MNI US MARKETS ANALYSIS - Curve Twist Steeper into Fedspeak

Highlights:

- Treasury curve sits mildly twist steeper Friday; markets on watch for first post-FOMC Fedspeak

- Gold, Silver again charge higher

- USD Index in consolidation mode, awaiting Fed drivers

US TSYS: Modestly Twist Steeper, TY Bear Threat Still Present

Treasuries trade modestly twist steeper, with the front end keeping to tight ranges ahead of the resumption of Fedspeak after Wednesday’s FOMC decision. Upcoming focus will likely be on next week’s heavy data calendar including NFP and retail sales on Tuesday before CPI on Thursday.

- Cash yields range from 0.6bp lower (3s) to 2.1bp higher (20s and 30s).

- Curves have extended post-FOMC steepening, with 2s10s at 62.8bps vs ~57bps pre-FOMC and 5s30s at 108.6bps vs ~101bps pre-FOMC.

- 5s30s will start to be watched more closely if it pushes closer towards the Dec 3 two-and-a-half month high of 111bp.

- TYH6 trades at 112-10+ (-04) on thin cumulative volumes of 205k.

- It sits within some notable technical levels, with resistance seen at 112-13 (Dec 11 high and 20-day EMA) but a bear threat still present with a bear trigger at 111-29 (Dec 10 low).

- Data: Business formation statistics (1000ET)

- Fedspeak: Paulson (0800ET), Goolsbee (0830ET), Hammack (0830ET), Goolsbee (1035ET) and potential for Goolsbee & Schmid dissenting statements at some point – see FED bullet.

- Politics: Trump in swearing-in ceremony (1330ET), Trump in bill signing ceremony (1500ET)

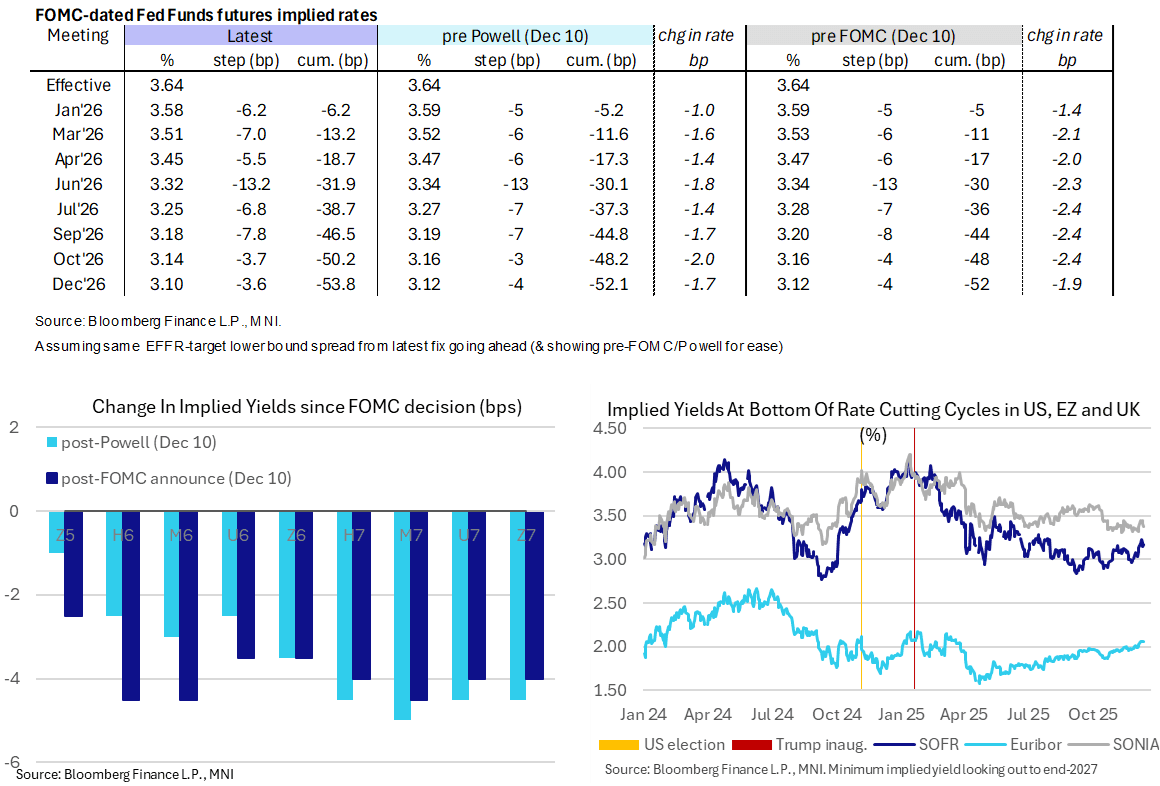

STIR: Next Fed Cuts Seen In June and Oct, Regional Presidents Reappointed

- Fed Funds implied rates are between 0-1bp lower on the day for 2026 meetings, pricing a next 25bp cut in June (with the new Fed chair) and then another 25bp cut fully priced for October.

- Cumulative cuts from an assumed 3.64% effective: 6bp Jan, 13bp Mar, 18.5bp Apr, 32bp Jun, 46.5bp Sep and 54bp Dec.

- SOFR futures in contrast are up to 2 ticks lower on the day looking to end-2027, nudging the terminal implied yield up to 3.165% (S6 and H7). For recent context, Tuesday closed at 3.225% for the highest close since July but it holds comfortably higher than the 15bp higher than in late November after NY Fed's Williams had set up this week's cut.

- Today sees a heavy resumption of Fedspeak, all from those who either definitely or likely objected to Wednesday's 25bp cut – see FED bullet.

- Yesterday saw an important announcement that the Federal Reserve’s Board had unanimously reappointed 11 of the 12 regional presidents to another 5 year term which had been due to expire on Feb 28. (The 12th is Atlanta's Bostic who had already announced his retirement.) It limits potential fallout from the Gov Cook lawsuit as her removal would have given greater sway when it came to a decision on regional president terms in the event that they were still outstanding.

- That said, we wouldn’t rule out further pressures here as changes can still be made with Board approval. For instance, leading contender for next Fed Chair Hassett supports Tsy Sc Bessent’s plan to impose a rule that regional presidents must have lived in their district for at least three years, a criteria that three currently don’t meet.

FED: Hawkish Or At Least Patient Fedspeak To Kickstart Post-FOMC Period

Today sees a resumption of Fedspeak starting with those who either definitely or likely objected to Wednesday's cut.

- 0800ET – Philly Fed’s Paulson (’26 voter) speaks on the economic outlook (text + Q&A). We suspect she was likely one of the six dots who objected to a cut this week with their dot plot choice, but any indications on 2026 view would be more notable having talked on an increasingly high bar to cutting as the Fed approaches a level where policy starts to be accommodative. She had described the higher unemployment rate of 4.44% in September as still being in the “neighborhood of full employment” and generally viewed the data as encouraging. "On the margin, I’m still a little more worried about the labor market than I am about inflation, but I expect to learn a lot between now and the next meeting." We watch for any indications of what she learned on the latter.

- 0830ET – Cleveland Fed’s Hammack (’26 voter) was very likely one of the soft dissenters for this week and we suspect she’s also likely one of the 3 dots who would have preferred to have kept rates on hold at previous levels through 2026 as well. She said Nov 20: “Inflation has been running above the Fed's 2% objective for four and a half years. Lowering interest rates to support the labor market risks prolonging this period of elevated inflation, and it could also encourage risk-taking in financial markets”.

- Chicago Fed’s Goolsbee (’25 voter, next voting ’27) is likely to publish a dissenting statement at some point today but failing that, he speaks on CNBC at 0830ET before appearing at an economic outlook symposium at 1035ET (just Q&A). He is the least hawkish of the dissenters (soft or otherwise) preferring a hold, having indicated beforehand that he objected to the near-term move amidst a data fog and that he clearly still sees rate cuts over the medium-term.

- Kansas City Fed’s Schmid (’25 voter, technically next set to vote in 2028) is also likely to publish a second dissenting statement. His October statement argued that he didn’t see a rate cut doing much to address stresses in the labor market that were likely arising primarily from structural changes in technology and demographics. He had also since warned that inflation is too high and that rate cuts could put the Fed’s commitment to 2% inflation in question.

STIR: Risks Of Dovish Counter Around ECB

This week’s hawkish repricing in the EUR STIR space has been well-documented, after Executive Board member Schnabel outlined her comfort with markets pricing the next rate move from the Bank as a hike.

- ECB-dated OIS now prices 7-8bp of hikes for ’26, with odds of any further easing withdrawn post-Schnabel.

- While the balance of risks has clearly shifted since the ECB deemed monetary policy to be “in a good place”, questions over the medium-term strength of the Eurozone economy and path of inflation remain evident.

- We have already noted that ongoing deployment of the “in a good place” phrase at next Thursday's post-decision press conference could encourage markets to price a flatter hiking cycle.

- A reminder that our policy team’s latest sources piece noted that December meeting communication will seek to reinforce two-way risks around the policy rate.

- Characterisation of the updated core inflation projections, which are expected to undershoot the 2% target in 2026 and 2027, will be key to the market reaction.

- Elsewhere, ECB President Lagarde recently suggested that the Bank will likely revise its GDP projections higher, so that should be discounted by markets at this stage. Also note that the scale of any upward revision is expected to be relatively negligible.

- Accordingly, various sell-side names have shown interest in received EUR STIR positions as cheap downside hedges “in case something goes wrong”.

- Commerzbank have noted that “while the monetary policy of the ECB is largely independent of the Fed, the strengthening euro puts more question marks behind the rate hike the market has begun speculating about for next year. Together with unwarranted real yield tightening at the long end and lower 2027 inflation projections, we consider 2026 Euribor and €STR forwards attractive ahead of next week's ECB meeting”.

SOFR: Net Long Setting Dominated On Thursday

OI data points to net long setting dominating as SOFR futures ticked higher on Thursday, as the post-FOMC dovish adjustment extended a little.

- Net short cover was seen in 3 of the front 4 contracts, although the net swings in those contracts was comfortably outweighed by net long setting in SFRZ5.

- Outside of the whites, net long setting was seen in 10 of the next 12 contracts.

| 11-Dec-25 | 10-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,289,492 | 1,291,916 | -2,424 | Whites | +64,876 |

SFRZ5 | 1,716,715 | 1,643,590 | +73,125 | Reds | +10,178 |

SFRH6 | 1,416,963 | 1,420,444 | -3,481 | Greens | +21,949 |

SFRM6 | 1,113,577 | 1,115,921 | -2,344 | Blues | +18,902 |

SFRU6 | 1,184,561 | 1,175,510 | +9,051 |

|

|

SFRZ6 | 1,153,289 | 1,169,878 | -16,589 |

|

|

SFRH7 | 876,409 | 856,418 | +19,991 |

|

|

SFRM7 | 768,556 | 770,831 | -2,275 |

|

|

SFRU7 | 811,784 | 804,909 | +6,875 |

|

|

SFRZ7 | 828,996 | 828,364 | +632 |

|

|

SFRH8 | 453,293 | 444,052 | +9,241 |

|

|

SFRM8 | 407,619 | 402,418 | +5,201 |

|

|

SFRU8 | 384,546 | 376,896 | +7,650 |

|

|

SFRZ8 | 327,532 | 322,261 | +5,271 |

|

|

SFRH9 | 200,280 | 195,706 | +4,574 |

|

|

SFRM9 | 205,034 | 203,627 | +1,407 |

|

|

EFSF ISSUANCE: EFSF / ESM 2026 funding plans

- The EFSF / ESM have confirmed their funding plans for 2026 (which match the provisional numbers published alongside their 2025 funding plan last year).

- EFSF 2026: E18.5bln (down from the E21.5bln in 2025). The 2027 estimate is E18.5bln.

- ESM 2026: E7.0bln (in line with the E7.0bln in 2025). The 2027 estimate is E6.5bln.

The ESM has also confirmed it will continue with 3/6-month bill auctions on the

first (3-month) and third (6-month) Tuesdays of each month through H1-26.

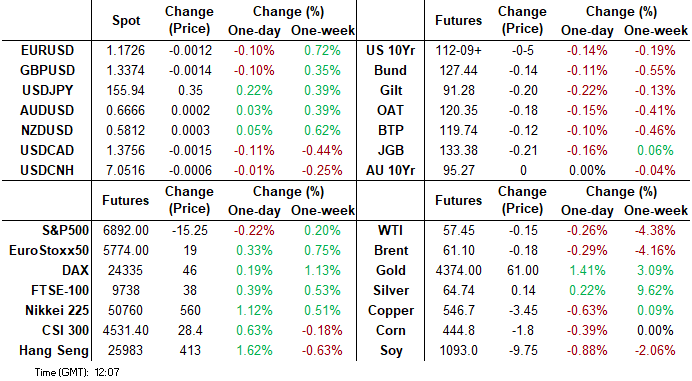

FOREX: DXY Consolidating Recent Weakness, USDCAD Extends Bearish Theme

- Having held resistance well across November, the USD Index’s pull lower has gathered downside momentum this week, assisted by a not so hawkish cut from the Fed and the associated constructive risk backdrop. This prompted the DXY to extend its three-week pullback to ~2.25% yesterday, with the DXY currently consolidating a 0.6% decline this week.

- CAD is an outperformer on Friday, extending the recent bull theme as the global FI hawkish repricing was particularly substantial for Canada. Expectations for BoC hikes through next year stand firm by now following stronger labour market data and a hawkish BoC meeting this week.

- This keeps the bear theme in USDCAD firmly intact as spot narrows the gap to 1.3727, the September 17 low. Short-term gains would be considered corrective and would allow an oversold condition to unwind, with initial firm resistance to watch is 1.3936, the 20-day EMA.

- Following yesterday's SNB decision, CHF this morning holds most gains seen over the past couple of sessions against a wide set of G10. USDCHF remains a key detriment of dollar weakness post FOMC. The pair narrowed in on clustered horizontal support into the 0.7829-78 area - marking the series of lows printed across Q3/Q4 this year.

- GBP has seen moderate pressure following the below-expectation October GDP figures. This led EURGBP to a 0.8775 overnight high, with recent gains signalling a possible reversal and the end of the corrective phase. Initial firm resistance to watch is unchanged at 0.8802, the Dec 2 high, while key short-term support has been defined at 0.8721, the Dec 9 low.

- The data calendar remains light for the rest of the day, with only Canada housing data being scheduled. Fedspeak is set to pick up, with Paulson, Hammack and Goolsbee appearing today. Goolsbee may be of particular focus as he was a hawkish dissenter in the FOMC earlier this week.

OPTIONS: Expiries for Dec12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.5bln), $1.1600(E629mln), $1.1700(E840mln)

- USD/JPY: Y154.00($614mln), Y155.00($1.3bln), Y156.00-15($1.2bln)

- GBP/USD: $1.3240-55(Gbp1.1bln), $1.3330(Gbp782mln), $1.3415(Gbp593mln)

- AUD/USD: $0.6650(A$897mln)

- USD/CAD: C$1.3780-00($1.6bln)

EQUITIES: Thursday's Gains Strengthen a Bull Theme for Eurostoxx Futures

- A bull cycle in Eurostoxx 50 futures remains intact and Thursday's gains strengthen a bull theme. Price is trading above the 20- and 50-day EMAs, and has cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5637.69, the 50-day EMA.

- A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high yesterday strengthens the bull theme. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. Sights are on the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support to watch is at 6823.86, the 20-day EMA.

COMMODITIES: Gold Narrows Gap to Key Resistance and Bull Trigger at $4381.50

- A bearish theme in WTI futures remains intact and the move down this week reinforces this theme. Note that moving average studies are in a bear-mode position, highlighting a dominant medium-term downtrend. A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Gold traded higher yesterday, reinforcing a bullish theme. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4060.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 12/12/2025 | 1300/0800 | Philly Fed's Anna Paulson | ||

| 12/12/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 12/12/2025 | 1330/0830 | * | Building Permits | |

| 12/12/2025 | 1330/0830 | ** | Wholesale Trade | |

| 12/12/2025 | 1330/0830 | Cleveland Fed's Beth Hammack | ||

| 12/12/2025 | 1535/1035 | Chicago Fed's Austan Goolsbee | ||

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |