MNI US MARKETS ANALYSIS - Awaiting Trump Decision on Iran

Highlights:

- Markets await Trump decision on US involvement in Iran, Khamenei states Iran is not one to surrender

- Treasuries see support on prospect of prolonged instability

- Weekly jobless claims due a day early, ahead of FOMC decision & Powell presser

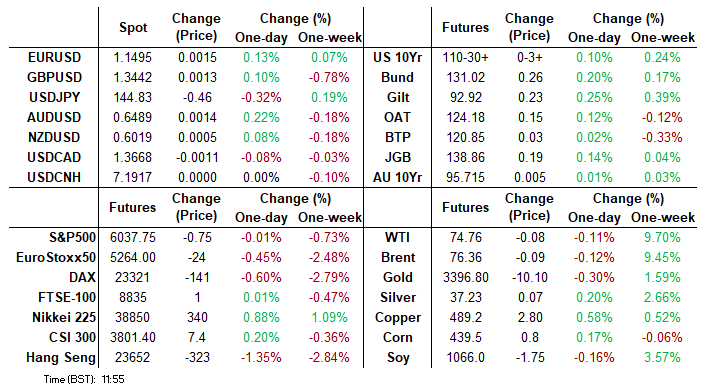

US TSYS: Session Highs With Iran Headlines, Modest Moves With FOMC Later

- Treasuries have slowly extended session highs with Iran’s Khamenei saying it will not accept an imposed peace or war and that Iranians do not answer well to language of threat, per Reuters reporting.

- Gains from yesterday’s close are limited having more than reversed earlier losses -- cash yields are only 1.5-2bp lower.

- TYU5 is at session highs of 110-30+ (+03+) on modest cumulative volumes of 270k.

- It remains below yesterday’s fleeting spike to 111-00 and doesn’t trouble resistance at 111-13 (Jun 13 high) or 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg).

- Data: MBA mortgage data (0700ET), Jobless claims (0830ET), Housing starts/building permits May (0830ET), TIC flows Apr (1600ET)

- Fed: FOMC decision and SEP (1400ET), Powell press conference (1430ET)

- Bill issuance: US Tsy $65B 4W & $55B 8W bill auctions (1130ET), US Tsy $60B 17W bill auction (1300ET)

- For other geopol matters, Trump The President has lunch with the Chief of Army Staff of the Islamic Republic of Pakistan at 1300ET.

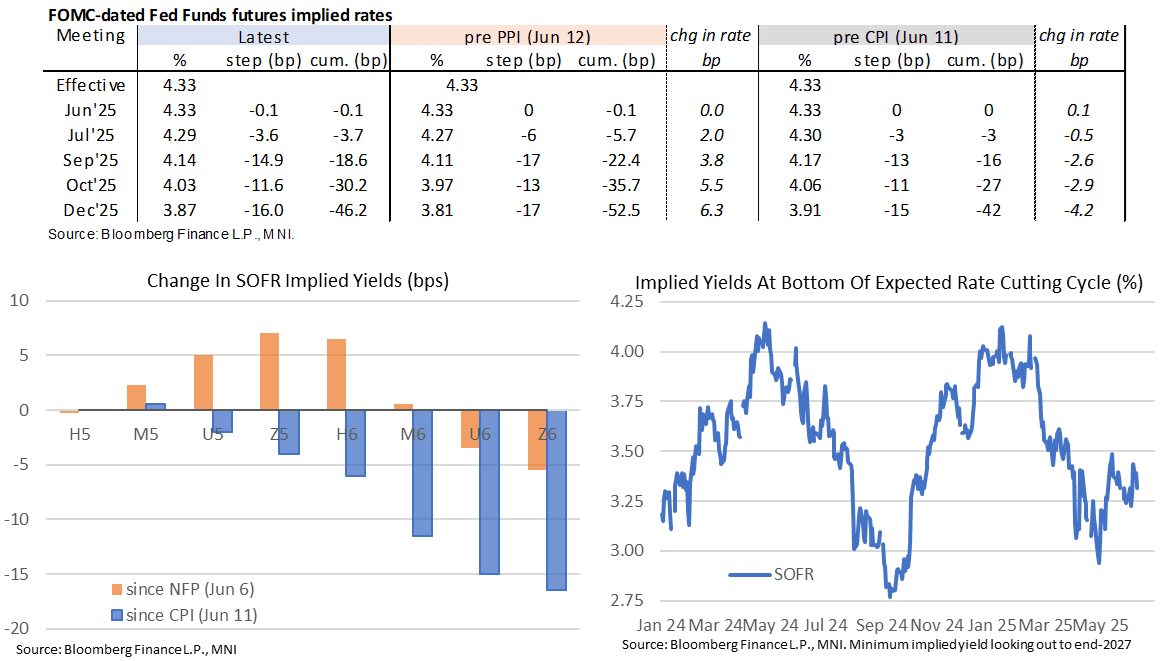

STIR: Fed Not Seen Cutting Until October Ahead Of Today’s FOMC w/ Dot Plot

- Fed Funds implied rates are 2bp lower than yesterday’s most hawkish levels for the Dec’25 FOMC meeting although still only have a next cut priced for October.

- Cumulative cuts from 4.33% effective: 0bp for today, 3.5bp Jul, 18.5bp Sep, 30bp Oct and 46bp Dec.

- The SOFR implied terminal yield of 3.265% (SFRZ6) is 1.5bp lower on the day, consolidating yesterday’s twist flattening on intensification in geopolitical tensions.

- Today’s docket is of course headlined by the FOMC decision. MNI Preview here.

- Special mention does however go to weekly jobless at 0830ET, brought a day forward owing to tomorrow’s Juneteenth holiday. Initial claims cover a payrolls reference period whilst continuing claims will be watched after their notable push higher in the latest two weeks.

CENTRAL BANK PREVIEWS

MNI FED PREVIEW - JUNE 2025: Holding in Anticipation

The FOMC will hold rates for a 4th consecutive meeting in June, and continue to convey a patient stance on future rate cut decisions amid elevated policy-related uncertainty. The new quarterly projections will still signal the resumption of rate cuts later this year, but likely only one 25bp reduction instead of the two cuts envisaged at the March meeting. While risks to both the Fed’s inflation and employment mandates remain elevated, with the new 2025 forecasts looking increasingly reflective of stagflation, the Committee should still signal rate cuts through end-2026 of a similar magnitude to its previous set of projections.

MNI BOE PREVIEW - JUNE 2025: All About the Vote and Minutes

The June MPC meeting will be a surprise to markets if the outcome is anything other than an on hold decision with unchanged official guidance. Expectations are relatively strongly pointing towards a 7-2 vote split with both Dhingra and Taylor likely to follow up their votes for a 50bp cut in May with a vote for a sequential cut (the magnitude of which is unlikely to elicit a market reaction). The main focus is on whether the dataflow has been enough to convince any other members of the MPC to vote for sequential cuts.

MNI SNB PREVIEW - JUNE 2025: Rates to Follow CPI?

Markets see a 25bp policy rate cut to 0.00% as most likely but do acknowledge the risks of an outsized cut into negative territory, with OIS-implied odds standing around 80:20 for a 25bps move vs a 50bps step. Inflation has slowed further since the March meeting and turned negative, moving below the SNB’s target range for the first time in 4 years. However, the SNB targets medium-term CPI trends, rather than short-term, which will be the focus in the update to inflation forecasts.

MNI NORGES BANK PREVIEW - JUNE 2025: Gearing Up for the H2 Cut

Norges Bank is firmly expected to hold rates at 4.50% on Thursday, at a quarterly meeting which includes an updated MPR and rate path projection. We expect guidance that the policy rate “will most likely be reduced in the course of 2025” will remain unchanged, with a risk of firmer guidance towards a September cut. Developments since the March meeting should warrant a modest downward revision to the rate path, but we still expect the June iteration to be consistent with two cuts this year.

MNI BCB PREVIEW - JUNE 2025: Hike or Hold, Caution to Remain

A narrow majority of analysts lean towards the BCB keeping the Selic rate steady in June at 14.75%. This follows lower-than-anticipated inflation figures last week, better behaved inflation expectations and the strong performance for the Brazilian real across 2025. However, with economic activity appearing resilient and the labour market still tight, the Copom may opt to hike rates by a further 25bp, as the committee continues to stubbornly pursue the convergence of inflation to target.

MNI CBRT PREVIEW - JUNE 2025: Room to Hold Until July

The CBRT is expected to keep its one-week repo rate unchanged at 46.00% this month following a 350bp hike in April, but risks of a rate cut are noted by some analysts given the recent slowdown in monthly inflation. However, upside price pressure stemming from FX weakness post the arrest of the Istanbul mayor Ekram Imamoglu in March ultimately warrants further caution, while increased funding through the key policy window has already led to a reduction in the weighted-average funding rate.

US TSY FUTURES: Long Setting Dominated On Tuesday

OI data points to a mix of net long setting (TU, FV, UXY & US) and short cover (TY & WN) as Tsy futures finished higher on Tuesday, aided by SLR reform speculation in the NY afternoon.

- Net long setting dominated in curve-wide terms.

| 17-Jun-25 | 16-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,029,264 | 3,975,590 | +53,674 | +2,097,210 |

FV | 6,945,667 | 6,897,181 | +48,486 | +2,112,007 |

TY | 4,818,136 | 4,828,930 | -10,794 | -716,177 |

UXY | 2,367,382 | 2,346,803 | +20,579 | +1,801,301 |

US | 1,736,373 | 1,727,928 | +8,445 | +1,169,595 |

WN | 1,887,640 | 1,893,164 | -5,524 | -1,013,962 |

|

| Total | +114,866 | +5,449,975 |

IRAN: Khamenei Stresses No Surrender, Distaste For U.S. Threats

RTRS carrying headlines covering further comments from Iranian Supreme Leader Khamenei:

- “They should know that Iran will not surrender and any U.S. strike will have serious irreparable consequences”.

- “Those who know Iran's history know that Iranians do not answer well to language of threat”.

- “Iran will not accept an imposed peace or war”.

RIKSBANK: Long-end Rate Path Revision More Dovish In Context Of Other F'casts

SEK weakness has extended since this morning’s Riksbank decision, where rates were cut to 2.00% as expected but the signals in the policy statement and June MPR rate path leant dovish. In the press conference, Governor Thedeen tried to play down the dovish signal from the front-end of the June rate path (which assigns a ~50% probability of another cut this year). However, markets may be paying some attention to the downward rate path revision in 2026-2028. The “terminal” point of the rate path in Q1 2028 was 2.01%, well below the 2.25% level that had anchored long-end projections since the September 2024 decision (when the Riksbank’s revised 1-3% nominal neutral estimate was announced).

- A reminder that the first three quarters of the rate path represent the Executive Board's best assessment of policy rates, while further out the path is an output of staff's macroeconomic models.

- This long-end revision is particularly notable in the context of the June MPR's updated macroeconomic projections. The medium-term forecasts for unemployment, the GDP gap and CPIF ex-energy are all relatively unchanged compared to March. Meanwhile, the long-term KIX effective exchange rate forecast is actually higher than before (which indicates a weaker exchange rate and all else equal would be a hawkish rate path input).

- Overall, the June projections suggest the Riksbank staff’s macroeconomic framework is structurally more dovish compared to March, with uncertainty-related weakness in the next year or two needing to be compensated with lower rates through the projection horizon. The June meeting minutes (released June 25) will provide insight on whether such an outlook is echoed by Executive Board members.

- EURSEK is now up 0.5% on the session, through the May 27 high of 10.9937 and narrowing the gap to the next resistance at 11.0850 (April 28 high).

- The decision has reinforced bullish technical conditions in NOKSEK, with the cross up 0.3% today and approaching clustered resistance around 0.9646 (March 21 high) and 0.9651(trendline drawn from the March 2022 high).

FOREX: Vols See Support on Fed Meeting, Fraught Geopolitical Risk

- Front-end FX vols are seeing support this morning: EUR/USD overnight implied neared 20 points at one point as markets looked ahead to the Fed decision as well as continued instability in the Middle-east, as the scope for escalation grows and could include controlled energy flow through the Strait of Hormuz or possible US involvement to ensure the "unconditional surrender" of the Tehran regime.

- GBP saw some early support on the back of a 0.1ppt higher-than-expected UK CPI Y/Y print, helping GBP/USD add ~30 pips to overnight gains. EUR/GBP came under similar pressure, putting the cross back to the overnight lows of 0.8547. Gains were shallow, however, as services CPI came in slightly soft, leaving inflation broadly infitting with the BoE's forecasts at this stage. Markets continue to price just under 50bps of BoE easing by year-end.

- EUR/SEK rallied on the back of the Riksbank's 25bps rate cut. While the move was largely as expected, the bank made it clear that further easing could be forthcoming, with another cut this year likely. EUR/SEK was marked above 11.00 for the first time since early May, clearing the 11.0124 100-dma in the process.

- AUD is furtively outperforming early Wednesday, keeping AUD/USD inside the uptrend channel drawn off the late April lows. AUD is recouping some of this week's lost ground as enhanced geopolitical uncertainty countered any tailwind from better commodities prices. Australian jobs data is the next focal point, due Thursday.

- Weekly jobless claims data are due today, brought forward by one day thanks to Thursday's Juneteenth market holiday. The Fed decision follows, and while no change in headline policy is expected, the press conference will remain of interest as the Fed Chair comes under pressure from the White House for being "too slow" on easing monetary policy.

OPTIONS: Expiries for Jun18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.2bln), $1.1600-04(E1.0bln), $1.1645-50(E1.2bln)

- USD/JPY: Y144.00($725mln)

- NZD/USD: $0.5760(N$1.2bln)

- USD/CAD: C$1.3600($1.4bln)

- USD/CNY: Cny7.3000($858mln)

EQUITIES: Eurostoxx 50 Futures Close to Recent Lows, Remain Below 50-Day EMA

- Eurostoxx 50 futures are trading closer to their recent lows. The latest pullback has resulted in a breach of the 50-day EMA at 5298.64. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would signal a short-term top and highlight scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5355.88, the 20-day EMA.

- The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. For now, the most recent pullback is considered corrective. The contract has pierced support at 6003.83, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5896.83. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

COMMODITIES: Continuation Higher for WTI Futures Would Expose $80 Handle

- WTI futures traded sharply higher last week and last Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $68.49, the Jun 13 low. A breach of this level would signal scope for a deeper retracement.

- A bullish theme in Gold remains intact and recent gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3271.7, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP | |

| 19/06/2025 | - | NorgesBank Meeting | ||

| 19/06/2025 | - | Swiss National Bank Meeting | ||

| 19/06/2025 | 0130/1130 | *** | Labor Force Survey | |

| 19/06/2025 | 0730/0930 | *** | SNB PolicyRate | |

| 19/06/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 19/06/2025 | 0730/0930 | ECB's Lagarde On Economic and Financial Integration | ||

| 19/06/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 19/06/2025 | 0900/1100 | ** | Construction Production | |

| 19/06/2025 | 0945/1145 | ECB de Guindos On Eurozone Economic Outlook | ||

| 19/06/2025 | 1030/1230 | ECB Lagarde Keynote Speech At Economic Integration Conference | ||

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | - | ECB Cipollone At Eurogroup Meeting | ||

| 19/06/2025 | 1600/1800 | ECB Lagarde At Financi'Elles event |