MNI US MARKETS ANALYSIS - Curve Steeper into Tax Bill Vote

Highlights:

- Curve steepens further as markets prime for Big Beautiful Bill

- USD/JPY hits new pullback low before modest bounce into NY hours

- Weekly claims the data highlight, with ample Fedspeak due

US TSYS: Steepening Extends; Trump Bill Vote Before Claims and PMIs

- Treasuries have extended yesterday’s steepening, with the front end to belly firming (aided by -1.6% declines in WTI) but the long end consolidating yesterday’s sell-off.

- A weak 20Y auction, with a 1.2bp tail and a bid-to-cover falling to a low end of the range 2.46x after 2.63x prior, sparked a sharp sell-off with 30Y yields punching above the week’s earlier ytd highs.

- Today sees immediate focus on the passing of President Trump’s “big, beautiful bill”. The package is expected to pass after pressure from Trump and House Republican leadership yesterday won over hardline GOP conservatives who threatened to tank the bill, citing concerns over the deficit implications of the package.

- If the bill is passed, it will be handed to the Senate for the next stage of the process. Senate Majority Leader John Thune (R-SD) has said he wants to send the package to Trump's desk by July 4.

- Later on sees weekly jobless claims - covering a payrolls reference period for initial claims - and flash May PMIs. A 10Y TIPS auction is unlikely to elicit the same reaction as yesterday’s 20Y but weakness could still be of note.

- Cash yields are 0.6-2.5bp lower, with declines led by 5s and with 30s lagging. 30Y yields at 5.086% after 5.1072% overnight, a level that prior to Oct-Nov 2023 was last seen in 2007.

- 5s30s at 94.8bp having touched 96bp overnight in a move back closer to ytd highs of 100bps on May 1.

- TYM5 sits at 109-19+ (+03+) after yesterday’s clearance of 109-18+ (May 15 low), on solid cumulative volumes of 445k.

- The 109-13 overnight marked the latest step towards a key support at 109-08 (Apr 11 low). Resistance meanwhile is seen at 110-21+ (May 16 high).

- Data: Jobless claims (0830ET), Chicago Fed national activity Apr (0830ET), S&P Global US PMIs May prelim (0945ET), Existing home sales Apr (1000ET), KC Fed mfg index May (1100ET)

- Fedspeak: Barkin (0800ET), Williams (1400ET) – see STIR bullet.

- Coupon issuance: US Tsy $18B 10Y TIPS re-open auction (1300ET)

- Bill issuance: US Tsy $85B 4W & $75B 8W bill auctions (1130ET)

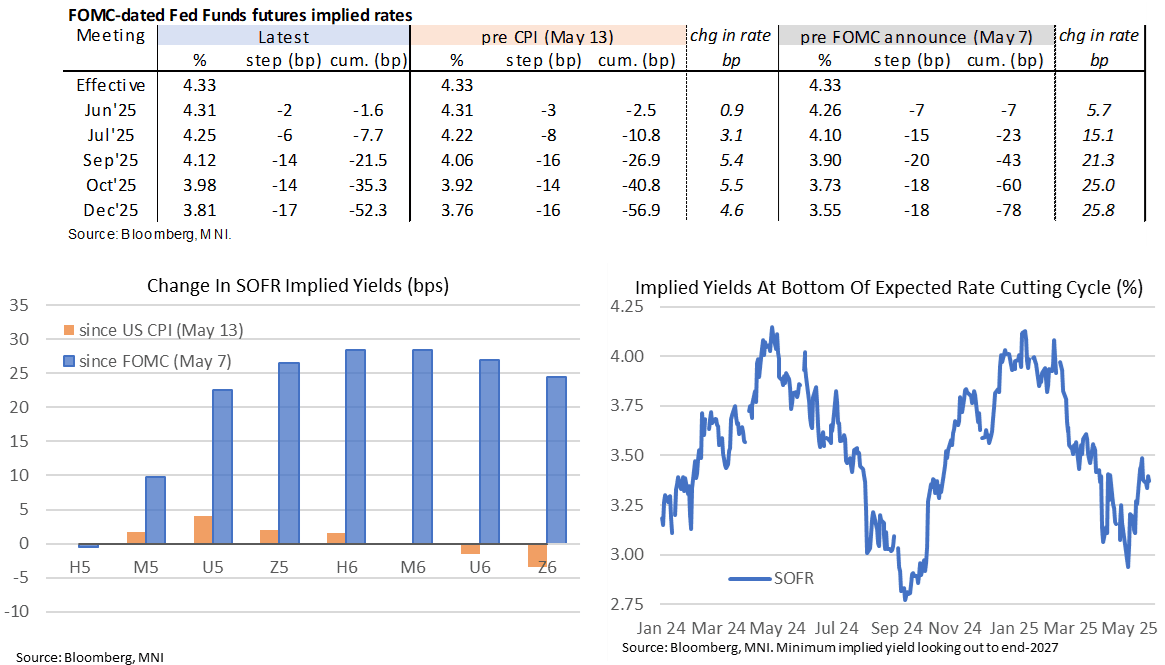

STIR: Fed Rate Path Eases But Still Close To 50bp Of Cuts For 2025

- Fed Funds implied rates are up to 1.5bp lower for 2025 meetings overnight, belatedly drifting lower after equities slid on a weak 20Y auction yesterday that saw 30Y yields hit fresh highs since 2023.

- Cumulative cuts from 4.33% effective: 1.5bp Jun, 7.5bp Jul, 21.5bp Sep, 35.5bp Oct and 52.5bp Dec.

- The terminal rate of 3.37% (SFRZ6) is 3bp lower but remains in relatively tight ranges seen since May 15.

- Today sees Richmond Fed’s Barkin (non-voter) in a fireside chat at 0800ET before NY Fed’s Williams (voter) giving keynote remarks at 1400ET. We could also see more pop-up speakers with the Atlanta Fed’s financial markets conference now concluded.

- Barkin hasn’t touched on monetary policy or the economic outlook in his two appearances so far this week . He last noted on May 9 that consumer spending and business investment is still very solid although it’s not a given that firms can raise prices on tariffs.

- Williams on Monday was more explicit than usual in offering a rough timetable behind rate cut patience, with broader FOMC communications continuing to suggest that a cut before the end of summer is not in the frame.

STIR: Short Setting & Long Cover Dominated On SOFR Strip On Wednesday

OI data points to a mix of net long and short setting, along with long cover, in the SOFR whites on Wednesday.

- A mix of net short setting and long cover was then seen further out the strip, driving twist steepening.

| 21-May-25 | 20-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,050,602 | 1,037,109 | +13,493 | Whites | -5,101 |

SFRM5 | 1,220,901 | 1,219,874 | +1,027 | Reds | -3,249 |

SFRU5 | 1,085,535 | 1,084,216 | +1,319 | Greens | +17,702 |

SFRZ5 | 1,078,861 | 1,099,801 | -20,940 | Blues | +5,911 |

SFRH6 | 762,008 | 769,832 | -7,824 |

|

|

SFRM6 | 734,810 | 724,987 | +9,823 |

|

|

SFRU6 | 742,579 | 746,434 | -3,855 |

|

|

SFRZ6 | 885,850 | 887,243 | -1,393 |

|

|

SFRH7 | 726,310 | 720,423 | +5,887 |

|

|

SFRM7 | 596,466 | 597,455 | -989 |

|

|

SFRU7 | 392,347 | 382,175 | +10,172 |

|

|

SFRZ7 | 409,439 | 406,807 | +2,632 |

|

|

SFRH8 | 267,599 | 268,937 | -1,338 |

|

|

SFRM8 | 197,420 | 193,588 | +3,832 |

|

|

SFRU8 | 152,517 | 153,614 | -1,097 |

|

|

SFRZ8 | 170,270 | 165,756 | +4,514 |

|

|

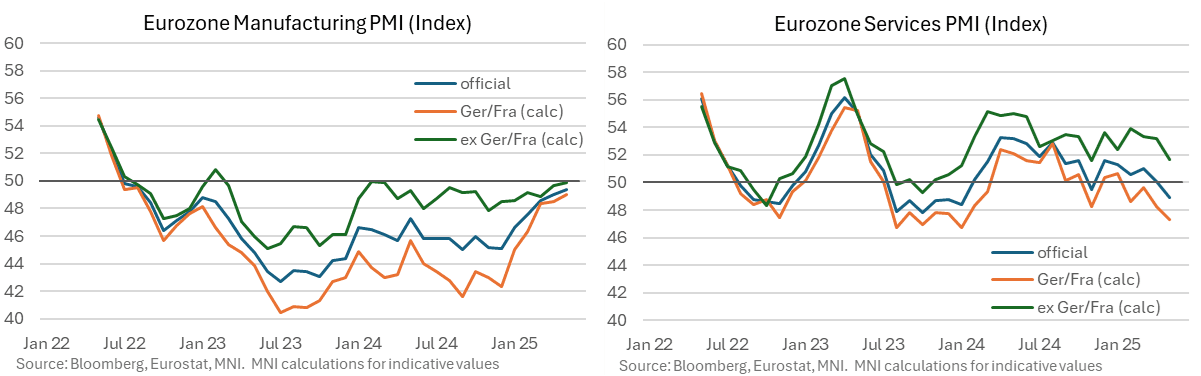

EUROZONE DATA: German and French Service PMI Weakness Starting To Drag Elsewhere

The Eurozone composite PMI disappointed in the flash May release, surprisingly falling to 49.5 (cons 50.6) after 50.4 in April for its first sub-50 reading in five months. Full press release here.

- The weakness was led by services at 48.9 (vs cons 50.5 after 50.1) for its lowest since Jan 2024. That in turn was driven by a particularly weak German reading at 47.2 (vs cons 49.5 after 49.0) for its lowest since Nov 2022.

- Manufacturing at least firmed a touch more than expected to 49.4 (cons 49.2) after 49.0 in April for its highest since Aug 2022. It has been sub-50 since Jun 2022 but has at least recovered from 45.1 as recently as December.

- For services specifically, the surprise slide in German activity left it on similar footing to France, which inched 0.1pt higher to 47.4 for a third reading with a 47 handle after a particularly low 45.3 in Feb.

- Countries other than Germany and France are still doing a lot of the heavy lifting in service activity, although our rough calculation suggests further moderation here as well. Specifically, we estimate a service PMI ex Germany & France fell from 53.2 to 51.6 for its join lowest since Jan 2024. This had been 53.9 in Feb and whilst there can be a 0.1-0.2pt margin of error, the trend direction is clear.

- Back to EZ wide price components, manufacturing input costs decreased by the most since Mar 2024 which helped see selling prices fall for the first time in three months. Conversely, services input costs “were up sharply again, with the pace of inflation slightly stronger than in April” which fed through to a rise in services charges. Composite output price inflation eased to a seven-month low.

EUROPE ISSUANCE UPDATE:

Spain auction results

- E1.821bln of the 5.15% Oct-28 Obli. Avg yield 2.251% (bid-to-cover 1.47x).

- E2.754bln of the 3.10% Jul-31 Obli. Avg yield 2.75% (bid-to-cover 1.63x).

- E1.647bln of the 1.00% Jul-42 Green Obli. Avg yield 3.847% (bid-to-cover 1.74x).

France MT auction results

- Decent French auction with the low price exceeding the mid-price for all line and the top of the E12.5bln range sold.

- Bid-to-covers generally strong. A little softer than last month for the 2.70% Feb-31 OAT but only because the volume sold was almost 50% larger than last month.

- E3.94bln of the 2.40% Sep-28 OAT. Avg yield 2.3% (bid-to-cover 3.34x).

- E6.102bln of the 2.70% Feb-31 OAT. Avg yield 2.72% (bid-to-cover 2.53x).

- E2.455bln of the 0% May-32 OAT. Avg yield 2.91% (bid-to-cover 3.80x).

France I/L auction results:

- E964mln of the 0.10% Jul-31 OATei. Avg yield 0.83% (bid-to-cover 2.55x).

- E379mln of the 3.15% Jul-32 OATei. Avg yield 0.91% (bid-to-cover 3.28x).

- E255mln of the 1.80% Jul-40 OATei. Avg yield 1.58% (bid-to-cover 2.99x).

- E380mln of the 0.10% Jul-53 OATei. Avg yield 1.73% (bid-to-cover 3.16x).

SWEDEN: NDO Up Auction Sizing, Widen Deficit Projections

Sweden's NDO are to meet a "larger borrowing requirement by continuing to increase the supply of government bonds". The NDO are to increase nominal bond supply to SEK 6bln from SEK 5bln per auctions, and are to add "a few" auctions, and introduce new bonds more frequently.

- On FX borrowing, the NDO's new plan has plans for an additional FX bond for 2025.

- Budget deficit is projected to hit SEK 93bln this year, from SEK 65bln previously, while 2026 deficit is projected to hit SEK 89bln from SEK 35bln prior estimate.

FOREX: USD Index Off Lows as Yield Curve Consolidates Steepening

- The USD Index trades higher, with the greenback gaining against most others in G10 as the long-end of the yield curve consolidates after yesterday's upside. The 30y yield hit 5.1% at the high, and holds within range of that level into the NY crossover, as angst over the White House's fiscal plans continues to play out in bond markets. A vote on the Big Beautiful Bill could come imminently as the House pulls an all-nighter, leaving ample headline risk ahead of the Thursday opening bell.

- USD/JPY makes light work of overnight lows following the European PMIs. German and French prelim data held up well for manufacturing, but showed a services sector that remains weaker than forecast. This morning's price action sees spot drift through downtrendline support drawn off the May 14 low on the 15-minute candle chart (trendline last at 142.99), extending the downside scope to include layered support between 141.99 - 142.36.

- The strong co-movement between USD/JPY and longer-end US yields remain the key driver here, a relationship that's firmed since mid-March - and the cemented break above 5% in 30-year yields this week poses further downside risks for USDJPY.

- Prelim US PMI numbers due later today are expected to show US activity broadly inline with April - showing generally few material signs of an economic slowdown as a result of Trump's tariffs. Existing home sales and weekly jobless claims data are also due. The central bank speaker slate is busier, with BoE's Breeden, Dhingra & Pill all set to speak - and comment touching on this week's higher-than-expected UK inflation print will be carefully watched. Fed's Barkin & Williams are also set to make appearances, as well as ECB's Elderson, de Guindos & Nagel.

JPY: Clearance of 5% in US 30y Yield Extends Downside Risk in USD/JPY

- USD/JPY makes light work of overnight lows to hit a new multi-week low following the European PMIs and despite general stability in the USD.

- This morning's price action also sees spot drift through downtrendline support drawn off the May 14 low on the 15-minute candle chart (trendline last at 142.99), extending the downside scope to include layered support between 141.99 - 142.36.

- The strong co-movement between USD/JPY and longer-end US yields remain the key driver here, a relationship that's firmed since mid-March - and the cemented break above 5% in 30-year yields this week poses further downside risks for USDJPY.

- The spell of weakness off mid-May highs marks seven consecutive sessions of lower lows, affirming the pick-up in near-term downside momentum evident in the growing discount between the 50- and 200-dmas. This discount now stands at 2.5%, the largest since October last year.

OPTIONS: Expiries for May22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1175(E1.9bln), $1.1300-15(E828mln), $1.1390-00(E510mln)

- GBP/USD: $1.3260-70(Gbp1.5bln), $1.3390-95(Gbp673mln)

- EUR/GBP: Gbp0.8590-00(E790mln)

- USD/JPY: Y143.50($602mln)

- USD/CAD: C$1.3700($659mln), C$1.4050($1.3bln)

EQUITIES: Bullish Theme in E-Mini S&P Intact Despite Recent Pullback

Eurostoxx 50 futures continue to trade at their recent highs and a bullish theme remains intact. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg, and maintains the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Key support to watch lies at 5211.33, the 50-day EMA. Clearance of this level would signal a possible reversal. A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. An important resistance at 5837.25, the Mar 25 high and a bull trigger, has recently been cleared. This has strengthened the current bullish theme, and paves the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5703.54, the 50-day EMA. A clear break of it would highlight a potential reversal.

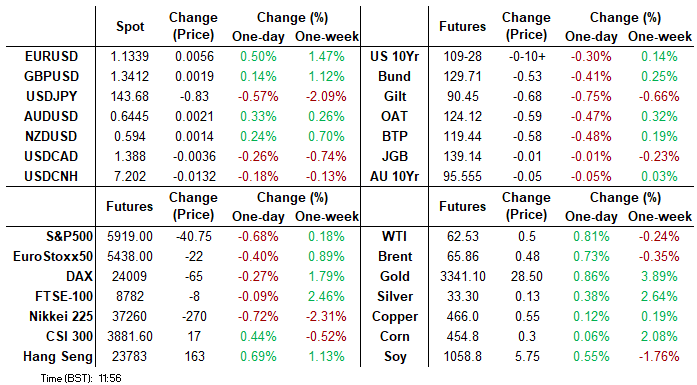

- Japan's NIKKEI closed lower by 313.11 pts or -0.84% at 36985.87 and the TOPIX ended 15.79 pts lower or -0.58% at 2717.09.

- Elsewhere, in China the SHANGHAI closed lower by 7.385 pts or -0.22% at 3380.188 and the HANG SENG ended 283.47 pts lower or -1.19% at 23544.31.

- Across Europe, Germany's DAX trades lower by 144.2 pts or -0.6% at 23977.95, FTSE 100 lower by 56.61 pts or -0.64% at 8730.02, CAC 40 down 54.89 pts or -0.69% at 7855.6 and Euro Stoxx 50 down 38.53 pts or -0.71% at 5415.93.

- Dow Jones mini down 15 pts or -0.04% at 41933, S&P 500 mini up 10.5 pts or +0.18% at 5871.5, NASDAQ mini up 55.5 pts or +0.26% at 21212.25.

COMMODITIES: Reversal Signal in WTI Strengthens a Bearish Theme

WTI futures traded to a fresh short-term cycle high Wednesday before finding resistance. The recovery since Apr 9, still appears corrective. Key resistance to watch is $62.82, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. Yesterday’s price pattern is a shooting star candle - a reversal signal. Gold has recovered from its recent lows and is again trading higher, today. The climb signals the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals remain bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. A continuation would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

- WTI Crude down $0.68 or -1.1% at $60.86

- Natural Gas down $0.04 or -1.25% at $3.326

- Gold spot down $4.45 or -0.13% at $3312.64

- Copper up $1.3 or +0.28% at $468.4

- Silver down $0.04 or -0.12% at $33.355

- Platinum down $3.69 or -0.34% at $1073.6

| Date | GMT/Local | Impact | Country | Event |

| 22/05/2025 | 1050/1150 | BOE's Breeden On Climate Panel | ||

| 22/05/2025 | 1100/1200 | BOE's Dhingra On UK Productivity Panel | ||

| 22/05/2025 | 1130/1330 | ECB April Minutes Released | ||

| 22/05/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 22/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 22/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 22/05/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/05/2025 | 1230/1330 | BOE's Pill At MonPol Conference (Text 16:30BST) | ||

| 22/05/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 22/05/2025 | 1400/1000 | *** | NAR existing home sales | |

| 22/05/2025 | 1400/1000 | * | Services Revenues | |

| 22/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 22/05/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 22/05/2025 | 1500/1700 | ECB's Elderson Dinner Speech at Biodiversity Day | ||

| 22/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 22/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 22/05/2025 | 1535/1735 | ECB's de Guindos Speech in Madrid | ||

| 22/05/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 22/05/2025 | 1800/1400 | New York Fed's John Williams | ||

| 22/05/2025 | 1900/1500 | New York Fed's Roberto Perli | ||

| 23/05/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 23/05/2025 | 2330/0830 | *** | CPI | |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |