MNI US MARKETS ANALYSIS - Ceasefire Already on Shaky Ground

Highlights:

- Iran-Israel ceasefire on shaky ground, as Trump sternly warns both sides of violations

- Powell headlines a busy Fed schedule with semiannual policy testimony

- USD/JPY holds U-turn, poses threat to bullish backdrop

US TSYS: Twist Steeper Ahead Of A Busy Session Including Powell and 2Y Supply

- Treasuries trade twist steeper although are within yesterday’s wide ranges.

- The front end is supported by crude oil futures adding to yesterday’s heavy declines on limited Iran retaliation to US strikes. The long end sees some spillover from German supply expectations following Reuters headlines with the DFA Q3 announcement, although losses have been pared there.

- Today sees a heavy session, with Fedspeak headlined by day one of Fed Chair Powell’s semi-annual congressional testimony plus an update on consumer confidence in June before 2Y supply.

- Cash yields are 1.9bp lower (2s) to 1.2bp higher (30s).

- TYU5 deals at 111-09+ (-05) on reasonable cumulative volumes of 385k.

- Yesterday’s high of 111-20+ comfortably breached resistance at 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg), highlighting a stronger reversal. It opens 111-30 (76.4% retrace) whilst support is seen at 110-21+ (50-day EMA).

- Data: Current account Q1 (0830ET), Philly Fed non-mfg Jun (0830ET), FHFA and S&P CoreLogic house prices Apr (0900ET), Conf Board consumer survey Jun (1000ET), Richmond Fed mfg Jun (1000ET)

- Fedspeak: Powell text (likely 0830ET), Hammack on mon pol (0915ET), Powell appearance (1000ET), Williams keynote remarks (1230ET), Kashkari town hall (1345ET), Collins on housing (1400ET), Barr (1600ET), Schmid on economic outlook (2015ET) – see FED bullet

- Coupon issuance: US Tsy $69B 2Y note auction - 91282CNL1 (1300ET). Last month’s 2Y auction was solid, with a 1bp trade through for its highest since Feb, although had some mixed peripheral stats.

- Bill issuance: US Tsy $55B 6W Bill auction (1130ET)

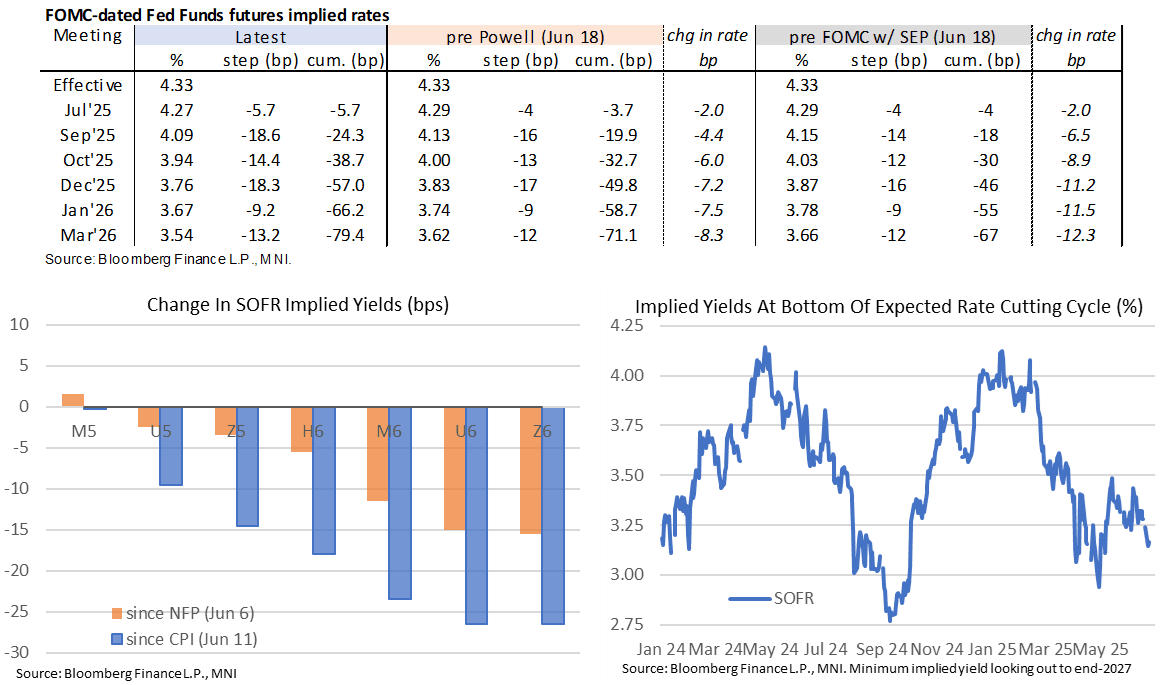

STIR: Holding Shift To Next Fed Cut Around Sep Rather Than Oct

- Fed Funds implied rates are up to 2bp lower on the day, helped by crude oil futures (WTI -2.9%, mostly at the open) on US-Iran ceasefire headlines, although are off yesterday’s dovish extremes.

- Oil saw heavy declines yesterday on limited Iranian retaliation to US strikes and Fed VC for Supervision Bowman gave a surprisingly dovish pivot as she eyes a July cut.

- Cumulative cuts from 4.33% effective: 5.5bp Jul, 24.5bp Sep, 38.5bp Oct, 57bp Dec and 66.5bp Jan.

- SOFR implied yields meanwhile are 1-2bp higher across contracts out to 2027 after heavy declines yesterday.

- For example, the terminal of 3.165% (SFRZ6, +2bp) sees a small increase after yesterday’s 9.5bp drop to its lowest close since May 7, i.e. prior to US-China trade de-escalation on May 12 after weekend talks in Geneva.

- Fed Chair Powell leads today’s docket (with text likely released at 0830ET) but with some notable other FOMC appearances as well – see the earlier FED bullet.

FED: Powell (Text Likely 0830ET) Leads A Heavy Fedspeak Line-Up

- Today sees a heavy Fedspeak schedule headlined by Fed Chair Powell’s House appearance, with text likely to be released at 0830ET judging by historical precedent before the appearance at 1000ET.

- Coming so soon after Wednesday’s FOMC press conference, we’d expect a repeat of him being far from emphatic about the prospect of rate cuts, all but taking a cut at the July meeting off the table.

- From the July presser: “As long as the economy is solid, as long as we're seeing the kind of labor market that we have and reasonably decent growth, and inflation moving down, we feel like the right thing to do is to be where we are, where our policy stance is, and learn more. And in particular we feel like we're going to learn a great deal more over the summer on tariffs."

- With repeated attacks from President Trump including calls for rates to be materially lower, expect a partisan approach to questions. Trump on Truth Social overnight: “I hope Congress really works this very dumb, hardheaded person, over. We will be paying for his incompetence for many years to come. THE BOARD SHOULD ACTIVATE.”

- Broader Fedspeak will also be important considering the dot plot revealed a particularly divided FOMC with seven pencilling in zero cuts this year through to two looking for three cuts.

- VC for Supervision Bowman (voter) surprised yesterday with an abrupt chance in stance, eyeing a July cut if “inflation pressures remain contained”. That echoed a dovish Waller on Friday kickstarting post-FOMC Fedspeak.

- A July cut isn't universally expected on the FOMC: Bostic (non-voter) told Reuters there is no rush to cut rates and that he still sees a single rate cut last this year; Barkin (non-voter) sees no rush to cut rates, whilst Daly (non-voter) thinks the Fed but can’t wait so long before fundamentals necessitate cuts but is looking more to the fall.

- Today sees more speakers with voting roles for 2025 - Hammack, Williams, Collins and Schmid are all likely to have monetary policy relevant content:

- 0830ET/1000ET – Powell Semiannual Policy Testimony

- 0915ET – Cleveland Fed’s Hammack (’26) on monetary policy (text + Q&A)

- 1230ET – NY Fed’s Williams (voter) keynote remarks (text + Q&A)

- 1345ET – Minneapolis Fed’s Kashkari (’26) in town hall (Q&A only)

- 1400ET – Boston Fed’s Collins (’25) on housing (text only)

- 1600ET – Gov. Barr (voter) welcoming remarks

- 2015ET – KC Fed’s Schmid (’25) speaks on economic outlook (text + Q&A)

SOFR: Long Setting Most Prominent In Futures On Monday

OI data points to a mix of net short cover and long setting in SOFR futures on Monday, with offsetting positioning swings seen in the whites, before the latter came to the fore further out the strip.

| 23-Jun-25 | 20-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,293,498 | 1,312,571 | -19,073 | Whites | -846 |

SFRU5 | 1,153,931 | 1,144,006 | +9,925 | Reds | +31,852 |

SFRZ5 | 1,282,554 | 1,265,648 | +16,906 | Greens | +10,910 |

SFRH6 | 991,335 | 999,939 | -8,604 | Blues | +11,396 |

SFRM6 | 849,963 | 844,140 | +5,823 |

|

|

SFRU6 | 805,505 | 798,701 | +6,804 |

|

|

SFRZ6 | 917,736 | 906,074 | +11,662 |

|

|

SFRH7 | 689,435 | 681,872 | +7,563 |

|

|

SFRM7 | 633,197 | 632,729 | +468 |

|

|

SFRU7 | 443,572 | 437,726 | +5,846 |

|

|

SFRZ7 | 411,025 | 405,895 | +5,130 |

|

|

SFRH8 | 297,503 | 298,037 | -534 |

|

|

SFRM8 | 230,638 | 224,521 | +6,117 |

|

|

SFRU8 | 193,828 | 186,259 | +7,569 |

|

|

SFRZ8 | 172,310 | 172,007 | +303 |

|

|

SFRH9 | 139,839 | 142,432 | -2,593 |

|

|

US TSY FUTURES: Long Setting Seen Across The Curve On Monday

OI data points to relatively meaningful net long setting in curve-wide DV01 terms (~$9mn) during Monday’s rally, with the most meaningful long setting coming in FV & TY futures.

- All contracts were seemingly subjected to net long setting.

| 23-Jun-25 | 20-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,127,962 | 4,121,261 | +6,701 | +260,739 |

FV | 7,029,288 | 6,967,318 | +61,970 | +2,702,396 |

TY | 4,850,733 | 4,806,569 | +44,164 | +2,937,083 |

UXY | 2,375,518 | 2,369,300 | +6,218 | +545,331 |

US | 1,753,736 | 1,746,583 | +7,153 | +1,028,832 |

WN | 1,884,958 | 1,877,008 | +7,950 | +1,455,940 |

|

| Total | +134,156 | +8,930,320 |

EUROPE ISSUANCE UPDATE:

DFA Q3 issuance plan update

DFA announces E15bln increase in bond issuance, E4bln in Bubill issuance

Highlights by maturity:

- 7-year Bund: E8bln (over half the increase): As we expected there will be a new 7-year Bund with a maturity of Nov-32. This has two auctions in the quarter of E4bln each (in August and November).

- Schatz: E2bln increase: Reopenings increased to E5bln in August (from E4bln) with two September reopenings of E4.5bln rather than E4.0bln

- 10-year Bund: E2.5bln increase: New issue increased to E6bln (from E5bln) with three reopenings of E5.0bln rather than E4.5bln

- 15-year: E2.0bln increase: Expanding to E2.5bln each

- 30-year: E0.5bln increase for the July auction to E2.5bln

- In the press Q&A following the announcement, the following headlined (from Reuters):

50-YEAR BOND NOT PLANNED FOR THIS YEAR BUT INTERNAL CONDITIONS HAVE BEEN CREATED

WILL PROBABLY CONTINUE UPWARD ADJUSTMENTS TO BOND ISSUANCE IN Q4

VERY GOOD DEMAND FOR LONG-TERM BONDS" RTRS

Slovenia syndication: Update

- E1bln WNG of the new 10-year Jul-35 SLOREP SLB. Revised guidance at MS + 65bps area (initial was MS+70bps Area), Books in excess of E3.1bln.

UK auction results

- GBP1.7bln of the 1.125% Sep-35 Linker. Avg yield 1.386% (bid-to-cover 3.02x).

German auction results

- E4bln (E3.066bln allotted) of the 1.70% Jun-27 Schatz. Avg yield 1.85% (bid-to-offer 2.24x; bid-to-cover 2.92x).

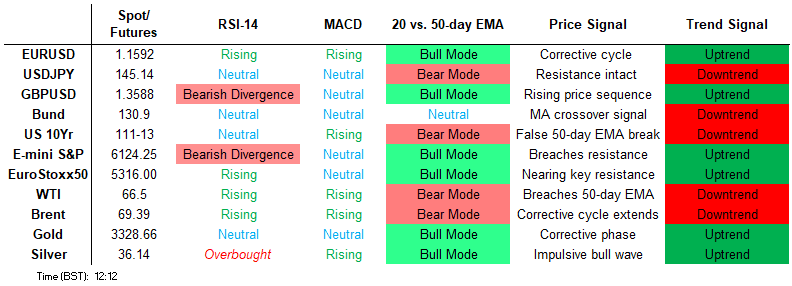

FOREX: USD/JPY Holds Bearish Reversal Pattern

- USD/JPY's reversal off the weekly high has held well, with spot returning to well within range of the Y145.00 handle having traded Y148 at the high yesterday. The remarkable about-turn, triggered by the announcement of a Israel-Iran ceasefire, has looked through early signs of fragility. Israel detected inbound missile strikes, which have been denied via state-run Iranian media.

- This keeps the USD weaker on the day, buoying GBP/USD and EUR/USD through 1.36 and 1.16 respectively, as rallies remain shallow. Geopolitical risk remains the primary focus, however markets seem to be of the view that we're through the worst of the Middle-east tensions and there's a relatively minimal risk of an oil price spike hereon.

- Becalmed commodities markets are allowing risk proxy currencies to outperform. As such, AUD and NZD are easily the best performers in G10, tipping both AUD/USD and NZD/USD back into the uptrend channel dtrawn off the May lows.

- Canadian CPI data is a calendar highlight Tuesday - particularly as USD/CAD reversed hard off highs on the challenge of the 50-dma this week. This brings today's CPI release into sharper focus, particularly given the partial pricing for a July 30 rate cut (OIS sees just over 1:3 probability of a 25bps cut) as well as the now-prolonged trade talks with the US, on which Carney stated yesterday his government are still focused on after an overnight call with Trump.

CANADA: USDCAD Primary Downtrend Intact, 50-Day EMA Resistance Holds [1/2]

- The sharp moves/reversals for both oil markets and the dollar on Monday have provided offsetting forces for the USDCAD exchange rate, keeping the pair in a relatively confined 88 pip range this week. The spike to 1.3798 appears technically corrective, and the primary downtrend is bolstered by the 50-day EMA capping the topside for now. The pair has not been above this average since early April.

- Continued dollar weakness would place attention back on key support and the bear trigger, which has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend.

- At 1330BST (0830ET) we get the first of two monthly CPI readings ahead of the next BOC decision on July 30. Consensus for the Y/Y headline reading is 1.7%, with a slight upward skew, while the average of the BOC's preferred trim and median core measures is seen coming in at 3.0% Y/Y (3.15% unrounded in April), the highest in over a year.

- Another upside surprise in core measures could see a retracement of recent cut repricing (last 10bp, vs 6bp last week), with analysts remaining split on July easing expectations. This would likely reinforce the underlying bearish theme for USDCAD.

CANADA: EURCAD Approaching Key Pandemic Pivot Around 1.6000 [2/2]

- However, a reading in line with or below expectations would keep the door open to a cut amid a pullback in the 3mma annualized rate in trim/median average to 3.1/3.2% from 3.4% prior. A key beneficiary of any follow through Canadian dollar weakness would likely be EURCAD, given the ongoing resilience for the single currency and the close proximity to key medium-term technical parameters for the cross.

- EURCAD's Monday close was the second highest of the year, and puts spot within range of heavy layered resistance between 1.5960 - 1.5990, daily highs dating back to the covid pandemic in 2020. Clearance of this area and the psychological 1.6000 mark would place the cross at levels last seen in 2018 and target 1.6153, the 2018 highs.

- Deutsche Bank have stated that CAD is one of their less preferred currencies – their forecasts for G10 have only the dollar and CHF performing worse, and in Blueprint they recommend long EURCAD.

- Aside from the data, the now-prolonged trade talks with the US remain another key driver, on which Carney stated his government are still focused on after the most recent call with US president Trump. Separately, the EU and Canada signed a security and defense agreement on Monday, meant to be a step in a New EU-Canada Strategic Partnership of the Future.

OPTIONS: Expiries for Jun24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E612mln)

- USD/JPY: Y145.00($582mln)

- USD/CAD: C$1.3775($665mln)

EQUITIES: Trend Condition in E-Mini S&P Unchanged and Bullish

- A short-term bear cycle in Eurostoxx 50 futures remains intact, however, the recovery from Monday’s low appears to be a potential reversal. The contract has traded above the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme and signal scope for a stronger recovery. This would open 5486.00, the May 20 high and bull trigger. On the downside, a break of yesterday’s 5194.00 low would reinstate a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s strong start reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been pierced. A clear break of this level would confirm a resumption of the uptrend that started Apr 7. This would open the 6200.00 handle, a Fibonacci projection. Key support remains at the 50-day EMA - at 5913.50. A clear break of it would signal a reversal.

COMMODITIES: WTI Futures Reverse Sharply From Monday's Highs

- WTI futures have reversed sharply from Monday’s session high. For now, the sell-off is considered corrective and the pullback has allowed a recent overbought condition to unwind. Support to watch is at the 50-day EMA, at $64.51. It has been pierced, a clear break of it would signal scope for a deeper retracement. On the upside, initial resistance to watch is $71.39, the 50.0% retracement of the Jun 23 - 24 high-low range.

- A bullish theme in Gold remains intact and the latest pullback is considered corrective. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has recently been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3286.2, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 24/06/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 24/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 24/06/2025 | 1400/1500 | BOE Bailey At Lords Econ Affairs Committee | ||

| 24/06/2025 | 1540/1640 | BOE Pill At Gold Standard Conference | ||

| 24/06/2025 | 1550/1650 | BOE Breeden At UK Finance Digital Innovation Summit | ||

| 24/06/2025 | 1630/1230 | New York Fed's John Williams | ||

| 24/06/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/06/2025 | 1805/1405 | Boston Fed's Susan Collins | ||

| 24/06/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 25/06/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/06/2025 | 0015/2015 | Kansas City Fed's Jeff Schmid | ||

| 25/06/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 25/06/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 25/06/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/06/2025 | 0700/0900 | ** | PPI | |

| 25/06/2025 | 0700/0900 | *** | GDP (f) | |

| 25/06/2025 | 0845/0945 | BOE Lombardelli At BOE MonPol Conference | ||

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | BOE Pill On Panel At BOE MonPol Conference | ||

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf | ||

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 25/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 25/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/06/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 25/06/2025 | 1800/1400 | Federal Reserve Board Meeting |