MNI US MARKETS ANALYSIS - CPI Next Litmus Test for Fed Path

Highlights:

- Market vols subdued into CPI, next litmus test for Fed rate path

- UK spending review seen favouring defence, healthcare

- China, US agree on next steps for trade, agreement goes to Xi, Trump for sign-off

US TSYS: Bear Steeper In Another Lighter Start Before CPI and 10Y Supply

- Treasuries are bear steeper as they extend yesterday’s post-1000ET sell-off, with CPI in focus (MNI Preview) before 10Y supply. For the latter, long-end pressures are less acute than has been the case in previous months but it will nevertheless mark an important test of duration demand.

- A federal appeals court yesterday extended a short-term reprieve for the Trump Administration as it challenges last month’s trade court ruling that blocked tariffs. Trump has just now described this as a “great and important win for the US”.

- Today’s China statement after a conclusion of US-China talks offered nothing concrete. It urged dispute resolution via dialog, vowed to reduce the misunderstanding and promoted the long-term development of China-US ties.

- Cash yields are 1-4bp higher, with increases led by 20s and 30s.

- The modest steepening sees curves lift a little further off what had been flats for recent weeks, including 2s10s at 47.5bp (+1.9bp) and 5s30s at 86.5bp (+2bp).

- TYU5 has recently touched a session low of 110-00+ (- 06) on another overnight session with light volumes, currently at 240k.

- It extends a pullback off yesterday’s high of 110-14 having stopped short of testing 110-19+ (50-day EMA). A bearish threat is still present, with support at 109-26 (May 29 low) before a bear trigger at 109-12+ (May 22 low).

- Data: CPI May (0830ET), Real av earnings May (0830ET), Federal budget balance May (1400ET)

- Coupon issuance: US Tsy $39B 10Y Note re-open - 91282CNC1 (1300ET). Last month’s 10Y saw a strong 1.3bp stop through but with weaker details than the previous auction.

- Bill issuance: US Tsy $60B 17W bill auction (1130ET)

- Bloomberg reports that HK pensions plan to sell down their Treasury holdings within three months if the US loses its last AAA rating (by Japan’s Rating & Investment Information Inc.)

STIR: Next Fed Cut Seen In October Ahead Of CPI

- Fed Funds implied rates for 2025 meetings are close to late May’s most hawkish levels since February, with a next cut fully priced for Oct and less than two cuts fully priced to year-end.

- There has been little net impact on near-term meetings from the US appeals court late yesterday ruling that tariffs can stay in place longer or the more recent China statement following two days of US-China talks in London.

- That’s ahead of today’s CPI report for May. An upside surprise could tee up a hawkish Fed next week, emboldening more members to pencil in at most one cut in 2025.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Jun2025_a86717a017.pdf

- Cumulative cuts from 4.33% effective: 0bp Jun, 3.5bp Jul, 16.5bp Sep, 28bp Oct and 43.5bp Dec.

- The SOFR implied terminal yield of 3.41% (SFRZ6, +2bp) is still a little off Friday’s post-payrolls close of 3.435% at what was its highest since May 14.

US INFLATION: MNI US CPI Preview: An Important Pre-FOMC Steer

- We have published and e-mailed to subscribers the MNI US CPI Preview.

- Please find the full report including MNI analysis plus detailed analyst estimates, here: https://media.marketnews.com/USCPI_Prev_Jun2025_a86717a017.pdf

- Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April.

- We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares.

- The broad assumption is that May could have started to see a greater tariff impact than April but that firmer increases are more likely to show in summer months.

- Both headline and core CPI Y/Y inflation should firm one to two tenths after lows since early 2021, whilst the six-month core rate should see a similar print after four months running hotter than the Y/Y.

- We have seen preliminary core PCE estimates center on 0.22% M/M for May (median, 0.24% average), due the usual updates after Wednesday’s CPI and Thursday’s PPI. One area to watch in the latter will the extent of a bounce in portfolio management and investment advice after sliding with equities in April.

- The Fed rate path is close to its most hawkish since February, with a next cut fully priced for October.

- A dovish surprise could see a more limited reaction on the assumption that strength is yet to come for consumer prices, unless it’s seen across some of the less volatile services components. On the flipside, an upside surprise can see a further kicking out of rate cut expectations and could tee up a hawkish Fed SEP.

UK: POLITICAL RISK - Spending Review 2025

MNI's Political Risk team has published an article looking at the political implications of tomorrow's Spending Review, particularly in the context of the Labour government's challenge from the right-wing populist Reform UK in opinion polls.

HONG KONG: HK Pensions Fund to Cut Tsy Holdings if US Lose Last AAA Rating

Hong Kong's pension plan are planning to cut Treasury holdings if the US loses its AAA rating, according to Bloomberg sources.

Highlights from the piece:

- Hong Kong’s pension fund managers have formed a preliminary plan to sell down their Treasury holdings within as soon as three months if the US loses its last recognized top credit rating

- Industry groups including the Hong Kong Investment Funds Association and the Hong Kong Trustees’ Association discussed the proposal with the pensions regulator on Wednesday

Worth noting this is a regulatory, rules-based investment decision, as set out by local regulations: "managers of the city’s HK$1.3 trillion ($166 billion) Mandatory Provident Fund system can only invest more than 10% of their funds in Treasuries if the US has a AAA or equivalent rating from an approved agency."

"The downgrade of US sovereign debt by Moody’s Ratings last month left Japan’s Rating & Investment Information Inc. as the only remaining approved firm with the highest score."

US TSY FUTURES: Short Cover In Long End On Tuesday

OI data suggests that net short cover in TY futures provided the only real positioning swing of note on Tuesday, as the futures curve twist flattened.

- Instances of net short setting (TU) and short cover (UXY, US & WN) seen elsewhere were modest.

- The unchanged price status of FV makes it difficult to provide any meaningful inference when it comes to the modest net position build indicated by OI.

| 10-Jun-25 | 09-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,963,228 | 3,956,470 | +6,758 | +266,267 |

FV | 6,785,428 | 6,780,461 | +4,967 | +215,994 |

TY | 4,716,473 | 4,770,026 | -53,553 | -3,530,261 |

UXY | 2,299,192 | 2,301,029 | -1,837 | -159,324 |

US | 1,720,829 | 1,722,289 | -1,460 | -198,908 |

WN | 1,887,843 | 1,889,388 | -1,545 | -278,200 |

|

| Total | -46,670 | -3,684,432 |

STIR: Short Setting Dominated In Front Of SOFR Strip On Tuesday

OI data suggests that net short setting dominated through the SOFR reds on Tuesday (5/8 contracts in that area saw relatively heavy net shorts added), before a mix of net long setting and short cover came to the fore in SSFRZ7 through SFRZ8

| 10-Jun-25 | 09-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,067,243 | 1,068,096 | -853 | Whites | +27,563 |

SFRM5 | 1,432,476 | 1,431,730 | +746 | Reds | +117,169 |

SFRU5 | 1,169,347 | 1,153,856 | +15,491 | Greens | -3,970 |

SFRZ5 | 1,144,414 | 1,132,235 | +12,179 | Blues | +1,014 |

SFRH6 | 914,573 | 867,533 | +47,040 |

|

|

SFRM6 | 862,434 | 827,191 | +35,243 |

|

|

SFRU6 | 787,983 | 750,132 | +37,851 |

|

|

SFRZ6 | 861,686 | 864,651 | -2,965 |

|

|

SFRH7 | 660,039 | 676,524 | -16,485 |

|

|

SFRM7 | 600,624 | 590,189 | +10,435 |

|

|

SFRU7 | 426,208 | 422,239 | +3,969 |

|

|

SFRZ7 | 404,689 | 406,578 | -1,889 |

|

|

SFRH8 | 305,079 | 302,377 | +2,702 |

|

|

SFRM8 | 218,742 | 219,274 | -532 |

|

|

SFRU8 | 169,586 | 168,860 | +726 |

|

|

SFRZ8 | 169,072 | 170,954 | -1,882 |

|

|

JAPAN: PM Denies 'Cash Handouts' As Oppo. Seen To Back Off From No Conf. Motion

Speaking as part of the final leaders' debate of the current session of the House of Representatives, PM Shigeru Ishiba counters recent reports about the prospect of cash handouts ahead of the House of Councillors election due by late July. Reuters reports Ishiba saying that it is "not true that the gov't is currently considering providing cash handouts" and that people "should be cautious about any plans that would deteriorate already tattered state finances."

- This would seem to counter a report in Asahi Shimbun, claiming that Ishiba's conservative Liberal Democratic Party (LDP) and its coalition allies Komeito are considering a 'payment scheme' to 'combat price rises'. Shimbun: "There will be no income restrictions, and every citizen will receive 20,000 yen (USD137) in cash. An additional 20,000 yen will be provided to households not subject to resident tax."

- Ishiba, responding to a question from the leader of the Japanese Communist Party, said cutting the consumption tax was "not appropriate,".

- There has been speculation that main opposition centre-left Constitutional Democratic Party (CDP) leader Yoshihiko Noda could submit a no=confidence motion in Ishiba's minority gov't, but reports claim that Noda may delay this until after the sidelines summit between the PM and US President Donald Trump on the sidelines of the G7 summit in Canada running 15-17 June.

ECB: Further Currency Shifts May Strengthen Euro’s Global Role

- The ECB has published its annual report into the euro. President Lagarde’s foreword notes that:

- “The euro continued to hold its position as the second most important currency globally” in 2024.

- “Further shifts may be underway in the landscape of international currencies. The tariffs imposed by the US Administration have led to highly unusual cross-asset correlations. This could strengthen the global role of the euro and underscores the importance for European policymakers of creating the necessary conditions for this to occur.”

- “The number one priority must be advancing the savings and investment union to fully leverage European financial markets. […] The planned issuance of bonds at the EU level – as Europe takes charge of its own defence – could make an important contribution to achieving these objectives.”

- The report goes on to note that “the share of gold in global foreign reserves at market prices, at 20%, surpassed the share of the euro (16%). Survey data suggest that two-thirds of central banks invested in gold for purposes of diversification, while two-fifths did so as protection against geopolitical risk.”

- Euro strength has received close attention from policy makers since its decoupling with factors such as rate differentials, something that first started with EU/German defence and infrastructure investment plans before kicking up a gear with US reciprocal tariff announcements in April.

- The holding of relatively high EUR/USD rates (currently 1.1436) appears to have given Governing Council members added confidence that a deposit rate of 2%, reached after last week’s 25bp cut for 200bp of easing for the cycle, leaves policy in a good place with implications of a pause ahead.

- Lagarde has previously talked on the potential benefits of a growing global role. This from May 26: “Increasing the international role of the euro can have positive implications for the euro area. It would allow EU governments and businesses to borrow at a lower cost, helping boost our internal demand at a time when external demand is becoming less certain.”

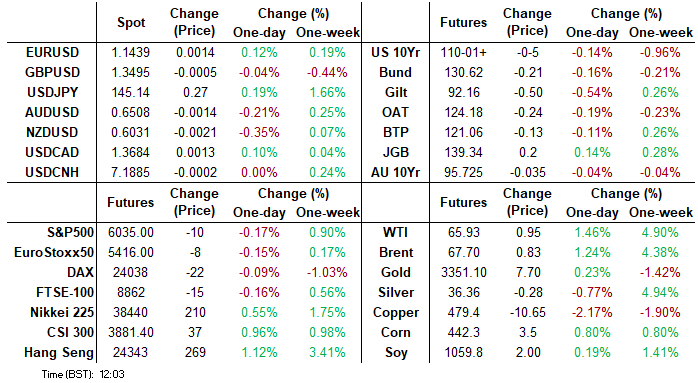

FOREX: Vols See Minimal Pre-CPI Premium, DXY Clear of Test of Downtrendline

- The USD Index is firmer, but well off session highs - keeping markets clear of any material test on the downtrendline resistance drawn off the early February high (today crossing at 99.462, just below the 100.004 50-dma). This level remains a key focus headed through the several inflation releases this week (CPI today, PPI tomorrow).

- Meanwhile, the front-end of the G10 FX vol curve remains subdued headed into today's CPI print, with vols sold on the back of confirmation that US and Chinese officials had agreed on an approach for trade negotiations - that now awaits sign-off from the Chinese, US Presidents. Statements from both sides show little substantive progress on the key issues, leaving an element of uncertainty on the table ahead.

- EUR/USD is well off lows, but spot remains inside the weekly range - the ECB's wage tracker saw a minor upward revision - leaving little ripple in ECB rates markets that price one further 25bps rate cut before year-end.

- With overnight USD/JPY vols briefly above 15 points today, either side of the post-Liberation Day average, which suggests the underlying spot downtrend remains intact for now, despite the bounce off last week's lows. As such, 142.12 / 145.29 remain the key parameters.

OPTIONS: Expiries for Jun10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E2.2bln), $1.1400(E2.2bln), $1.1498-00(E1.0bln)

- USD/JPY: Y143.00($889mln), Y144.90-00($1.2bln)

- GBP/USD: $1.3450(Gbp758mln), $1.3600-05(Gbp565mln)

- AUD/USD: $0.6350-65(A$1.0bln) $0.6495-00(A$799mln)

- USD/CAD: C$1.3760($570mln), C$1.3800($527mln)

UK: Cabinet Giving Final Sign-Off Before Spending Review At ~12:30BST

Prime Minister Sir Keir Starmer is holding a cabinet meeting to give final sign-off to Chancellor of the Exchequer Rachel Reeves' Spending Review, set to be delivered later today. Ministers leading all gov't departments have now given their approval to their settlements, with Home Secretary Yvette Cooper seen to be the last holdout, likely indicating a sub-par settlement for the department in charge of policing, borders, and immigration (among other areas) in Cooper's view.

- The Mirror highlights the main announcements already known: £15.6 billion for public transport projects in England's city regions; £16.7 billion for nuclear power projects, including £14.2 billion for the new Sizewell C power plant in Suffolk; £39 billion over the next 10 years to build affordable and social housing; An extension of the £3 bus fare cap until March 2027; £445 million for upgrades to Welsh railways.

- These funds come as part of a mix of the GBP113B made available for infrastructure due to looser borrowing rules on capital investment, and the distribution of funds among the already-existing 'envelope' from the Autumn 2024 budget.

- Chancellor Reeves is set to deliver the Spending Review statement at around 12:30BST (07:30ET, 13:30CET). Livestream here.

COMMODITIES: WTI Futures Extending Current Bull Cycle

- WTI futures have traded higher this week, extending the current bull cycle. The contract has cleared the 50-day EMA, signalling scope for an extension towards $67.14 next, a Fibonacci retracement. It is still possible that the recovery since early May is a correction. MA studies are in a bear-mode position, highlighting a dominant M/T downtrend. Support to watch lies at $59.74, the May 30 low. A break would highlight a potential bearish reversal.

- A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals remain bullish - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would refocus attention on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, the next support to monitor is $3245.6, the 50-day EMA.

EQUITIES: E-Mini S&P Trading at Fresh Cycle High, Focus on $6057.00 Next

- Eurostoxx 50 futures continue to trade at their recent highs. The trend condition is bullish - moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen the bull theme. Key support to watch lies at 5205.88, the 50-day EMA. A clear break of this average would signal a possible reversal.

- The trend condition in S&P E-Minis remains bullish and the contract has again traded to a fresh cycle high, today. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. Sights are on 6057.00 next, the Mar 3 high. Key support to watch lies at 5808.04, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget | |

| 12/06/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 12/06/2025 | 0600/0700 | ** | Trade Balance | |

| 12/06/2025 | 0600/0700 | ** | Index of Services | |

| 12/06/2025 | 0600/0700 | *** | Index of Production | |

| 12/06/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/06/2025 | 0900/1100 | ECB Schnabel Visits "House of the Euro" | ||

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI | |

| 12/06/2025 | 1400/1000 | * | Services Revenues | |

| 12/06/2025 | 1415/1615 | ECB Elderson At Senior Supervisors Conference | ||

| 12/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 12/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/06/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond |