MNI US MARKETS ANALYSIS - CPI Gives First Post-Tariff Glimpse

Highlights:

- US CPI in focus, with markets expecting steady headline & Core

- US inflation data provides first glimpse at post-tariffs economy

- Equities hold tariff rollback gains as Trump heads to Middle-East for more deal-making

US TSYS: TYA Eyes Latest Support Ahead Of CPI

- Treasuries broadly consolidate yesterday’s sell-off on US-China trade de-escalation ahead of today’s US CPI report for April.

- MNI US CPI Preview here.

- Cash yields are 0-2.5bp lower on the day, with declines led by 2s/3s and with 20s lagging the move.

- 2s10s at 46.7bp and 5s30s at 81bp sit within some wide recent ranges.

- TYM5 trades at 110-06 (+01), maintaining the softer tone on modest cumulative volumes of 290k.

- Yesterday’s low of 110-01+ met latest support at a 76.4% retracement of the Apr 11 – May 1 bull leg, after which lies a key 109-08 (Apr 24 low). To the upside, resistance at 111-04+ (20-day EMA).

- Some recent downside flow: TYN5 109.00/108.00 put spread 20K lots blocked at 0-14 (05:32:08ET) following 21K of the FVN5 107.00/106.25 put spread being blocked through the London morning.

- Data: US CPI Apr (0830ET), Real avg earnings Apr (0830ET)

- Fedspeak: None scheduled

- Bill issuance: US Tsy $48B 52W & $70B 6W bill auctions (1130ET)

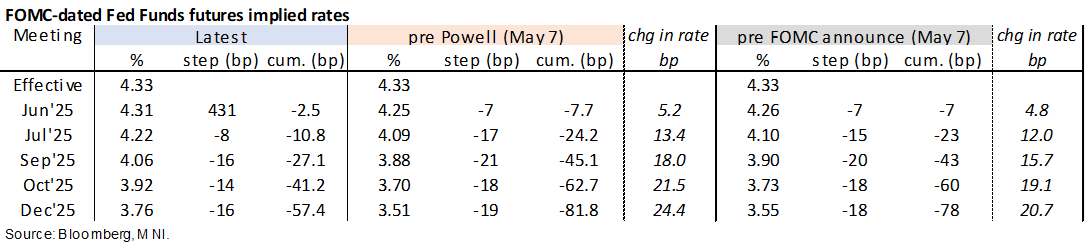

STIR: Less Than 50/50 Odds Of Next Fed Cut In July Ahead Of CPI

- Fed Funds implied rates sit between 1bp higher (Jul) and 1bp lower (Dec) for 2025 meetings overnight, broadly holding yesterday’s significant hawkish re-pricing on US-China trade de-escalation.

- It only just sees a next Fed cut fully priced for September (three meetings away) ahead of today’s US CPI report for April.

- MNI US CPI Preview here.

- Cumulative cuts from 4.33% effective: 2.5bp Jun, 11bp Jul, 27bp Sep, 41bp Oct and 57bp Dec.

- SOFR implied terminal yields are 4bp lower on the day at 3.39% (SFRZ6) for back to almost exactly at levels prior to initial Apr 2 Liberation Day tariff announcements.

- There is no Fedspeak scheduled for today. Two permanent voters in Waller and Jefferson are scheduled tomorrow before Powell follows just 10 minutes after US PPI and retail sales on Thursday.

US DATA: Small Businesses More Focused On Tax Cuts And Jobs Act Renewal

Interestingly, whilst the NFIB press release notes the sudden and dramatic changing in costs from tariffs, inflation is in third place on small businesses list of concerns. Excerpts from the press release (in full here):

- “Very few small businesses export their goods and services, but millions acquire imported goods as inputs to their operations and those supply chains are currently at risk. Tarriff policy is suddenly and dramatically changing relative prices (costs), and relative prices drive all decisions. Uncertainly remains elevated and thus caution clouds spending, hiring, and investing decisions.”

- “While the quality of the available labor force remains the top problem, taxes are close behind, and for over 51 years have received the most votes for single most important business problem. Renewal of the Tax Cuts and Jobs Act (TCJA) remains a major source of uncertainty. Nearly 1 in 10 owners view government regulations and red tape as their top business problem, a form of taxation in which the government directs the expenditure of resources for compliance.”

- “Inflation continues to fade in the list of concerns (now ranking third). Actual inflation is low, although not quite at the Fed’s goal of 2 percent. But prices are still rising, and what owners want to see is a reversal of the cumulative 20 percent increase in prices under the Biden administration. History tells us that this has always required a slowdown in the economy. Massive improvements in productivity, which reduce production costs (especially in services), can trigger lower selling prices. This is a far more attractive path to achieving their goal. However, this will require substantial investment. Capital spending has been anemic since 2020, and capital spending plans are at the lowest level seen since 2020.”

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen On Monday

OI data points to a mix of net long cover (TU, FV & US) and short setting (TY, UXY & WN) as the recent round of weakness in Tsy futures extended on Monday.

- The most concentrated net positioning adjustment seemed to come via net short setting in the intermediates (TY & UXY), with the net curve-wide bias also tilted towards net short setting.

| 12-May-25 | 09-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,072,279 | 4,093,359 | -21,080 | -764,134 |

FV | 6,835,380 | 6,851,273 | -15,893 | -673,142 |

TY | 4,964,269 | 4,942,821 | +21,448 | +1,365,649 |

UXY | 2,304,757 | 2,286,675 | +18,082 | +1,571,134 |

US | 1,809,291 | 1,816,826 | -7,535 | -941,319 |

WN | 1,891,950 | 1,886,381 | +5,569 | +1,001,366 |

|

| Total | +591 | +1,559,554 |

STIR: Short Setting Dominated Front Of SOFR Strip Monday, Long Cover Further Out

OI data points to a mix of net short setting and long cover as most SOFR futures finished lower on Monday. Short setting was more prominent through the reds, before long cover moved to the fore further out the strip.

| 12-May-25 | 09-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,091,676 | 1,102,121 | -10,445 | Whites | +54,730 |

SFRM5 | 1,220,210 | 1,220,031 | +179 | Reds | +26,067 |

SFRU5 | 1,013,935 | 994,156 | +19,779 | Greens | -18,229 |

SFRZ5 | 1,136,845 | 1,091,628 | +45,217 | Blues | -717 |

SFRH6 | 765,246 | 754,764 | +10,482 |

|

|

SFRM6 | 743,359 | 741,591 | +1,768 |

|

|

SFRU6 | 715,907 | 727,795 | -11,888 |

|

|

SFRZ6 | 862,797 | 837,092 | +25,705 |

|

|

SFRH7 | 659,364 | 665,326 | -5,962 |

|

|

SFRM7 | 569,460 | 569,243 | +217 |

|

|

SFRU7 | 357,881 | 368,219 | -10,338 |

|

|

SFRZ7 | 395,311 | 397,457 | -2,146 |

|

|

SFRH8 | 274,574 | 276,103 | -1,529 |

|

|

SFRM8 | 185,218 | 187,995 | -2,777 |

|

|

SFRU8 | 156,495 | 152,494 | +4,001 |

|

|

SFRZ8 | 165,149 | 165,561 | -412 |

|

|

EUROPE ISSUANCE UPDATE:

EU syndication: Final terms

- E7bln (upsized from E6bln guidance; MNI had expected E5-9bln) of the new 20-year Oct-45 EU-bond. Books in excess of E64bln, spread set at MS+110bp (guidance was MS + 112bps area).

Netherlands auction results:

- E1.98bln of the 2.00% Jan-54 DSL. Avg yield 3.228%.

UK auction results:

- GBP1bln of the 0.625% Mar-45 Linker. Avg yield 2.235% (bid-to-cover 3.19x).

Italy auction results:

- E3.5bln of the 2.65% Jun-28 BTP. Avg yield 2.4% (bid-to-cover 1.51x).

- E2.5bln of the 3.25% Jul-32 BTP. Avg yield 3.28% (bid-to-cover 1.60x).

- E1.5bln of the 4.45% Sep-43 BTP. Avg yield 4.26% (bid-to-cover 1.68x).

Germany auction results:

- Given the recent string of weak German auctions across the curve, today’s 2.16x bid-to-cover ratio for the 1.70% Jun-27 Schatz (vs 1.69x prior) will likely come as somewhat of a relief. This was the first re-opening of this line after launching in April.

- It’s still worth noting that the low price of 99.510 was a touch below the 99.512 pre-auction mid-price. However, there has been limited reaction in the secondary price of the bond and Schatz futures in the minutes after the results were published.

- E4.5bln (E3.401bln allotted) of the 1.70% Jun-27 Schatz. Avg yield 1.94% (bid-to-offer 1.63x; bid-to-cover 2.16x).

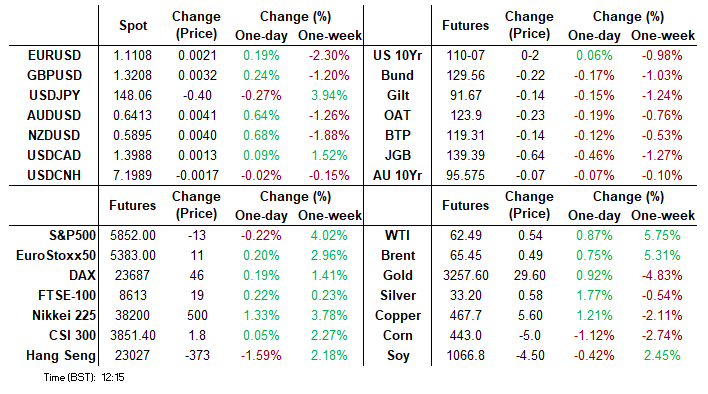

FOREX: Closely Monitoring 50-Day EMA Support for EURUSD

- The Euro has been unable to garner much support on Tuesday, spending the majority of the session consolidating just above the 1.11 mark, up 0.2% on the session. The single currency relatively underperforms the likes of AUD, NZD and CHF in G10. The de-escalation in global trade tensions remain the primary driver behind the repositioning in EURUSD, however, stalled negotiations between the EU/US are likely providing an additional EUR headwind.

- From a trend perspective, recent EURUSD weakness appears corrective as key signals remain bullish. However, the pair has breached the 20-day EMA and pierced 1.1082, the 50-day EMA. A clean break of the average would strengthen a bear threat and signal scope for a move towards 1.1026, the 38.2% retracement of the Feb 3 - Apr 21 bull cycle.

- BBVA have noted that even if there is additional USD strength in the short term, they view these levels as good opportunities for long positions in EUR to hedge against the medium- to long-term rise that they expect for the pair.

- In similar vein, Nordea point out that fiscal stimulus and targeted investment policies will support economic growth next year. With global portfolios still heavily concentrated in US assets, even a modest rotation toward Europe could provide meaningful support to the euro.

- Nordea expect a broader diversification of assets and currencies to unfold over several years. They believe EURUSD will move up toward the 1.20 level by the end of 2026, but would not be surprised if it could play out even faster.

- ING think EURUSD has completed a first leg in a sequence of what could be a multi-year bull trend. They imagine this current corrective dip will find good buyers in the 1.1030/50 area, with outside risk of a move down to 1.0850. This week's decline makes ING feel more comfortable about their year-end target of 1.13, which otherwise had looked too conservative.

FOREX: Dollar Index Resistance Holds For Now, US CPI Up Next

- Risk appetite has consolidated following Monday's surge, allowing USD indices to track moderately lower early Tuesday. The Ice USD index broadly held its first main resistance point at the 50-day EMA, an average that has capped DXY gains since March. With that said, the greenback is holding the majority of yesterday’s advance, and with US CPI providing the next impulse later today, the short-term trajectory for the DXY will be closely monitored.

- A similar dynamic for major equity benchmarks is allowing the likes of AUD and NZD to outperform on the session, both rising over half a percent against the dollar, while the Euro has been unable to garner much support.

- Recent EURUSD weakness appears corrective as key trend signals remain bullish. However, the pair has breached the 20-day EMA and pierced 1.1082, the 50-day EMA. A clean break of the average would strengthen a bear threat and signal scope for a move towards 1.1026, the 38.2% retracement of the Feb 3 - Apr 21 bull cycle.

- USDCHF (-0.61%) has also respected its 50-day EMA as well, pulling lower from its 0.8476 recovery high to approach the 0.8400 mark. Overnight straddle pricing incorporates a move of just +/- 45 pips from current spot levels, suggesting that resistance will likely remain intact. However, should yesterday’s boost to risk dominate any developments regarding US inflation and the dollar rally continue, USDCHF will eye a move towards 0.8578, the April 10 high.

- The quantity side of the UK labour market report broadly met expectations, which has kept GBPUSD steady, just above the 1.32 handle. A minor head and shoulders formation on the daily chart highlights a reversal and reinforces the likelihood of a corrective pullback near-term. Key support to watch is 1.3087.

OPTIONS: Expiries for May13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1145-50(E1.0bln), $1.1290-00(E727mln), $1.1325(E600mln), $1.1355-60(E1.1bln), $1.1370-75(E1.8bln), $1.1415-20(E1.3bln), $1.1450(E1.1bln)

- USD/JPY: Y143.00($1.5bln), Y146.75(E567mln), Y151.00($1.2bln)

- GBP/USD: $1.3200(Gbp599mln)

- EUR/GBP: Gbp0.8695(E580mln)

- AUD/USD: $0.6545(A$811mln)

- USD/CAD: C$1.3875-85($1.2bln)

- USD/CNY: Cny7.2500($519mln)

EQUITIES: Monday's Rally in E-Mini S&P Reinforces Bullish Conditions

- Strong gains in the Eurostoxx 50 futures contract on Monday reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5142.89, the 20-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and Monday’s strong gains reinforce bullish conditions. The contract has pierced an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on 5896.25, a Fibonacci retracement. Initial firm support to watch lies at 5637.98, the 50-day EMA.

COMMODITIES: Short-Term Gains for WTI Futures Still Considered Corrective

- A downtrend in WTI futures remains intact and short-term gains are considered corrective. For now, the corrective cycle remains in play and price has traded through the 20-day EMA. Key resistance to watch is $63.55, the 50-day EMA, a clear break of this level would highlight a stronger reversal. This would open $66.41, the Apr 4 high. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger.

- The latest pullback in Gold appears corrective. Key short-term support to watch is $3202.0, the May 1 low. A clear break of this level would undermine the short-term bullish theme and signal scope for a deeper retracement. This would open $3164.3, 61.8% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA is at $3161.0. The medium-term trend condition remains bullish, a reversal would refocus attention on $3500.1, the Apr 22 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 13/05/2025 | - | ECB's De Guindos At ECOFIN Meeting | ||

| 13/05/2025 | 1230/0830 | *** | CPI | |

| 13/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 13/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 14/05/2025 | 0130/1130 | *** | Quarterly wage price index | |

| 14/05/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/05/2025 | 0600/0800 | *** | HICP (f) | |

| 14/05/2025 | 0700/0900 | *** | HICP (f) | |

| 14/05/2025 | 0715/0815 | BOE Breeden At ISDA Conference | ||

| 14/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 14/05/2025 | 0915/0515 | Fed Governor Christopher Waller | ||

| 14/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 14/05/2025 | - | *** | Money Supply | |

| 14/05/2025 | - | *** | New Loans | |

| 14/05/2025 | - | *** | Social Financing | |

| 14/05/2025 | 1230/0830 | * | Building Permits | |

| 14/05/2025 | 1240/1440 | ECB's Cipollone On Liquidity Issues Panel | ||

| 14/05/2025 | 1310/0910 | Fed Vice Chair Philip Jefferson | ||

| 14/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 14/05/2025 | 2140/1740 | San Francisco Fed's Mary Daly |