bln), C$1.3780-00($592mln), C$1.3930-50($540mln)

- USD/CNY: Cny7.3000($819mln)

EQUITIES: Trend Condition in Eurostoxx Futures Bullish, S/T Weakness Corrective

- The trend condition in Eurostoxx 50 futures is bullish and S/T weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of it would strengthen a bearish threat and expose the reversal trigger at 5194.00, the Jun 23 low. For bulls, a stronger resumption of gains would refocus attention on 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- The trend set-up in S&P E-Minis remains bullish and short-term weakness is considered corrective. A fresh cycle high this week maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6189.50. Support at the 20-day EMA is at 6333.64.

COMMODITIES: WTI Futures Holding Onto the Bulk of This Week’s Gains

- WTI futures are holding on to this week’s gains. The climb marks an extension of the current corrective cycle. $69.41, the 50.0% retracement of the Jun 23-24 downleg, has been cleared. A continuation higher would open $70.96 next, the 61.8% retracement point. On the downside, support to watch is the 50-day EMA, at $65.37. The average has been pierced, a clear break of it would expose $58.17, the May 30 low.

- Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3319.9, the 50-day EMA. A clear break of this level signals scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

| Date | GMT/Local | Impact | Country | Event |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/08/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 01/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |