MNI US MARKETS ANALYSIS - Bulk of Dovish Shift Holds in STIR

Highlights:

- Fed in focus as Trump could name new governor to replace Kugler as soon as this week

- Bulk of dovish shift in STIRS holds, keeping USD in check

- Equities point to higher open on Wall Street - although ESA still below support

US TSYS: Stabilization Before A Thin Docket Ahead After Last Week’s Swings

- Treasuries have recently pared losses to further limit moves from Friday’s close with the nonfarm payrolls report and its hugely weak two-month revisions digested. For a succinct summary of last week's swings seen after a patient Fed and weak payrolls report, see the MNI US Macro Weekly (link here).

- We touch on it more in the STIR bullet but President Trump says he will announce a new Fed Governor and BLS commissioner in the coming days following a surprise resignation/termination on Friday.

- Cash yields are 1-2bp higher on the day, with 2Y yields for instance more than 25bp before pre-payrolls levels.

- 10Y yields, currently at 4.232%, appeared to meet some support at 4.20% on Friday, touching 4.2002%. It last breached 4.20% on Jul 1 and before that late Apr/early May.

- TYU5 trades at 112-05+ (-01) having pulled back off an overnight high of 112-12, on solid cumulative volumes of 510k as non-US participants caught up with Friday’s price action.

- Friday’s rally punched through 111-14+ (Jul 22/30 high) whilst the overnight high stopped just short of resistance at a bull trigger of 112-12+ (Jul 1 high). There’s further resistance seen shortly after with 112-15 (61.8% retrace of Apr 7-11 sell-off).

- Data: Factory orders Jun (1000ET)

- Fedspeak: None scheduled

- Bill issuance: US Tsy $82B 13W, $73B 26W bill auctions (1130ET)

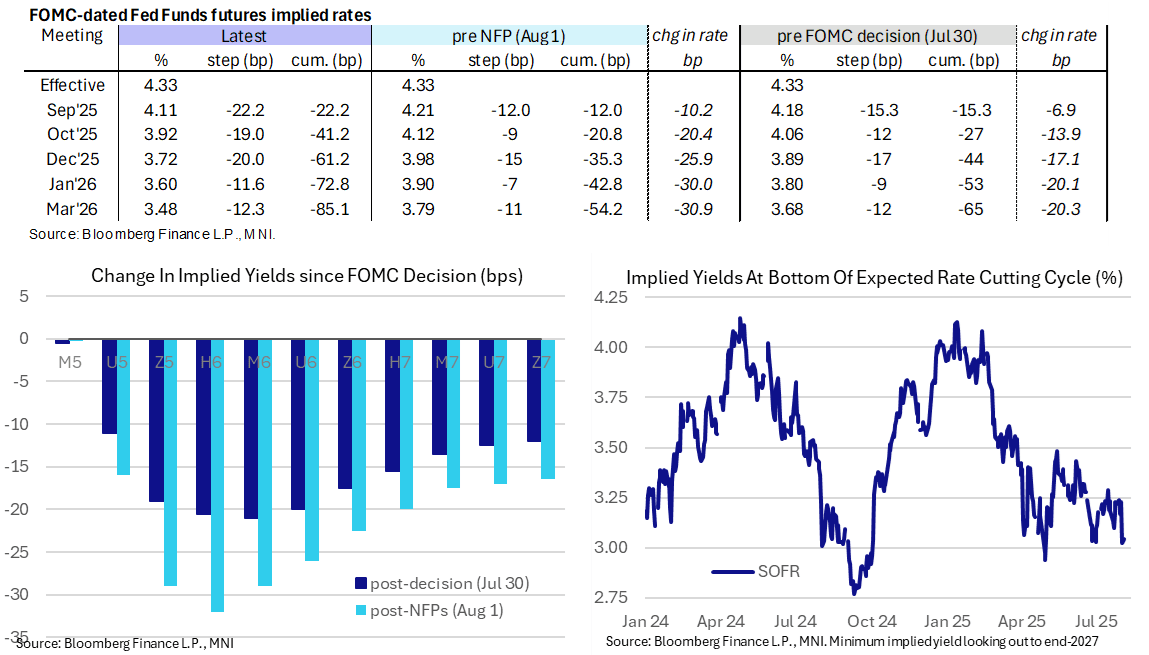

STIR: Bulk Of NFP Dovish Lurch Held, New Fed Governor In Coming Days

- Fed Funds implied rates have pared some of late Friday/early overnight dovish extremes but still hold the vast majority of the slide on Friday’s soft payrolls report.

- Cumulative cuts from 4.33% effective: 22bp Sep, 41bp Oct, 61.5bp Dec, 73bp Jan and 85bp Mar.

- The SOFR implied terminal yield of 3.045% (SFRH7) is 2bp higher on the day for still 20bp lower since payrolls.

- The 61bp of cuts to year-end compares with a median 50bp from June’s SEP. Considering the unemployment rate of 4.25% in July vs the 4.5% seen averaging in 4Q25 in those same projections, it shouldn’t be surprisingly that Friday’s first reaction to the payrolls report was measured:

- Hammack (’26 voter, hawk) said the US labor market still appears healthy, though fresh jobs numbers released Friday constituted a “disappointing report to be sure.”

- Bostic (non-voter) hasn’t changed his view that there should be just one rate cut this year.

- Fed Governor Kugler (permanent voter) resigned late on Friday, vacating her board of governors seat due to expire in January. “I am proud to have tackled this role with integrity, a strong commitment to serving the public, and with a data-driven approach strongly based on my expertise in labor markets and inflation.” It’s a surprise although she had missed last week’s FOMC meeting.

- Trump has said he’ll appoint a new Fed governor in the coming days, along with a new BLS commissioner after Friday’s extraordinary decision to fire McEntarfer after a weak report. See more on the latter from the MNI Policy Team at MNI INTERVIEW: Ex-Chief Says BLS Can Withstand Trump Pressure (Aug 1).

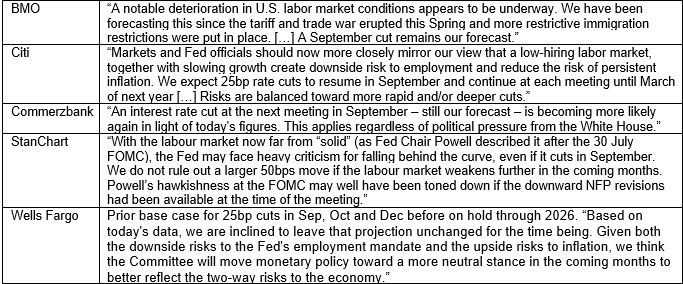

US OUTLOOK/OPINION: Analysts On Balance Less Convinced On Sept Cut [1/2]

- There has been a slight paring in expectations of cut at the next FOMC meeting on Sept 16-17 although there is still 21bp of easing priced vs 12bp before Friday's payrolls report.

- Analysts are less convinced at this stage, at least on balance. The five in the table below continue to expect a September cut (and we assume Goldman Sachs do as well but there wasn't reference in their data note) vs nine at least officially still looking for a later starting point for a resumption of cuts.

Analysts Calling For 25bp Cut In September – No View Changes But Standard Chartered Discuss 50bp

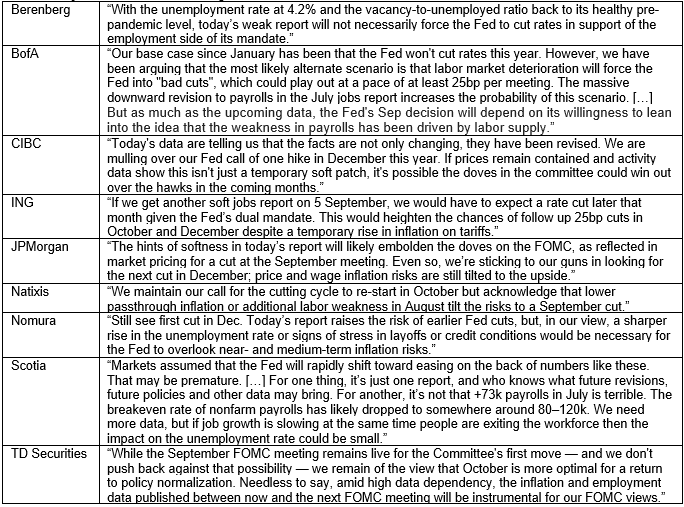

US OUTLOOK/OPINION: Analysts Less Convinced On Sept Cut Than Market [2/2]

Other Analyst Calls – Some Starting To Question More Hawkish Views

SOFR: Mix Of Net Long Setting & Short Cover Seen Friday

OI data points to net short cover dominating in the white pack on the SOFR futures strip on Friday, before net long setting came to the fore further out the strip.

- Futures rallied on a combination of the soft economic data, President Trump's choice to make changes at the BLS and the resignation of Fed's Kugler.

| 01-Aug-25 | 31-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,234,142 | 1,253,764 | -19,622 | Whites | -10,537 |

SFRU5 | 1,304,217 | 1,319,881 | -15,664 | Reds | +2,934 |

SFRZ5 | 1,356,716 | 1,316,869 | +39,847 | Greens | +43,794 |

SFRH6 | 1,068,748 | 1,083,846 | -15,098 | Blues | +20,446 |

SFRM6 | 887,941 | 886,557 | +1,384 |

|

|

SFRU6 | 845,706 | 847,985 | -2,279 |

|

|

SFRZ6 | 931,604 | 924,990 | +6,614 |

|

|

SFRH7 | 720,393 | 723,178 | -2,785 |

|

|

SFRM7 | 711,550 | 710,800 | +750 |

|

|

SFRU7 | 565,561 | 532,978 | +32,583 |

|

|

SFRZ7 | 485,714 | 476,762 | +8,952 |

|

|

SFRH8 | 331,553 | 330,044 | +1,509 |

|

|

SFRM8 | 260,560 | 250,177 | +10,383 |

|

|

SFRU8 | 205,641 | 201,107 | +4,534 |

|

|

SFRZ8 | 208,248 | 206,749 | +1,499 |

|

|

SFRH9 | 149,121 | 145,091 | +4,030 |

|

|

US TSY FUTURES: Net Long Setting Dominated On Friday

OI data points to net long setting dominating on Friday, as the soft economic data, President Trump's choice to make changes at the BLS and the resignation of Fed's Kugler factored into the rally in Tsys.

- Over $7mln of net DV01 equivalent was added across the curve, with the only interruption to the wider theme coming via modest net short cover in US futures.

| 01-Aug-25 | 31-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,544,796 | 4,534,737 | +10,059 | +370,945 |

FV | 6,982,337 | 6,957,890 | +24,447 | +1,047,782 |

TY | 4,975,435 | 4,930,762 | +44,673 | +2,956,817 |

UXY | 2,448,676 | 2,425,449 | +23,227 | +2,038,570 |

US | 1,737,964 | 1,739,990 | -2,026 | -283,762 |

WN | 1,955,341 | 1,948,621 | +6,720 | +1,224,258 |

|

| Total | +107,100 | +7,354,610 |

US-RUSSIA: Kremlin Downplays US Nuclear Sub Deployment; Putin May Meet Witkoff

Reuters reports comments from Kremlin spox Dmitry Peskov. Says that Russia "has no desire to get into a polemic with [US President Donald] Trump over nuclear submarines", adding "Its obvious that US submarines are already on combat duty anyway." This comes after Trump told media over the weekend that he had instructed the US Navy to move two nuclear submarines "in the appropriate region" [i.e.closer to Russia] following inflammatory comments from former president and current Deputy Chair of the National Security Council Dmitry Medvedev.

- In a social media spat that escalated after Trump referred to Russia's "dying economy", Medvedev wrote "Let [Trump] remember his favorite movies about ‘The Walking Dead,’ as well as how dangerous the non-existent in nature ‘Dead Hand’ can be". The phrase 'dead hand' was viewed as a thinly-veiled reference to the Soviet-era 'dead hand' nuclear strategy, in which nuclear weapons could supposedly still be launched even if the personnel in control were killed in a first strike.

- Peskov says "Everyone should be very, very careful with nuclear rhetoric". Claims that "We're not talking about any kind of nuclear escalation." Does not say anything on if Medvedev has been told to tone down his statements, says it is the president's position that matters.

- Regarding Trump's 8 August deadline for Russia moving to end the war in Ukraine, Peskov says that President Vladimir Putin may meet with Trump's Middle East envoy Steve Witkoff this week, claiming these meetings and US mediation in general are "always useful and important".

ISRAEL: US/Israel Eye Compr. Gaza Deal, Backed By Threat Of New IDF Offensive

Israel and the US appear to be pivoting strategy away from an incremental Gaza ceasefire to a comprehensive deal, after the latest round of mediated talks with Hamas stalled. The FT reports that Israel is “threatening to expand its military offensive into additional areas of Gaza in a bid to increase pressure on Hamas...” The piece chimes with an Al Monitor report, highlighted by MNI on 29 July: See: Israeli Officials To Present New Gaza Strategy To US Counterparts

- NYT reports PM Benjamin Netanyahu and President Donald Trump are "working on a deal that would present Hamas with an ultimatum: release the remaining hostages and agree [to disarm], or Israel’s military campaign would continue."

- Trump’s Middle East envoy, Steve Witkoff, said Trump wants to “shift” Gaza policy, while an Israeli official said: “There will be no more partial deals,” per Semafor.

- Witkoff said Saturday: "Hamas has said it is prepared to demilitarize... multiple Arab governments are now demanding that Hamas demilitarizes. So we are very very close to a solution..." According to Axios, Hamas responded by stressing “it will not disarm before the establishment of an independent Palestinian state with Jerusalem as its capital.”

- A renewed Israeli offensive in Gaza is likely to invite more international pressure on the Netanyahu govt. CNN reports that a new letter to recognise a Palestinian state is gaining signatures in the US House of Representatives, following pledges from France, the UK, Canada, and Portugal to conditionally recognise a Palestinian state in September.

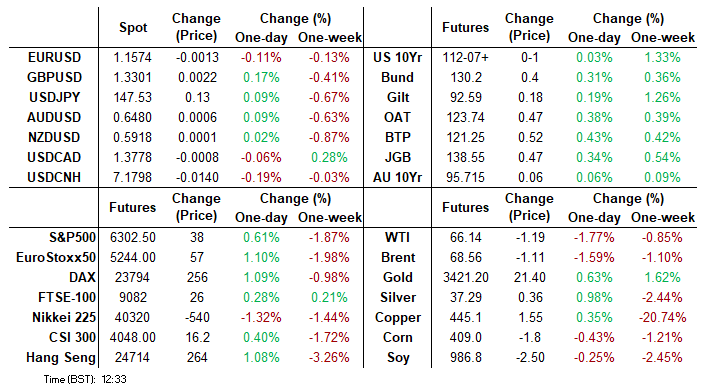

FOREX: USD Moderates, Aiding Relief Recovery for GBP/USD

- The USD is moderating early Monday, prompting the ICE USD Index to head into NY hours holding the bulk of the Friday pullback - but stopping short of any further weakness. The reaction seen since Friday's poor payrolls print (as well as Trump's subsequent firing of the head of the BLS) has held - keeping markets well priced for a more activist Fed later in 2025.

- Greenback consolidation has aided a bounce for GBP, keeping GBP/USD either side of the 1.33 handle and within range of 1.3345, the 100-dma. Despite this, the bearish theme in GBPUSD remains intact for now. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. These levels could be of greater consequence later this week on the BoE rate decision. The MPC are uniformly expected to cut rates by 25bps, however the vote split among the board will be carefully watched.

- The short-term bullish corrective phase in USDCAD remains in play despite sharp weakness Friday. On the recent run higher, price traded through the 50-day EMA at 1.3739 and this has been followed by a break of resistance at 1.3798, the Jun 23 high. A bullish trend condition in EURJPY remains intact and for now the recent move down is considered corrective. Key support to watch lies at the 50-day EMA at 169.17. A clear break of the EMA is required to highlight a stronger short-term bearish threat.

- Factory orders and durable goods orders are the scheduled highlights Monday. There are no scheduled Fed appearances today, however any comments or speculation will come under close scrutiny given Kugler's resignation over the weekend.

OPTIONS: Expiries for Aug04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1445-50(E1.1bln), $1.1500-10(E1.9bln), $1.1550-65(E3.0bln), $1.1585-00(E1.8bln), $1.1600(E1.1bln)

- USD/JPY: Y148.65-80($549mln), Y149.50($753mln), Y150.00($1.2bln), Y150.50($967mln)EUR/JPY: Y173.00(E570mln)

- AUD/USD: $0.6445-65(A$1.4bln)

- NZD/USD: $0.6030-50(N$590mln)

- USD/CAD: C$1.3778-90($783mln)

EQUITIES: ESA Clears First Notable Support Post-NFP

- E-mini S&P sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. This puts price well clear of support at the 20-day EMA, at 6336.64, signaling scope for a deeper retracement toward the 50-day EMA.

- The trend condition in Eurostoxx 50 futures faltered Friday, with short-term weakness resulting in a break of the bear trigger. Having shown below 5194.00, the Jun 23 low, the April 30 hi/lo range at 5078-5138 becomes the area of downside interest.

COMMODITIES: WTI Futures Pressured into Friday Close

- WTI futures slipped into the Friday close, erasing the gains posted earlier in the week. Support to watch is the 50-day EMA, at $65.37. The average has been pierced, a clear break of it would expose $58.17, the May 30 low.

- Gold benefited from the soft NFP print on Friday, returning prices toward the top-end of the recent range. This supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact.

| Date | GMT/Local | Impact | Country | Event |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/08/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 05/08/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/08/2025 | 0645/0845 | * | Industrial Production | |

| 05/08/2025 | 0700/0900 | ** | Industrial Production | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 05/08/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/08/2025 | 0900/1100 | ** | PPI | |

| 05/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 05/08/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/08/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/08/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 05/08/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result |